Spekulatius

-

Posts

15,099 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

POLL - Likelihood of Taiwan Invasion by China before 2030

Spekulatius replied to Luke's topic in General Discussion

Worth checking out if interested in the topic: https://www.bloomberg.com/news/articles/2024-01-15/what-would-a-chinese-invasion-of-taiwan-do-to-the-global-economy?srnd=oddlots -

POLL - Likelihood of Taiwan Invasion by China before 2030

Spekulatius replied to Luke's topic in General Discussion

On the topic of a Taiwan invasion , I voted 2030-2040. I don’t think Xi is ready to challenge the US and invade Taiwan before that and maybe even not on this timeframe. I do feel like Xi will do something then, perhaps contra to better judgement, because he is driven by ideology and then his time will run out. I think he want to see his picture on walls after the is gone as the great leader of China. -

You are billionaire and spent your time picking fights on Twitter / X. Seems like a very dumb thing to do with your time if you are that rich and independent.

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

I watched the first episode of Night Country as it dropped and it is superb. Great backdrop, storyline and acting. TV at its finest. -

Current valuations a actually should not matter that much over a 30 year period, it all about growth and longevity. Personally, I think the right answer over such a period is to buy and index or something that is likely to renew itself over time. The reason why I think renewal is critical is because the future over such a long period like 30 years is unknowable. my concern with some time like Berkshire is that the leadership as we know it will be gone (even Abel is not going to hang around that long) and they also have the coffee can approach which could end up burdening Berkshire with a lot of deadwood, unless they start to dump some business or spin them off over time. So my choice would be QQQ, or SPY or perhaps something like Investor AB or Exor which is designed as a Holdco and probably will refresh their holdings over time. I think some structural advantaged business like Railroads could work too, because I don’t think they will be disrupted in the next 30 years. I think the nifty fifty have

-

They better be careful with $KW. I don't know about the loans, but the stock does not look good.

-

On to the next calamity. My wife told me flu season is pretty bad. Nurses have to wear masks again.

-

"Violatility" - I like this expression.

