jfan

-

Posts

539 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by jfan

-

The Less-Efficient Market Hypothesis by Cliff Asness

jfan replied to Viking's topic in General Discussion

thanks for highlighting this article. I read this paper when it came out and coupled with Mike Green/David Einhorn's thoughts on this structure , have been thinking about where the puck is going in the next couple decades. I wonder if this is evolving into an age of conglomerates again. With small public businesses not getting any investor attention, it seems ripe for someone to consolidate them and control the cash flows in a private manner. Berkshire started this trend, and Fairfax is following, with increasing dollars allocated to private investments or take-private transactions. It is a bit of a conundrum wrt to the ease of accessing public investments at a low cost these days with more than plentiful information out there at our fingertips and the opportunity for decent future returns. The market structure seems to drive exponentially asset prices for those loved public equities and ignore everyone else. Coupled with the inherent laziness to actually do the work to understand what we are buying and owning, I feel people are just relying on the 1st order concept that "the market will return 7% indefinitely as they have in the past" which drives more market distortions. Investing is simple but not easy to do well. -

Can buying over-valued stocks be value investing?

jfan replied to jfan's topic in General Discussion

Curious, what did you try and why did you choose what you did? -

Can buying over-valued stocks be value investing?

jfan replied to jfan's topic in General Discussion

@SharperDingaan this is a great example but the one thing I would add to this wrt to using a company's share price as a currency in this context, is that the when o/g commodity prices are up, their acquisition targets are also pricey, and hence at best a neutral but more likely value destructive due to expensiveness and bidding wars for the assets. It only makes sense if you can find cheap targets in preferably a fragmented market. @73 Reds Investing is very much like Yin & Yang, there is a balance between sticking to what works and being intellectually curious to learning new frameworks. What I feel I can learn from the Bill Millers, George Soros and the best traders out there (not that I am one), is their ability to acquire, assimilate new information, and pivot and change their minds in the face of disconfirming evidence. Kudos to you for exploring new ideas. @ArminvanBuyout I have not studied these companies in extensive detail to understand all their products and strategies, but what I would add is that these potential over-price high-tech businesses use their expensive shares to acquire human capital (maybe not other businesses), which at some point lead to 2 problems: 1) diseconomies of scale wrt to its growing workforce, 2) ever increasing need for higher share prices to keep their work force happy which at points in time could be too expensive for their productive value. I suppose at some time there will be a reckoning here as well as it did happen in the dot.com bubble, unless management is so good as to organize themselves to be continuously innovative and find new markets over time eg Amazon's Bezo days. Costco is an interesting thought as well wrt to its expensive share price and lack of increasing of their overall share count, obviously we know that this is a high quality business, I guess we can think of its heady stock price as an untapped resource that gives it optionality in the future. -

Can buying over-valued stocks be value investing?

jfan replied to jfan's topic in General Discussion

Quote from William Thorndike's Outsider chapter on Singleton "Singleton took full advantage of this extended arbitrage opportunity (lofty conglomerate P/E ratios, low competition for acquisitions), and between 1961 and 1969, he purchased 130 companies in industries ranging from aviation electronics to specialty metals and insurance. All but 2 of these companies were acquired using Teledyne's pricey stock." Reading the above 2023 case study, and excerpts from Thorndike's book, this was just one capital allocation factor, he also utilized purchase price discipline, targeted specific technological niches, and ran a particular decentralized organization (that later was deemed inefficient) in addition to focus on cash flows. It seems known when to growth, how to grow, the environment that you operate in, and financial levers that can be pulled, in addition to management incentives/motivation are all key decision factors. -

Can buying over-valued stocks be value investing?

