All Activity

- Past hour

-

Another example of this garbage. Norway scored 3 goals, one was disallowed. Brazil did nothing all game and was given two penalty kicks on plays in which neither scoring opp/penalty was anywhere near being an 80%+ chance of a goal. Justice prevailed but was just aggravating to watch the game being artificially kept close

-

That one-liner key sentence is actually kind of clicl-bait, @Spekulatius LoLz! - Furthermore I simply lost my focus and attention after a quarter of the interview because of Anthony Scaramuccis T- or sweat shirt and the view to his bookshelf [nosy!] I swallow the rest of the interview after some sleep. The take is very interesting for a European citizen like me.

-

Americans donated a record $617B in 2025! Cheers! https://philanthropy.indianapolis.iu.edu/news-events/news/_news/2026/giving-usa-report-2026.html

-

Insurance - The Engine That Drives Fairfax

SafetyinNumbers replied to Viking's topic in Fairfax Financial

Great write up as usual Viking. Thank you. The minority interests seem to be structured as preferred shares masquerading as common shares. Effectively, this reduces operating earnings until the minority interest is bought back. It also ensures the capital deployed to buy in the minority interest earn very high returns. The key to compounding is high returns on incremental capital deployed. -

Yup...no one can say that the big guns didn't show up. Cheers!

-

Congrats to Norway beating Brazil! Haaland, Messi and Mbappe have now all scored 7 goals so far, followed by Kane with 5 goals.

- Today

-

So the FIFA dismissed Balogun's red card after pressure from the U.S... Didn't know the US was scared of a country literally 0.3% your size and 3.5% your population. That said his red car was very light so... bring it on! I'll be up at 2 am with friends watching in silence so we don't wake up the kids.

-

Does NK have the resources to initiate a 51% attack even if most mining stops? From what I understand bitcoin fees represent 1% of mining income, therefore in that extreme case you'd expect there to still be some miners around so attack cost won't be zero. But do you think all miners will stop if input cost > cost to mine? And is that happening or has ever happened or likely to happen? Reminds me a bit of negative cash flowing real estate. Lots of people carry negative cost with their tenants while hoping for the capital cost of the house to eventually outstrip that loss. The funds obviously come from borrowing or some other side venture. So I guess the price of bitcoin is also critical for this and the question is if the price of bitcoin has some components independent of mining costs. Even its speculative or ideological value of people buying it would prop it up in the absence of profitable mining?

-

Same as it was with Brexit, and MAGA; the ruling classes have done such a poor job for the average Joe, and for so long, that Joe increasingly sees the alternative as better. The growing wealth extremes, the harder it is economically becoming for Joe, the rich flaunting their wealth and privilege, etc, etc. The rational solution is increasingly fuck 'em, let 'em all burn, and immigrate to a better life elsewhere. Visit, but don't live there. Of course, the growing nationalism isn't good, and conflicts will be largely unavoidable. While NATO's re invigoration and supply chain upgrades aren't a bad thing; the sad reality is that the rest of Europe typically does best, only after large areas of it have been economically devastated (wars, disease, etc). About once every three generations (70-100 years) on average. Add AI, and what are these people to do for a job? Rational behaviour .... we just don't want to hear it. SD

-

Pretty good, interview: Key sentence: Trump runs the Democratic Party. I think he is right about that.

