Spekulatius

-

Posts

15,090 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

If you like NG or LNG, then you may want to look at $GTLS. Today was a presentation on SumZero about Chart Industries that looked compelling enough to buy a few shares almost immediately. lots of things to like! But also some risk (see the news from Biden to pot. postpone new LNG export facilities). https://x.com/BDubes82/status/1755312527389729213?s=20

-

SDF - Kali & Salz is a totally different business (salt mines). They are a high cost producer in this commodity space (Belarus and the Canadian potash mines are low cost producers) so I don’t think it’s an attractive business. KWS is family controlled and it’s the 4th largest seed producer in the world and the only publicly traded pure play. It’s a unique business with lots of IP and deep barriers to entry. KWS plows 18-19% of their revenues into R&D . The third largest seed producer is the French Vilmorin and they went private a year or so ago.

-

Also bought just a bit of PARA so I stay interested in the soap opera. Added a few shares of PM premarket (earnings looked alright to me). I bought a starter in KWS.DE (seed company) as well on a weak earnings report. They did keep the annual forecast but we will see.

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

Apple has another winner with “Masters of the air”. Top notch show throughout (cast, production, special effects, storyline). -

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

Watched it for ~45min and had to stop. Simply depressing. -

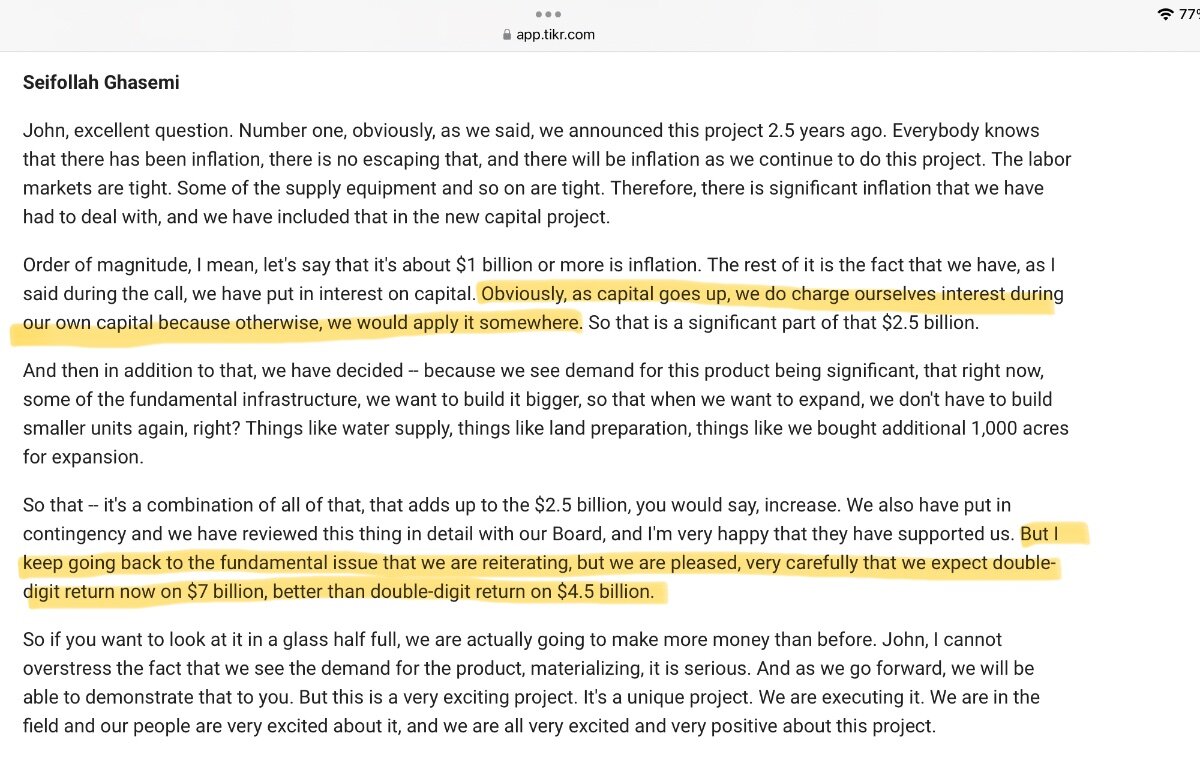

The more I read his CC transcript answers, the less I like Ghasemi , the APD CEO. Her is for example how he defends the cost inflation with their Louisiana project. his answer is basically, we make double digit return and a double digit return on $7B is better than a double digit return on $4.5B Capex. Granted some of the cost increase is just increase in scope, but still, the logic alone gives me shivers. There are other things in the latest conference call that give me second thoughts like the back loaded guidance which assume an extremely sting 2nd half after guiding down Q2 below the prior year. Ai think chances are high they don’t make their earnings target this year. (I sold my few shares pre market today, putting APD back in my watchlist.)

