gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Sure - It is no surprise that utilities are permitted to pass the costs of mitigation to the customers. What we don't know (and I doubt) is that utilities would be able to pass liability judgements on to the customers ultimately. Mitigation is normal course of business. Multi-billion dollar liability judgements are another matter altogether.

-

That's interesting - I feel like some of Fairfax's trading / changes to holdings are not reflected in the 13-F that Dataroma uses. As an example, inside Odyssey Re (q3 NAIC filing) we see some Orla Mining purchases but also this purchase of Kennedy Wilson, where the 13-F shows no change in KW holdings during the quarter. (this chart is security, purchase date, source, number of shares, dollar cost paid)

-

Not sure if there is any interest here but for the curious, here is Odyssey Re's Q3 NAIC filing - tables on investments are towards the end. 23680.2023.P.Q3.P.O.3.4626988.pdf

-

Fascinating stuff!

-

SD, I've heard you call so many different things "cash equivalents" it is starting to lose meaning LOL

-

To quote Charlie Munger at the 2012 AGM: "And I don’t think you need to worry about Warren’s side investments. His investments in Berkshire are so huge and those are so small, relevantly, that if that’s your main problem in life, you have a very favored life."

-

ProPublica article out this morning: https://www.propublica.org/article/warren-buffett-privately-traded-stocks-berkshire-hathaway-ethics-irs?taid=654cafb069a63b000142e9d4&utm_campaign=trueanthem&utm_medium=social&utm_source=twitter edit: I read the article and there doesn't seem to be a whole lot there. I was actually confused when the article ended so abruptly.

-

Just to clarify - does everybody on this site that owns Bitcoin or other cryptocurrencies own them because they think they are going to go up in price? (again, apparently we are all still keeping score in the USD unit of account, so yes I mean up in price against the USD). I get that some of you are excited by the revolution but the reason you own it is that you think it is going to go up, right? So separating out the reason you think it's impressive or useful - it is a bet that more people will try to fit through a narrow doorway in the future making the price of the relatively inelastic thing you own go higher? There is a lot of romanticizing about the revolution but everybody I have asked (the ones who actually lower themselves to my level to answer the question) has admitted to me that the reason they own the thing is that they think it is going to go up.

-

Warren is addicted to Yen borrowing! Back at the trough with another prospectus today https://www.sec.gov/Archives/edgar/data/1067983/000119312523272880/d532609d424b5.htm

-

I'll go out on a limb and guess that ValueArb is not a big MMT guy

-

https://www.bis.org/publ/qtrpdf/r_qt2309w.htm This is a recent BIS paper describing some of the above mentioned issues. The worry is that the tightening of margin requirements on futures and/or the tightening of available leverage through the cash bond repo market can (and has) destabilized the treasury market in a hurry. The US is very sensitive about the stability and liquidity of their government bond market.

-

So we use the Us Dollar as our unit of account, like the metric system or something like that, but we don't "invest" in the US Dollar by taking a position in currency and calling it a day. We buy productive assets of various types. We just keep score in US dollar. Even Bitcoin folks seem to keep score in the US dollar unit of account - every BTC thing I see is quoting the BTC-US Dollar cross. So with Bitcoin or other Cryptocurrencies I guess the idea is to invest in the currency itself and that's it - hold "cash," wait, profit?

-

Everyone hates commercial real estate and Kennedy Wilson is at a new 52 week low. Bill McMorrow bought $1.23 million worth of KW stock in the open market yesterday. Maybe Bill needs to bring over some Brookfield real estate guys to put some spin on things!? https://www.sec.gov/Archives/edgar/data/1408100/000140810023000142/xslF345X03/wk-form4_1699311214.xml https://ir.kennedywilson.com/~/media/Files/K/Kennedy-Wilson-IR-V2/documents/3q-2023-supplemental-and-release.pdf https://ir.kennedywilson.com/~/media/Files/K/Kennedy-Wilson-IR-V2/reports-and-presentations/presentations/q3-2023-investor-presentation.pdf

-

Don't fret, we have been managing "demand destruction" with supply destruction for a while now - we will shrink our way to a bull market, call the Saudis!

-

Synchronized global deflationary Recession ... obviously!

-

I feel like he's trying to say something else that isn't such a mainstream take on it. He makes the very rare (for journalists anyway) admission that "Yet the end-buyers of the debt are unlikely to disappear since government deficits automatically create the very savings that are then channeled into financial assets. The real issue is that the financial plumbing meant to make all this happen has become dangerously creaky." He also acknowledges that the Citadel's of the world running massive leveraged Treasury basis trade books (long the actual bonds, short the futures, insane leverage on the bonds provided cheaply by the repo market) have taken on some of the role of primary dealers in creating a huge pool of demand for cash bonds. (This is "bond warehouse managers" notion he closes with - picture Ken Griffin) The government seems worried about these massive basis trade books because they seemed to have a hiccup for a short period of time when the COVID panic first broke (Treasury market was chaotic instead of what may have been predicted as an immediate flight to safe assets). I thought maybe the author was trying to get at the real issue with the basis trade in a time of crisis like that, which is that it relies on a loose, liquid repo market for all that leverage and as soon as the repo market tightens up the giant basis trade hedge funds become sellers of treasuries and buyers of their short futures positions (to unwind leverage on their trade). This is why the central bank is so focused on loosening up dollar funding shortages in crisis moments like that - to un-tighten the global market for stuff like repo. It's not quite a LTCM situation but I think maybe that is what regulators are hinting that they are worried about. Not sure he fully developed a point in the article though so was curious if anybody else got a point.