-

For those who want more information, below is the full quote (lightly edited) from Fairfax's 2026 AGM that Article #6 above was based on. Question from Moderator Jeff Stacey Prem and Peter, our first question is about the current insurance environment. The question is as follows. Fairfax had record underwriting profits in 2025 of $1.8 billion and achieved its objective of $1.5 billion. You commented, however, in your shareholder letter that insurance pricing is beginning to soften. I would appreciate hearing any additional comments you might have about the current insurance underwriting environment. And specifically, do you think that Fairfax can still achieve its $1.5 billion underwriting profit target in a soft insurance market? V. Watsa - Founder, Chairman & CEO Thank you, Jeff. Peter will usually answer this. But we do have Andy Barnard, Brian Young, Lou Iglesias and Silvy Wright here. So, we'll ask them instead. As Andy makes his way up to speak, let me just say… yesterday I had people ask me: “What is the biggest -- best -- acquisition you've ever made?” The best one is Markel Insurance - the first one (1985) - because otherwise, you're not in the P/C insurance game. And the second best was a small company called Skandia America Re (1996). And why? Because I had to get someone to run Skandia. I went to New York three times to get Andy Bernard. The first time he said, "You got to be kidding me.” Over dinner he said, “I'm not going to leave Transatlantic to come and join Skandia." That's how it began. After a second and third attempt, ultimately, we were fortunate to get him 30 years ago. He's had a huge impact on Fairfax. In 2011, all of the insurance companies began reporting to him. After he started in his new role – 15 years ago (2011) – he said that he hoped that the insurance business will have the same reputation of being fantastic like the investment business that we had at the time. And the investment business did a little less well, and the insurance business has done fabulously well. Andy, over to you. Come on in. Andrew Barnard - Chairman of Fairfax Insurance Group Thank you very much, Prem, for all of that. I'm going to let Brian and the others talk about our position, the market and our prospects. As Prem mentioned, I've been in this role now for 15 years, and I thought I'd just give a little brief broad perspective on how I look back on that. I divide that 15 years, which started in 2011, into two periods. First, 2011 up to 2019. Looking back with the benefit of hindsight – this was a period of preparation. During that period, we added Allied World and Brit – two very powerful new platforms with capabilities that really build out our suite of products. We had Crum & Forrester, bolstering its capabilities. We had a few small acquisitions. Earlier on in that time Northbridge finished its integration, which really positioned it as a much stronger company. And of course, during this time, Odyssey and Zenith flourished. (Yes, Zenith had a few tough years at the beginning.) And we built out the international operation during the latter part of that first period. As Peter mentioned, it has become a significant business that we think will serve us well in the future. This was really a period of preparation that brought us to 2020. At Fairfax, across our companies, we now had in place excellent leaders, leaders that are fully aligned with Fairfax’s culture, that embody the trust, the transparency, the talent that without which our decentralized system could not function. That's all in place as we roll into 2020. Of course, the big thing at the start of the year was the pandemic. A lot of companies heading to the hills, a lot of uncertainty. Plus, we had a very attractive hard market that had already been underway – and I think the pandemic just accelerated it. So, we were at that time in just a unique position because of our structure, our capability, our leadership to thrive. And thrive, we did. Over the subsequent years, we go into the second period, 2020 up to 2025. From 2020, we virtually doubled our premium volume, and almost all of that was organic with the one exception of GIG. The vast majority of that growth was organic, driven by our companies by their leaderships, by their management teams. And more importantly than that, our underwriting profit over that period more than quadrupled. This is where we really came into our heyday. Today, to 2026, we're recognized as an underwriting powerhouse in the industry by the marketplace, by the rating agencies. We had huge increases in our ratings over the last 1.5 years. Looking back on it all over the past 15 years – with the benefit of hindsight – we just positioned ourselves so favorably to really take off when the market conditions were supportive of that strategy. I believe that what we built is built to last. It is built to withstand the pressures of the market cycle. Those who follow the industry know that we're in a softening cycle where things become more challenging. But we're very confident about our capabilities – about our management abilities – to navigate through some more challenging times and to sustain superior performance as we go into the future from here. I've been in this industry now for close to 50 years. I've been at Fairfax for 30 years. I'm not going anywhere quite yet. However, my good friend and partner of the last 36 years, Brian Young, is taking on a larger and larger share of the oversight responsibilities in Fairfax. Those of you who have followed Odyssey will know Brian took the helm in 2011. It's very clear that Brian is someone that knows how to make money in this business. And so, I think our future is very, very bright as we move forward from here. So let me turn the microphone over to my friend, Brian Young. Brian Young - President of Fairfax Insurance Group Thank you, Andy. I learned some big news a few minutes ago. Andy told me that he is going to be a grandfather for the third time. So big hand to Andy. I will cover the AI question (from earlier), the current market environment and our ability to generate an underwriting profit in the current environment. But first I want to highlight, as Peter mentioned, $1.82 billion of underwriting profit in 2025, fractionally higher than $1.79 billion in 2024. Combined ratio of 93%. Embedded in that was 4.8 points of CAT loss or the $1.2 billion, the