Spekulatius

-

Posts

19,051 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

Great podcast episode recommendation thread

Spekulatius replied to Liberty's topic in General Discussion

Business breakdowns by itself is a great podcast series, but I found the Episode about the Ethereum blockchain particular great and I am generally indifferent to crypto. What I like about this podcast is that it describes actually what can be done with the Ethereum blockchain and why it was the designed the way it is and differences to Bitcoin. https://podcasts.apple.com/us/podcast/ethereum-into-the-ether-business-breakdowns-ep-09/id1559120677?i=1000522314009 -

You can’t shut down Bitcoin or other cryptocurrencies, but you could deter institutions or even citizens from owning and using it, via taxes, money laundering laws etc. If you can’t use it, any crypto currency is pretty worthless, imo. It is also true that the marginal cost (which consist of energy and depreciation for crypto mining equipment) is set by the price of the cryptocurrency , so the more valuable crypto becomes, the higher the consumption of resources. I think we would have a similar problem if we were on gold standard without inflation. We would have to dig for more and more gold if the economy expands to create enough currency to facilitate trade and have a enough gold as A store value (outside of the productive economy). From a macro economic perspective, it is quite interesting to see how this is going to play out. Maybe there is a play here in Iceland real estate or some utilities in countries with an abundance of cheap energy, besides the obvious AMD and NVDA.

-

I would buy BAH before I would buy TYL. BAH is more federal government consulting , I think @Inofeisone gave some interesting insight that they can leverage this to get more business from states and cities. BAH is a consulting business model that in some way looks similar like my cherished defense contractor stocks, but perhaps with better organic growth prospects. BAH stock has seen some multiple expansion but it is not close to being valued like TYL (for good reasons) but if they can compete against them in the future, this could become a different story. It is a great business as the business relationships last often many decades. That reminds me to do more work on BAH (I put it in the maybe pile a while ago.)

-

There is also a sweet and short one with CNBC: I always enjoy his commentary. He doesn’t have a fixed view and keeps an open mind.

-

Ok, yes, this makes sense.

-

How does someone who has been actively on this site for a while get value from a Phil Town course? That stuff seems pretty basic, at least based on my first look.

-

^ I assumed the lower provisioning was caused by a better than expected loan losses due to stimulus checks. I don’t know if they arbitrarily juiced their results. Frankly, I don’t care, if what they are doing is good for society or of it is fintech or a grubby payday lender. If they can lend at ~100% APR (which is what their income statement and balance sheet suggests) and lever it just 2:1 and keep loan losses to a manageable 30-50% () this business prints money like no other. I do think that there is absolutely no reason to sell a business it’s economics like this, so I assume some sort of regression is going to happen and the folks selling the business know this. I think I just keep watching this post deal and see how the business goes. Perhaps I take a flyer on the warrants if they are cheap enough.

-

Doge is a hustle and Elon is a hustler.

-

It is easier to create new cryptos than it is to create new elements. If you are a celebrity (Kardishan) or an organization (think NFL) or a company (Tesla) to name some examples, is there really a downside to create to create your own crypto currency and promote the hell out of it? The technical barriers to entry are nil. Dodge coin has proven to get to $100B in market value. That’s larger than the entire US airline industry in terms of market cap.

-

This is a pretty good Twitter thread on the “True Lending rule” from the Trump administration that made life easier for subprime lenders that operate across many states: Repealing this rule could impose some additional regularity cost for lenders like OppFi, but it is not clear how much that would affect the bottom line. OppFi tried to sell itself as Fintech, but it really is a deep subprime lender. The profitability and growth has been mind boggling - they basically 10x their size and equity (equity growth from $9M to $99M) just through retained profits. I don’t care how you call this, if it is that profitable, it is probably the best business I have seen ever. Of course there is the catch, if something is too good to be true, then it typically is. I suspect as this grows in size, someone takes a close look at it and then the problems start. It was mentioned in the podcasts is that their Glassdoor reviews (4.4*) and BBB rating are pretty good. The Glassdoor reviews look a bit generic and it is clear that management or HR is looking very closely at them. The high number of reviews in Glassdoor (~190 reviews for ~500 employees) suggests that management is managing Glassdoor postings too. I searched in the Apple App Store and didn’t find and App for AppFi or Apploans. Strange. Fascinating to see how this plays out.

