glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

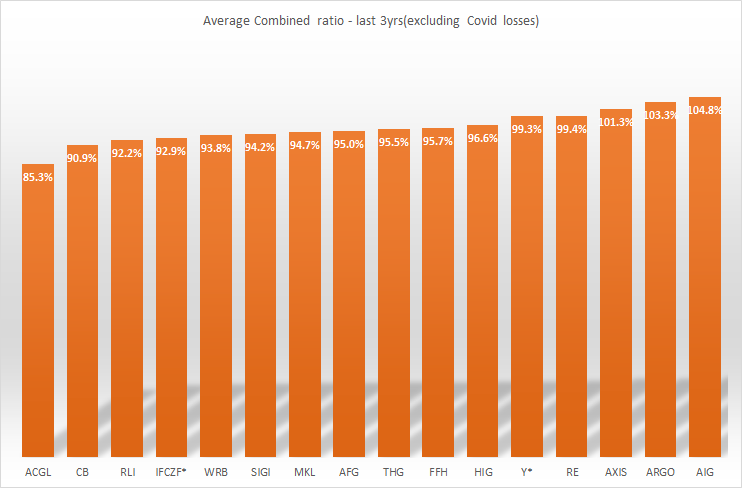

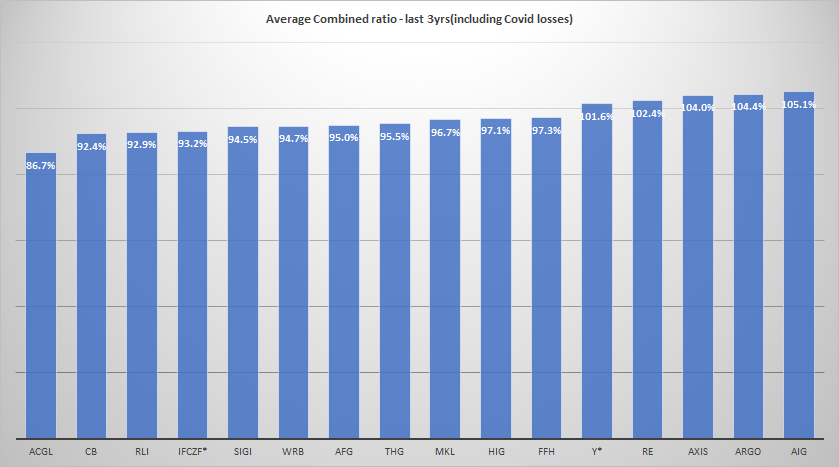

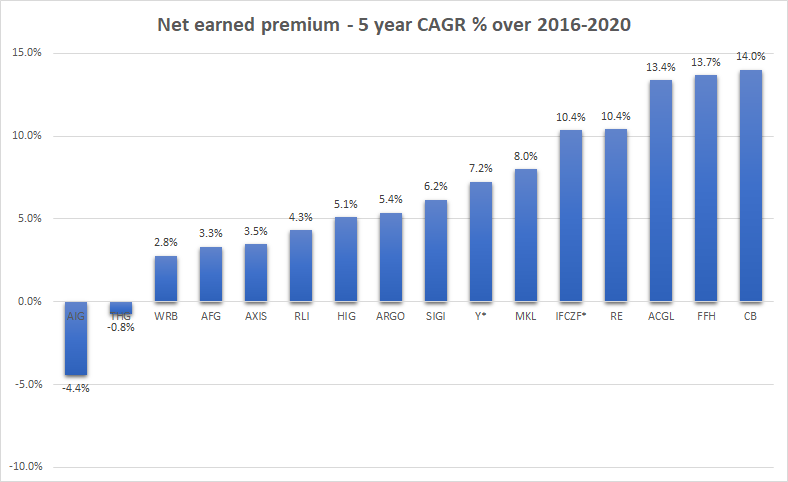

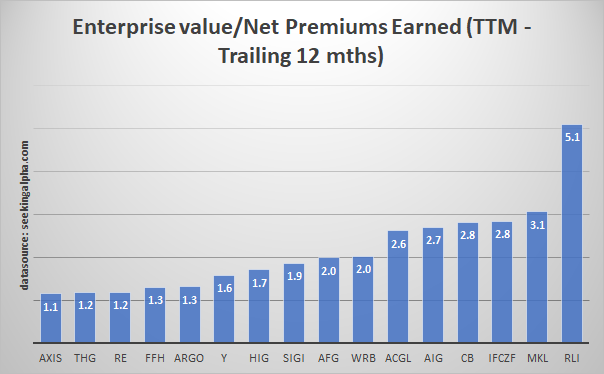

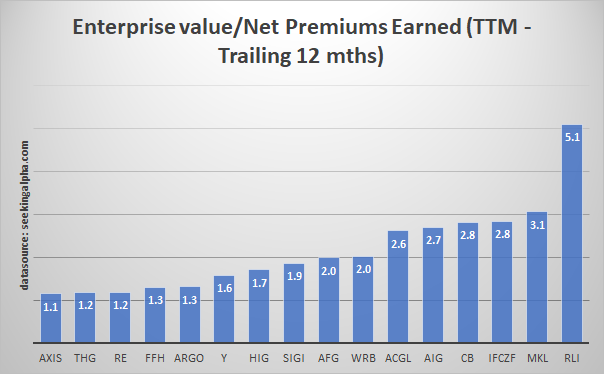

I think this might be an under-appreciated part of Fairfax - underwriting profit & growth rate - is a function of both the combined ratio & the net earned premium growth rate. I have put some more charts together - 1. combined ratio I have done two charts, sourcing data from sec.gov comparing Fairfax to 15 insurer peers - making estimates where insurer is not disclosing the % point impact on combined ratio from Covid. (note below as well that ACGL's combined ratio is skewed lower due to its mortgage insurance business that has a much lower combined ratio than P&C ops) Fairfax's has averaged a combined ratio (excluding covid losses) of 95.7% over last 3 years (2018-2020) which is close to, albeit slightly above, peer group median of 95% and less than its peer group average of 96.6%. (note this combined ratio is only for Fairfax's consolidated insurance ops which represent around 88% of its GWP) Next the combined ratio if we include impact of covid losses on combined ratio - Fairfax is sitting at 97.3% which is above Peer median of 95.5% but below the peer average of 97.8%. Assuming covid losses continue to fall, I would expect Fairfax's combined ratio (excluding covid losses) is probably a better proxy moving forward. 2. Net earned premium growth Sourcing data from seeking alpha - appears that Fairfax appears to be growing net earned premium faster than majority of its peers on a 5 year CAGR% (however, note that Fairfax's net earned premium growth includes positive impact from Allied World acquisition in 2017) Looking at trailing 12 mths ending 30 June 2021, Fairfax's net earned premium growth looks high again relative to peers From the above, Fairfax's underwriting profit (looking