biggest being the California wildfires in Q1. Within the 93%, we benefited from 2.9 points of favorable reserve development. And it's important to note that Fairfax has had 19 consecutive years of favorable reserve development for the last 2 decades. Our reserves have been a store of value. As you all know, all of our companies are really focused on disciplined underwriting and strong reserving. Prudent reserving is really foundational to disciplined underwriting. We have more than 30 operating companies. Nearly all of them equalled or exceeded expectations from an underwriting perspective in 2025. The small number that didn't – we weren't expecting them to make underwriting profits given the market circumstances that they faced. So, there were no negative surprises in any of our companies. I'd like to highlight a few standout performers, focused first on the big companies. Let's start with the most recent recipient of the Athappan Award, Allied World. Our largest insurance company generating record underwriting profit of $546 million – a fantastic result. Congratulations, Lou and to the team. I'm going to let Lou come up and tell us what the secret sauce is that's made Allied World so successful. The second company I'd like to highlight is last year's recipient of the Athappan Award, Northbridge. Silvy and team delivered the lowest combined ratio, at 88.3%, of all our big companies. In the last 4 out of 5 years, Northbridge has delivered a combined ratio below 90%. And Silvy will come up after Lou and give us an update on Northbridge. Turning to the international side. We generated $220 million of underwriting profit, more than double what we generated in 2024. The standout performers – Colonnade, Bryte and Singapore Re – all generated record underwriting profits. Singapore Re, headed by Philippe Mallier, had not only the lowest combined ratio on the international side, they had the lowest combined ratio of all of our companies at 77%. Well done, Philippe. Our premiums were $33.3 billion. It is slowing down. The market is getting more challenging, no doubt. And we have to exercise more discipline. We have to be more selective in the risks that we take. We have to focus on our line size deployment. But we still think there's opportunity out there in the market. The sectors of the business that are under the most pressure are the ones that have generated the most profit. So yes, the margins are shrinking, but we still think the margins are ok. When the margins are not there - when there is not that margin of safety we need to take on the volatility of insurance – then we're going to scale back. There's no pressure on any of our companies to write for top line growth. And I've experienced that at Odyssey working there for 28 years, leading it for 14 years, never did I or any of our people have any pressure to write for top line. On the question of AI, it's important in our decentralized structure, innovation comes from the ground. It can't be forced from the top down. And we've got 30-plus wonderful businesses. Everyone is focused. AI may well be very transformative. We're not at the cutting edge, and we don't really want to be at the cutting edge. We're where we think we need to be in the pack with the rest of the insurance industry. To understand and take advantage of the innovative things that we're doing at the company level, we formed an AI working group, across the Fairfax organization. We have more than 75 people participating in the working group. We have developed more than 100 use cases. We have a SharePoint site. If we develop a use case in a company in a certain part of the world, we can share that with the other companies through the forum, through the SharePoint site. In terms of the AI use cases, most of them have really been focused on improving process, doing things faster and smarter – trying to underwrite more business efficiently through the use of AI. Using AI to inform our underwriting decisions. Marc Adee (President of Crum and Forster) has used the phrase, and I think it's great, does AI bang the cash register, does it lower your loss ratio, does it lower your expense ratio? I would say right now we're not banging the cash register yet. With AI, we are able to underwrite more business using the tool than previously. Lowering the loss ratio, lowering the expense ratio in terms of the AI tools that we're using, that's really the focus. And I think lastly, it's really important to say, and Prem has emphasized it ad nauseam that AI will not cost us any jobs. We don't believe in laying off employees. Period. And that includes AI. If AI allows us to operate more efficiently then maybe the rate of growth in our employee count will slow down, which will help the expense ratio. But it won't come at the expense of people. Thank you. Now I would like to turn it over to Lou. Louis Iglesias - President of Allied World Thank you, Brian. Great to see everybody. It's good to see so many of you, I only get to see once a year and talk about our businesses here at Fairfax and at Allied. And it's also not every day that I feel like Allied World has won the Stanley Cup. So we're really proud of that as well. Brian mentioned our underwriting profit. We did have a record year last year on underwriting profit. We also had a high watermark on our net income. And I just want to recognize the investment group at Fairfax, who does a tremendous job on our portfolio. Having that type of net income really helps our cash flow and everything else. So, it's really, really good to see. We grew our company to $7.4 billion last year. And Brian talked about the market a bit. It is softening some. I would say it's getting a little bit more price competitive. But for those of you who've been with our industry for a long time, it's not a traditional soft market. We're not bottoming out. Terms and conditions are holding pretty well. Combined ratios don't have so much pressure on them, still manage the profitability. There are opportunities around the world to be able to get some growth. So we're not giving up on that because I think there are certainly some opportunities. What I wanted to talk about just for a couple of minutes is what are some of the things that we do to help us manage the cycle. We feel like we've built a company that could perform in all segments of the cycle. And in order for that to