gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Immigration might be a drag on certain state and local economies but it is a positive for the national economy. Especially when you have labor shortages, low birth rates, undesirable demographic issues.

-

My biggest forward looking concern about inflation is a Trump presidency. Trade wars, tariffs, deglobalization, tighter immigration. I would add replacing Jay Powell if I thought the Federal Reserve had anything to do with inflation.

-

Bro, it's mission accomplished

-

(re: APD) - my friend works for their division that makes huge heat exchangers for LNG facilities down in Florida and that division is just killing it. Unfortunately it is a small part of the overall company. That division will build a lot of hydrogen infrastructure as well, but today it is primarily LNG.

-

Thanks for the post wondering. I am just a basic American know-nothing but I shared your post with my much smarter friend from Kerala and this was his reply: ------------------ I agree 100% about the standard of the airport. I had a chance to see it while I was there a year ago, and I was mindblown that this is an Indian airport. The new airports in Mumbai and Delhi are also apparently world-class, but I didn't see them, so i have to take the word of a 100mn people for it BJP will rule for the next +20 years for sure. They have a lot going for them. They are nowhere as corrupt, they have an understanding of the majority of the population, especially the Hindi-speaking, north Indian belt. They have a cadre system tied to the Hindu society that trains them young, and they are very active in rural India, college unions, temples, etc. The only other party that has anything similar is the Communist Party which is only relevant in 2 states. They have proper organization and structure for absorbing anyone, including from your opponents, with clarity about their future, and a way up. They are very intentional about avoiding bureaucracy and nepotism, which is hard to avoid in a developing country like India. Indian political system has always been rigged, but that does not mean the elections. For the first 60 years after Independence, it was rigged in the favour of the Indian National Congress, and now BJP has "unrigged" the system through several acts like demonetization - which hampered the black money funding that INC used to benefit from. In the absence of an official lobbying system like in the US, all funding is under the table. In addition, political power used to be exerted by goondas or criminals. Even religious minority groups used to be funded in the name of secularism but were criminal organizations for INC's benefit. Those groups have been dismantled by several goonda acts. The Kashmir/ Pakistan border was a contentious issue with such groups standing in the way of any development/ changes. BJP enabled the police/ army to dismantle such groups, flirting with human rights issues. Previous Indian political parties used to play politics with religion, favoring one over another to create divisions and also use them for votes. BJP is the party of the right, and transparent about what they are. They maintain that India is a country of Hindus as the name suggests (Hindustan) and the others are welcome. Previously, we used to call the country secular, as in the constitution. But, I also think most of the population were never of this belief, nor will be. This was only an idea among socialist elites who ran the country till India opened up the economy in the 1990s. None of this is surprising including what his Indian colleagues said. BJP has a much smaller presence in South India where Bangalore is situated as well. We have 6 different states speaking 6 different languages, who think their cultures are way different than northern Indians'. As I said very different from the Hindi-speaking belt. But they don't form a majority. All these states have different parties ruling them, who can't get along with each other, and hence a fractured opposition. The main reason why the BJP will rule for another 20 years is the absence of leadership, strong opposition, or a semblance of a nationwide structure/ organization that can build something to beat them. Modi and the leadership of the BJP are quite selfless in prioritizing the party, Hinduism, and the country in that order. People respect that and the lack of corruption and nepotism which the INC was notorious for. INC leader - leader of the opposition is the grand grandson of the first Prime Minister. Every generation in that family has gone on to become the Prime Minister. Most people have had enough. -------------------

-

These days he would call Greg not Warren. In the zirp years they might have just used a bank line but I think Omaha has been clear that they would prefer the subs come to BRK for cash instead of using high rate bank financing. Greg is the guy all of these CEOs are dealing with (except Ajit). I think he's doing a good job but not everyone is sold on the Greg Abel show.

-

Thanks for posting the article. Strange that they would say this out loud (I'm sure not uncommon but probably illegal) - "Forest River and Starcraft agreed to stop making school buses in 2020, when it acquired REV Group’s competing shuttle bus business."

-

Yeah, the Eurozone is now 5 consecutive quarters of essentially zero economic growth. But it's not a recession. Technically

-

No way!