jfan replied to jfan's topic in General Discussion

Purchasing over-valued stocks in businesses that use their shares as currency is fought with risk and I would agree that most of the time this does not work in the long run. I think the primary danger of these roll-ups is the people element ie it gets really addictive to see those revenues, cash flows, and stock prices go up and to the right over time. Doing this as the only business strategy will most likely end in failure ie conglomerates in the 1960s (ITT, Litton), Mississippi Bubble, South Seas Bubble, etc. Similarly, Cathie Woods' business of pumping world-changing tech companies based on a story, is also not investing but gambling/speculating. However, that said, I think we can learn something from everyone including her (ie she introduced me to the mental model of Wright's law which I later read in Bionomics - which was an interesting read btw). But for the few truly good allocators out there, using their stock as an acquisition currency, is a lever that can be sometimes pulled or repetitively pulled in the right situation for the long-term. Other examples that come to mind (please correct me if I'm wrong about the details) - Buffett issuing shares to purchase GenRe during the height of the dot.com mania - Prem issuing shares to purchase undervalued insurance companies during the early 2000s - Singleton during the 1960s using Teledyne shares to serially acquire companies (see link below) The reason I started this thread was not promote buying over-valued growth stocks especially when the market feels toppy (and Buffett is a net seller, holding lots of cash), but better understand the rare situations when this is actually rational and why. Just like buying low PE stocks without discrimination and concentrating them in your portfolio, isn't intelligent either. Eliminating ALL over-valued growth stocks without discrimination could result in a significant opportunity cost. PS: found this case study about Teledyne that people might enjoy reading Teledyne Technologies—A Conglomerate Phoenix That Rose from the Ashes with Henry Singleton’s Corporate DNA Intact -

A Thought Experiment It is common occurrence where overvalued companies often issue shares to purchase other businesses. If the other business is cheap, you can create a roll-up strategy that incrementally puts the expensive multiple on the cheaply valued acquisition cash flows (if there is any). The problem is that most of these acquirers, overpay, over-estimate the synergies, under-estimate the integration costs, and with ever enlarging human capital, there are diseconomies of scale aka bureaucracy. Now what happens if you do have a good capital allocator, who does actually use their expensive shares to buy truly inexpensive/undervalued assets and has the ability to do this over and over again? Most of these stocks are often expensive and have a price chart that is up and to the right. But most value investors want to pay for things that are cheap, with low expectations. It is quite comfortable for them to pay for a business that has a declining price, and with some work, decided that the consensus is wrong, and expectations are far too low, and cheer when the business buys back its stock. However, this former over-valued case, it too creates value, just in the opposite direction. But it feels really weird for traditional value investors to buy such things. So let's accept this weirdness for a moment, what sort of asset characteristics would be a great purchase? 1) requires little maintenance capex 2) has potential to appreciate by adding adjacent revenue streams, increasing network effects for the acquiring business, allows you to marginalize other competitors 3) low risk for integration 4) high certainty of synergies 4) truly undervalued/underappreciated at the current purchase price. Now let's say, this company can keep doing this, and eventually get taken up into a major index. Now the index investors who are not price conscious, are forced to keep buying the marginal shares. This increases the stock price further, which allows the capital allocator to issue more shares to purchase more undervalued assets. So from an asset/share point-of-view, you the minority shareholder, gets more assets/share incrementally despite more absolute shares joining the float. a) Should you entertain investing in these businesses? b) Would you pay a premium to Net asset value for such a business? And if so, how much of a premium? c) How and when would you decide to buy them? Examples of the top of my head - Facebook buying WhatsApp and Instagram - Franco Nevada issuing shares to purchase more royalties - MicroStrategy issuing shares to buy BTC

-

Just curious, where does everyone think BTC will top out this cycle? 1) $150K 2) $200K 3) $250K 4) $300K+ My vote $300K.

-

@SafetyinNumbers Great podcast! Thank you!

-

The supply is built into the codebase. To make a change requires the a majority of the nodes to agree to the change. During the blocksize wars, the miners wanted the network to change to increase transactional throughput and misjudged the degree of voting power they had. They assumed that having all the hashing power gave them more influence. However, the node operators and open-source programmers were able to mount a response rejecting their hard fork proposal. As with any voting system, it does require the node operators to be educated well enough to reject such changes. That said, most people (including myself) are not technical, so to some degree we rely on the open source ecosystem to keep the network true to its roots. This is a risk. But as the system grows, it will be harder and harder to achieve any consensus, and hence most proposals will be in deadlock, and the existing codebase will not change.

