gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

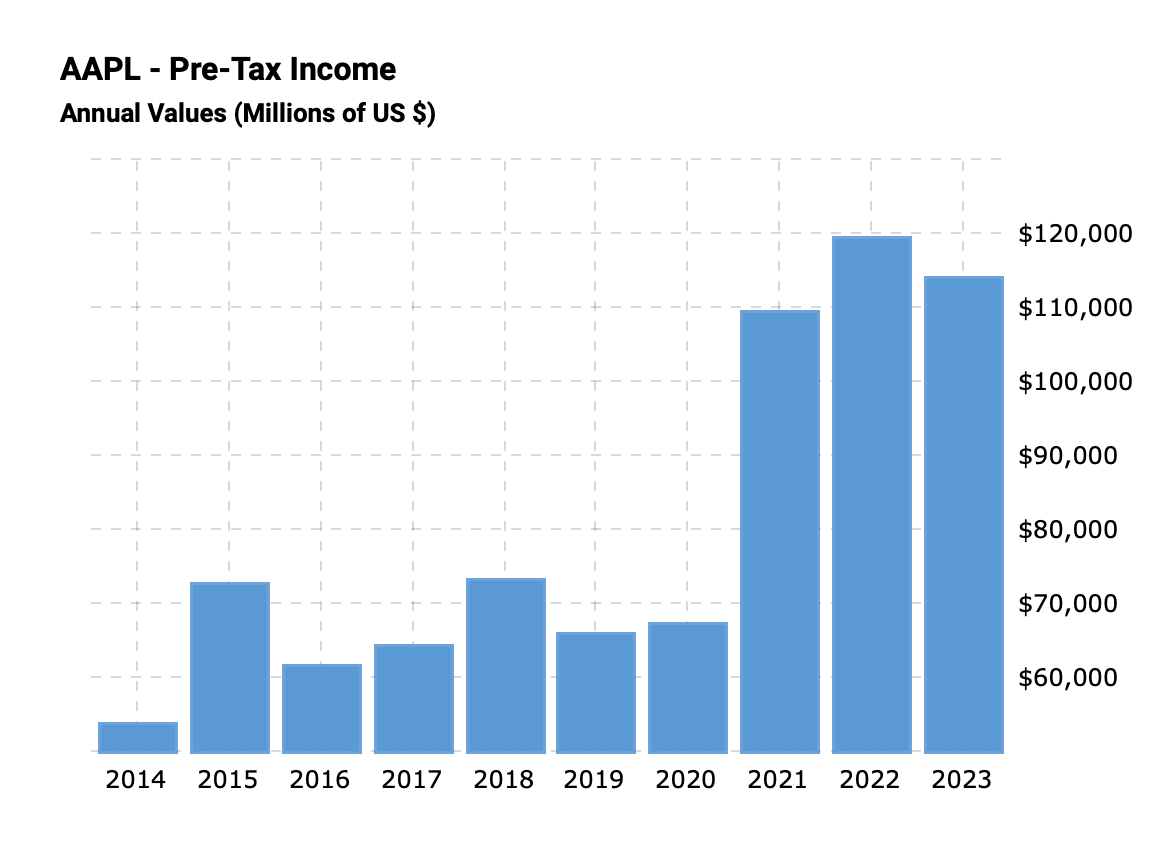

What are you talking about? https://www.macrotrends.net/stocks/charts/AAPL/apple/net-income And Revenues up 20% total over 9 years? Haven't they doubled? (while over 1/3 of shares retired) https://www.macrotrends.net/stocks/charts/AAPL/apple/revenue No wonder you guys think it's such a dog. Just remember that this company has returned $600 Billion in excess capital it generated and didn't need in its business in the last 6 years that Buffett has owned it. $600 Billion out the door and the market says what's left is worth $3T.