-

I mean he does make it easy to tease him since he is also actively recruiting initial investors for his proposed macro hedge fund on twitter (don't think that would be legal over here in the states, no?). But Alfonso isn't so bad, he is correct about QT being completely sterilized and ineffective. (QE was basically pointless as well, although it probably tightened MBS spreads somewhat). But you are right, these guys on twitter all have something to sell ya. Except Bill (wabuffo)! Who gives away his best stuff for free

-

I'm not sure they need to replace Charlie's seat on the board. He wasn't an independent director and they already have two other vice chairmen. They can take their time if they do intend to nominate someone.

-

How to buy stocks in the London AIM market?

gfp replied to TorontoChaosTheatre's topic in General Discussion

Just to make sure I have this right, the approximate market cap of this company is something like $314m USD ? -

good post sweet - lots of wisdom here

-

More out with the old at Pilot - https://www.reuters.com/business/pilot-energy-business-president-marketing-chief-out-shakeup-2024-01-30/

-

How to buy stocks in the London AIM market?

gfp replied to TorontoChaosTheatre's topic in General Discussion

I'm curious what the idea is here. Is your thesis that the pipeline that transports oil from kurdistan to turkey will be reopened sometime soon or what? -

How to buy stocks in the London AIM market?

gfp replied to TorontoChaosTheatre's topic in General Discussion

Yeah, Interactive Brokers lists it as LSE, it doesn't appear to be difficult to transact in. Anyone that can execute trades on the LSE should be able to buy some. Or you could try the US OTC listed GUKYF if you can't get access to the LSE. I don't think you are going to find call options, LEAPS or otherwise. Be careful... -

How to buy stocks in the London AIM market?

gfp replied to TorontoChaosTheatre's topic in General Discussion

Interactive brokers seems to let me trade GKP in London with no problem, but obviously the market is closed so I don't know for sure. I am not in Canada though. Have you tried to place an order for the somewhat illiquid unsponsored ADR, ticker GUKYF on the US OTC markets? I don't think you will find listed options on this company but I'm not an expert in London market options. -

How to buy stocks in the London AIM market?

gfp replied to TorontoChaosTheatre's topic in General Discussion

Just to be clear, the ticker of the investment you are trying to make is GKP in London? Or that was just an example and you want to buy something more obscure? -

And remember also that "construction jobs" includes all of the infrastructure type jobs that are still ramping. The lady standing on the interstate holding a sign that says 'yield' and 'stop' is a construction worker. The huge federal spending on this stuff got pushed down to the states, where it sits for a while before making its way into the actual economy. There is a lag before that federal deficit stimulus shows up in a private construction company's pocket. And of course existing home sales being frozen out of the market is a huge tailwind for new construction. It is their primary competition. Mortgage rates have already peaked and are coming down. Large national builders can offer creative financing buy-downs for buyers. New construction is generally a lot more inexpensive to insure. Right there you have hit a number of the pain points for home buyers currently.

-

Yeah I thought the 2 & 20 line was lazy analysis as well. I am aware of the 1.5% on invested capital and .5% on uninvested capital plus 20% over a 5% hurdle language, but do we know if the 5% hurdle is annually compounding or just 5% over the last high water mark? At a lot of funds, when they have a hurdle rate and a high water mark - the hurdle doesn't compound annually if they don't exceed it. So the 5% annually you think you are getting "for free" turns out to be 5% over a multi-year period after a drawdown and isn't nearly what it sounded like. Does that make sense? An annually compounding 5% hurdle vs a simple 5% hurdle over the last high water mark.