-

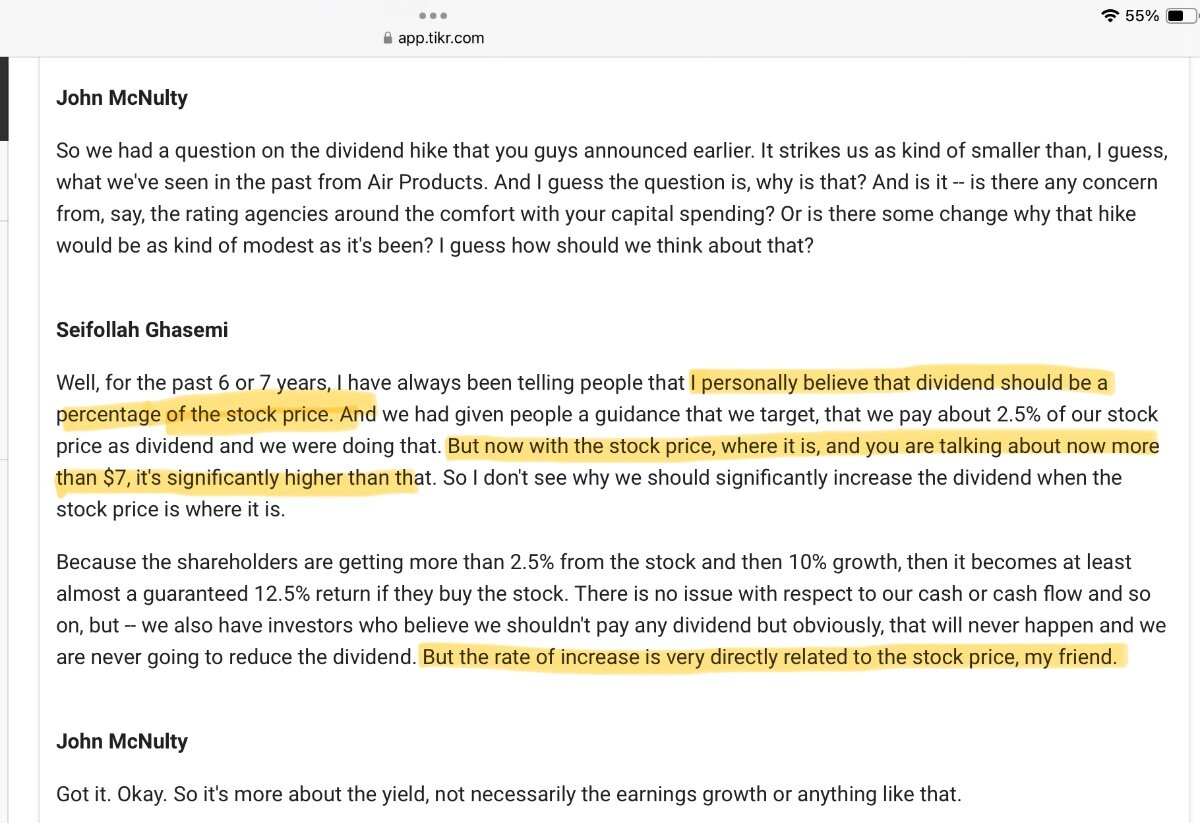

I also bought a few shares at the same price towards the close. I have to say I did not like management answers in the CC at all. His answer regarding the smallish dividend raise was downright strange and somewhat concerning. Really, the dividend is dependent on the share price based on a target yield? I have not heard that one before, except with some badly managed MLP’s. Anyways, may not matter long term and it’s a business I understand well. I think a couple years from now, this will be larger and more profitable, but near term, things could be a bit choppy.