-

So, I listened to Bill Brewster’s business brew podcast and he has an episode where he interviews Jared Kaplan from OppFi. OppFi is going public via a merger with the FGNA SPAC this year. Bill and Jared talks a lot of about OppFi business, which caters to subprime customers and why it is a good value proposition for them. Anyhow, I looked at OppFi’s pre IPO numbers and almost can’t believe how profitable it is, to the point where the numbers are absurd: https://www.sec.gov/Archives/edgar/data/0001818502/000119312521135035/d135342dprer14a.htm#tx135342_22 The numbers are almost absurd. Their revenue is about equal to the size of their balance sheet, which means APR is around 100%. ROE is about 200%. they bumped up their equity from $37M to almost $100M through earnings last year. last year was probably a best better than average due to stimulus preventing defaults on their extremely low credit worthy customers but even befor thwt, the numbers look quite Impressive. Quite frankly, what I don’t understand is why they are going public at all (you don’t really need to raise external capital with this profitability) and Joe the customers don’t default en masse with the type of loans. This is not really addressed in the podcast, but the filing shows the profitability so unless this is all fake or not repeatable, it is one of the best business I have ever seen. The FGNA SPAC is launched by Kyle Cerminara and Larry Swets (which I understand some have mixed feelings about), but are well known in fintwit for their BTN involvement #lumbergang. (No position yet).

-

John Hampton posted something interesting on Twitter. Type in the Google window: “ How to buy “ and see what comes up. Here is mine:

-

Reduced GD a little. I feel it has reached fair value around $190/share.