-

$825 Billion

-

I guess you folks are just going to be disappointed then

-

Sometimes it's just best to let Warren and Charlie explain it themselves -

-

Because number might go down on a brokerage statement? This isn't an options position. The company isn't going poof anytime soon.

-

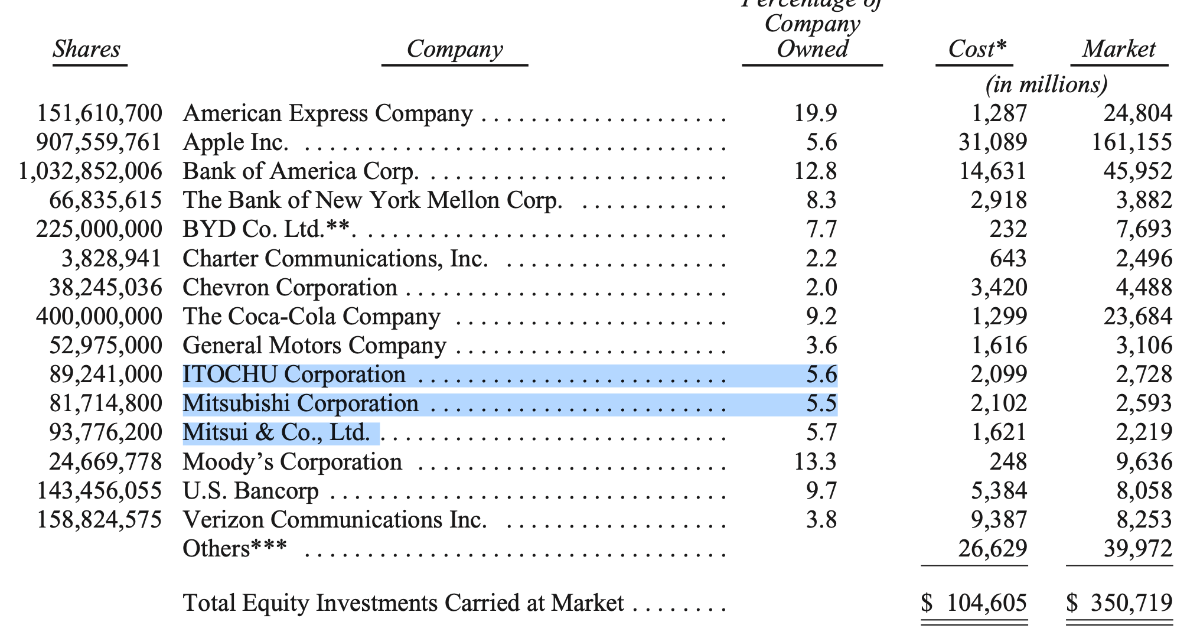

Well the fastest and surest way to destroy a bunch of money would be realizing a $140 Billion capital gain and paying the tax to the treasury. There goes $30 Billion that won't work on your behalf ever again. So now he's turned $177 Billion of Apple stock into $147 Billion in cash. Now what? He is not in any way constrained by his cash levels when it comes to buying back Berkshire shares currently. God forbid he invests the $147 Billion in a stock that might go down! Pretend this chart is the pretax earnings of a wholly owned Berkshire subsidiary like the Railroad or something. Pretend it's called Acme and Berkshire bought it in 2018 and it's doing well. There is no daily quote or capital gain or deferred capital gains tax, just a wholly owned subsidiary that is doing well. Would you think it was a problem? Would you need to IPO BNSF for $140 Billion in taxable cash tomorrow just because you could? Warren spends so much time with Ted and Todd discussing what really makes a good business. They are super rare and even rarer at size. Not easy to replace.