-

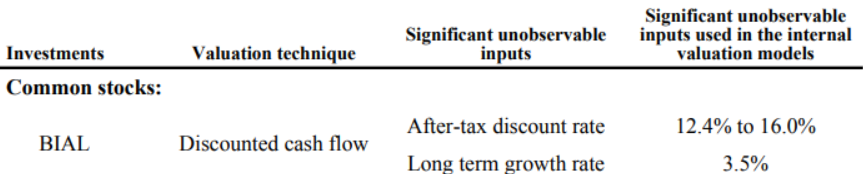

edit: This is the VIC post, not my own work. It seems like it was written by https://www.linkedin.com/in/rajpgokul/?originalSubdomain=in ---------------------------------------------------------------------------------------------- Description Fairfax India - Solid portfolio of investments available at a 40%+ discount to NAV ! Elevator Pitch: Fairfax India has a portfolio of growth businesses trading at reasonable valuations. The IPO of Bangalore airport (largest asset in the portfolio) would be a key catalyst in the next 2 years and will show how attractively it has been marked by the management. The fee structure is exorbitant (2/20 structure like a PE fund), but a mix of factors (entry discount, share buybacks, cheap leverage etc) will allow investors to get similar (if not better) returns as the underlying growth in NAV (~15% expected CAGR over the next 5 years). Investment Thesis: Fairfax India owns 59% of the Bangalore airport after the recent acquisition of 10% additional stake from Siemens. This is the crown jewel of Fairfax India and pretty much equates to 1.6 billion USD in value. This would translate into 85% of the current market cap and 54% of overall NAV/ Book value. Thus, a bet on Fairfax India is a bet on Bangalore airport, at least in the next 3-5 year time frame. Bangalore Airport: Bangalore Airport is an extremely attractive asset to own. I believe that the true discovered value of the airport in a domestic IPO process would be upwards of 4 billion USD compared with the management’s mark of 2.7 billion USD. The reason for the conservative marking of the asset would be due to the recent transaction of Fairfax India buying 10% stake from Siemens around these levels. In my view, Siemens was an uneconomic seller (they got this stake in return for building the asset in 2007) and Fairfax India was able to get an attractive deal for themselves. In 2019, Fairfax was able to sell part of the Bangalore airport to OMERS at a similar valuation to the current mark. The peer valuations of other Indian airports are 3X higher now than 4 years back. The Bangalore airport would have a rousing welcome in Indian markets and be bid up by domestic investors as high quality long duration assets which benefit from urban consumption growth are rare. Bangalore has been India’s fastest growing city for the last 2-3 decades (not only in India, but globally as well) and is well exposed to secular trends like technology, electronics manufacturing etc to drive further growth. The Bangalore airport has the concession until 2068 (almost 45 years from now). The airport when opened was far outside the city, but the city continues to develop towards the airport with multiple infrastructure projects to connect the airport with the city. The airport within the next 3 years would be well connected by Metro and Suburban trains in addition to the strong road infrastructure that has already been built. This is important as the airport has almost 460 acres of land that it can develop and lease. The airport has a regulated ROE of 16% on passenger fees and then unregulated income from retail, advertising, parking rentals, etc. Within the Indian airport space, Delhi was amongst the first airports that went to private hands. As per their last results, the regulated passenger revenue was just 1/3rd of the total revenues and the remaining 2/3rd was from unregulated sources (Land rental & retail - 33%, Duty Free & F/B - 19%, Parking & Ads - 6% and Others - 8%). This shows that an investment in the airport is a bet on the discretionary consumption trend of Bangalore. As India gets richer and more Indians travel and spend money on retail/ F&B etc, Bangalore airport will achieve higher operating leverage and profits will grow exponentially. That is a no brainer bet from a 10-20 year view (FWIW, I live in the suburbs of Bangalore and have absolute conviction on the city’s growth). The airport has been growing passenger volumes at double digit rate over the last 10 years and we can expect the same going forward as well. Bangalore airport is expected to achieve full capacity by 2030 with almost 90 million yearly passengers. To put that in perspective, London’s Heathrow in 2019 (pre-COVID peak) flew 80 million passengers. The city is expected to start searching for land for a 2nd airport within the next few years as it continues to grow (current population is 13 million people). The absolute valuation of 2.6 billion USD for Bangalore airport looks attractive from a general thumb check across similar assets in India and globally. The management uses the following conservative inputs to calculate their value. From the private filings of the Bangalore airport, the approximate data points are as follows: The airport opened its new Terminal 2 last year and that creates accounting entries that are difficult to normalise. Also, there are certain tax writebacks that make it difficult to analyse the true earnings power. Indian passenger traffic