-

I'm curious what people think the author is saying in this article.

-

The idea is that the investment bank / counterparty took an offsetting long position to hedge their exposure

-

It is not at all clear whether they owe tax on these gains since the underlying is the issuer's own shares. I meant to ask on a CC but can never seem to remember to do so on the actual mornings of the calls. When an issuer buys their own stock, doesn't retire it, and then sells it for a profit, there is no tax owed (at least in the US).

-

OXY reports tomorrow FWIW

-

This is another trade publication newsletter that might be interesting to some of the insurance investors here seeking color and market updates. I guess this is "conference season" for the industry, from Monaco to Baden-Baden and now this APCIA conference. There have been a dozen or so of these trade publications released multiple times a day out of these conferences. This one is from this morning at APCIA https://pdf.static.prod.wbm.infomaker.io/d7acfe62-7581-5e24-a1e2-3ed1ac45f801?utm_source=listrak&utm_medium=email&utm_term=Download+issue+two%3a+6+November&utm_campaign=Welcome+to+our+APCIA+2023+Day+Two+edition%3a+Monday%2c+6+November And another free issue released Tuesday, Nov 7th: https://pdf.static.prod.wbm.infomaker.io/fa81cb8a-3628-5b26-b592-188668fbfe9b?utm_source=listrak&utm_medium=email&utm_term=Download-here&utm_campaign=Welcome+to+our+APCIA+2023+Day+Three+edition%3a+Tuesday%2c+7+November

-

It should be noted, though, that Berkshire’s operating subsidiaries outside of Insurance are not performing particularly well. They are profitable, but a not shooting the lights out. This is partially due to economic weakness, partially due to their particular mix of industries. Business is hard - they ain’t all Apples and Googles

-

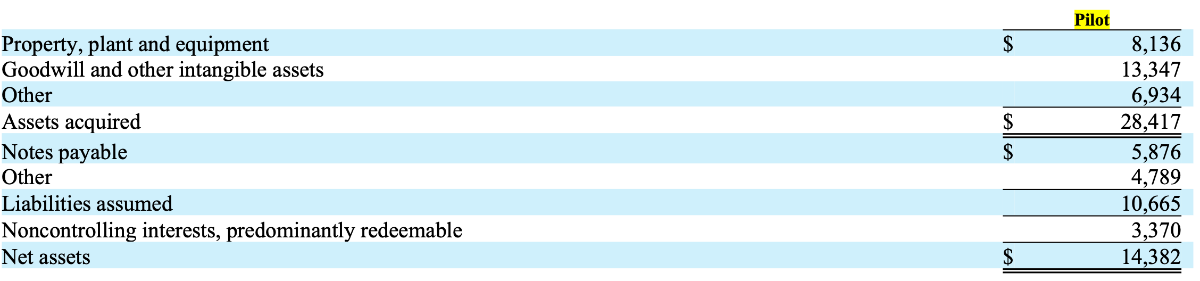

Berkshire described the big jump in depreciation and amortization at Pilot in the first quarter 10Q: " a significant portion of which derived from depreciation of property, plant and equipment assets and amortization of intangible assets that were remeasured to fair value in connection with the application of the acquisition accounting method in 2023" The acquisition premium resulted in a huge amount of goodwill and other intangibles as well as writing up the property & equipment where they could justify it:

-

Just to be clear, this isn't an impairment or a write down, this is a write UP to the acquisition price (a big premium to the carrying value of the net assets of the company under their historical basis - a very normal situation for an acquired company that sells above book value). The write UP results in increased depreciation and amortization which depresses reported earnings but has no effect on "owner earnings" or cash earnings or whatever you want to call them. The only reason there was a 1 month delay in adopting the acquisition method of accounting was that it takes time to assign values to the various categories like identifiable assets, intangibles, goodwill, etc..

-

There isn't any problem with Berkshire's method of accounting, which Berkshire uses on their other acquisitions and understates profitability in a way that is consistent with Berkshire's conservative accounting style and rejection of earnings "optics." There is no reason Pilot can't keep two sets of books, or simply adjust the Berkshire-kept figures for the excess depreciation and amortization and include derivative hedging gain/loss. Companies do this all the time. Hell, a lot of companies keep three sets of parallel books. That's why I think they will just negotiate an adjustment to the computation of earnings before taxes and settle the matter. Since it impacts Berkshire's reputation as an acquirer that "does right by their seller partners," I feel like there is more to the story when you consider the other changes Pilot and Berkshire made. Pilot brought in a commodity trader CEO and started trading a lot more around energy commodities (a business Berkshire exited), Berkshire fired that CEO and the CFO immediately after assuming control, Berkshire exited the more trading-related businesses and focused back on the plain vanilla lines of business Pilot was in at the time of the original deal.