gfp

-

Posts

5,347 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

ECIP plays - CZBS, MFBP, PCB, CZBS, UBAB, BFCC

gfp replied to formthirteen's topic in General Discussion

I don't know where to post this but it is always interesting to read Tim Eriksen's quarterly letters at Cedar Creek. I am posting it here even though it isn't primarily discussing ECIP recipient banks, because there is a lot of overlap in the folks that would find both interesting. (and there is some ECIP content). Tim used to post on this board occasionally and is active in Expert Market microcaps that most brokers don't offer. Kind of a cool throwback to the types of companies a young Warren Buffett got to sift through. https://static1.squarespace.com/static/5ea6570a0ba57d406203e048/t/64badaa2b743f43df05f5d0f/1689967267033/Q2+2023+Results+for+Cedar+Creek+Partners.pdf -

https://www.sec.gov/Archives/edgar/data/718877/000119312523188107/d491908dsc13ga.htm Berkshire's ATVI holdings are much lower than many assumed (as of June 30th)

-

I guess I am missing something. I was under the impression that 95 strike calls expire worthless on a cash deal at 95. They aren't in the money at 95. It would be a loss of 31 cents.

-

Isn't the deal price 95 cash?

-

what are the "weeklies 95s?" 95 strike call options that you are long???

-

I'm not sure comparing the pricing power of tobacco companies with the pricing power of insurance companies is as simple as that. Insurance companies are price takers, despite the current point in the cycle making it look otherwise to some.

-

https://www.reinsurancene.ws/berkshire-gets-giant-1bn-share-of-florida-citizens-reinsurance-renewal/

-

I guess it's a sign of the times that Berkshire is so large now that a $3.3 Billion acquisition is not material enough to warrant a press release or an 8K from the parent company - just a press release and 8K for the BHE subsidiary. Now we know what they plan to do with the BYD proceeds. I wonder if there is room to expand at Cove Point.

-

Yeah I don't blame them. I heard Warren Buffett was in his 90's and hadn't diversified out of stocks at all! Seriously though, have people who are 77-86 years old in 90+% equity portfolios too. Imagine you own Berkshire and you are old and rich. You aren't going to spend even close to what you have. Why would you sell and pay tax just to reinvest the after-tax proceeds in something else at that age?

-

Yeah we didn't talk about whether he was pleased with his investment track record or not. I imagine not. He is pleased with how things are going at the operating business called St. Joe Company. He's borderline giddy on it. (he's not broke by the way)

-

Nice! I hadn't seen that. "funded with cash on hand including cash realized from the liquidation of certain investments." LOL - that's a new line! Sorry BYD, we would rather have the cash for LNG... https://www.brkenergy.com/news/article/brknews_covepoint_07102023

-

I spent a couple days with Berkowitz touring almost every St. Joe development property and I think he's pretty pleased with how things are going. Did he have a master plan to have almost his entire fund be in one illiquid concentrated holding? No, he did not.