-

It's funny how much ink is spilled obsessing over Berkshire's "Apple problem!" Like an investment working out perfectly and (perhaps) getting ahead of itself is some kind of big problem. I don't think Buffett frets about the position being $177 Billion. I think the rest of Berkshire will continue to get larger and nobody will care about $177 Billion any more. The numbers are going to get larger. When Berkshire is allocating capital over a $2 Trillion asset base and Apple is 15% of it and still buying in shares and growing their dividend I don't think people will obsess over the insane 15% concentration. Imagine Warren makes a new public market investment with a $50 Billion cost basis this year. That would not be unexpected or crazy. You would hope it would work out and be a good investment. So you would have another huge $200 Billion problem to obsess over! Some things at BRK never change. #numberGoUp

-

BMO raises target price to C$1550 from C$1400

-

Man, looking back at the holdings he had before he closed down the first version of Praetorian, I haven't found a single holding that is even still publicly listed International Monetary Systems, Ltd International Commercial Television Inc Bingo.com Ltd Timberline Resources Group (still public at .047/share) DAC Technologies Group International, Inc There are no extra points awarded for degree of difficulty or obscurity in investing. Hopefully that is the lesson he learned from the first go round. He still dabbles in little shitcos like Surgepays, which isn't going anywhere long term but is scrappy and trying to exploit some government subsidy for poor people to get online on a cheap tablet. Praetorian's SURG position reminds me of his old style. (and I would be surprised if it still listed 10 years from now, much like the names above)

-

I thought that was a riff on the old line gun owners used?

-

according to my quote services, FRFHF did touch $1000 this morning.

-

I was traumatized by the fire, "PacifiCorp's Fire" " The latest verdict on behalf of nine victims includes damages for both economic losses and emotional distress. The company had already been found liable in the previous trial for failing to heed weather warnings and shut off electricity in its service areas ahead of a wind storm that toppled power lines. " “Each of them in this trial told you about the enduring trauma they had suffered because of PacifiCorp’s fires,” the attorney, Nicholas Rosinia, said Monday. “This is an extraordinary case full of extraordinary stories of survival and of bravery and of life-altering loss.” https://www.bloomberg.com/news/articles/2024-01-23/berkshire-fire-tab-grows-62-million-after-more-victims-testify?srnd=premium

-

There are definitely not any shares available to short

-

simultaneous all time closing highs in Berkshire & Fairfax - who'd of thought? The CoBF namesakes are holding up.

-

Brown and Brown results out, market likes it. https://investor.bbinsurance.com/news-releases/news-release-details/brown-brown-inc-announces-fourth-quarter-2023-results-including

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

gfp replied to twacowfca's topic in General Discussion

Who knows what Trump would have gotten done if COVID hadn't have come along. Once it did, Trump was checked out and Mnuchin was too busy and understaffed to handle much else. No indication so far that Mnuchin would come back for a 2nd Trump term so you have to wonder what kind of goofball cabinet he ends up putting together. I'm not even sure Kushner would come back and that would be kind of scary (to not have Kushner). -

Thanks DamienC. I looked at both your mash-ups. Just a suggestion - if you are going to post these regularly maybe just reply to your own topic/thread instead of creating a brand new thread with each post. I don't know about the self-promotion angle, but it seems to be free so as long as it stays free you might be OK there.

-

Q4 2023 was decent for Fairfax's 3.9m shares of Micron as well

-

He didn't really, but his fund had a drawdown

-

And then many years later the corroding usb sticks finally rusted through the Nord Stream pipeline and she blew?

-

Thanks. So very rich or very dead. Reminds me of the gold bugs that bury the gold in the back 40 but don't trust anyone with the information and die.

-

I am far from knowledgable about this stuff, but how possible is it that the key to access the "satoshi nakamoto" coins has just been lost and nobody has access to the coins?

