All Activity

- Past hour

-

It is a good thread every year to discuss the best ideas for the year. But right now everything changes so fast, therefore it is after the first 6 month of the year a good time to think about the choices from the start of the year or to discuss new ideas which starting to get interesting in the last months. New ideas for me. I was very optimistic about nintendo at the start, it is still a great company but with a lot of question marks after the last months, the management is not good. I bought Netflix and Microsoft the last days. Amrize still a big idea. Mgm was a big idea at the start and then came the buyout proposal. Exor was a big holding, i was frustrated before and then came the Luce, i sold all. in the last months i bought a few times S&P Global. What are your thoughts? New ideas? or comments on your picks from the start of 2026

- Today

-

"singer Parastoo Ahmadi and eight other musicians who were each sentenced to 74 lashes, a two-year travel ban and two-year ban on artistic activities. Their sentences relate to a live-streamed 2024 concert in Qom province where Parastoo Ahmadi performed unveiled in a sleeveless dress" Why would someone root for such a country to win?

-

Great quote from a great player! I'd not heard that one....

-

I was watching Algeria-Austria. Rooting for not getting a tie, so Iran can advance. The last 5 min I gave up as they were just bouncing around. Switched to Argentina and Jordan. Only to switch back after the surprise Algeria goal that brought Iran back, only to lose it again after Austria did the impossible. Iran had two offsides that in my books should have been goals. Anyhow at least Canada advanced today and will face off either the Netherlands or the Moroccans.

-

Flamingo‘s over Russia, love to see it: Check out what they look like- it’s a cheap jet engine (pulse jet) strapped on a rocket and payload body. It’s basically a V1 with GPS.

-

Insurance - The Engine That Drives Fairfax

SafetyinNumbers replied to Viking's topic in Fairfax Financial

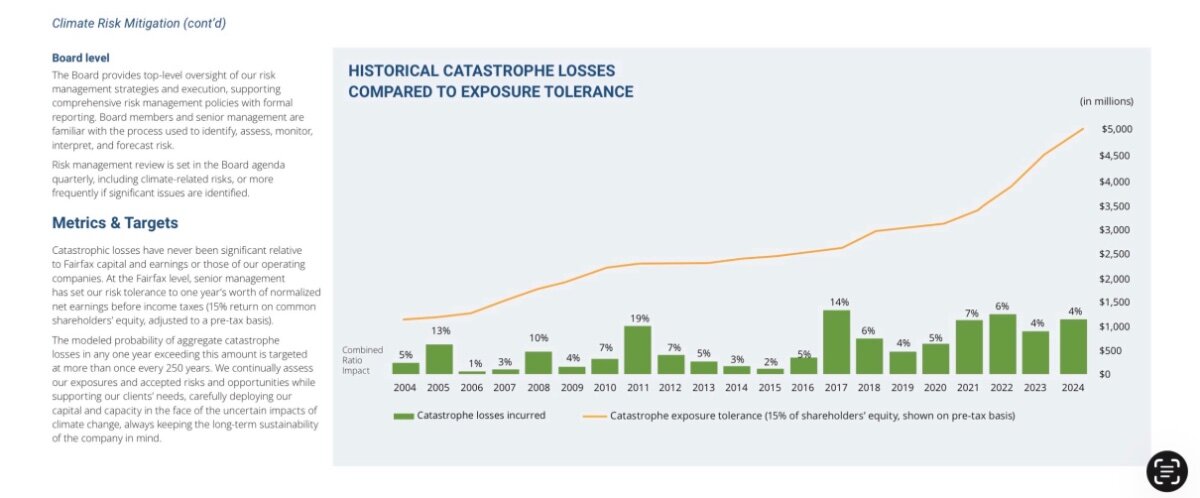

The way it was described to me is they took the pricing but didn’t expand coverage so cat has shrunk as a percentage of total premiums. This chart in the 2024 Climate report shows how far away cat losses are from 15% shareholder’s equity and that the gap is getting wider. This means if there is a really bad cat, we’ll be able to write a lot of business at great prices and premium growth will accelerate. I think this will lead to multiple expansion as quant buyers will show up. This is another “free” option in the Fairfax story that investors assign a discount to and not.a premium which would be more appropriate.