happen, we have to execute on many strategies every single day. The company has to be structured in a way to give us that ability. There are a couple of things in there. The first thing to talk about is the structure of having a very flat organization. You see that elsewhere in Fairfax. We have a very flat organization at Allied. We don't have many layers. So strategies and communication moves quickly. This gives us the opportunity to move fast in different marketplaces around the world. So as the markets change, we can change strategies. We can execute on those strategies. Our underwriters are at the desk since there's not lots of layers. They don't have to get multiple sign-offs to do their job to able to make a decision. We run with the mantra of hire really great people. And give them the authority and accountability to be able to get the job done. Additionally, we have product diversity – over 40 products. We are in 29 offices around the world – 11 countries and 4 continents. We're expanding our presence around the world geographically. So, the earnings stream is very diverse. And when we have that type of diverse earnings stream it really limits earnings volatility. So when the market starts to get a little bit tougher, it's really helpful to have different earnings streams because you may have to slow some down. If you're not getting the marketplace that you like in a certain product or a certain country, you're going to have to slow that down, but maybe there's an opportunity someplace else. So the diverse earnings stream is really very helpful. And I think you see that throughout Fairfax as well. The third thing that I would touch on is underwriting discipline. Underwriting discipline helps in every marketplace, whether it's a hard market, soft market in the middle. It's extremely important. It runs through every Fairfax company. It's part of the culture of Fairfax. Now what does that mean really? Our underwriters understand rate adequacy, they understand when they're negotiating a deal, where that rate crosses the line to not being enough for the exposure that they're taking on. When we run into that situation, we have the ability to say no. We say no a lot more than we say yes. But what we really prefer to do is to say, "No, we don't like the deal that way, but we do like it this other way. And we'll put a proposal out that works for us, and we hope works for the client. And we've been able to do business like that and sell deals like that fairly often, even in this marketplace when things are getting just a little bit softer. So that's been very helpful. Now nothing works without great people. And every year, I come up here, and I think I talk about how great the people are at Allied. We've had people with us for a very long period of time. They've seen all different cycles, so they understand how to manage in and through the different cycles. And we have a very low attrition rate at the company. So our people are really the key to making all the strategies work. And so for us, we're going to continue to do the things that we're good at. As the markets soften some, we're going to limit our mistakes so that when the market does get to a better place, we can do all the things that Andy talked about that we did a couple of years ago and not have any distractions. Thank you very much, everybody. Have a great day. Silvy Wright - President of Northbridge Financial Good morning, everyone. First, I'll start with a little confession to Lou. Northbridge employees wanted to do a Rory McIlroy (repeat as winners of the Athappan Cup), but we are happy that Allied World won this year. First a little perspective on Canada. Northbridge represents the Canadian insurance operations for Fairfax. With $3.4 billion in revenue, we're the third largest commercial insurer in Canada. We have a very good position - maybe a smaller fish at Fairfax but a bigger fish in this country. What are market conditions? What happened in '25, as Lou said, the price competition really started to ramp up. And we're starting to see competitors trying to buy business. And sorry, I apologize for being a broken record, but once again, we are not pressured to write premium at a loss. And so, in 2025, our employees did the right thing. They remained disciplined, not only in underwriting but claims and expense management. But equally important, we doubled down on really focusing on customer loyalty, customer service and customer safety. So not only be there when things go wrong, but we're trying to help our customers have safer operations. As a result, we did not grow in 2025. However, we did have a record year, as Brian noted. In 2026, it looks like the price competition continues and we will manage accordingly. Along with just being disciplined, we're also looking at building areas where we can grow when it's the right time to grow. For instance, increasing our lines on renewable energy in Canada. So just manage the market and then be ready to go when it's time. And one more comment. We talked about the culture many times and the beautiful word of being empowered not just at the president level, but throughout the company. I just wanted to share with you that our employees are like you, they're shareholders. Over 70% of our employees at Northbridge are shareholders. So not only are they empowered but they're owners in doing the right thing. Thank you. V. Watsa - Founder, Chairman & CEO Thank you very much Silvy. Peter, anything to add, final words, on the insurance industry? Peter Clarke - President & COO Sure. Just two quick things, Prem. And I mentioned in my remarks that we write $33 billion of premium across the world and that grew by 2.3% this year. It's interesting when you look at the international operations and how we benefit from diversification and scale. Bryte in South Africa grew 20% this year, Colonnade 18%, Asia was up 15% and Polish Re was up 15%. And so even though North America rates are coming down, we're maybe not growing as much, we have all these opportunities around the world. Secondly, I just have to comment that we have 2 cups in Fairfax. One is the Mr. Athappan Cup. And we also have a hockey game between the Fairfax head office and the Allied World Group, and unfortunately, now Allied owns both cups for this year and I have to say it did come into the evaluation process a bit, but we left that aside.

