Spekulatius

-

Posts

19,051 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

I don’t think it is likely that FFH’s discount to NAV will close, the complexity and the fact that it is an controlled entity will make sure of that, even if performance improves (which is the bet that we are making). I can see this going to 1x book perhaps, but quite frankly, I don’t see this going to 1.3x book for a long time. This is more of a reversal to the mean stock than a LTBH compounder for sure.

-

If a Buffett made a mistake, it was selling Disney shares he received from the Capital Cities merger in 1998. His earlier sells were the correct decision. Buffett back then could flip assets and get higher return than pretty much any compounder could. That changed over the years due to size and a changing investment environment.

If a Buffett made a mistake, it was selling Disney shares he received from the Capital Cities merger in 1998. His earlier sells were the correct decision. Buffett back then could flip assets and get higher return than pretty much any compounder could. That changed over the years due to size and a changing investment environment. -

^ Holding discounts persists due to complexity and FFH’s complexity has been going up over time. Then add to this sometimes questionable execution and volatile performance and you get to where we are. I believe the best way to reduce holding company discounts is to reduce complexity. There is plenty of stuff that could need some trimming: 1) Stelco and RFP. they should dump RFP or at least get large cash dividends to invest elsewhere. Perhaps weed out some Private Investments that don’t work out (Toys are US etc). 2) WTH are they doing in Africa. If they think they have expertise and an edge in India, they should put the focus there. I think they should get rid of FF Africa and roll proceeds into FF India. also get rid of that Egyptian bank when they get a chance - this country has screwed over investors several times (nationalization) and will probably continue to do so. 3) some of the insurance subs probably could use some pruning, but they are not the main issue now. Besides reducing complexity, higher interest rates will be the main driver of revaluation. I think higher interest rates are becoming more likely and they will benefit long tail insurers like FFH in particular. If interest rates really rip, you want to own life insurers, I think.

-

While we could be missing something as far as business is concerned, I think the likely explanation that fund flows into tobacco equity is negative because ESG and investment mandates exclude more and more investors from owning them. I know quite a few investors who would never own tobacco /nicotine stocks (for ESG or other reasons) and actually Berkshire is one of them. I actually think it is possible that this changes when Buffett is not around any more.

-

Some good ideas posted on this thread, so maybe worth keeping it up. Within the compounder basket, I like and recently bought or added: LMT, ATVI, TTWO, FISV, NTDOY All of these have some hair, but they have reasonable LT track records (except NTDOY depending on your timeframe) and are in attractive industries with tailwinds. I think AMZN is also reasonable (bought it early this year).

-

Yeah, mine filled literally in the last few seconds, I believe. I paid $393 and a few pennies. Someone really wanted to get rid of shares before the weekend.

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

Spekulatius replied to thepupil's topic in General Discussion

You guys better make money by the boatload with these rents. -

Picked up a few FRFHF shares at the close.

-

I would say "Amen", if I were religious. Why do people mess with an inferior vehicle like FF India when they can perfectly align themselves with an operator and just buy FFH?

-

Small adds to BTI, MO, BMY, NTDOY, MXCT MEGACPO.MX and a starter in ALSN.

-

I am also adding to BTI. Might add to MO as well. Owning tobacco stocks means getting constantly screwed over while cashing in ever increasing dividends.

-

^ Again, maybe I appear like a smartass, but it doesn't take much to rip the Communist Manifesto apart. Karl Marx basically stated that he could predict the future outline of history as a fairly rigid sequence of events that would inevitably end in communism. The idea to predict the future far out is already ludicrous by itself and even his disciple Lenin realized that and said screw the model and started the revolution in Russia even though technically the country wasn't ripe yet. So really he Manifesto has been proven wrong as a model and of course communism never really worked either. If you want to teach history in a simple book, read the "Animal Farm" from George Orwell. Even kids can understand that one. I wish students in history classes in school would study the source material and in this case read this very short (36 pages) treatise. The teacher just need to ask a simple question - did any of the things Marx predicted actually happen? I think some interesting discussion should flow from there.

-

Cathy's picks aren't so hot recently. This is how I imagine it looks like when the reveals a new one:

-

Agreed. i do think semi equipment manufacturers will see a lot of pain once the boom subsides. TSMC can scale their Capex down and will generate strong FCF in a downturn. They will be fine. A lot of the semi "experts" on twitter never have seen a down turn in semi's. Even the 2008/2009 recession was pretty short lived. 2000-2002 not so much. The industry has gotten better handling downturns though due to consolidation and better supply chain management (Flexible cost structure). It is still fairly cyclical. I don't work in semi's, but our sector is loosely related and after customers buying everything we could deliver in 2020 and mid 2021, we know see a glut in inventory for some of our components and orders are way down. I have seen about 4 of these cycles since I started working ( the 2001-2002 downturn was by far the worst) and they never get old. I think we will see the same cycle post COVID pretty much in every industry and commodity.

-

I can even condense it in one sentence: Don’t be an asshole and don’t fool yourself. You should get very far just living by that. Easier said than done though.