at combined ratio) on each $1 of earned premium appears to be close to peer median, but Fairfax looks to be growing its net earned premium at a faster rate than many of its peers. Yet on an enterprise value to net earned premium multiple - Fairfax looks to be cheap at 1.3 x its net earned premium, which is a large discount to its peer median of 2.0 x . I have put this chart up before, but including again to illustrate Further, this net earned premium multiple above is based on consolidated net earned premium & excludes impact of net earned premium from Fairfax's non-consolidated subs (GIG, Digit).

-

Kamesh Goyal is estimating they can get to an annualised run-rate of 6,500 crore (approx US$850 mil) in GWP by Oct-22 & expects to cross the 2% market share. Looks like they grew approx 4x faster than the rest of the industry in 1H FY22 https://economictimes.indiatimes.com/industry/banking/finance/insure/digit-insurance-eyes-rs-6500-cr-in-premia-sales-by-october-2022/articleshow/87081261.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst Fairfax-promoted Digit Insurance is confident of taking its premia sales to over Rs 6,500 crore when it completes five years of operations in the next October, a top official of the Bengaluru-based general insurer has said. While the industry grew 16-17 per cent in the first half, Digit has grown over 67 per cent to Rs 2,196 crore, driven primarily by the health segment, Goyal said. "Going by the company's faster growth rate so far at close to Rs 2,200 crore in premia sales in the first half of FY22, we will easily cross the FY21's Rs 3,243 crore with a minor profit which was crimped by the pandemic claims," Goyal said. He added that given a high base, "I hope to scale past Rs 6,500 crore with premia sales by the time we enter the sixth year of operation next October". Goyal expects to cross the two per cent market share by then, from the current 1.68 per cent of the over Rs 2.2 lakh crore as of June 2021.