-

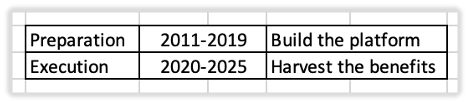

Article 6 - the final article in our 6-part series on Fairfax's insurance business. Why Fairfax's Insurance Platform Is Built to Last Insights from Fairfax's 2026 AGM In a previous article, we reviewed Fairfax's insurance transformation from 2014 to 2025. That story was told through financial results. Net premiums written increased from $6.1 billion to $26.3 billion. Float more than tripled. Most importantly, shareholders participated in that growth on a per-share basis. The increase in size is easy to see. It is evident in Fairfax's reported financial statements. What is less well understood is how much the quality of the insurance franchise has improved over the past fifteen years. Record underwriting profits are one visible sign of that improvement, but the real story lies beneath the numbers. The 2026 Annual General Meeting provided compelling evidence of that transformation. Rather than focusing on financial results, investors heard directly from the executives who built and now operate Fairfax's insurance business. Although each spoke from a different perspective, together they described the same underlying system: a decentralized organization built around exceptional people, disciplined underwriting, and long-term thinking. Understanding both changes—the growth in scale and the improvement in quality—is essential to understanding Fairfax today—and why the company's insurance business has never been better positioned for the future. Prem Watsa: It Starts with People Prem Watsa opened the discussion by talking about acquisitions. But he was not really talking about acquisitions. He described Markel (Canada) as Fairfax's most important acquisition because it established the company in the property and casualty insurance business. He then identified Skandia America Re as his second most important acquisition—not because of the business itself, but because it ultimately led to Andy Barnard joining Fairfax and building its global insurance operations. As Watsa explained: "The best one is Markel Insurance because otherwise you're not in the P/C insurance game. And the second best was a small company called Skandia America Re... because it brought Andy Barnard to Fairfax." It was a classic Prem Watsa answer. Fairfax's greatest asset is not its float, investment portfolio, or insurance subsidiaries. It is the people running them. That theme ran throughout the AGM and provided the foundation for everything that followed. Andy Barnard: Fifteen Years of Preparation Andy Barnard then provided perhaps the clearest framework for understanding Fairfax's recent success. Looking back on his fifteen years leading Fairfax's insurance operations, Barnard divided the period into two distinct phases. From 2011 to 2019, Fairfax prepared for future growth. The company acquired Brit and Allied World, expanded internationally, strengthened leadership teams, and built the organizational capabilities needed to compete on a global scale. The second phase began in 2020. With the platform in place, Fairfax was positioned to capitalize on a hardening insurance market. Premium volume nearly doubled, underwriting profits surged, and years of preparation translated into exceptional operating results. Barnard summarized the period this way: "The first period, from 2011 to 2019, was a period of preparation... The second period, from 2020 to 2025... we virtually doubled our premium volume, and our underwriting profit more than quadrupled." Exhibit 1: Andy Barnard's Framework Barnard's framework also helps investors better understand the insurance cycle. Hard markets create opportunities, but only companies that have spent years preparing are positioned to capitalize on them. Fairfax's insurance franchise was built before the hard market arrived. The hard market simply revealed its strength. Brian Young: The Message for Today If Barnard explained the past, Brian Young focused on the present. His message addressed investor concerns about a softening insurance market. Fairfax remains committed to underwriting discipline. There is no pressure on operating companies to write business simply to maintain premium growth. Growth matters, but profitability matters more. As Young stated: "There's no pressure on any of our companies to write for top line growth." This helps explain why growth has recently slowed across parts of Fairfax's insurance operations. Management is deliberately choosing underwriting profitability over market share. For long-term shareholders, that is exactly the right decision. Lou Iglesias: How Discipline Works Lou Iglesias of Allied World provided a clear illustration of Fairfax's decentralized operating structure. Authority is pushed down to experienced underwriters. Decisions are made close to the customer and close to the risk. Underwriters are trusted to exercise judgment—including walking away when pricing becomes inadequate. Iglesias summarized the philosophy simply: "Hire really great people and give them the authority and accountability to get the job done." Rather than relying on centralized oversight, Fairfax relies on capable people supported by clear accountability. It is the practical application of the philosophy Prem Watsa described at the beginning of the discussion. Silvy Wright: Discipline in Practice Silvy Wright showed how that philosophy works in practice. Northbridge did not pursue premium growth aggressively in 2025. Instead, management maintained underwriting standards while competing through customer service, claims management, relationships, and helping customers improve safety. Growth slowed. Results remained strong. As Wright explained: "We are not pressured to write premium at a loss." For investors, this illustrates an important principle. In insurance, slower premium growth is not necessarily a sign of weakness. It can be evidence of underwriting discipline. Peter Clarke: The Benefits of Scale Peter Clarke concluded the discussion by highlighting one of Fairfax's greatest competitive advantages: diversification. Today, Fairfax operates across numerous geographies, products, and markets. When pricing weakens in one area, capital can be redirected to more attractive opportunities elsewhere. As Clarke observed: "Even though North America rates are coming down, we have all these opportunities around the world." This flexibility is one of the lasting benefits of building a global insurance platform. What Investors Learned An earlier article documented Fairfax's insurance transformation through financial results. The 2026 AGM explained how those results were achieved. A consistent picture emerged. Fairfax's success was not simply the product of a favorable insurance market. It reflected years of preparation, disciplined capital allocation, decentralized decision-making, and an unwavering commitment to underwriting profitability. More importantly, the AGM demonstrated that Fairfax's insurance business has become better—not just bigger. Over the past fifteen years, the company has assembled an exceptional leadership team, strengthened its underwriting culture, expanded into attractive global markets, and built a decentralized operating model that empowers talented people to make disciplined decisions close to the customer. These improvements are structural rather than cyclical. Insurance pricing will inevitably fluctuate over time. Premium growth will accelerate during hard markets and slow during soft markets. Those cycles are outside management's control. The quality of Fairfax's people, its underwriting discipline, its decentralized operating model, and its global platform are different. Those are enduring competitive advantages that should persist through multiple insurance cycles. The financial statements tell investors that Fairfax has become much larger. The 2026 AGM explained why it has become much stronger. Understanding both changes is essential to understanding Fairfax today—and why the company's insurance business has never been better positioned for the future.

