gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Wild man Buffett went out of his comfort zone to buy a 2 year note at 4% before yields fell back - he's gone rogue

-

No chance - I feel like this discussion is mistaking Fairfax India (FIH.U - almost certainly a PFIC for US investors, best in an IRA or similar) for Fairfax Financial, which is definitely an operating company.

-

to tell the world, "we're not even close to panic prices you pussies"

-

New Buffett interview and video snip - https://www.cnbc.com/2026/03/31/warren-buffett-says-hes-still-making-calls-on-investments-at-berkshire-flags-tiny-new-buy.html

-

We can shift seamlessly from analysts claiming they are over-earning from an era of high risk free rates to worrying about mark to market losses from rising yields. There's always something to fuss over

-

"very little free float" is over a Trillion dollars and something like 80% of the market cap of the company. The S&P 500 weightings are free-float adjusted anyway.

-

It may not be obvious, but it is very unlikely that Berkshire is currently repurchasing its stock. When Greg announced the repurchase and we saw the one-day buying in the proxy, that was during an open period. Berkshire could buy during that period until the date two weeks before Q1 end. To repurchase shares outside of that period requires an automatic rules based purchase plan, which I don't believe Berkshire has used in the past, but could try using under the Abel era. Those plans have to have their rules defined during an open period but then have a 30 day delay before they can become active.

-

I always thought the difference between a "MGA" - Managing General Agent - and the type of general agency system or wholesale brokerages we are normally talking about is that with a MGA the Insurance carrier has delegated their "underwriting pen" to the MGA. I'm sure NICO has done that in specific relationships, but I think it was probably pretty rare and required a special relationship. This is the only one I remember but their may have been some others https://kemahcapital.com/kemah-capital-announces-underwriting-agreement-with-members-of-the-berkshire-hathaway-group-of-insurance-companies.html Most of the time I remember NICO delegating their underwriting authority to another entity it has been something like an automatic quota share agreement - like Insurance Australia - IAG. They ended that, not sure how it went.

-

“My own strong bias”. LOL…. good luck fella!

-

I don't have an issue with them but no US corporate/enterprise paying customer beyond the scrappiest start-up is going to use Chinese models as part of their business. The context of my comment was revenue for the US frontier model companies For me personally, on a dedicated device, I wouldn't hesitate to use Kimi K2.5, MiniMax or other similar models.

-

I pay Open AI $20 per month but they probably lose money on that. It does seem like Anthropic is a bit more focused on building a business that at least resembles a sustainable business model. A lot will change as soon as a "good enough" open source model that isn't Chinese is available to run on cheap local hardware. Traffic can be routed to "good enough" free-ish local device and only to expensive per token frontier models when actually needed. That inflection could be a problem for the big spending frontier model companies. I'm sure OpenAI's pre-IPO financials were looking pretty scary.

-

Tail Risk - Is It Part of Your Investment Framework?

gfp replied to Viking's topic in General Discussion

The "money is credit" point is basically right. I think you probably miss the multiplier effect of dollar denominated instruments ("USD money") that are created by offshore banks entirely outside of the US government / Treasury / Federal Reserve / US Banking industry. These forms of money are extremely large and far more prone to tightening, changing in price, risk aversion behavior, etc. Think of the US dollar like the metric system - a unit of account - any offshore entity can create instruments that are denominated in this "metric system" - it isn't required that something be an "authentic government created US dollar" for it to effect monetary tightness or loose-ness. I suspect that one of the big reasons Fairfax wanted to make a big bet on deflation (that didn't work out at all for them) was that something fundamentally changed in the GFC around 08-09 that was a step change in the global funding markets. Post GFC, trust was gone and it didn't matter if you were a blue chip name or Joe Schmo - you had to post collateral for everything and that was a big change. And good collateral - with haircuts for anything even slightly less than pristine US T-bills. The size, terms, and circulation of the global eurodollar market was knee-capped and never recovered. It is still huge - larger than the market for "authentic US dollars" - but dollar funding has been tighter ever since that step change. It's not just the "amount of dollars that exist" that impact "deflationary monetary conditions", tightness or looseness of money. It is the recirculation or maybe think of it as the "velocity of money" that matters. Money hoarded because institutions are slightly increasing risk aversion behavior is money that either isn't willing to be recirculated or isn't willing to be recirculated at anywhere near the price it was available at yesterday. That's why you often hear that "repo markets" are showing stresses below the surface during bouts of tight money - an increase in risk aversion behavior by everybody, especially primary dealers and global eurodollar banks. But deflationary monetary conditions - tight money - is not exactly the same thing as inflation or deflation for consumer prices. We will continue to have bouts of tight money here and there but governments will not allow deflation to persist to where it shows up in the CPI because our system doesn't function well that way. Even with all the AI predictions of mass deflation of consumer prices, I don't see it actually happening. Like you said - our system is built on credit and credit is underpinned by collateral and deflation of collateral doesn't go well. And deflation in consumer prices, outside of the "good deflation" we saw in technology products for most of our lifetimes, can really slow the economy as people put off buying because prices will be lower next month. -