-

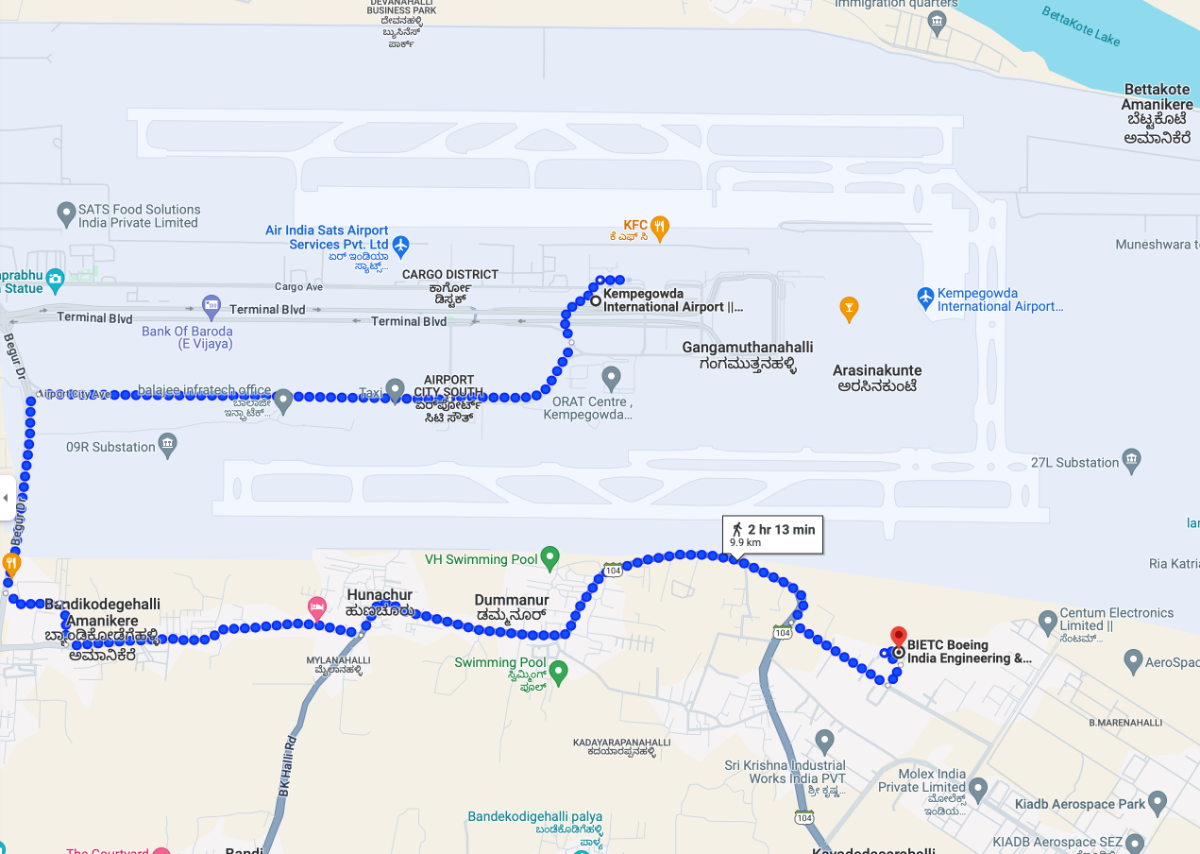

Modi recently inaugurated a new global engineering and technology campus for Boeing directly next to Kempegowda Intl. Airport in Bangalore. I don't think this is on land owned by Anchorage but it is directly next to the airport, which seems like another positive for the investment. https://timesofindia.indiatimes.com/india/pm-modi-inaugurates-boeings-largest-campus-outside-us-in-bengaluru/articleshow/106985702.cms?from=mdr&from=mdr

-

Three of them were already appearing the year before when he did include the top 15 table -

-

His US fund has a $5m minimum for new investors. Maybe some of the big guys or offshore investors could slide in. I think the "newsletter" product, KEDM, is primarily special situations, event-driven, arbitrage type ideas. It is a monitor of all the potentially compelling current event driven situations. I haven't seen many of these in his actual fund but he does allude to the event driven book in his letters. I don't know what the idea is behind KEDM, but if it helps pay the salaries of a team of researchers that are also working for the fund then there is something helpful there.