-

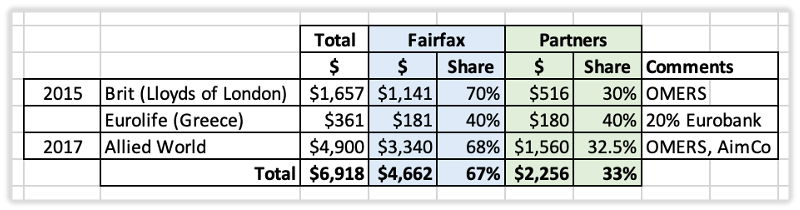

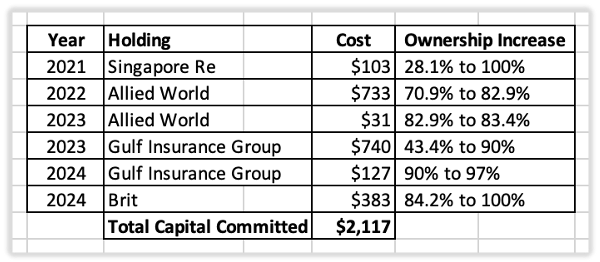

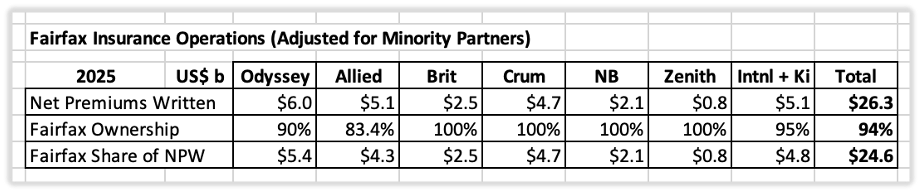

Article #5 in our 6 part series on Fairfax's insurance business. Let me know if I got the high-level description of the call option feature correct. Partnerships: An Underappreciated Growth Strategy Previous articles explained how Fairfax built one of the world's largest property and casualty insurance groups through disciplined acquisitions, strong underwriting, and organic growth. Another important contributor has received much less attention: partnerships. Over the past fifteen years, Fairfax repeatedly partnered with long-term investors to accelerate the expansion of its global insurance platform. Rather than funding every acquisition itself, management shared ownership of selected businesses, allowing Fairfax to acquire interests in more high-quality insurers than it could have using only its own capital. The strategy evolved over time. Partnerships initially maximized the size of Fairfax's insurance platform. As internally generated capital accumulated, Fairfax increasingly used that capital to increase its ownership of those same businesses. Together, the two phases illustrate one of Fairfax's more innovative capital allocation strategies. Phase One: Building the Insurance Platform By the early 2010s, Fairfax's acquisition strategy had evolved. Rather than focusing primarily on distressed insurers, management increasingly targeted higher-quality insurance businesses. These acquisitions required substantially more capital but also offered stronger long-term growth prospects. At the same time, Fairfax's equity hedging program reduced internally generated capital available for acquisitions. Partnerships helped solved that problem. By investing alongside long-term partners, Fairfax could pursue larger opportunities without relying solely on its own balance sheet. Fairfax generally used two partnership models. In some cases, it acquired control immediately. In others, it acquired a significant minority interest and patiently waited for the opportunity to obtain control. Although structured differently, both approaches pursued the same objective: long-term ownership of outstanding insurance businesses. Model 1: Controlling Partnerships In some transactions, Fairfax acquired control immediately while inviting partners to invest alongside it. Fairfax sourced the opportunity, negotiated the acquisition, and remained the controlling shareholder. Its partners—primarily Canadian pension funds—provided part of the required equity. Brit and Allied World are the best examples. Exhibit 1: Fairfax – Model 1: Controlling Partnerships The three largest transactions required almost US$6.9 billion of capital. Fairfax invested approximately US$4.7 billion, while partners contributed US$2.3 billion. As a result, Fairfax controlled almost US$7 billion of insurance acquisitions while providing only about two-thirds of the required capital. Accounting Implications Because Fairfax owned more than 50% of these businesses, it consolidated 100% of their premiums, assets, liabilities and operating results into its financial statements. Economically, however, Fairfax owned less than 100%. The partners' share of earnings was reported separately as non-controlling interests. Model 2: Strategic Minority Investments Not every opportunity required immediate control. Sometimes Fairfax acquired a significant minority interest while another shareholder remained in control. Rather than insisting on ownership from day one, management built a long-term relationship, learned the business and waited patiently for the opportunity to acquire control. Singapore Re and Gulf Insurance Group illustrate this approach. Fairfax was comfortable sitting in the passenger seat until the opportunity arose to move into the driver's seat. Exhibit 2: Fairfax – Model 2: Strategic Minority Investments Fairfax initially acquired a 28.1% interest in Singapore Re in 2009 and a 43.4% interest in Gulf Insurance Group in 2010. In both cases, Fairfax eventually acquired control years later. Accounting Implications Because Fairfax initially owned between 20% and 50%, these investments were accounted for using the equity method (share of profit of associates). As a result, their premiums, underwriting results and float did not appear in Fairfax's reported insurance operations until control was obtained. The different accounting treatments help explain why the economic impact of Fairfax's partnership strategy is not always obvious from the financial statements. Phase Two: Increasing Economic Ownership By 2021, Fairfax had entered a new phase. Years of disciplined underwriting, a strong insurance market, improving investment income, and substantial operating cash flow began transforming the company’s financial position. Fairfax was generating far more capital internally than it had a decade earlier. Rather than buying new insurers at significantly higher valuations, management began increasing its ownership of businesses it already owned. Between 2021 and 2024, Fairfax committed approximately US$2.1 billion to buy out partners in four existing insurance businesses. Singapore Re: increased ownership to 100% Brit: increased ownership to 100% Gulf Insurance Group: increased ownership from 43.4% to approximately 97% Allied World: increased ownership from 70.9% to 83.4% Exhibit 3: Fairfax – Insurance Partners Bought Out (2021–2024) The strategy had evolved. Initially, partnerships allowed Fairfax to build a larger insurance platform than it could otherwise have afforded. Now they allowed Fairfax to increase its ownership of the underwriting profits, investment income, float, and long-term value generated by that platform. Why Investors Miss the Economics The accounting creates an interesting