-

If inflation is really at 5% and the government is paying 5% on bonds then it isn’t really paying anything, as the principle is getting eroded at the same rate than interest rates are paid. It is an even better deal for the government, if you take into account that taxes get paid on interested. This is effectively still a negative interest rates. Also keep in mind that with 5% inflation, the GDP will go up by 5% in nominal terms, plus whatever real growth we get, so the borrowing base gets larger. Again government never pay back debt, they just roll it over.

-

Interesting. I listen to this episode from Broken Silicon pod cast and that fellow with 40 years of experience expects that the semi shortage will become a glut, probably in 12 month or so. I believe Mr Market will smell the rat before the turn happens most likely. I think there is going to be a lot of money made with puts if you can time it well. Insert “First time?” GIF here. https://podcasts.apple.com/us/podcast/broken-silicon/id1467317304?i=1000536154890

-

I don't think one even needs the "Site:" command any more. I just type in "thecobf.com BAC" in the chrome input bar and off it goes.

-

Look at the thread title. If that doesn't sound the hook line from a self help guru, then I don't know what is. I know very little about his other work, and that isn't really the focus of this thread. I also don't even know about political biases, nor do I even care. Self help gurus go into my trash inbox and that's all there is to it. Others may find value in what he does, which is also fine with me.

-

Treasuries are not an "investment", they are a way to park money. Treasuries are hyper liquid, can be used as a collateral and are "safe". This make them a cash alternative ( with short duration) for a lot of institutions even though they offer very low yields.

-

I believe the ascent of crypto competing with gold has more to do with it. The correlation with the stimulus package is coincidental.

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

I watched the first show from the Foundation series and it is mesmerizing. Great production. I have read Asimov, but never the Foundation series. They could really develop this into a franchise, imo. -

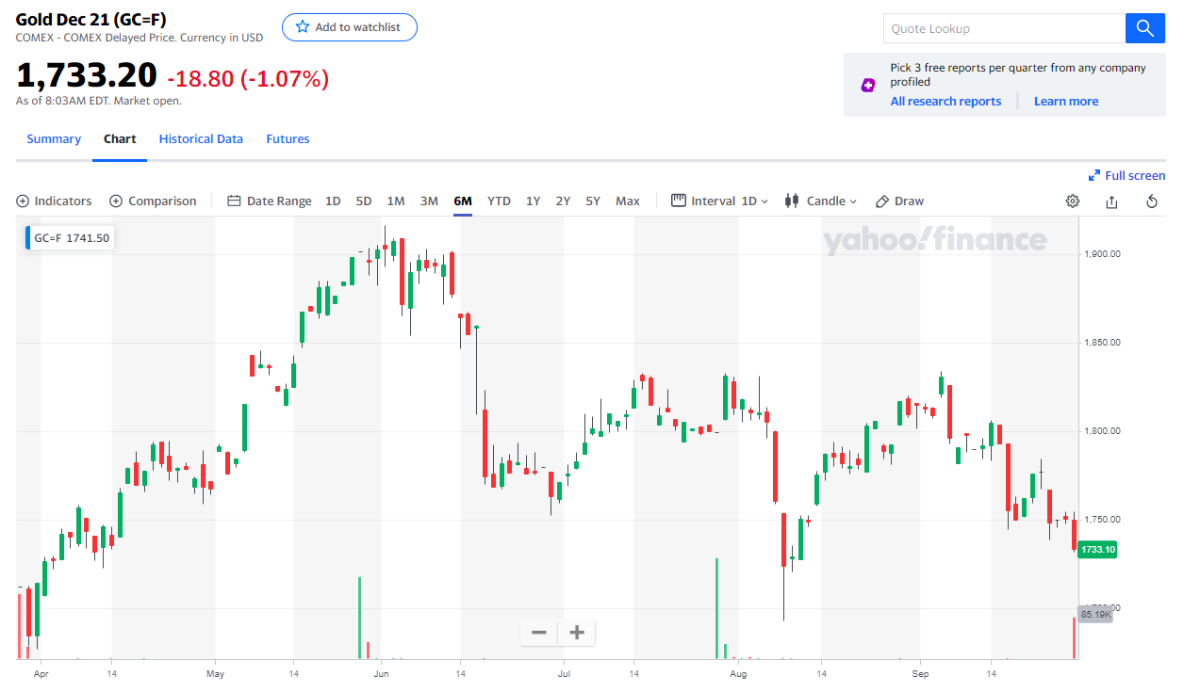

Interesting - gold used to be the classical inflation trade and trending down. This occurs every time there is hint of rising interest rates:

-

No argument here that it can go on much longer. But here id a contrarian point, at least for equity markets: The Fed pretty much said that they are going to stop tapering toward the end of this year and in the past, this has let to temporary hiccups. I actually think that what the Fed does (specially tapering) is not as important than what the treasury does, but I think many differ and those panicking may be all it takes to get things moving downstairs, at least for a while. Now, there is a question if the Fed does what they said they are going to do. I think they will. Anyways, for a longer term investor, that’s noise regardless which way it goes.

-

It doesn‘t look like fear of losing money is the prevalent theme currently. If anything, the boom in collectibles from baseball cards , to vintage cars, NFT or crypto, booming real estate and expanding equity valuation as well as cheap credit (basically record low yield spreads) seems to indicate Ehe complete opposite. So in my opinion, the inflation trade is already in full swing. If you enter now, you are by no means early here. Thats doesn’t mean it can’t keep going.