-

Nothing wrong with CNBC itself, even the mighty Buffett watches it in the background with mute on. I usually run Bloomberg TV on low volume when I work from home. So there is value in them. But think of them as distribution channels rather than content creators. For instance CNBC has 98% market share of anything Berkshire. Great content through the same exact pipeline that also bring Lousy Joe from Squawkpod. There are however key differences between CNBC and Bloomberg. The former caters to domestic business news while the latter caters to international/global news. You can watch Bloomberg TV at 2 AM and it will be aired via HK. On newspaper side, WSJ caters to domestic business news while FT/The Economist cater to global news. So I don’t see this as CNBC fault or a MAGA thing. This is just Joe acting like a child. That kind of behaviour is unacceptable.

-

Eventually, Germany, France and other states will have to adopt air conditioning because these temperatures are way higher than they used to be and also for longer in many summers. Good business for air conditioning and heat pump manufacturers potentially.

-

I'm now convinced that Blake is simply trolling the forum, posting nonsense and laughing as people respond seriously to try to set him straight. But you went too far with this one. Bravo... fooled me for a long time.

- Yesterday

-

Fairfax’s insurance business is much larger. In recent years, its exposure to catastrophes has come down a little. More resilient: At the same time, the dramatic increase in Fairfax’s earnings (and sources) is important. Additionally, Fairfax has been building additional resilience into their business model: the significant increase in non-insurance consolidated holdings in recent years. I think looking to the ratings agencies (specifically AM Best) can provide another helpful take… they have increased Fairfax’s ratings twice in recent years. Lots of positive developments. It is encouraging.

-

Insurance - The Engine That Drives Fairfax

SafetyinNumbers replied to Viking's topic in Fairfax Financial

A large cat would hurt near term BVPS growth but probably result in multiple expansion that would more than offset it. Long term they will get it back anyway, -

He's right. IDK why no one can understand nuance anymore. He punches it up but all he's been saying with a few short exceptions is that it's risky so adjust your allocation to ex US, tilt value, and some other assets consistent with your plan/risk perimeters. Kernen has been a clown since at least the 90s.

-

Thanks @Maverick47 for going back to the annual report for the catastrophe risk. Reading it again I can how complex it would be to come up with a framework for each insurance company to sustain such of an event.

-

Yeah, it was very hot, here. Next week it will get better. I bought an air condition for my working room in the garden house 2 weeks ago. It is a No-Brainer! Fully tax deductable and it cools in the summer and heats in the winter and is working with electricity from solar panels. Mitsubishi Electronics seems to make the best products.