paradox. During the first phase of the strategy, controlling partnerships immediately increased Fairfax's reported premiums, underwriting results, and float because those businesses were fully consolidated. During the second phase, buying out minority partners produced no change in those reported operating measures because the businesses had already been consolidated. Instead, the benefit flowed directly to Fairfax shareholders through increased ownership of the earnings those businesses generated. The insurance platform did not become larger. Fairfax simply owned more of it. That distinction is easy to overlook. Many investors focus on premium growth when evaluating insurers. Viewed through that lens, buying out minority partners appears to accomplish very little. Economically, however, Fairfax increased its ownership of businesses already producing substantial underwriting profits, investment income, and float. The growth shifted from the top line to the bottom line. For long-term shareholders, that is what ultimately matters. Controlling Partnerships: The Call Option Advantage The controlling partnership model contained another important feature: call options. When Fairfax negotiated these transactions, it secured the right to purchase its partners' interests in the future using valuation frameworks established at the time of the original investment. What is a call option? "A call option is a financial contract that gives the buyer the right, but not the obligation, to purchase a specific stock or asset at a predetermined price (the 'strike price') before a set expiration date. Buyers pay a fee, called a 'premium,' for this contract." — Investopedia What makes a call option valuable? "The primary benefit of holding a call option is the right, but not the obligation, to buy an asset at a set price before a specific date. This allows you to profit if the asset's market price rises, while strictly limiting your total potential loss to the initial cost paid." — Investopedia The same principle applies to Fairfax's controlling partnerships. The best time to acquire insurance businesses is typically during a soft insurance market, when underwriting results are weaker and valuations are generally lower. The most expensive time is often near the end of a hard market, when strong premium growth and improved underwriting profitability have increased earnings and driven valuations materially higher. Many of Fairfax's partnership agreements were negotiated during a soft insurance market. The call options established valuation frameworks at that time. Since then, one of the strongest hard insurance markets in decades has materially increased underwriting profits, earnings, and the value of high-quality insurance companies. The practical effect is significant. Fairfax can increase its ownership of certain businesses today while paying prices based on valuation frameworks negotiated during a soft market. In effect, management has the opportunity to acquire larger ownership interests in high-quality businesses at below-current market valuations. For shareholders, the call option feature transformed what initially appeared to be a financing arrangement into a long-term capital allocation advantage. What Remains? Fairfax is approximately half way through the process. Between 2021 and 2024, Fairfax increased its ownership of Singapore Re to 100%, Brit to 100%, Gulf Insurance Group to approximately 97%, and Allied World to 83.4%. By 2025, Fairfax economically owned approximately US$24.6 billion of its reported US$26.3 billion of net premiums written. Minority partners now account for only about US$1.7 billion, or roughly 6%, of reported premiums. Exhibit 4: Remaining Minority Interests (2025) The largest remaining minority interests are Allied World and Odyssey, where Fairfax owns approximately 83.4% and 90%, respectively. These businesses represent the largest remaining opportunity to increase Fairfax's ownership of an insurance platform it already controls. What Have We Learned? Fairfax's partnership strategy was much more than a financing tool. It was an innovative capital allocation strategy designed to exploit the insurance cycle. During the soft market, partnerships allowed Fairfax to acquire substantially more high-quality insurance businesses than it could have financed using only its own capital, when valuations were most attractive. As underwriting profits, investment income, and operating cash flow strengthened, management shifted to the second phase of the strategy—using internally generated capital to increase its ownership of those same businesses rather than acquiring new insurers at much higher valuations. The call option feature made the strategy even more powerful. By negotiating the right to purchase its partners' interests using valuation frameworks established years earlier, Fairfax positioned itself to increase ownership after one of the strongest hard insurance markets in decades while effectively paying soft-market prices. The accounting makes the economics easy to miss. Partnerships initially increased reported premiums because controlled businesses were fully consolidated. Later buyouts produced little change in reported premiums, but materially increased Fairfax's ownership of underwriting profits, investment income, float, and future earnings. Viewed across an entire insurance cycle, this is classic Fairfax: patient, creative, unconventional, and long term in its thinking. Management built flexibility into the original transactions, waited for the economics to become highly favourable, and then deployed internally generated capital when the opportunity was greatest. The result was a larger insurance franchise, greater economic ownership for common shareholders, and another meaningful contributor to long-term per-share value creation.