-

Should have monetized my “unique insight” better. Thought about buying some short dated puts but those things work maybe 1/3 or 1/4 times for me, so left it alone. I very much like the industrial gas business. It’s like having a small royalty on industrial growth Each semiconductor fab build in the US will consume technical gases as long as they operate. This is a structurally advantaged business because once a supply is locked in, the customers rarely switch and the suppliers are highly concentrated. (Air Liquide, Lind, APD, Nippon Sanso (Matheson in the US) ). Those business will grow for decades and likely more than the GDP.

-

Andrew Wilkinson Thirst Post/Book

Spekulatius replied to TorontoChaosTheatre's topic in General Discussion

He always seems to be selling something. Not sure about Tiny either, saw it peddled on Twitter and in a podcasts. Anything that is peddled on Twitter (or X now ) should be approached with extreme caution. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

Spekulatius replied to tnathan's topic in General Discussion

The GFC may have a bit to do with BRO stagnation in that timeframe. When you look at earnings and revenues for BRO from 2006-2011, they were essentially flat for BRO and only started to rise again in 2012. Rising share prices are simply fueled by rising revenues and earnings and both simply were not there from 2006-2011. Any 100 bagger will likely go through periods of underperformance that last for years. -

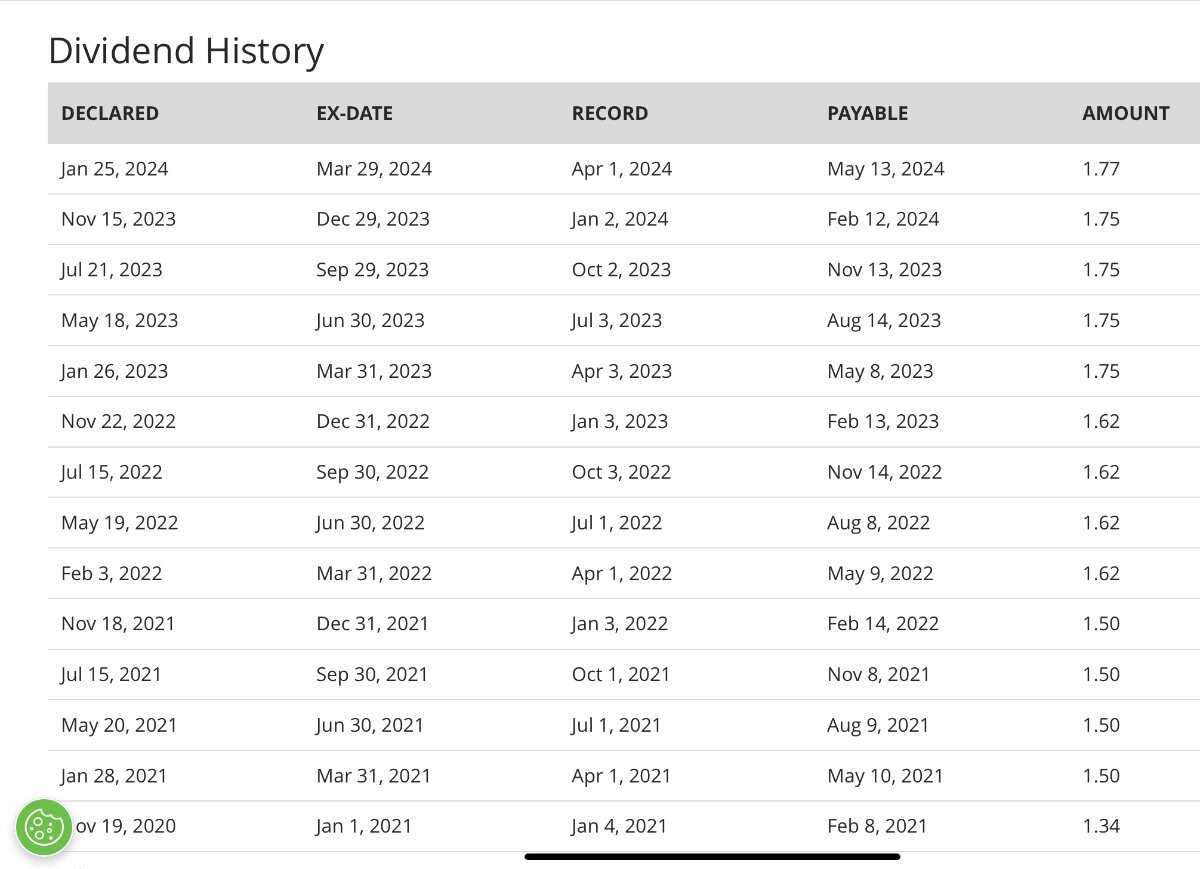

@cknucks regarding APD - did you see the very marginal dividend increase? It’s only a bit more than 1% and traditionally, APD raised their dividend by 10% annually. The current raise is much smaller. I may be reading tea- leaves here, but I think there is a decent chance that their outlook disappoints or that there is an issue with their ongoing investments.

-