-

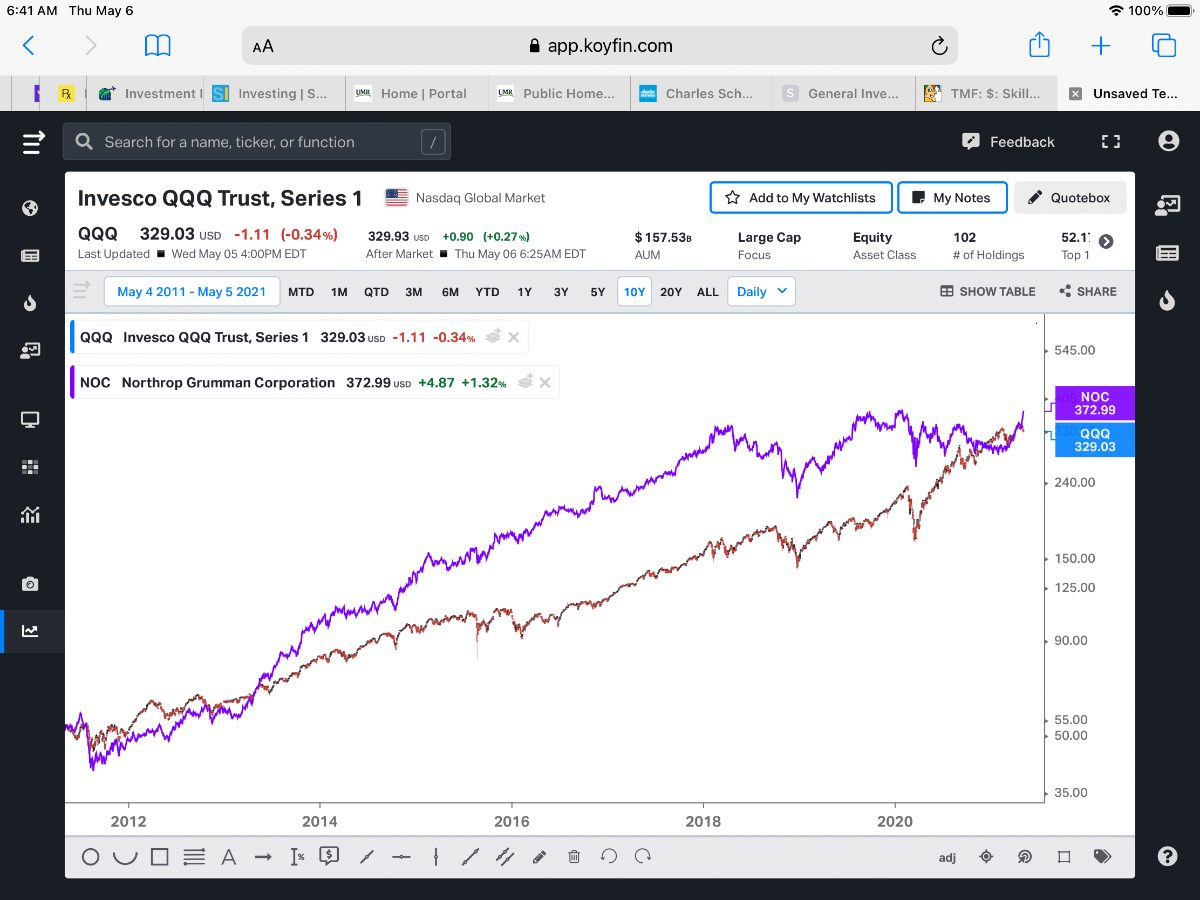

NOC results were quite strong, due to new programs contributing ( GBSD, space, classified) so this is just a friendly reminder (thanks to @lhamtil from Twitter) that NOC has beaten the QQQ over the last 10 years as well as 20 years (NOC has underperformed the QQQ since 2018 though).

-

Tracking positions in QLYS and in recent medtech IPO NPCE (speculative).

-

Primer: A Look at India's History and the Path Ahead

Spekulatius replied to nwoodman's topic in Fairfax Financial

Also, how are folks that are closer to India than I am judging Modi? He seems to be incompetent at best and perhaps even malevolent. In addition to the stretched valuation metrics (see above), this looks like a lousy setup for a stock market - high valuations, declining profitability and lousy leadership ( which really matters in Emerging or 2nd world countries). India always has been the country that could but never actually got the job done. Why would this time be different? -

Transcript from tikr.com: https://app.tikr.com/stock/transcript?cid=255251&tid=2594156&ts=2266536&e=696911379&refCode=o94y6y#

-

Sold my RNR - disappointing business performance. Stock went up since I bought it, but I lost confidence.

-

@Castanza Holly Molly, what a project. We just do small stuff like painting, replacing faucets etc. but nothing like this. I agree on YouTube being an amazing resource. There is almost nothing that can done that can’t be found in YouTube.

-

The herd immunity apparently never really get's reached because immunity wanes and the emergence of new variants that partially render the natural immune system defense obsolete. That is probably why we are seeing a second wave in countries like Brazil and now India. I think we will see more and more the mRNA vaccines becoming the gold standard here because of high efficacy and the ability to ,more quickly fine tune them against variants. i fully expect to get a BionNtech booster shot tuned for protection against variants probably by winter 2021. Vulnerable countries beyond Brazil and India are China (low vaccination and mostly crappy vaccine), Japan (already in shutdown) and pretty much the rest of SE Asia (low vaccination). The US is probably close to peak vaccination rates and should be able to export vaccine pretty soon to help out.

-

It might be time to have an ounce of prevention and vaccinate the portfolio a bit just in case this has consequences beyond just India. it is not that we never have seen this before.

-

Central bank policy makes no sense to me. QE makes no sense (imo) but it does not prevent central banks from trying.

-

Mohnish Pabrai Q&A at Indiana University.

Spekulatius replied to MattR's topic in General Discussion

There is nothing wrong with changing your mind of course, but $150M isn’t exactly small change nor is buying an entire company usually an easy to reverse decision, so I think this episode reflects very badly on how much he knows about what he buys or owns. -

Mohnish Pabrai Q&A at Indiana University.

Spekulatius replied to MattR's topic in General Discussion

I guess “cinches” have replaced the “spawners”. -

Yeah, the updates continue, they will get it right eventually.