-

You are welcome. The root on X, @therationalroot has some really interesting ideas and put together some visualization with historical BTC data. He has some interviews on YouTube that you might enjoy. Caveat: some of the interviewers are a bit nutty

-

@73 Reds There are a number of models out there that different people have proposed in terms of valuation. Every model has some limitations, but even our traditional finance models have limits (ie DCFs, relative valuations, P/E & P/B ratios etc). In addition to @TwoCitiesCapital's models mentioned, another one that I found useful is on Charles Edward's Medium posts (he runs a digital asset fund) Bitcoin’s Production Cost. An Estimate of Bitcoin’s Production and… | by Charles Edwards | Capriole | Medium Bitcoin Energy-Value Equivalence. The Intrinsic Value of Bitcoin as… | by Charles Edwards | Capriole | Medium More simplistic relative models include % market cap relative to gold, relative to dollar-denominated debt, relative to real estate. Others have analysed the blockchain for ratio signals or wallet distribution/activity to look for over and under-valuation moments. Glassnode is a service you can sign-up and learn/use their data. Greg was quite astute that sometimes it just "feeling" the secular sentiments and behaviour change in the population over time (paraphasing him: digital adoption, level of trust in government, computing power, open-source technologies, etc) @wachtwoord posted a really good document here a while ago. I've attached it below. Even Cathy Wood has some reading material that might shed some light. I don't think it will get you the precise answer you are looking but might be a starting point. Buried within Edwards blog, is a quote from Satoshi about how he thought initially the production costs will drive BTC's value but as this drops, the transaction fees will play a much larger role in the future. This then requires a functioning market that obeys general supply - demand for block space. John Pfeffer - An Institutional Investors Take on Cryptoassets - 2017 Dec.pdf

-

I was just looking at the miner innovation over time. The current 2024-25 models have up to 860 Th/s with an energy efficiency of 13 J/Th at a $19/Th pricing. If look back to 2018 for example, a miner might have 20.5 TH/s with an energy efficiency of 75 J/Th at prices between $50 - 200/Th. Despite, the total hash rate going up over time, the cost and the energy efficiency to run the network gets lower and better pretty consistently.

-

Do you have to source for this quote? I was always under the impression that the core business was to have peer-to-peer money that was censorship resistant. There is a nuance to Gresham's law, in that it only applies to the situation where there is a fixed exchange often under governmental decree. In these cases, the bad money replaces the good money in a country as the transactional medium (the good money gets hoarded or sold internationally in exchange for the bad money). There already exists many wrapped BTC tokens on various blockchains entities (WBTC [eth], cbBTC [coinbase], kBTC [kraken]) exchanged at fixed ratios, one could imagine that these formats will potentially take over transaction volumes or at least act as a competitive limit to BTC transactions (base layer and lightning network). Taking this a bit further, if a country wanted to control its out digital fiat token and limit its citizen's from using BTC, they could wrap their token as well. All these self-motivated entities could limit/hinder the future development of a proper market-based mining transaction fee? (just talking out loud - idk) The inventors of BTC may be hoping for an application of Thier's law (reverse of Gresham's) where in the absence of legal tender laws, people will choose good money over bad in a free market system where the rate of inflation is high enough to reduce the real demand for the bad money. Perhaps, it is still technically too challenging for the general public to use to enable wide spread daily adoption.

