Spekulatius

-

Posts

19,051 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

So, $KPLT has blown up already and $OPFI isn't doing too well either after their earnings report (trading (<$8/share). Also, the total sharecount is definitely 120M shares, which I think does not even include some equity compensation. I had initially assumed 80-90M shares. https://www.sec.gov/ix?doc=/Archives/edgar/data/0001818502/000119312521242313/d92438ds1.htm#rom92438_14 No position. Watching this from the cheap seats is definitely better than owning.

-

COST - Sold the other half in my tax deferred account I am keeping my small position in my taxable account

-

Bought/Added: KNBE (flipped position already) MSP: small starter (added before earnings) NTDOY (add) MGACPO.MX (add) TGTX (tracker)

-

I think these numbers are too high. It assumes no recession or even slowdown in the economy (BRK’s MSR, investments are fairly economy sensitive). Buybacks get less bang for the buck (in terms of % reduction in shares outstanding) at current valuations multiples. I think high single digits is far more likely. It seems that everyone’s expectation for future returns are creeping up with valuation going higher.

-

A few thoughts : Anyone noticed that Berkshire insurance underwriting combined ratio seems nothing to rave about. Premiums are rising in what seems to be a hard market, but they barely make any underwriting profit (~$376M). It doesn’t look that great when many other insurers are putting up great numbers. They bought back shares for ~$28B reducing share count by ~5%. ~$28B was the profit This quarter. It is not bad a bad buyback rate, but not exactly Teledyne league either. Anyways, decent quarter for a no brainer sleep well Investment.

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

Sounds like my kind of show. I will give it a try. -

Yes, we can have both. MMT something...

-

I wish this were just a dot com bubble. We now have an everything bubble, due to low interest rates. The lower interest rates for longer changes everything.

-

NTDOY / Nintendo (starter) and a tracker in ATVI.

-

Adds to FISV and Prosus /PROHY.

-

Probably this:

-

$LHX, running a tight ship. Probably the best management team out there except maybe $NOC. https://finance.yahoo.com/news/l3harris-reports-strong-second-quarter-103000248.html It is not a cheap stock anymore, but they execute very well.

-

Is it just me who thinks that writing TRS swaps in size on their own shares is a bad idea from a risk Management perspective? The very real possibility of a feedback loop of poor stock performance with real market-Market losses affecting the balance sheet should keep someone away, especially as insurance company. Just because it worked last time doesn’t make this a good process.

-

Sold ~1/2 of my $COST in my tax deferred accounts today. Looking a bit frothy.

-

The deal is done. Sponsor had to forfeit some founder shares and warrants to get this closed, which improves the economics a bit for existing shareholders (less shares and warrants outstanding): Sponsor Forfeiture Agreement In connection with the signing of the Waiver Letter, on July 15, 2021, FG New America Investors LLC (the “Sponsor”) entered into a sponsor forfeiture agreement (the “Sponsor Forfeiture Agreement”) with the Company and OppFi, pursuant to which the Sponsor agreed to forfeit: (i) 2,500,000 shares of the Company’s Class B common stock, (ii) 1,600,000 warrants to purchase shares of the Company’s Class A common stock at an exercise price of $11.50 and (iii) 600,000 warrants to purchase shares of the Company’s Class A Common Stock at an exercise price of $15.00, held by it, immediately prior to and contingent upon the Closing. It doesn’t look to me that Mr Market is enthusiastic about this deal, so I think the chances that this one trades significantly below $10 at some point are pretty high. No position personally.

-

Speaking of the too hard pile, I think FFH for me is one stock that belongs there. I agree it is cheap, but I think there are comparable business that are easier to handicap. For example ORI - a holding of mine has some equity exposure through a diversified portfolio of dividend stocks. no big swings and they keep a certain equity exposure at a fraction of book value with the goal of some capital appreciation and more importantly dividend income. No drama and it seems to be working quite nicely. ORI trades at <1.1x Book value and in my opinion is and easier bet to make going forward than FFH at 0.85x, but each it’s own.

-

Market Disconnect is One of the Craziest I've Seen in 23 Years!

