gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

That's great Reds, I figured you were a hard money guy from your other posts. A lot less work and similar risk profile to many other forms of real estate investment. Has it been your experience that the income is taxed at a much higher rate, all in, versus a more traditional income property investment? I feel like I barely pay any tax at all on our RE income but my impression of hard money was that it was fully taxed.

-

I'm curious to hear what side hustles were spawned by the side hustle that is this website!

-

Yikes! How quick a decade goes by. The 16 year old from my post is 25 now. Still sucks at math. Seems like everybody has a substack with subscription income these days - there must be some succeeding at that game. Information publishing has always been a decent business and twitter seems to be a primary marketing tool. Personally, we still rent out apartments. First of the month comes around like clockwork

-

@Vish_ram that looks wonderful. You stay in real beds in villages or in a tent along the way? I assume the former?

-

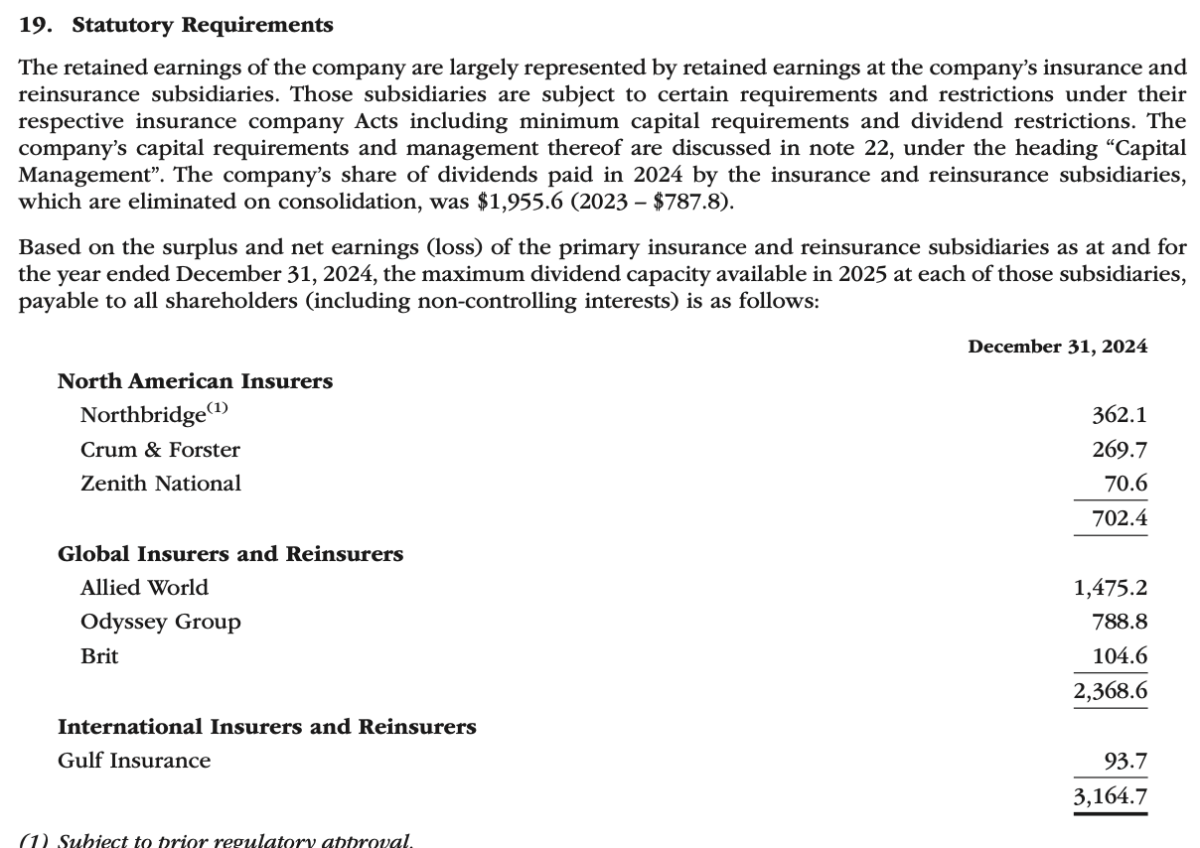

That is possible. I was just thinking they were factoring in the passage of time. The screenshot from the annual report was from year-end. Time marches on and capital accumulates!

-

I would imagine the analyst is referring to the approximate amount of "excess capital" the insurance subsidiaries could do without yet still maintain their current volume of business. As in, what is available to be distributed to the holding company and used for shareholder stuff like share repurchases and dividends. Not sure the analyst is factoring in things like buying in minority interests in subsidiaries. If the insurance subsidiaries remain profitable and stop growing quickly, there will be "excess capital" that can be distributed out

-

There was a lot that was going wrong at Dexter. I heard factory workers in Maine say that orders were drying up to a trickle and Alfond would instruct them to keep production up, to the point where they literally had nowhere to store the accumulating inventory. Buffett should have known better, Harry Bottle would have painted a line on the wall LOL... But nobody would even bring up Dexter if Warren hadn't paid in shares. Berkshire bought a ton of businesses that went to zero. It was paying in stock that made it hurt.