-

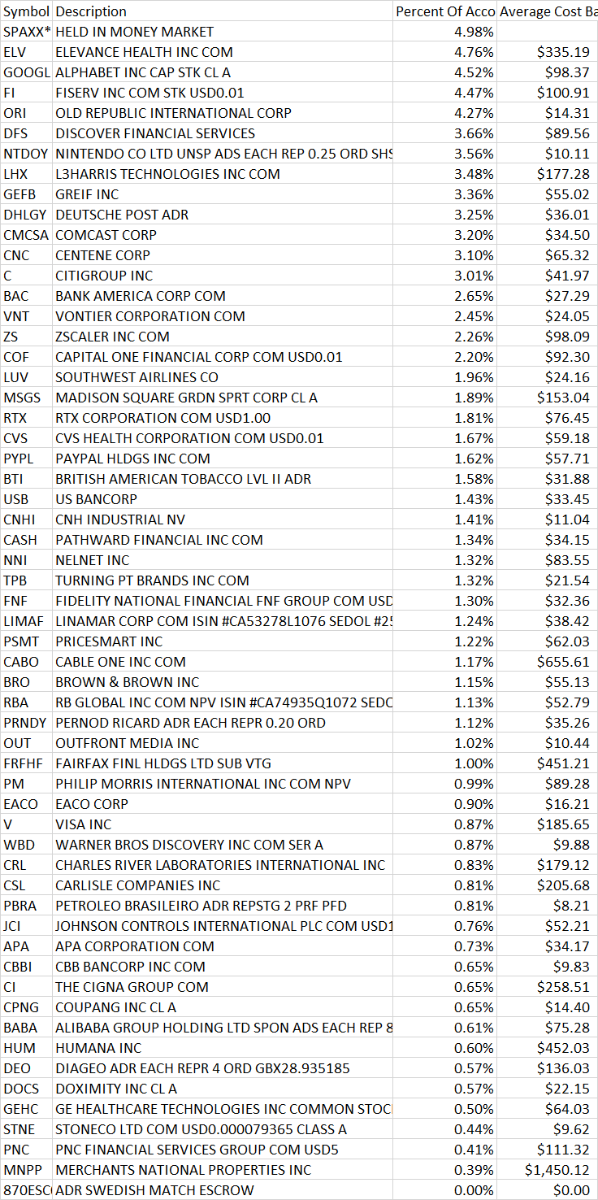

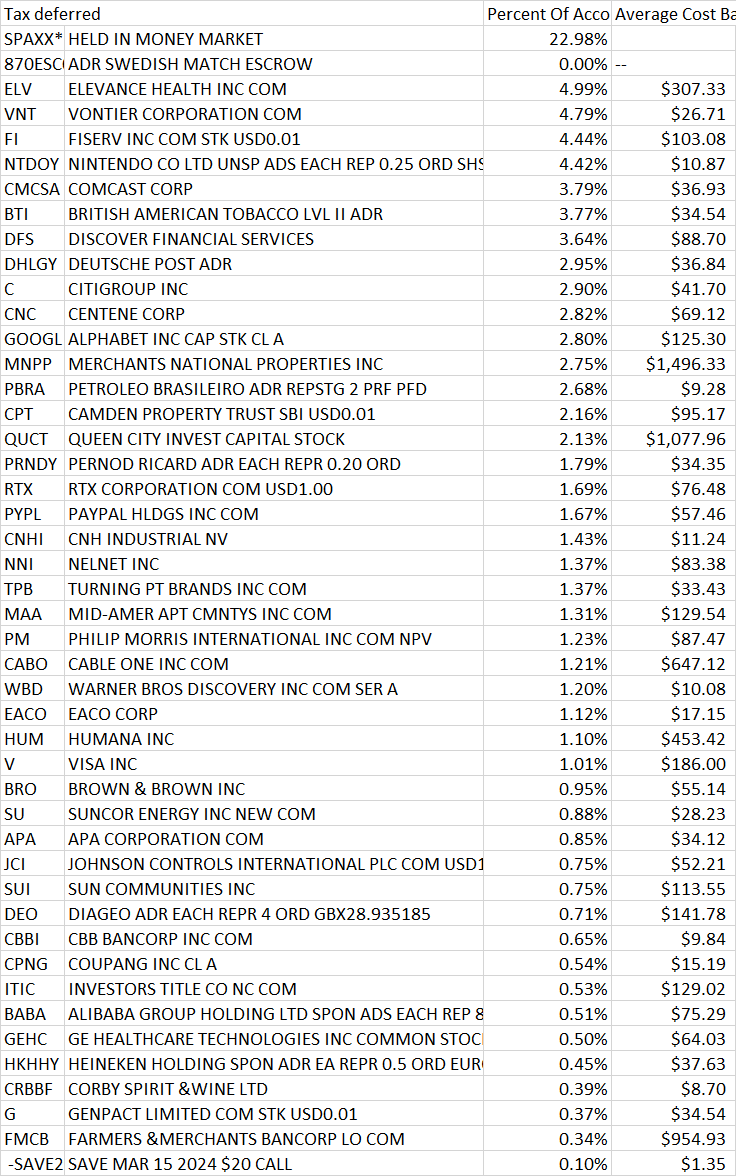

EACO was one I found about 10 years ago. Somehow tried to buy it around $2.5 or so and somehow only got an odd lot of 30 shares when the stock moved on no news. I totally forgot about it, but kept the shares. Two years ago, I noticed a price movement in my brokerage account. I checked on the stock 10-K filing again on their IR site and couldn't believe how much it has grown over the last 10 years. The stock traded at a PE of 6 or thereabouts trading around $16 and change. I also noticed a few trades going off on a relatively tight bid ask. Put some bids in several accounts and got a few hundred shares. I looked later the same day, if I could buy more but the offer was gone. Got another 100 shares a few month later for $19 somehow. I guess you have to get them when you can. EACO owns a sub that does creates part kits for Aerospace - it's basically a value added Distributor. The owner controls almost all the shares - I have no idea why it's still public- the float is minimal. FWIW this years earning are $4.34/ share - the last stale quote is $34.

-

What are you listening to ? (Music thread)

Spekulatius replied to Spekulatius's topic in General Discussion

Nice one to fade the Friday: -

@dealraker - thanks for sharing. The by far most consequential decision was to do nothing.