FYBR has presentations in their IR section with uptake rates for the fiber builds and they do plan to get to 40% in a couple of years and track the progress to some extend. This applies to areas where there is no or at most one broadband competitor and they are mostly targeting DSL customers. But yes, the uptake time ramp is critical for the IRR, if it really takes 10 years + to get to 40% penetration, then the IRR are probably not that great. I think any fiber build that does not get to 49% penetration is probably it going to have a great returns because I have not seen many fiber builds with much less than $2K cost per connection (all in cost, not what some of those fiber overbuilders companies are posting ).

-

Added a bit more $JCI yesterday and $APA today.

-

The returns depend on uptake and cost to build. I think you can charge $70/month for broadband / give or take. Thats $840 in revenue/ year in re Neue at 80% margins. Uptake is probably 40-60% depending on competitive situation. If you assume 50% uptake, that gets you to $336 annual EBITDA and a 15% min requirement assumes the all in build cost needs to be $2240/connected location. Thats my napkin math. One thing that worries me is that some of the subsidized ACAM funded builds seems to have costs of $6k or more per connection. Even with a 50% subsidy (usually, it’s less) , that still a net $3k /connection and works only with very high uptakes. Some ACAM builds have cost up to $10K/connected home and I think those will be uneconomic.

-

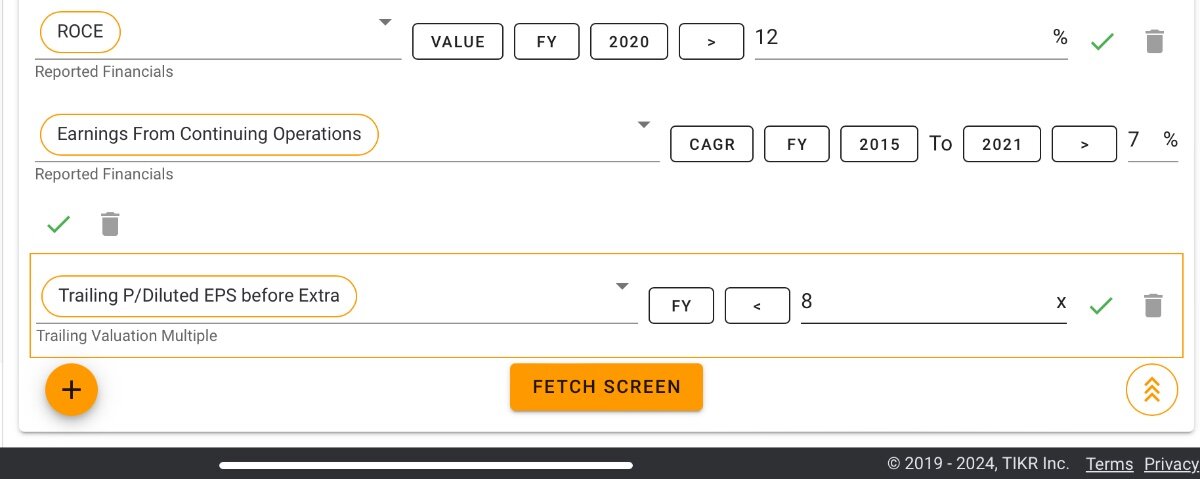

TIKR.com | Free Beta with Coverage of 50k+ Global Stocks

Spekulatius replied to Garpy's topic in General Discussion

Tikr has various attributes that you can screen for that are basically PE (screening fot OE<8) Below is what I use. I also use TEV/EBIT in some of my screens. I sometimes have issues with negative valued and than need to out in another criterium like (PE>0 etc) to eliminate those, if those results are too much of a nuisance.