-

Thanks Bill, another great post. I have a question for you. In normal times (as in not during some debt ceiling-related distortion), since the Treasury department usually maintains some significant positive balance in the Treasury General Account, is it true in principle that the deficit spending (government reserve balances becoming private sector reserve balances) pre-funds the private sector "cash" that is used to purchase the treasury securities that "fund" those deficits? My contention is that as soon as some of the TGA reserve balance is deficit-spent into the private sector, it becomes the IOU of the government and then some of that newly created government IOU (private sector reserve balance) is swapped for a treasury security. Private sector owned bank reserves pay a high rate of interest currently (4.4%), so "borrowing" actually saves significant money, under present conditions, if the treasury elects to "borrow" for 2-5 years.

-

Just when you think work is over for the weekend you get an order fill in Canada and realize they are still trading up there! Y'all still got the exchange open!

-

No. I would not assume any of that

-

The difference is that the move in the FX for the bonds gets reported in operating earnings and the move in the stocks is buried in much bigger mark to market gain/loss that tends to get separated from operating earnings. Plus the japanese trading houses earn a lot of their income in dollars so they aren't pure JPY businesses.

-

EUROB has been repurchasing its own shares daily. Fairfax owned 32.26% of EUROB on 3/31 and will participate in the EUROB repurchase (sell shares directly to EUROB) in order to keep their ownership "close to, but below" 33% "in order to maintain its total equity stake in Eurobank Holdings close to, but below, the regulatory threshold of 33% of Eurobank Holdings’ voting rights."

-

It becomes a lot easier if "the market" performs poorly. Berkshire will trade down with the index and the Tim Cook scenario unfolds with big numbers. A hundred billion dollars a year of capital return through repurchases? Count me in

-

It is possible there was some broad analyst call that I missed. I assumed some of it was deferred selling after end of quarter window dressing but it does see very widespread across the industry. (AAME did hit a new 52 week high this morning, LOL) The only insurance specific thing that I know of today is the Bermuda Monetary Authority finally releasing the year-end 2024 financial statements for all the Bermuda domiciled insurance subsidiaries. December 31 2024 was a long time ago though... https://www.bma.bm/public-filing-overview edit: oh, and this out of Florida? https://www.insurancebusinessmag.com/us/news/regulatory/florida-cuts-state-hurricane-reinsurance-funding-reinsurers-brace-for-impact-541241.aspx

-

Here's another one for the Saint Joe crowd. Why it was significant that JOE closed off its lows three days ago ->

-

yes, the utility is not about what already happened. It is about what the pattern, when broken, predicts for the immediate future. value bros love to hate on chart patterns and any number of other techniques but most value bros underperform the indices for their entire careers while expecting to be paid for their genius. Chart patterns are useful in helping decide when to wait, when to increase or decrease position size, when to sell aggressively, where to set clouds of multiple limit orders, etc.

-

Here is a fairly textbook bull flag in MSGE. We'll see how it resolves TOL and TDW from the earlier posts are behaving as you would expect from a "chart" standpoint. (I don't own either of them, just noticed the patterns) FIH.u continues to look pretty good on the chart, as it did when it was posted in this thread.

-

The biggest factors for me are: Large gains on USD strength (JPY and EUR borrowings) - not only can these not recur, they can reverse in the billions GEICO over-earning - combined ratio was crazy low vs. target of around 96 Peak T-bill rates (will be somewhat offset by increased cash balances this year)

-

They sell an undifferentiated commodity product and their investment track record has been "spotty" ! Look out below

-

Today is a Canadian holiday with no stock market right?

-

For any of you BRK-heads that ordered the reprint of the annual meeting book - Celebrating 60 Years of a Profitable Partnership - my copy just arrived in the mail, straight from Farnam Street!

-

What about you Marco? Do you already live in the suburbs or do you live in the big city?

-

I'm curious to read the Skechers merger proxy whenever it is finally released. That should give a hint if Berkshire got a call on that deal before backing off or being outbid. Berkshire is still growing many large businesses organically and is certainly not capital constrained if there are any good ideas anywhere at all. They over-earned by quite a bit last year for several reasons so it will take a while for the market to readjust. In the mean time, money comes in the door every day.

-

https://www.businesswire.com/news/home/20250627982115/en/Berkshire-Hathaway-Inc.-News-Release

-

Yes, definitely! And there are important differences in the duration and structure of the float as well. Berkshire is very focused on long lived float even if they expect it to be approximately break-even. But Fairfax has been a much bigger investor in fixed income and fixed-income-adjacent securities, helping to balance out the risks of higher leverage. But you definitely need to trust that they aren't going to incinerate money on the investment side. edit: I should add that my comparison to Berkshire in 1996 wasn't meant to be some huge endorsement of either - Berkshire shares have only appreciated by 11 or 12% percent a year from '96 I believe. Just fine, but not the returns people assume when they hear "the next Berkshire Hathaway!" lol