Spekulatius

-

Posts

19,032 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

This low tech attack works because Russia does not even have a rudimentary air defense system in place to defend their bases. Something like this: https://www.rheinmetall.com/en/products/air-defence/air-defence-systems/drone-defence-toolbox

-

The new Taurus cruise missile with upgraded engine could reach Moscow from the Ukraine. Would be fun to put some on the Kremlin's roof every once in a while. It would serve Putin well to spent his days in bunkers. Also, Ukraine has terminated several high profile Russian generals in Russia close to Putin with their commando groups. They are getting better at this and if Putin shows up at the wrong place at the wrong time, he could be exterminated too. This may have r may not end the war, but is worth a shot as any sniper would say.

-

The West Bank is troubled but could still work out in terms of it becoming a peaceful territory next to Israel. Israel should do everything it can to prevent the West bank to become another Gaza but it also depends on what the current administration and population does or if Hamas can also gain a stronger foothold there. Do you have an answer to your own question. Was there critical fork in the road where Israel took the wrong and lo the subsequent carnage could have been prevented in hindsight (potentially)?

-

40 aircraft destroyed in a single day . Drones were started from within Russia. Nice special operations. these trains are needed by Russia to launch the glide bombs that Ukraine has much difficulty with: https://apnews.com/article/russia-ukraine-war-sumy-region-18966d4b286ffb6f4e764b94a6afaf61

-

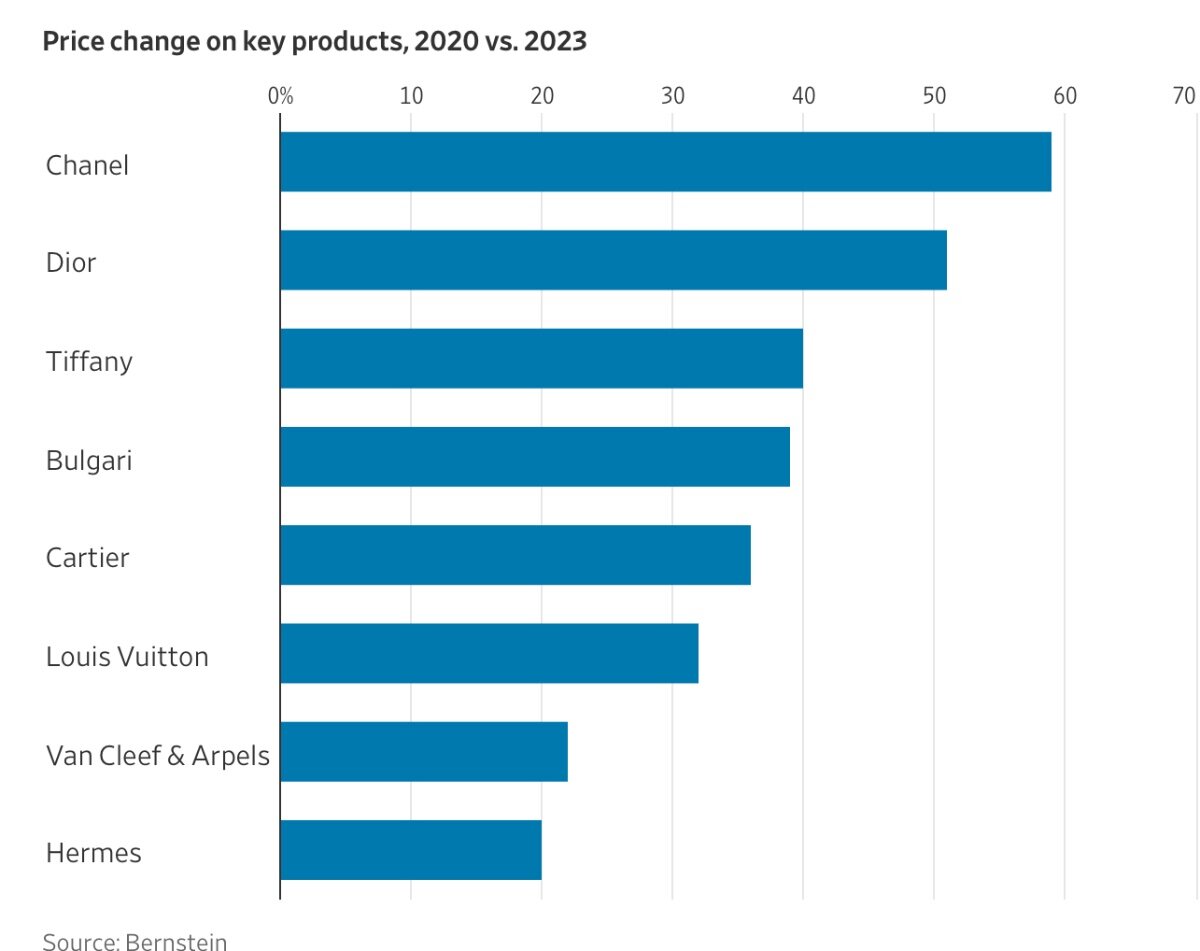

I guess you can raise your prices too much after all: https://www.wsj.com/business/retail/designer-price-hikes-lvmh-chanel-58b8a941?mod=hp_lead_pos6 This chart is really interesting. It seems like the worst performers are those that raised their prices the most. I guess the best pricing power is the latent one that remains unused:

-

Jamie as a banker is incentivized to be extremely cautious. He also knows he got this administrations ear. As far as cracks or not, it really depends not just on cold hard data, but also the implicit trust the bond market is having in the administration. I think Liz Mini Budget disaster in the UK is an example where the objective data wasn’t that bad and not the budget nit even that outrageously but the Mr Bonds collectively held a vote and voted “no confidence” and that’s was that. Those who think it can’t happen don’t take into account the reflexive nature of markets, imo.