Spekulatius replied to Parsad's topic in Fairfax Financial

It is likely that FFH is selling off due to lower interest rates, similar to other of the insurance peers. I don’t think there is anything special going on suppressing FFH in particular. A comparison with Teledyne / Singleton was always nonsense. Teledyne is an industrial and can be run without notional equity. FFH is a financial and need regulatory capital to run their insurance subs. They are already leveraged with some debt at the holding level and that‘s pretty much all there is possible. The other reason why FFH is trading at a discount is because their results are too inconsistent, compared to comps like BRK. I think they have the wrong structure, stuff like ATCO or Stelco really shouldn’t be held in an insurance umbrella. Those business are just too volatile for this. BRK hold quasi regulated equities like BHE Energy and their railroad subs which are really equity bonds. Those are keeping regulators happy as they deliver predictable results. -

I think the better way to look at SBC is to look at the dilution incurred relative to the amount of stock outstanding. Many SAAS stocks dilute quite a bit probably resulting in shares outstanding growing by or 3-5% annually, but this may still result in healthy per share growth, if a company is growing 30%+/ year. it is not so great for companies like WDAY where growth slows to 15% and yet shares outstanding still grow at a 3-5% annual clip. In any case, the SBC that makes the GAAP income statement look so ugly is a result of the high stock valuations at a given dilution rate. That assumes however, that the companies won’t grant more SBC if the multiples drop. From my experience, this is generally the case, if valuation metrics’s drop, company won’t make up for this by issuing more stocks and options. You can tell this by looking at companies that have traded at high multiples in the past, but at row trading cheaper like CSCO, ORCL. Ironically, even though they have aged gracefully in terms of morphing from growth into FCF plays, the market has not rewarded those companies much.

-

Bought some MEGACPO again (Mexican cable co). The first time didn’t work out as I sold when Mexico went into a COVID-19 tailspin. Perhaps now the second time does the trick. Seems eternally cheap though.

-

re SHVA - I have it on my watch list. I think it has been a Kuppy pick, or someone else from FinTwit. it seems to trade at roughly similar metrics than FISV, but with better growth. I did not feel that the risk from the “antitrust” like lawsuit from the regulator and the fact that it operates in a not so geopolitical stable area (Israel) makes it that great of a bargain.

-

A starter in FISV and a small add to VNT.