-

-

Insurance - The Engine That Drives Fairfax

Maverick47 replied to Viking's topic in Fairfax Financial

This is an important question for any insurer, @Hoodlum. The company has set risk management guidelines for this risk that are disclosed each year in the annual report under note 22. From the 2025 Annual Report: Catastrophe risk Catastropheriskarisesfromexposuretolargelossescausedbyeitherman-madeornaturalcatastrophesthatcould result in significant underwriting losses. Weather-related catastrophe losses are also affected by climate change which increases the unpredictability of both frequency and severity of such losses. As the company does not establish reserves for catastrophes in advance of the occurrence of such events, these events may cause volatility in the levels of incurred losses and reserves,subject to the effects of reinsurance recoveries.This volatility may also be contingent upon political and legal developments after the occurrence of the event. The company evaluates potential catastrophic events and assesses the probability of occurrence and magnitude of these events predominantly through probable maximum loss (“PML”) modeling techniques and through the aggregation of limits exposed. A wide range of events are simulated using the company’s proprietary and commercial models, includingsinglelargeeventsandmultipleeventsspanningthenumerousgeographicregionsinwhichthecompany assumes insurance risk. Each operating company has developed and applies strict underwriting guidelines for the amount of catastrophe exposure it may assume as a standalone entity for any one risk and location, and those guidelines are regularly monitored and updated. Operating companies also manage catastrophe exposure by diversifying risk across geographic regions, catastrophe types and other lines of business, factoring in levels of reinsurance protection, adjusting the amount of business written based on capital levels and adhering to risk tolerance guidelines. The company’s head office aggregates catastrophe exposure company-wide and continually monitors the group’s aggregate exposure. Independent exposure limits for each entity in the group are aggregated to produce an exposure limit for the group as there is presently no model capable of simultaneously projecting the magnitude andprobabilityoflossinallgeographicregionsinwhichthecompanyoperates.Currentlythecompany’sobjective istolimititscompany-widecatastrophelossexposuresuchthatoneyear’saggregatepre-taxnetcatastrophelosses would not exceed one year’s normalized net earnings before income taxes. The company takes a long term view and generally considers a 15% return on common shareholders’ equity, adjusted to a pre-tax basis, to be representative of one year’s normalized net earnings.The modeled probability of aggregate catastrophe losses in any one year exceeding this amount is generally more than once in every 250 years. The bottom line is that the company models the aggregate amount of multiple potential catastrophe events occurring anywhere around the world in a given calendar year and currently estimates that the likelihood that this amount will exceed 15% of common shareholders equity (roughly $3.9 billion on an after tax basis, or about $5 billion on a pre-tax basis, given 12 2025 shareholder equity of $26.3 billion) is less than 0.4%. This risk management guideline then essentially would appear to have the goal of turning aggregate catastrophe losses, those expected to occur more rarely than once every 250 years, or with a probability of less than 0.4% in any calendar year, into an income statement event, not a balance sheet event. We probably should also keep in mind that the company regularly records catastrophe losses around the world which are being charged for in their annual premiums and which cover the average annual level of catastrophe losses expected over the long term. I don’t know what the average number is, but I think 2025 cat losses were $1.2 billion, and the company recorded a combined ratio of 93% with pre tax underwriting profit of $1.8 billion. So a $5 billion pre tax year for catastrophes would appear to be only $3.8 billion pre tax above the actual 2025 result. Since the pre tax earnings in 2025 exceeded $3.8 billion, this appears to indicate to me that if 2025 had been the year with $5 billion in pretax catastrophe losses, the company would still have reported positive earnings of around $1 billion or so. Between cash on hand and short term securities, the company looks to be situated well to handle such a year. -

Check out my comprehensive 13F / Mutual Fund trackers (alphafiling.com)

Morgan replied to gym97's topic in General Discussion

Nice! -

Oh totally. If you go outside places like NYC, LA, etc people are friendly, trustworthy, and in general of significantly higher quality.

-

My strategy is to live in Europe, but have a portfolio of mostly US stocks. Best of both worlds.

-

I hate to say it, but I think a lot of the good career people have left or were forced out, and it's a rubber stamp operation now. The prior Chairman, Pham, fired or suspended a lot of enforcement people who she had a grudge against. The current chairman is undoing a lot of prior crypto enforcement cases and giving industry whatever they want. Rather than 5 Commissioners from both parties, there is only one, Selig, and he isn't an industry veteran like Gensler, who ran Goldman's asian offices. He's a guy, 10 years out of law school, who was not very high up at the SEC but was more pro crypto than Quintenz (Commodity Ken Doll), and didn't have a beef with the Winkelvii. I left before this administration took office because it sucked the last time Trump got elected and 1) I didn't want to spend the next four years undoing what I did the prior four years, 2) I had a feeling this time would be worse, and 3) the pro-fascist anti-immigrant stuff is too much for me. I have family members who have been tortured or killed for opposing dictators in Latam, and I'm not going to be a part of it here. I could've stayed, gotten close to the action and left to work for one of the new grifters, but I don't want to get rich that way.

-

Thanks @Viking for these great write ups on float and the impact on growth. I am sure you will include this in a future article but a larger float also increases risk during very large Cat events. Fairfax’s international and multi-line growth will certainly help to mitigate this better than in the past but I am curious how a 1 in 100 or 400 year hurricane event would impact Fairfax. How much cash should the US insurance subs and Fairfax keep on hand for such an event.