-

Just glancing at the rate of doubling of transaction volumes on-chain seems to be slowing down (4 years, prior doubling was 3 years, prior doubling was 2 years) and the transaction fees in BTC (excluding the coinbase rewards) has not budged at all (stuck at ~ 10 - 15 BTC). I think this gives some evidence that the transaction fee market isn't necessarily developing in BTC terms as expected. Food for thought. Source: Blockchain.com charts

-

I've purchased both this one and the one titled winning long-term games. Both are excellent reads that gave me some ah-ha moments. Survival is more important than performance. Play the games that you can survive and not the one's that others were successful in - reproducibility matters. Sub-optimization and redundancy are helpful to survival. This was really useful to think about portfolio construction, long-term investing and dispels some common notions that amateur dabblers like myself held. For example (as it applies to the non-professional) 1) Not being fully invested is not a terrible thing. It gives optionality, allows one to have a clear mind when situational crisis occurs, and achieving a "satisfactory" outcome can still get you to the end-goal without being the best (eg IRR). 2) small position sizes should not be shamed. Lots of unexpected stuff happens both positive and negative. For very long-term holding periods, both are increasing likely over time. 3) Also cutting your flowers should not be shamed. Idiosyncratic things can even happen to really great businesses especially as your time horizon lengthens. The goal is having your portfolio survive for an investment lifetime (50 years), not just 5 - 10 years. This framing also helps with patience. This series of books coupled with ideas from deep survival are super useful (eg survivor mentality).

-

People's thoughts on this issue of re-hypothecation of BTC and centralization of BTC holdings within 3rd parties reducing the ability to form a functional transaction fee market in the future to secure BTC mining? https://x.com/DU09BTC/status/1850544299500552195