-

TIKR.com | Free Beta with Coverage of 50k+ Global Stocks

Spekulatius replied to Garpy's topic in General Discussion

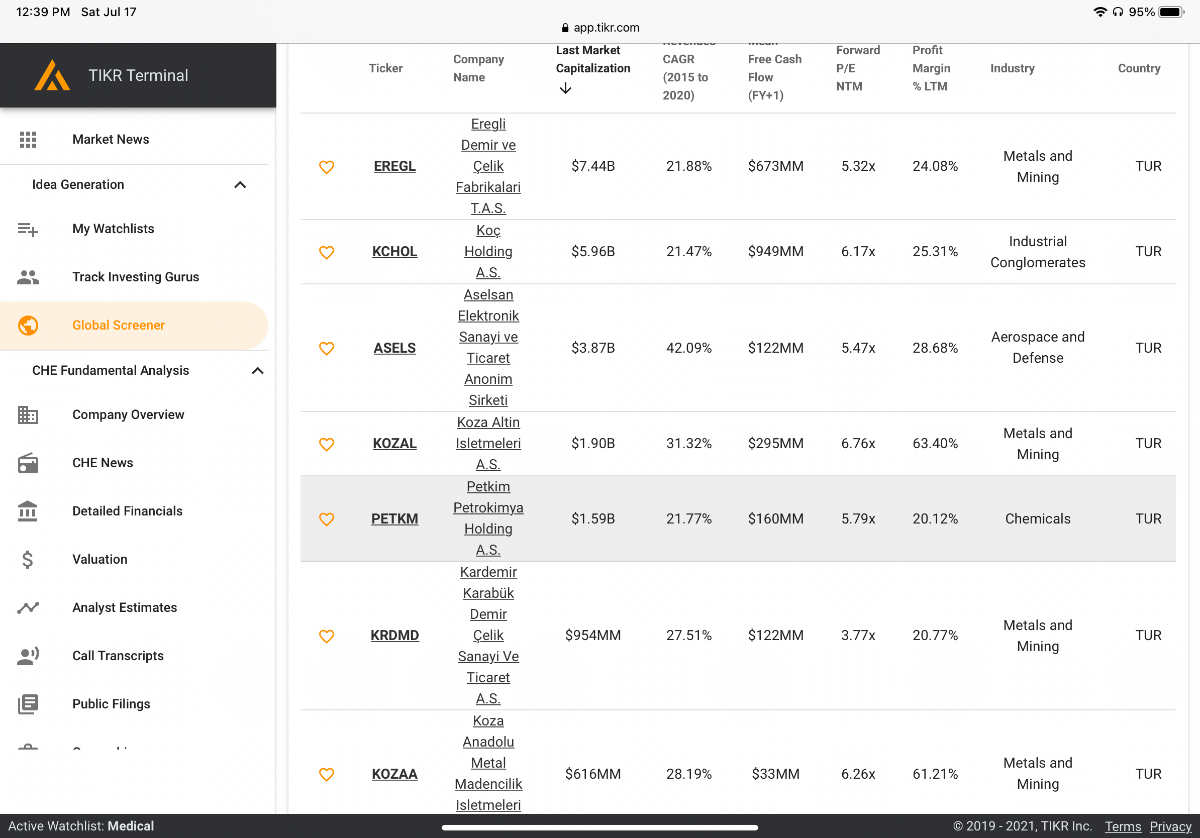

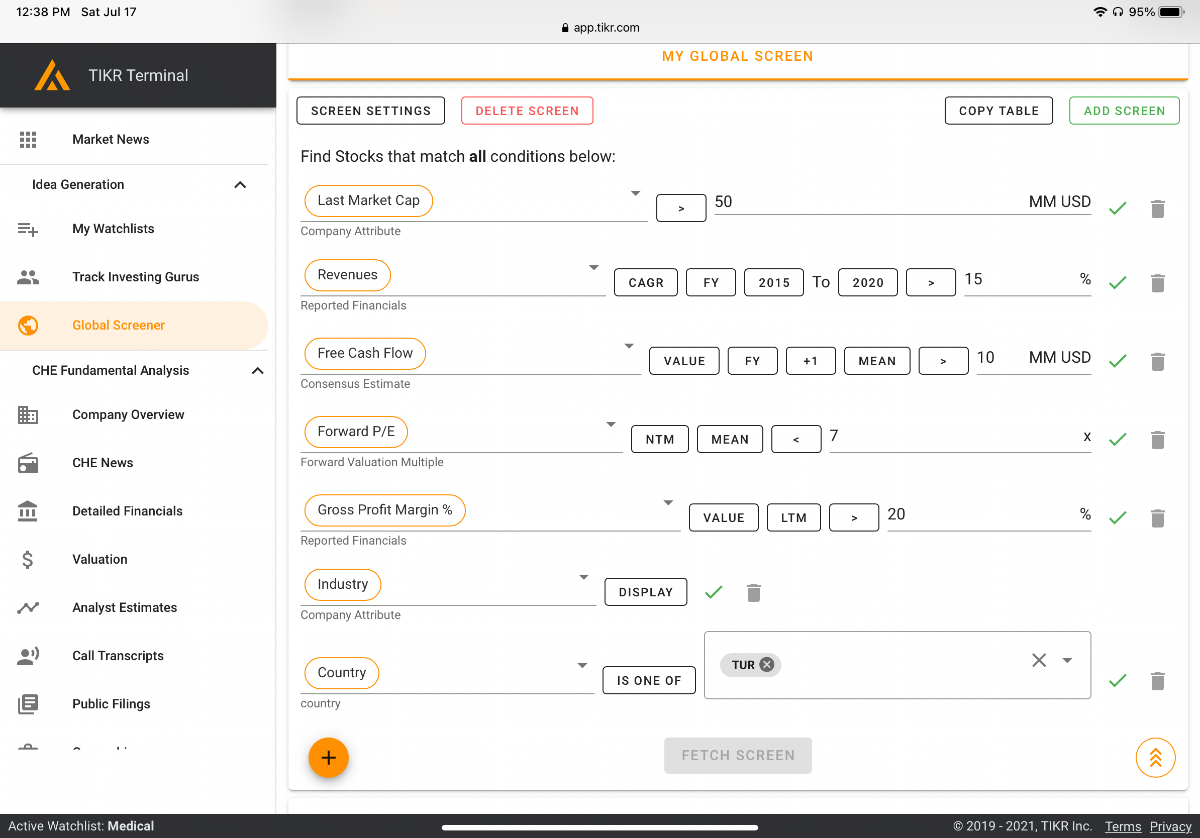

Ok, now Tikr @Garpy has a screener. Took it for spin for a country where Angels fear to tread - Turkey, with some pretty prohibitive valuation metrics and got some hits: KHOLY has an IDR that trades with somewhat in the US: (Edit, when looking at growth, just be aware that Turkey has ~15% inflation right now)

-

The USD is the best house in a bad neighborhood. There is just no alternative as far as fiat currencies are concerned. Yen and Euro both punish you with negative interest rates, the chinese yuan isn’t freely convertible, the Swiss Franc and the GBP are too small to matter ( GBP has worse fundamentals, imo). You can try Bitcoin or Gold which both have issues. Gold is probably the best of above ( imo). TINA basically.

-

The problem with Koyfin is that the GUI is not intuitive for most users. It requires a certain way to get something that comes very easy on most other platforms. My biggest beef is that it’s not useable on tablets like my iPad. This is how my screen looks like: It basically unusable. Desktop looks pretty good but most people use mobile platforms nowadays for a lot of things.

-

$MNPP is basically back to pre-COVID-19 levels but their biggest asset is a stake in a outdoor shopping mall. Even their office isn't doing too badly but there still could be long term fallout. https://backend.otcmarkets.com/otcapi/company/financial-report/284793/content