-

Right- the treasury is the boss, the Fed just manages their checking account.

-

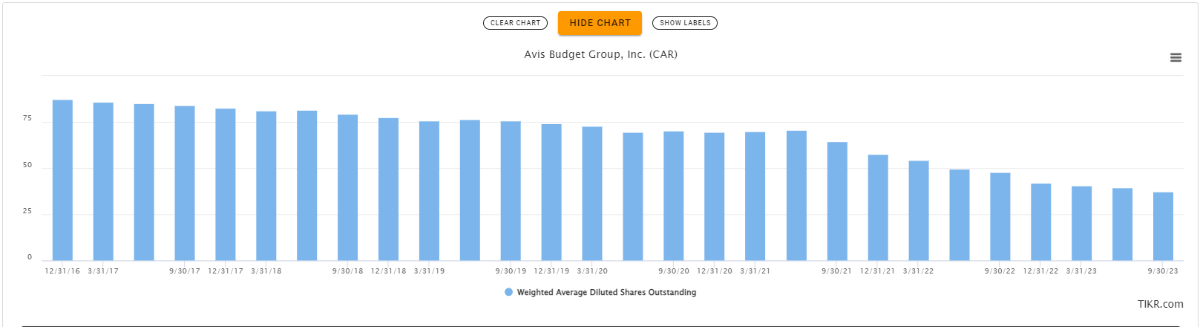

I am more interested in CAR than in HTZ - just based on how they seem to think based on CC transcripts but they both could be great bets. What is fascinating about CAR is their bonkers capital returns. They almost retired 2/3 of their shares and even so the shares have more than tripled, the market cap is actually not up that much. Bonkers, since the business is so much more profitable than in 2016. Even paid a $10 special dividend this year. The capital structure is also something to behold. $6B in market cap and they slapped $4.64B in corporate debt on it. The next layer is secured debt for the cars themselves - ~$17.5B. So it's leverage and top of leverage and just beautiful as long as it works and a zero if they run into trouble like like HTZ did in 2020. I think Europcar also went teats up and needed to be recapitalized. So you really need a management team that knows what they are doing. We should probably open a thread on those rental car co, as there sure is more input.

-

Bought more $HUM on the UNH induced scare this morning.

-

Great depressions help to get stuff done. See Hoover dam and Golden Gate bridge.

-

There are no options much less leaps with nanocaps. The exception may be a mid cap that becomes a nanocap because it is on the verge of bankruptcy but in this case, the stock is already trading like an option.

-

Got to spin the wheels a bit on $CAR. Those buybacks do get my attention: Went from ~90M shares in 2016 to 37M shares. Absolutely fascinating. Looks like a turbocharged version of $AZO.

-

@Dave86ch I am curious about your bucket. What have PBR, $COIN and #Ethereum to do with each other? Some with BIDU, DIS and #Bitcoin.

-

I don't think car rental is a melting ice cube. Ride sharing works, but if you need to do a lot of trips , then calling and waiting for Uber can become a hassle. For vacation trips and if you cover multiple locations, Ride shareing does not work either. Negative cash flow for fleet expansion is a good thing, if the ROIC is high. When the business stagnates or shrinks, the investment in new cars can drop and FCF should increase which creates a nice countercyclical aspect to the business.

-

I only research them when I buy and in many cases I let them sit there, until I see something happening (news, or share price movement) and then i take another look and may sell or buy more, depending on my view. I have not looked at ORI accounts this year for example - it just cruises along. (it was used in my tax deferred account as a source of funds down the road, that's why its gone there). I know a fellow in another board who always has 100+ positions, some of them bought 25 years ago.

-

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

Well,why would Disney take this? Rebel Moon is basically a Star Wars close as far as the storyline is concerned. And Zack not being creative with his imagery like @Parsad makes this a B- movie. -

Same here.

-

Probably CSU because the positions (in the legend of the chart) seem to be sorted by size.

-

Same than CPE though. To APA's defense, they did not pay a large premium and both Permian acreages fit well together. APA becomes more US centric in their asset base, which may have been the underlying reason for the merger. Unfortunately, it also dilutes their Suriname play, which I think is underappreciated.