-

https://www.ft.com/content/894aba60-de05-46b7-a8a8-9fd405c16889 Hermes vs Kering

-

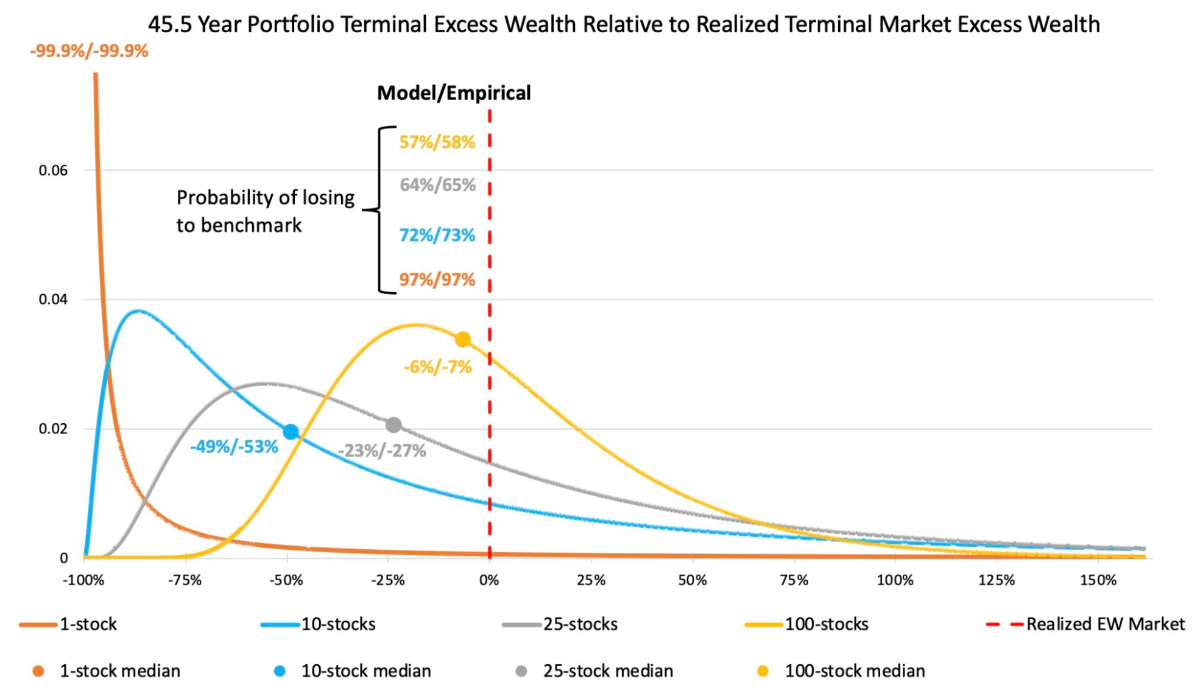

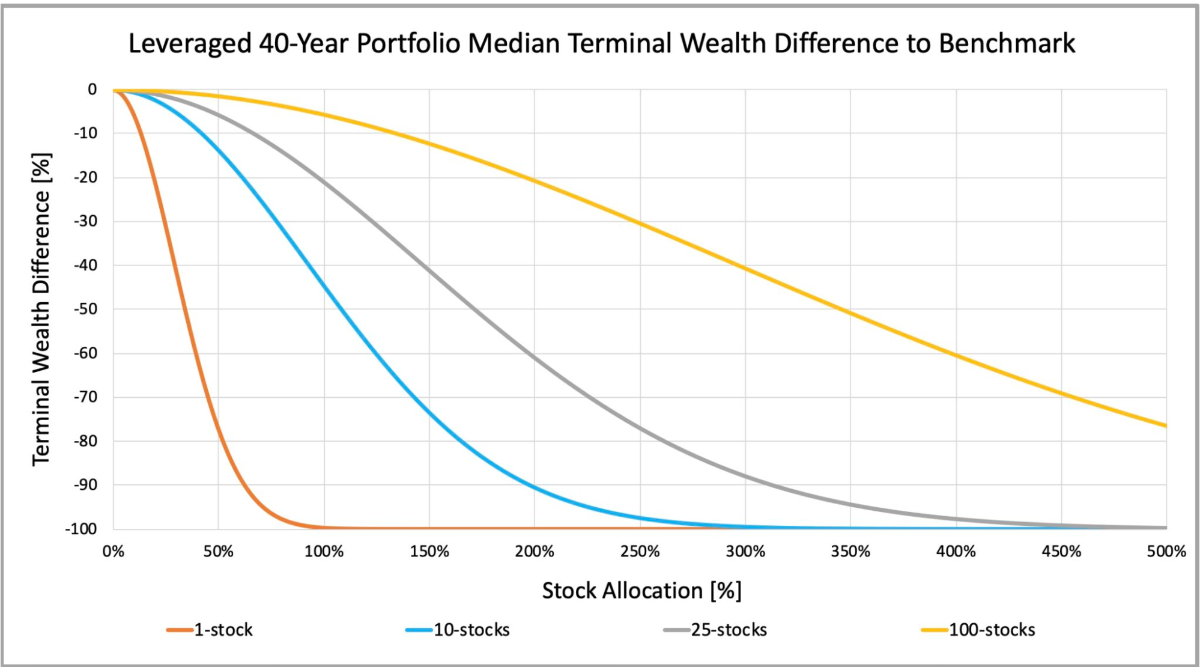

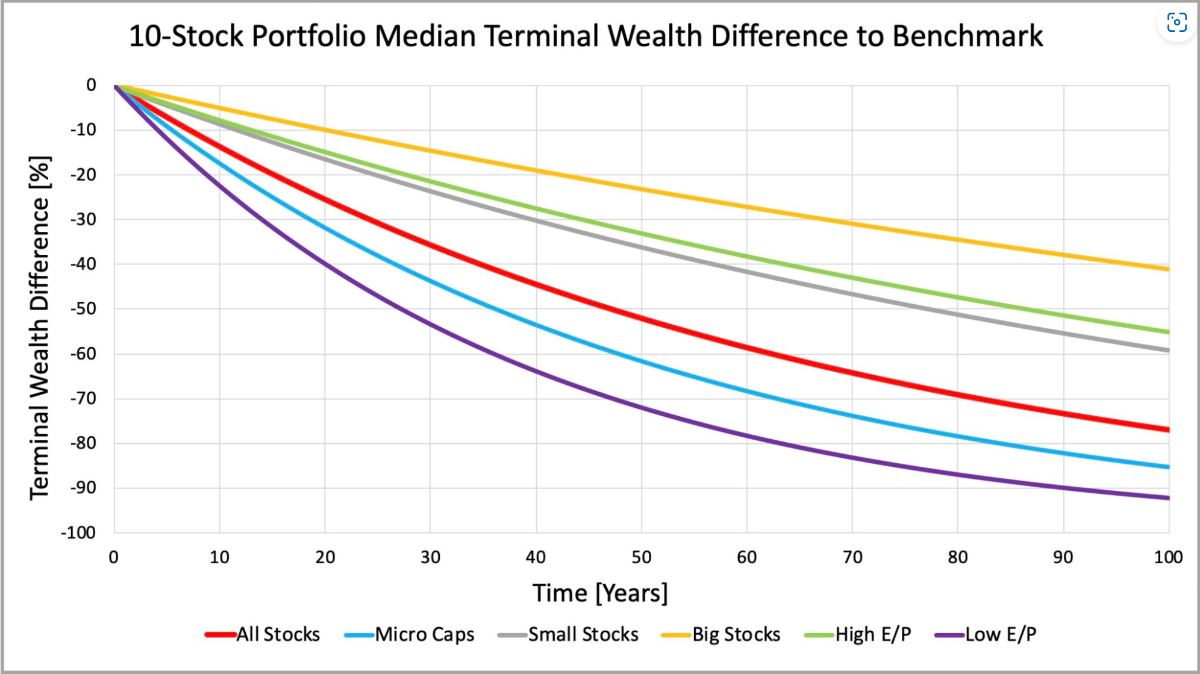

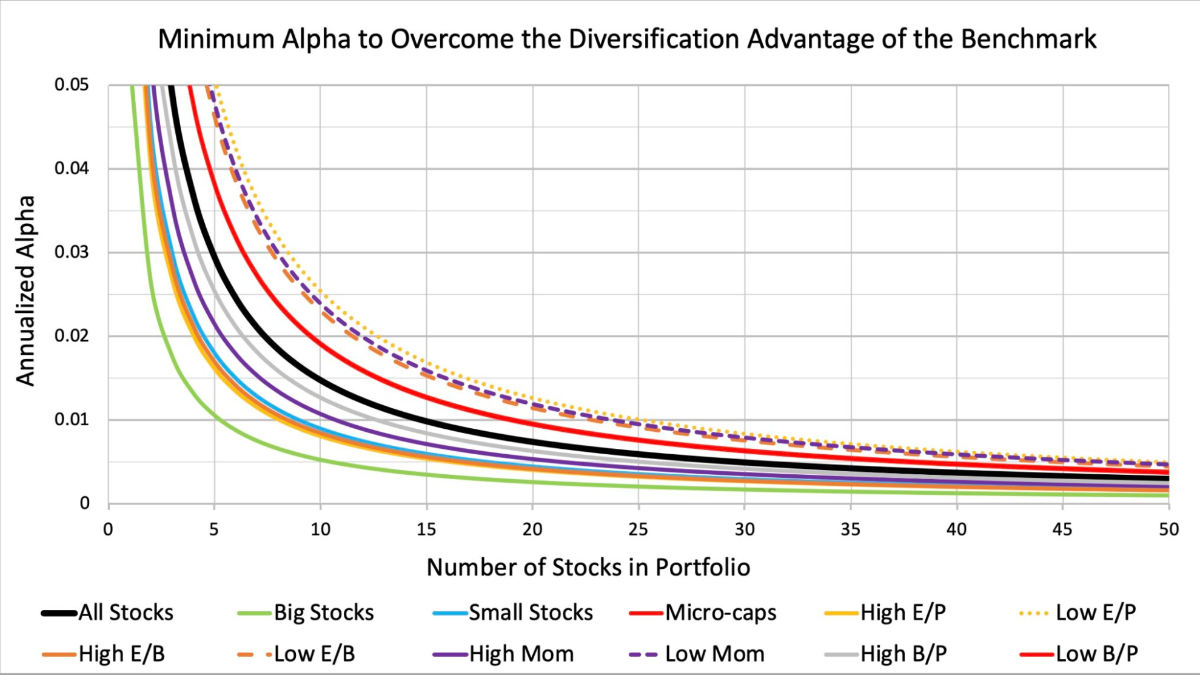

Outcast Beta Blog + Ergodicity, and their implication to portfolio construction The conventional wisdom among value investors is that: 1) invest with a mindset of holding a company's stock for 5 - 10 years, 2) concentrate on your best ideas where you have an edge/circle of competence/unique contrarian insight that is highly probable that you are right, 3) buy below intrinsic value (especially if market implied expectations are particularly extreme) and sell above it. The problem with this conventional wisdom, is that I feel it is incomplete and potentially dangerous to the goal of building wealth especially for the everyday retail investor. This is because it does not take into account the repeatability of a particular strategy in the long-term, nor the fact that long-term, really means one's life expectancy (not the planned holding period of a stock), for a specific individual. Buffett concentrating his portfolio in Coke was a big winner. Other value investors concentrating in Sears was a big loser. Miller riding Amazon was a big winner. Other value investors shorting Tesla was a big loser. Why did it work from some and blow-up others? After reading Outcast Beta's blog and learning about the concept of ergodicity, it gave me a bit of insight on how to think about this a bit more deeply as it pertains to myself as I learn how to construct a portfolio. The first