-

Wife is from Iran, came over in '79 after the revolution. We were rooting hard for them......and they were 92% likely to make the final 32 yesterday morning. Now they are out, thanks to the Algeria - Austria tie (both of whom advanced). Argh! Iran- who went undefeated - somehow is one of the 16 bounced?

-

@dealraker Next week my wife and I are going to Llandudno, which is in Conwy County, for 8 days, then by train up to the Aigas Field Centre in the Highlands for 10 days, followed by flying to London for two days. We also like being in small places and interacting with the locals. The whole point of going to London was so that I could visit the Royal Institution and I just found out the Ri will be closed when we are there , which it wasn't when we booked the trip. I'll call them tomorrow to see if there is anyway I can get a special tour.

-

-

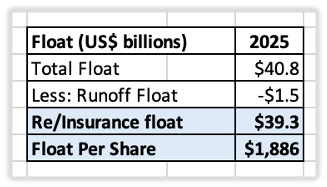

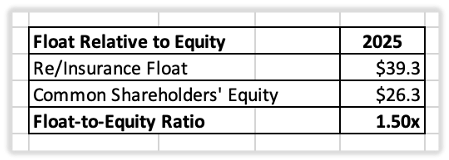

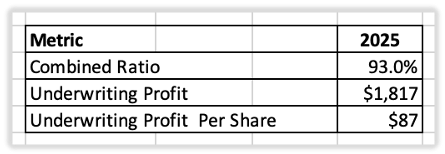

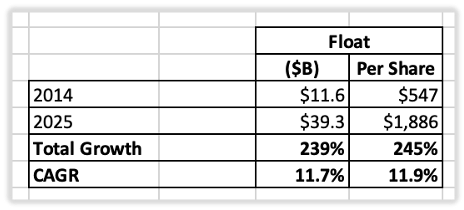

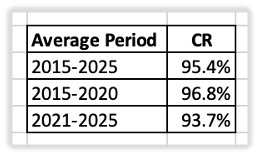

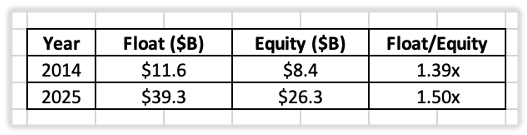

Article 2 in our series on Fairfax's insurance business Applying Buffett’s Float Framework to Fairfax In the previous article, Warren Buffett explained that investors should focus on three factors when evaluating an insurance company: The amount of float the company generates. The cost of that float. The long-term outlook for both. Let's apply Buffett's framework to Fairfax. Size: Fairfax Has Significant Float Warren Buffett's first test is simple: how much float does an insurer have? At December 31, 2025, Fairfax had total float of approximately $40.8 billion. For the purposes of this analysis, two adjustments have been made. First, runoff operations have been excluded. Runoff float has different economic characteristics than float generated by Fairfax's ongoing insurance and reinsurance businesses and is best analyzed separately. Second, Fairfax does not own 100% of certain subsidiaries, including Allied World and Odyssey. As a result, a portion of the float generated by those companies is attributable to minority shareholders rather than Fairfax shareholders. To keep the analysis simple and consistent with Fairfax's reported figures, no adjustment has been made for minority interests. After excluding runoff operations, Fairfax's insurance and reinsurance businesses generated approximately $39.3 billion of float, or about $1,882 per share. Exhibit 1: Insurance & Reinsurance Float Breakdown (2025) Fairfax has built a substantial float base. Before considering shareholders' equity, the company controls nearly $40 billion of investment capital generated by its insurance operations. Economic Significance: Float Exceeds Shareholders' Equity The size of float is important, but its significance becomes clearer when compared to shareholders' equity. At year-end 2025, Fairfax's common shareholders' equity was approximately $26.3 billion. Compared to insurance and reinsurance float of $39.3 billion, Fairfax's float-to-equity ratio was approximately 1.5x. Exhibit 2: Float Relative to Shareholders' Equity (2025) This means Fairfax had approximately $1.50 of float supporting every $1.00 of shareholder capital. Put differently, float was 50% larger than the equity supplied by shareholders. This is what makes float so valuable. When managed properly, it allows an insurer to control a substantially larger investment portfolio than shareholders' capital alone would support. Fairfax's investment portfolio is therefore funded not only by shareholders' equity, but also by a large pool of insurance float that has been built over decades of underwriting operations. Buffett's first test is therefore easily met. Fairfax has built a large and economically significant float base. Cost: Better Than Free Buffett's second test is the cost of float. Exhibit 3: Fairfax's Cost of Float (2025) In 2025, Fairfax reported a