-

thanks nwoodman re Digit capital raise Q. How is your solvency ratio looking like? It was 180 as of June 30. After the approval of the recent capital raise I would expect it to be more than 300 by December 31. It will be one of the highest in the industry. Hoping the approval should come sometime this month and we will close the transaction within thirty days. from Q2 2021 results as previously reported, upon closing of the Digit Insurance equity issuance in the third quarter, and upon final approval by the Indian government of its previously announced intention to increase foreign ownership limits, we anticipate recording an additional gain of approximately $1.4 billion or $46 in book value per basic share.

-

thanks Viking!

-

Agree Viking I just watched the interview - interesting to hear from investor psychology perspective that there are shareholders out there who 'bought in the 600s'' and who now might be just looking to cut their losses - that negative sentiment is obviously going to affect the share price which creates opportunity for others. I think maybe it does further highlight maybe the need to Fairfax to better articulate their value proposition and their approach to capital allocation/investment framework to fund managers who maybe have limited time to get their 'sound bites' from companies they are interested in investing in.

-

no worries Viking - I agree the set-up looks excellent for Fairfax. Mr Market just doesn't agree with us at the moment but agree its just being patient. I was actually thinking about this for the last few days I knew I wanted to do a peer comparison & share it with everyone here, but I wasn't sure how to get the data easily. I would have probably preferred to use NPW but NPE data was bit easier to get my hands on. I wanted to show visually how cheap I felt Fairfax was versus its peers (not just in terms of P/B) but in terms of the size of the insurance business relative to Fairfax's current market valuation. I just worked out yesterday that Fairfax's net earned premium in the first 6 mths of 2021 was 23% the size of Berkshire's - so its getting pretty big! And thats just their consolidated net earned premium so excludes non-consolidated investees like Digit. Also when you look at above charts, first chart showing EV/Net Premiums Earned - two insurers that have 1.2x versus Fairfax at 1.3x - namely Everest Re & Axis Capital both have been running combined ratios over 100% - so their insurance businesses are not as profitable as Fairfax - so when you start to weigh up these qualitative factors it gives even more colour to Fairfax's relative valuation advantage over peers IMO. Yep I think the catalysts are now there in terms of insurance & investment performance & they need to show consistency to earn that multiple re-rating. Unless we get a pretty big market correction or major shock to the economy & we need to re-set our expectations, I agree the set up looks great for Fairfax. -