Of course if you think about them as baskets like "Insurance Brokers", "Software", etc, they are more concentrated bets. But for me what works to refocus the portfolio when I get a bit of clutter is when one company I know very well gets very cheap and that is when you start looking critically at every position as a potential funding source to buy more of the one you know deeply. The further down the one you know goes, the more ruthless you are clearing pennies from the couch cushions until you are back to 3 or 4 positions and the portfolio is all cleaned up. But that's just me - I buy more of stuff I know well when it goes down. I don't have arbitrary "I'm already fully allocated in that name at 15% of assets" type of restrictions.

-

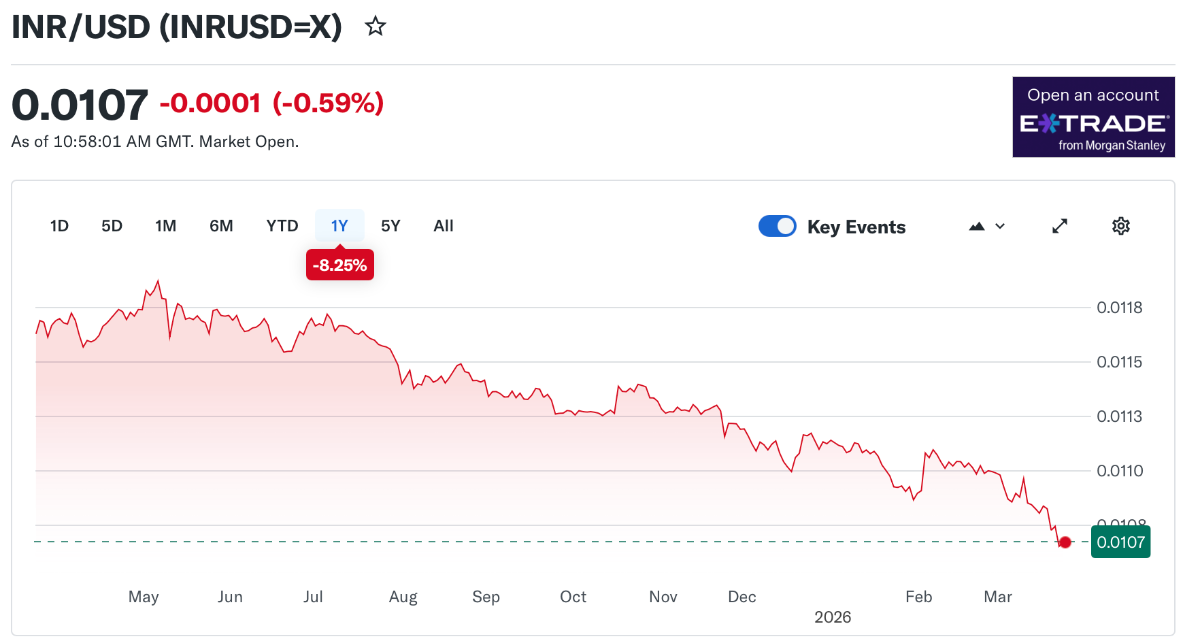

I watched it. A waste of time as I expected initially by the intro. These videos are all the same. A country is forced to sell treasury securities because their country is short of dollars locally (and since we are talking about $50 billion over an entire year it will also include periods where RBI tried several times to intervene in the currency market by selling dollars to unsuccessfully pause a decline in INR-USD). When a central bank intervenes in the open market to try to defend a level on their currency where do you think the dollars they are "selling" are coming from? The main point that actually sticks is that weaponizing SWIFT / USD networks against Russia highlighted a key risk for central banks. This was a blow to the USD's standing as a global standard. But the USD is still on one side of essentially every currency transformation and deeply ingrained in overseas funding markets. If I want to trade between JPY and INR the reality is that the JPY becomes USD and then the USD becomes INR. Because it is far cheaper with deeper liquidity to transform the asset that way. The value of a US dollar locally in India, or really anywhere in Asia, despite booming several economies, has gone straight up. Of course they would love to settle international trade with BRICS outside of the dollar. Their structural dollar short is killing them currently. But what they want is for trade partners to accept INR and that isn't going to happen any time soon. Because INR is not useful or demanded outside of India. Some day India will have sufficient exports that trading partners will be willing to accept INR to re-spend on Indian manufactured goods. But knock off generic drugs and basmati rice aren't yet a big enough factor. If you take just the RBI's currency holdings - what other options do they even have if they wanted to make a conscious decision to "diversify away from the USD" ? A German government bond? A French one? There aren't very many actual practical options. If anything, if I'm at the RBI, I am extremely concerned that my central bank only holds $325 Billion of USD. As we saw in the video - that can deplete awfully quickly when the country needs dollars.

-

Tail Risk - Is It Part of Your Investment Framework?

gfp replied to Viking's topic in General Discussion