-

Pretty good talk about the history of AI:

-

Good article, I'm curious how it plays out. I agree that free market is a most powerful force, and have faith in Adam Smith's model. Uncompetitive companies must close or improve, and a crisis is often helpful to overcome long standing inefficiencies. Companies which are successful for too long become stagnant. The question is how predatory pricing and massive state intervention works out for a nation of 1 billion people. China has a good shot for long term success, but it hasn't won yet. The last empire with state control over economy and industry was Soviet Union, and it failed badly. China allows quite a lot of free market besides state control, so here is innovation. China does hostile moves not only against Germany and Europe, but also against USA, South Korea, Japan, Taiwan, Israel and others. Together those countries could easily organize and compete.

-

Hard to ignore that this is going downhill for Russia ,even for those living in Moscow. They are importing fuel from India: https://youtu.be/WvgIQV45tEo?is=5lddlfyPJsnwhU9o

-

The metric that I'd be really looking at for BTC is input cost(electricity, hardware, etc) per bitcoin/price of a bitcoin. When the input cost is greater than cost to mine(aka the incentive to keep the "most secure and powerful decentralized computer network" running), that network will have the incentive to now turn itself off. That means entities with large amounts of resources (e.g. North Korea, NSA, CIA) can control that network to siphon the BTC off inconspicuously while running trick play on their propaganda machines to mitigate any appearance of abnormalities until it can not longer be hidden. When that happens, BTC will be as worthless as any other cryptocurrency. The trends in AI compete with BTC in very similar type of resources, and if AI really gains widespread adoption, it may be the thing that actually kills off BTC. If I were holding a lot of BTC, I'd put a healthy dose of resources into AI just to hedge.

-

You keep kidding yourself Richard - and keep telling me that your armed Antifa rioters and shooters were exercising their rights to "Free Speech". I can't help it you are delusional.

-

Since we discussed authoritarism here is a specific issue, since Antifa was brought up. Antifa literally Means Anti fascist which to my knowledge not illegal. It’s not an “organization” either. There is no Antifa leadership. It’s a loose term for left organization and typically small groups that have little if any coordination that range from those who do throw Molotov cocktails to college student groups who demonstrate on the college grounds. How this is designated a terrorist organizations shows how far we have drifted off to authoritarian side here. Declaring an organization a terrorist organization based on nebulous associations is done by intent to scare people and now creates the perception of an enemy within - a very old autocratic scare tactic. Say what you will about free speech in Europe, but I don’t think this would be possible. https://www.whitehouse.gov/presidential-actions/2025/09/designating-antifa-as-a-domestic-terrorist-organization/

-

lol , I know, and all those policies have been bad for Europe and good for everyone else.

-

Elites at the World "Economic" Forum have been saying tariffs are always bad while also firmly embracing "Green" ideology. China seized the advantage of their foolishness and European industry paid the price.

-

Berlingske - Commentary column - Samuel Rachlin [July 4th 2026] : Putin seeks way out, but is entangled, stuck in a war that keeps his utopia about Russian greatness and triumph alive [subscription protected] - - - o 0 o - - - Attached : 1. Article translated to English language by the use of Google Translate, 2. Article in Danish language, source for 1. - - - o 0 o - - - Note : Translation is far from perfect, I have only fixed the header here in this post, by posting the column header. - - - o 0 o - - - The whole situation is absolutely depressing to think about - I personally have a hard time to see a feasible alternative to just continuing the warfare activities, with continued massive losses of human lives. *sigh* Berlingske - Samuel Rachlin - Putin søger en udvej men er spundet ind i en krig der holder liv i hans utopi om Ruslands storhed og triumf - Opinion - English - 20260705.pdf Berlingske - Samuel Rachlin - Putin søger en udvej men er spundet ind i en krig der holder liv i hans utopi om Ruslands storhed og triumf - Opinion - Danish - 20260705.pdf

-

Only include dvidend and interest, less withdrawals to live on, as you are measuring the change in unleveraged capital. Use time weighted return. To double capital in 10 years you need around a 10 yr CAGR of 10% (72/10 + 2.8% inflation). For an RRSP/RRIF, substitute the higher of the minimum withdrawal required, or the amount drawn to live on. SD

Only include dvidend and interest, less withdrawals to live on, as you are measuring the change in unleveraged capital. Use time weighted return. To double capital in 10 years you need around a 10 yr CAGR of 10% (72/10 + 2.8% inflation). For an RRSP/RRIF, substitute the higher of the minimum withdrawal required, or the amount drawn to live on. SD -

they need to apply tariffs to protect their industry

-

Probably, about politics, I am the only on this site thinking that right, left and center are the same thing... I will not be very popular but basically this is how I see politics...