-

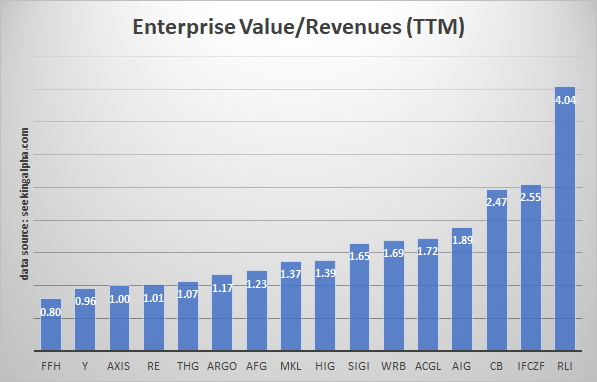

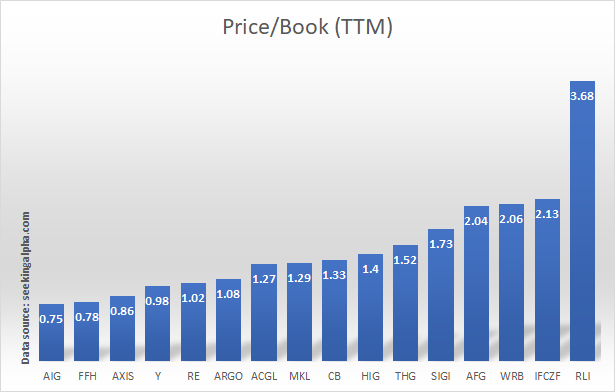

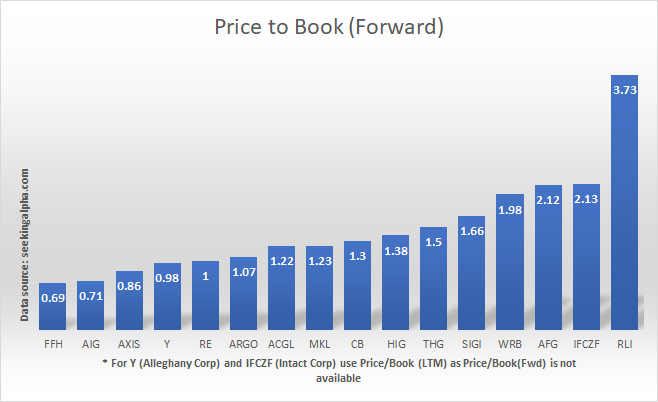

following on from this comment I have put together a few charts using data I sourced from seeking alpha - again I have tried to be careful with data but if any mistakes I apologise - as always please do your own due diligence Cheers! So I am comparing Fairfax to 15 of their insurance peers using data from 13/10/21. Just looking at valuation from a couple of different angles EV to net earned premium EV to revenues Price to Book Not considering other valuation measures such as combined ratios, premium growth, business mix, bvps growth rate expected etc but these are all relevant to valuation - we have talked about these on this forum. First chart - enterprise value to net premiums earned (side note on FFH - this reflects net earned premium that is consolidated & doesn't include their non-consolidated subs including Digit, Gulf Insurance etc) Now comparing enterprise value to last 12 mths of revenues (incl investment income & gains etc) Next Price to Book (TTM) Next Price to Book (Forward)

-

cheers nwoodman

-

Fairfax appears mentioned but I don't have a sub https://www.theglobeandmail.com/investing/markets/inside-the-market/article-three-stock-picks-from-matco-financials-anil-tahiliani/

-

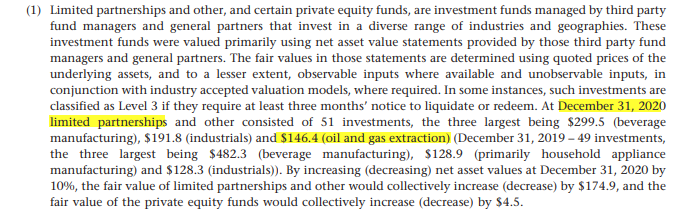

plus they have a bit more oil & gas exposure through their limited partnerships investment

-

https://www.fortuneindia.com/venture/we-knew-if-we-give-good-service-and-products-we-will-pull-through/106016

-

article on Eurobank The head of Eurobank underlined the very positive climate for the economy, the consolidation of the banks and the large amount of available funds for investments. https://www.businessdaily.gr/english-edition/50561_eurobank-ceo-greece-see-strongest-growth-sixties

-

interesting thanks Viking

-

omagh your calcs look wrong - they issued 5.1 mil shares at a 6% premium to BV to buy Allied World which effectively increased their BVPS by 1%, but you are suggesting they received a 20% approx boost to BVPS (4.6% compounded over 4 years) from issuing those shares. I would also say capital management & how you fund your business (with equity or debt) matters and I don't think BVPS growth that occurs, as result of buybacks or share issues, should be ignored when we evaluate performance. But I would probably agree that BVPS growth that is result of organic operating performance should be given a greater value weighting than BVPS growth that comes from equity issues at premium to BV. I think if you look across Fairfax's business in 2017 & compare it operationally/financial performance wise to 2021 you are comparing two different animals. Digit - 2017 had just opened its doors, in 2021 Digit was ranked for the 3rd year in the top 250 fintechs in the world. Atlas - 2017 first debt investment, over next 3 years 2022-2024 Fairfax could potentially receive a profit share (approx 47% stake unchanged) averaging around $280 mil based Atlas profit forecasts (below from Atlas Q2 21 presentation) on cash flows that are already contracted to their customers. From Mar-20 until now we have been dealing with a covid pandemic & just starting to get vaccination levels to a point where countries can start open up & get back to normal - this has had a huge impact on Fairfax's insurance underwriting and investments - the negative impact over next 4 years from covid will in all probably be a lot less So I think looking at the annual report & grabbing a few numbers & extrapolating that based on those numbers the next 4 years will look the same, without considering any of the business drivers (eg hard market, less impact from covid, investee performance etc) that will actually generate that BVPS growth, its unlikely to provide IMO the right insights you need to predict Fairfax's likely valuation/performance. Yes history matters but you need to put it in a context.