What I'm curious about is if Blake will sell his oil investments during this oil price spike or actually buy anything during a true panic with the cash position. In a "dash for cash" your cash only becomes more potent if you spend it. It doesn't show you a profit on its own - you have to be willing to abandon your security blanket when everybody is panicking. -

The 20 year treasury has a 5 handle again!

-

Warren Buffett Defends the ‘Giving Pledge’ Against Peter Thiel

gfp replied to Lotsofcoke's topic in Berkshire Hathaway

Kay Graham? Doesn't seem like Astrid fits the definition. It did sound like Susan had an affair but who knows.. its complicated -

I didn't watch that whole video but I always get a kick out of a huge dollar shortage in Asia being reported by the press as some kind of voluntary move by governments to "ditch the dollar." Does this chart make you think India is making a decision to ditch the USD? Or that there is a massive squeeze in dollar liquidity across Asia? And lets throw in some other free floating Asian currencies

-

It sounds like they are saying they were "getting out of US dollar exposure" and you heard the opposite

-

Covering all my SPY shorts this morning! Time for a rest

-

AJG had an Investor Day / meeting with management yesterday. The transcript is on Quatr app but I don't know how to link it here. They published a few slides from the CFO to accompany it https://s28.q4cdn.com/872121257/files/doc_downloads/2026/03/17/CFO-Commentary-Q1-2026-IR-Day-FINAL.pdf It is possible the webcast is also available for replay but I haven't tried -> https://investor.ajg.com/events-and-presentations/event-details/2026/Arthur-J-Gallagher--Co-Investor-Meeting-with-Management--2026-ubGGie_JQk/default.aspx

-

This week's video from Jordi is less on AI specifically and more of a general market conditions overview but it is worth watching if you are one of the value speculators investors on this board who is all juiced up with call options and leverage and not appreciating the deterioration occurring below the surface of the major indices. Don't get caught with your pants down fellas https://www.youtube.com/@JordiVisserLabs/videos

-

2025 Annual Report - Greg Abel's first annual letter

gfp replied to backtothebeach's topic in Berkshire Hathaway

No, Berkshire didn't purchase and A or B shares before the Annual Report was released. No clue what Feb. 2nd A-share volume was all about but it may not be "real." -

So Fairfax took this private exactly three years ago at $15.50 per share and is selling some at $28.30. 22% annualized plus all those distributions received over the last 3 years. (not considering the investment results before the take-private in this)

-

Seems like it's a little early to criticize this discrepancy? Ben started his track record at Marval in 2017 and took over the Chairman role at Fairfax India in mid-2024. Has Fairfax India even made a new public market investment since July 2024? Wouldn't the Chairman of the board role be pretty different than sole Portfolio Manager? You start at Fairfax India in July 2024, the Indian stock market peaks in September 2024 and then starts an 18 month correction Fairfax India is a US Dollar based investor so Indian stocks in general would have produced an 11% -ish loss on average since Ben was made chairman of FIH.