has smartly recovered from COVID and 2024 and 2025 should be good years for the airport. Public Equity Portfolio: Fairfax India has a public equity portfolio that as of today is equivalent to 1.25 billion USD. The major value in this comes from IIFL group and CSB Bank (almost 1 billion USD). We are bullish on IIFL Finance (largest position in our global portfolio and we own around 1.5% of the firm). The group is run by a wonderful owner-operator who understands capital efficiency and shareholder value creation. The stock trades at <10X earnings and 2.3X price to book with ROE and growth of 20%+. We don’t own CSB Bank directly, but it is a well run mid sized bank with a good management team that wants to scale up the business 10 fold over the next decade. The stock trades at 12X earnings and <2X book value with a healthy 18% ROE. The rest of the portfolio (IIFL securities, 5 Paisa, Fairchem Organics etc) are good businesses that are trading at reasonable valuations. There are no large valuation or growth risks that I see in their public portfolio. Private Portfolio: The largest allocations in the private portfolio outside of Bangalore airport are Sanmar (300 million USD) and NSE (176 million USD). Fairfax has investments in the holding company of Sanmar in line with the promoter family, but majority of the underlying value of the group is in the listed firm - Chemplast Sanmar. You can see from the market cap of the listed firm that the marking of the holding asset is reasonable. Fairfax’s indirect holding of the listed firm is approximately worth 220 million USD and the group has other large assets outside the listed firm in Egypt. Another way to check their valuation is that the pro-forma profit before tax of Sanmar for Fairfax’s stake was 39 million USD in 2022 (7.7X multiple on 2022 PBT). NSE is India’s largest stock exchange and should have a listing over the next few years. The exchange has been growing leaps and bounds with increasing equity participation in the country. It is a good asset that we should be happy to own for the next decade (marked at 19X 2022 earnings). The unlisted shares change hands currently at 25%+ higher than the valuation assigned by Fairfax team. The rest of the private portfolio is worth 350 million USD that is spread over 6-7 businesses. I don't have any strong views on them and are not material to our thesis. Valuation & other factors: The stock is trading at less than 60% of the underlying portfolio and I believe that is a large discount despite the high fee structure. The firm has been buying back shares (along with the parent Fairfax Financial) and the shares outstanding has reduced by 1.25% this year (they have retired 11% of outstanding shares in the last 5 years). I expect the share buybacks to accelerate as we get closer to the Bangalore airport IPO. The net debt is around 400 million USD, but has a 5 year tenure with 5% fixed cost. While the discount can theoretically widen even further from current levels, I believe that the current discount of 40% is on the higher end and the management can buy back shares aggressively if it persists (especially once the Bangalore airport listing gives them more liquidity). There are multiple levers of shareholder returns in Fairfax India - NAV compounding, discount narrowing, share buybacks etc. The biggest catalyst for the idea continues to be the expected IPO of the Bangalore airport. If the IPO doesn’t happen, then it is equivalent to paying a PE fund a 2/20 fee structure to get access to a good private deal (positive is that we are buying it at a 40% discount). So, the overall Risk-Reward looks attractive to us. I do not hold a position with the issuer such as employment, directorship, or consultancy. I and/or others I advise hold a material investment in the issuer's securities. Catalyst Bangalore Airport IPO, Share Buybacks

-

I don't know about land / farm prices being "cheap" in America. We have a family farm in Indiana (USA) and my Uncle is currently managing it. He told me a "medium quality farm in Indiana near our farm sold for $13,400 / acre recently." Now that price doesn't make sense to me for raw farmland at all. I see the financials, I know what the farm produces on average over time. There is tax. It just doesn't seem undervalued to me at all. Maybe somewhere else there is productive ag land that is much cheaper but $13,400/acre for Indiana farmland is just strange. I think @boilermaker75 has a similar farm in his family. Maybe he can chime in and tell me $13k is way off the mark and my uncle is smoking crack.

-

Thanks dealraker - nice to see BNSF take intermodal business from UNP.

-

Nice! I hadn't noticed it hit this morning. I love Fairfax dividend day. Something about getting it all at once that makes it seem like a lot.

-

I wonder how many people both purchase TIPS and criticize Buffett for holding his Coke shares - sure that he is missing something they get. (60 plus years of increases, .03 -> $1.84/sh during Berkshire's holding period)