-

Digit Insurance, a general insurance company offering health, car, bike and travel insurance, has been named one of the top 250 fintech companies globally using technology to transform financial services by CB Insights, a US-based market intelligence agency. Digit is the only Indian insurance company featured in the CB Insights Fintech 250 list. https://www.apnnews.com/digit-an-indian-insurance-company-to-make-it-to-cb-insights-fintech-250-list/

-

Has anyone tried out Onlia to buy insurance? Onlia is digital insurer JV between Fairfax & Achmea https://www.onlia.ca/about

-

spek Its definitely a risk I think about - to what extent will withdrawing stimulus/higher taxes weigh on economy - we have had this sugar hit post covid (eg high commodity pricing) which has driven stock prices of commodity producers up a lot but we all know its unsustainable - we have to be mindful. On the other hand, we are just about to come out of lockdown in Sydney, people are going to start going to restaurants, travelling etc the economy here & globally has been hurt by delta but we are going to reach the end of that eventually . So thinking about all of this I see positives & negatives but yes if we relapse into recession this would hurt Fairfax. But I guess I come back to this question - in buying FFH now am I being compensated for these risks with the company, industry & economy. Its then a 'bird in the hand' argument. Fairfax is at a historically very low 2/3 of BV, do I sell now & pay tax (in my case its held under a year & would be in the 30% area), in the hope I can buy it back next year at an even lower price plus I have to be compensated for tax paid etc? It just doesn't make sense to me. A lot of financials are trading much closer to fair value than Fairfax & I am not interested in them. As well as P/B I also look at the total enterprise value/revenue ratio which ignores debt in comparing insurers. When I checked tikr this week Fairfax is in the mid 0.7 area & the avg was 1.1 but then you have specialty insurers on much higher levels- but then also you have to compare on other metrics like product focus, geographic focus - an insurer that operates exclusively in US - how comparable is this to Fairfax that has this significant international business with higher growth rates & insurtech investments in Digit, Ki Yes you can trade FFH - I am not a technical trader but I could see there was probably a double bottom reached last week & then you can see a series of higher highs & higher lows earlier in the week - basically enough momentum for technical traders to jump in to earn a couple of percentage points.

-

this might be reason for jump today https://timesofindia.indiatimes.com/india/india-to-issue-tourist-visas-from-october-15/articleshow/86854319.cms

-

Thomas Cook India & SOTC survey reveals Significant travel intent for last quarter 2021 https://www.equitybulls.com/admin/news2006/news_det.asp?id=299178 Also looks like shares up around 23% since 30 Jun-21 based on mid-day trade - not a huge position but a circa $45 mil or so bump Even though we are in a bull run caution is setting in. Is it time to skew the portfolio towards deep value stocks? Are you sensing this change in mood? Right now, we are seeing a return to normalcy in India. The economy is beginning to revive, unlocking is happening and therefore whether it is the hotel companies like Chalet, Indian Hotels or Thomas Cook, all these are certainly seeing a lot of bookings. When they report the next quarter, you would see really strong numbers. .. Read more at: https://economictimes.indiatimes.com/markets/expert-view/has-the-market-mood-shifted-in-favour-of-deep-value-stocks-chakri-lokapriya-answers/articleshow/86840374.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