combined ratio of 93.0%. The company generated underwriting profits of approximately $1.8 billion while holding $39.3 billion of float. Viewed through Buffett's framework, Fairfax's float was better than free. Instead of paying to access this capital, Fairfax was paid to hold it. Trend: Growing Float Buffett believed the long-term trend was the most important factor of all. A large amount of float is valuable. A growing amount of float is even more valuable. Exhibit 4: Fairfax Insurance & Reinsurance Float Growth (2014–2025) From 2014 to 2025, Fairfax's float grew from approximately $11.6 billion to $39.3 billion. On a per-share basis, float increased from $547 to $1,886. This represents compound annual growth of approximately 12% over the past eleven years. Growth alone, however, is not enough. Buffett's third test also considers the long-term cost of float. Exhibit 5: Fairfax Combined Ratio (2015–2025) Fairfax delivered an average combined ratio of 95.4% from 2015 to 2025. The record includes years with elevated catastrophe losses. More importantly, underwriting performance has improved in recent years, with the average combined ratio declining from 97% in 2015–2020 to 94% in 2021–2025. Many insurers can grow float by sacrificing underwriting profitability. Others maintain underwriting discipline but struggle to grow. Fairfax accomplished both. Over the past eleven years, float increased by 245% while underwriting remained consistently profitable. Growing float is valuable. Growing float at a negative cost is even more valuable. A Fourth Question Buffett's three questions provide an excellent framework for evaluating an insurance company. I would add a fourth: How important is float to the business model? The answer depends on the relationship between float and shareholders' equity. The larger the float relative to equity, the greater its potential impact on shareholder returns. At year-end 2025, Fairfax's insurance and reinsurance float was approximately $39.3 billion compared to common shareholders' equity of $26.3 billion. Float was about 1.5 times larger than equity. Exhibit 6: Float Relative to Equity (2014 vs. 2025) What makes this particularly noteworthy is that the relationship has remained remarkably consistent over time. In 2014, float represented approximately 1.39 times shareholders' equity. By 2025, the ratio had increased modestly to 1.50 times. This means Fairfax has not only grown its float; it has preserved its importance within the business model. Despite substantial growth over the past decade, float remains larger than shareholders' equity and continues to provide meaningful leverage to shareholder capital. This distinguishes Fairfax from Berkshire Hathaway's evolution. As Berkshire grew into one of the world's largest companies, shareholders' equity expanded much faster than float, reducing float's relative importance over time. Fairfax has followed a different path. Insurance remains the foundation of the business, and float remains one of its most important competitive advantages. Buffett's Scorecard Viewed through Buffett's framework—and the additional question regarding the importance of float—Fairfax performs well across every measure. Float is large. Float has grown consistently over time. Float has been obtained at a negative cost. Float remains a significant contributor to shareholder returns. Individually, each characteristic is impressive. Together, they describe a valuable insurance franchise. Over the past eleven years, Fairfax has grown float from $11.6 billion to $39.3 billion, maintained profitable underwriting throughout that growth, and preserved the importance of float to its business model. Few insurers have accomplished all three simultaneously. Buffett's framework was designed to identify insurers with durable economics. By that standard, Fairfax appears to possess one of the strongest float franchises in the property and casualty insurance industry.