-

Or there is plenty of inventory above and below the ground. Also, cost of production where? There is a cost curve and for most of the production , the market price is still above the cost of production. Cost of production is always a curve, not a fixed value. It’s not quite that simple.

-

Crack in the bond market: https://www.wsj.com/finance/jpmorgans-jamie-dimon-predicts-crack-in-the-bond-market-citing-u-s-fiscal-mess-9d90cb3f?mod=trending_now_news_3 https://archive.ph/THArZ

-

Awesome trades. I agree on Elon, my wife mentioned to me that he looks like the drug addicts that get submitted to clinic for dialysis. His skin tone looks bad too. If he or somebody in his circle doesn’t intervene, he may not make it until 60 without spare parts. I think Trump is a gift to traders. For LTB&H not so much. Tariffs will go back and forth but I think the ending game is going to be tariffs, it’s just a question on how much.

-

Elon should take a few weeks off. He really needs it. Maybe he need rehab too. His behavior and appearance is bizarre. But Tesla went too the moon because he says he will go back to work . You can’t beat Elon, even if he looks beaten.

-

If you are lucky, my Whirlpool died in my new 2023 house 2 weeks after I moved in. I recommend LG, they actually produce many of them in Kentucky while Whirlpools low end stuff is made in Mexico. Don’t even bother with Samsung.

-

Well, the roaring twenties led to a boom in Florida real estate too and it crashed before 1929 in 1925: https://www.thebubblebubble.com/florida-property-bubble/#:~:text=Property prices fell under their,holdings to avoid going bankrupt.

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

The Netflix series - Turning point Vietnam war is excellent: https://www.netflix.com/title/81756795 Vietnam war documentaries are a dime in dozen but this one is better than others to explain the political background than others I have seen. -

I have no clue what Israel could have done to prevent Gaza disaster. I think none Israel’s attempts to defuse the situation was rewarded. For example when Israel pulled back their settlers decades ago, Hamas used that vacuum to install rocket artillery. The list goes on. Also, Gaza issue was established prior to 1967 with Britain leaving the area in 1948. I don’t think Israel can solve this on their own. They probably need to work with their Arab neighbors Egypt, Jordan, Saudis (money), UAE (money) and more or less kick the ball in their court. Perhaps these counties should offer citizenship to the Gaza populace willing to relocate. There ought to be a few after all this mayhem. Note that Gaza was controlled by Egypt until 1967 (maybe longer) but the populace there never had Egypt citizenship or could acquire it. That tells you something. Egypt wants nothing to do with Gaza or their population, or so it seems. Thats not to see that Israel is. To making a. Ist sie here bombing Gaza to smithereens. The solution can only be a diplomatic one because everything else ends up with terrorism. I don’t think anyone has ever figured out how to win a war against terrorists. In any case, I think Israel’s relationship with many Arab nations is good enough to negotiate a solution with them. I guess that’s my answer, but it would not have been possible in 1967, I think.

-

Dividend Portfolio for Retirement Income: 6% or higher club

Spekulatius replied to dipod's topic in General Discussion

PAX was yielding 6% when I bought it, currently ~4.6% . Rather than an absolute dividend yield, I would focus dividend and dividend growth potential. I think some. 3-4% yield era with good growth are preferable to some 6% yielders which have not got expected growth potential. Slso, some Japanese cos have been showing impressive dividend growth, due to soft pressure from the Tokyo stock exchange to improve valuations. Many business do this by boosting dividends and buybacks. just one example A&D Holon 7745 currently pays out 40Yen/ year but has announced a boost to 50yen. It’s not a high yield, but their balance sheet is great and they are growing nicely and payout low with over 200yen/share in earnings . They can easily keep raising their dividend by 20% for a couple of years and you end up with a nice yield that way. Thats just one of the many and I only mention it because I own it. -

Looks like there is a real issue: https://finance.yahoo.com/news/exclusive-china-magnet-pinch-threatens-193711597.html

-

Dividend Portfolio for Retirement Income: 6% or higher club

Spekulatius replied to dipod's topic in General Discussion

While true, they have not been successful with any alt product and PM and to a lesser extent BTI could eat their lunch. I think MO is very iffy. -

I forgot who said this but Trump is the wrong answer to the right questions. I think this is very true.

-

I think Trump punishes every country that can’t hit back . It’s quite simple. He really owned Bangladesh and Laos.

-

The German word is Endlösung I suspect.

-

commercial. So tariffs are back on the menu. Thank you for sharing. It’s tough enough to trade on this never mind running a business. The supplier I asked about the 35% +15% admin fee: tariff surcharge for that spare part told me that the part is from China, which explain the 35% . My guess is the 15% are extra

-

Bought at a discount through Exor of course.

-

Yes, actually US NATO spent is probably less than 2% of GDP.

-

I just got a quote today for spare parts at work: 35% tariff surcharge 15% tariff surcharge /admin fee. I asked how they came about these surcharges? This is from an US subsidy of an European company. I don’t think these parts come from Europe though. I suspect at least the 15% tariff surcharge/ admin fee is pure profit.

-

Sorry my post went in the wrong thread - deleted.