-

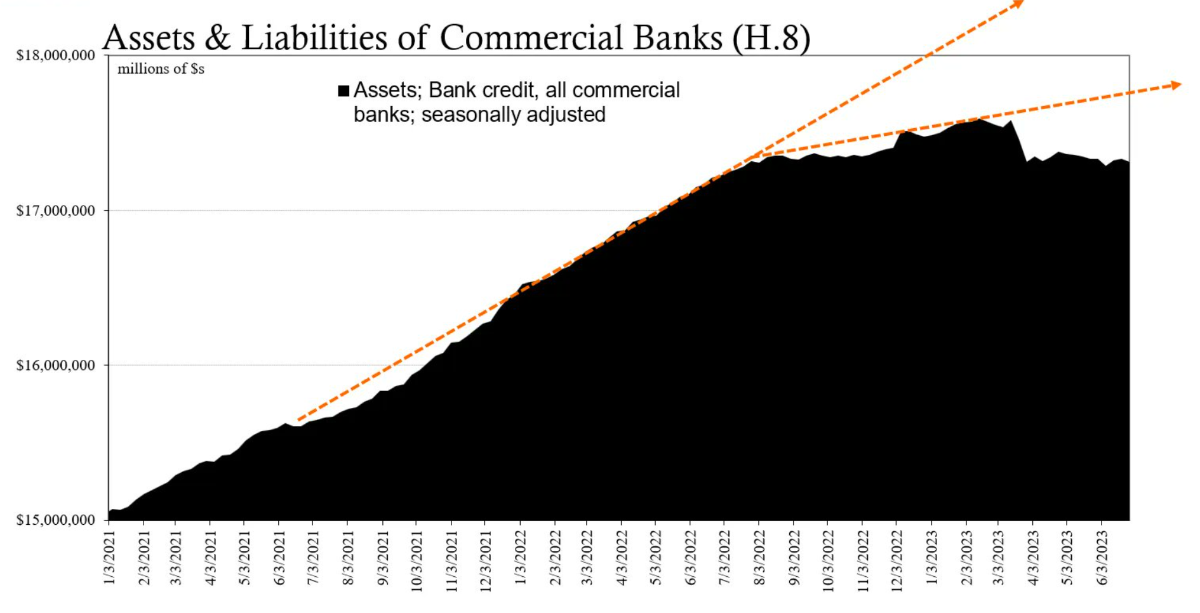

So midsize banks have already stopped expanding credit since March and, while generous in its "negative haircut," programs like BTFP are at least as expensive as other funding sources (currently 5.5%). Midsize bank profitability is going to look horrible by at least the 3rd quarter, if not already in the results we start to see next week. https://www.frbdiscountwindow.org

-

"As I have mentioned many times in the last 37 years, you, our shareholders, suffer a major negative as our company is not for sale at any price." - Prem, most recent annual letter to shareholders.

-

Seems like 22x earnings would be more than a 3.25% earnings yield and to add dividends on top of the earnings yield is double counting. Where does the money come from to pay the dividend - the earnings you already counted.

-

Just to clarify, do you hold mid 30's % allocation to cash equivalents or are you counting equities like UBS Group as an "equity cash equivalent?"

-

Well they didn't bite the last four times it happened in the past 8 months.

-

There isn't much to it but here it is as a pdf Buffett’s derivatives bonanza doesn’t prove that Taleb is wrong | Financial Times.pdf

-

Speaking of Warren and derivatives, the FT has a piece out this morning on Berkshire's use of derivatives - https://www.ft.com/content/f6524f65-188e-4d21-a943-18f9c6a61b8d (fwiw, I read it and didn't find it to be of much value. No mention at all that Berkshire's "huge" exposures to credit default swaps were essentially contained in a de novo bond assurance operation that was primarily writing 2nd-to-pay insurance on top of primary bond insurance coverage already in place. And no clue what the author is getting at asserting that Warren was allowed to be "creative" and "flexible" in his accounting for losses. Sheesh.)

-

It's pretty great that the corner of Berkshire and Fairfax message board was named after two securities that are almost tied in performance this millennium, with the smaller up-and-comer, Fairfax, clocking in at 846% vs. Berkshire's 826%. Going forward it is likely that Fairfax will continue to outperform Berkshire over long periods due primarily to the size difference. Unfortunately my dividends are taxed so Berkshire is ahead for this taxable American.

-

The way morningstar's chart works, they are telling you that Berkshire's A shares increased by that dollar amount during the period. It isn't the closing price.

-

Sure but my point was that in the 3 month period they purchased these forwards the 3Y note rate was between 4.75% and 3.4%. This isn't a case of waiting around for the 99th percentile or something. Those were the rates available during the quarter they chose to purchase the forward contracts. I think they thought they missed it and scrambled to lock in more at 3.75%.

-

What did you do before you retired?

-

Without dividends included gets you this, as mentioned by treasurehunt above: The US dollar OTC ticker didn't come along until a bit later but produces a result closer to tied somehow:

-

I'll have to defer to @boilermaker75 on his strategies for selecting the specific contracts to sell. I don't usually sell puts but I also don't leave unexecuted out of the money limit orders in place. Boilermaker has made a profitable consistent operation out of harvesting these premiums on stocks he would be happy to own (and immediately start selling calls against if he wanted to be lighter on them). By acceptable premium, I mean don't do it for 10 cents or something and pay a commission on top of that. "acceptable premium" will vary with the amount of time, price and volatility risk you are taking on. I'm not a big fan of selling long dated puts on individual stocks unless there is a specific strategy that involves it. I would stick to weeklies out to 2 months max.