-

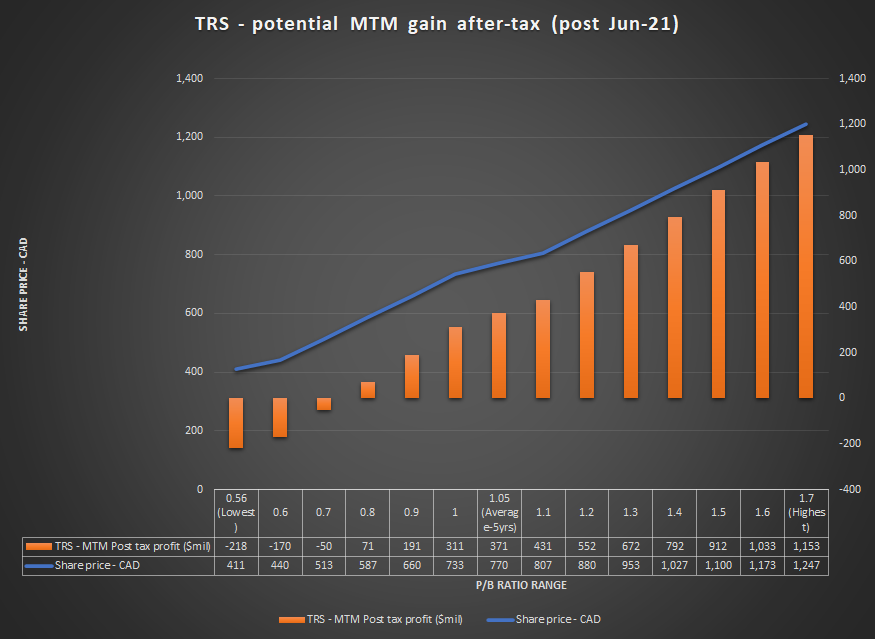

I would add that most of the time, valuation just becomes its own catalyst NYSE listing - is it really necessary? main reasons they gave were inconvenient, costly, US investors can buy on TSX anyway & doesn't impact their capital raising capability https://www.theglobeandmail.com/globe-investor/fairfax-financial-delisting-shares-from-nyse/article4215526/ Fairfax bought over 1.5% of their shares in last 12 mths but yes I would like to see hopefully more + bigger buybacks in future - the swaps are a synthetic buyback as well - fyi for those who are interested, here are my calc estimates if Fairfax returns to avg P/B in last 5 years, Fairfax will make around $370 mil after tax (@16.5% estimated tax - could change??) on these swaps (this is on top of any MTM gains up to 30 Jun-21) . Here are my estimates on potential return on swaps based on market price trading at different P/B ratios - hope its not too confusing Yes I am mindful they need to take advantage of monetising equity or wholly owned positions in an opportunitistic way this is something I am watching - RFP maybe they could have trimmed/ sold at $16 but I checked & apparently there is an analyst with an $18 price target on RFP & median price target of $16 - I haven't done a deep dive on this one but is it clear cut??. With BB the most they could have trimmed/sold at was around US$12.50 IMO - see my last post on reasons why. BB Is one I am more concerned about but in the context of everything else going on, at least BB is a smaller % of the overall pie now. On the flip side, there have been a lot of monetisations by Fairfax this year more so across their operating subs but still they are being opportunistic - Viking has done a good job covering these so no need to repeat.

-

I agree Viking - lets put BB in context - Fairfax are firing this year on so many fronts.

-

Also even though FFH was unable to sell - BB did have opportunity to raise capital at high price when meme stocks spiked - that would have benefited FFH -why didn't JC do it.

-

couple of things to jump in probably not saying anything new but - Prem implied that they would have sold BB in Q1 but couldn't due to an SEC rule & during the second spike this year (near US$15) it occured during a quiet period. - in renegotating the convertible debentures they brought down their average cost - they do have intent to exit BB but only at the right price. Fairfax investment team sold their BB positons in Q1 (Wade,Lace) - I don't think their methodology for investing in BB was wrong (JC had a good track record & BB had significant assets) at the beginning but sitting on it for such a long time was a big mistake - as gregmal said they have domain experience in insurance & so they have invested successfully in insurtech but they probably need a partner like a VC/fund/partnership specialist in tech investing to basically manage their tech investments outside of insurance like they do with property (eg Kennedy Wilson) - if BB had started off as a small position & stayed that way we probably wouldn't be talking about it much but it was a big, concentrated position & that is the issue. - it does raise issues around portfolio positioning (sector,geography) - how do Fairfax think about this in the context of their insurance liabilities - maybe I will submit this one to next AGM.

-

I think Fairfax see their AGM as their investor day - format was different this year with Covid - I went along time ago so not sure what the last 'in person' meeting was like. Yes agree would be great to hear their 5 year future plans for both insurance & investments also to hear from Wade Burton & other members of investment team. I agree that the website needs improvement (needs to be optimised for mobile so its easier for investors to use) & an IR email contact would be great. I did appreciate Prem answering 3 of my questions I submitted to this years AGM on Digit, the swaps & Blackberry - I am going to acknowledge that its not always easy for an individual investor to have your questions answered by the CEO directly.

-

so I think that would put FIH's stake of 1% on implied valuation of around US$234 mil versus carrying value of US$99 mil at 30 Jun-21 Calc total implied valuation 1.75 lakh crore = 1.75 tril INR USD/INR 74.77 USD 23.4 bil (FIH has 1% share) Looks like when they marked in June they might have applied a discount for lack of liquidity as unlisted - so so if the unlisted price has nearly doubled from 1750in March to around 3300INR-3500 they might mark up by around 80-100mil from 30 Jun-21 valuation - thats my guesstimate assuming they think that unlisted price is reasonable Cheers.