-

How can you manipulate the VIX? It is a calculated number based on pricing changes (=volatility) of the stock market. Stating that the VIX is manipulated is the same than stating the the movements of the entire stock market is manipulated (I think). It makes no sense.

-

Seems relevant not just for $SLB. The Saudis are basically saying they don’t need that much capacity any more. https://finance.yahoo.com/m/8934cccf-80de-37a9-8dd3-89e59ccaa3a0/saudi-arabia’s-directive.html

-

Anders luck knows history very well. I watched some of the podcasts. What he describes is what’s called “Salami Taktik”. It means the aggressive power takes a bit (a slice of Salami so to speak ) and that watches what happens. If no credible counter, you take an other slice. Is it going to happen? Probably not. Would it be Putin’s playbook, if he were to start something? Absolutely.

-

Available for free now as a PDF: https://www.mcdonough-investments.com/_files/ugd/662cde_668e3018ef6e40fbb571f89677f88474.pdf

-

Human progress is hard to predict. If you followed tech progress and projections in the 70‘s‘s, you would have bet that most power is generated by nuclear power stations and that we would have a colony on Mars. Nobody predicted that we would have the equivalent of a supercomputer in our pocket that can connect to other superconductors in other people’s pockets anywhere in the world, Nuclear power didn’t happen because people soured on it not because it wasn’t technically possible. The Mary colony didn’t happen because after the Moon interest interest waned and we did not make any progress on rocket engine tech chemical powered rocket engines are limited in terms of what can be accomplished. The supercomputer ( smartphone ) became possible because Moore law kept compounding for 45 years and it is basically unthinkable what you can accomplish compounding technology at that rate for a long time. The rocket engine tech did not compound and is more or less still the same than it was in the late 60‘s. Investing is betting on human progress more or less and over t/e long term just as hard as predicting progress.

-

@cknucks Thank you for your input. I am very aware that technical gases is a structurally advantaged business. I have two concerns with APD: 1) I am not sure that the valuation reflects the higher interest rates going forward. APD is basically similar to an utility as they invest in assets with LT cash flows growing faster than the economy probably because they supply growth sectors like semiconductors and trends to outsource some non- core functions (like producing gases for internal consumption) rather than buying/outsource them. Cost of capital is likely to go up. Sure new project will likely take this into account, but the existing plant stock is likely locked in. Maybe those distinguishing plants benefit from inflation. 2) Most of the new projects have not locked in contracts. APD‘s management spent a lotmof time answering questions about the increased cost of the Louisiana plant, which their board just approved for $7B in Capex. there are no locked in prices for the end products which is Blue hydrogen and ammonia. They don’t lock in prices because they think that they can sell those green product for healthy premiums to regular products when the plant comes online. Maybe, but I am not sure we can predict those premiums yet. APD has a ton of the projects at several stages of progress, so there is a bit of execution risk which could add delays or increased cost and perhaps most likely both. I have put APD on my watchlist and will it monitor closely. At a PE of 20x, I don’t think there is all that much margin of safety here, but yo may not give them enough credit for the longevity of the business.

-

Bingo. Biden is not doing well with young voters, so my guess is that he feels he needs to do something.

-

I have bought and sold my fair shares of these nanocaps that trade for 50c on the dollar. most of my sales were out of frustration and be sued yo lost patience. They require lots of patience and may not work for a decade (I am not kidding here) . They are also not hard to find at all. The hard part is finding those with decent management or a catalyst. Thats probably no more than 10% of the population. Knowing what management is up to is absolutely critical, much more so this if your discount to fair value is 50% or 2/3 of fair value.

-

If you don’t mind a grab bag of assets, buy QUCT. You get 25k of farmland ( the result of a 19th century Mexican land grant) in near coastal central California for basically free. I am not sure it ever gets monetized though.

-

@John Hjorth Spirax Sarco - a great Uk company has the same thing , you can get a free hard copy of a book about their history. I ordered it and got it a bit later. It’s a great company too, but fully valued. https://www.spiraxsarcoengineering.com/about-us/our-history