lesson I learned is that survival is more important than performance, and the only way to survive is to have a strategy that I can live with and reproduce in a consistent manner. This strategy will depend on the game that I choose to play, which in turn depends on my own skillset, knowledge base, and temperament (or in the case of professional investors, their clients). This coupled with one's own personal time frame (ie months - years - decades), will govern the interplay between the number of stocks and the degree of leverage (% of stocks in a portfolio of stocks & cash equivalents). The second lesson I learned is that greater the deviance of portfolio from a well diversified index, the wider the distribution of outcomes I will be exposed to in terms of geometric returns, total wealth accumulated, and probability of losing as compared to a benchmark index. The most practical way to minimize this deviance is from diversification. Where I was surprised, was the degree of diversification necessary especially as one's time frame lengthens. In fact, over a 40+ year investing time frame, a randomly-selected portfolio could require > 25 - 100+ stocks to reduce this drag. Interestingly, but not surprising, is that selecting stocks > 20th percentile in market size, cheap, profitable stocks, and having a lower % of stocks in the portfolio reduces the degree of diversification necessary to reduce the variance drag in a less than perfectly diversified portfolio compared to the benchmark. Although not precise, inspecting the graphs in Outcast's blog, it seems that selecting stocks > 50th percentile in mkt cap will reduce the # of stocks by 50%, and selecting cheap, or profitable, or stocks > 20th percentile market cap will reduce the # of stocks by 30%. Starting with the assumption of a 100% stock portfolio, it would seem that ~ 120 - 150 stocks get you close to a well-diversified portfolio. By using the above selection criteria (ie big, cheap, profitable), I would be looking at ~ 18 - 22 stock positions over a 40+ year investing life-time, which is remarkably close to Buffett's punch card rule of thumb for the buy & hold investor. It may also be consistent with Munger's 3 stock portfolio with ~ 5 year holding periods over a ~ 40 year investing life (ie 24 stock positions over a lifetime). In either case, a significant factor contributing to Buffett and Munger's success, is creating ergodicity. This can be done both in measurable and philosophical ways (qualitative). It can be, as shown in Outcast's blog, through diversification in the number and styles of stocks. But diversification can also be done through time, such as a buying a full position of 1 in 20 punch card positions every 2 years when you can find them at a decent price or alternatively accumulating small amounts of your evolving list of 20+ favored businesses over time. Core to this, is avoid the potential of zeros or extremely negative outcomes in a manner than does not cause permanent irreversible damage to your overall portfolio (taking into account future certain cash flows from other sources such as employment). Furthermore, reducing the % of your portfolio that is comprised of VC-like bets, as you age and get closer to the fixed income stage of life also helps, because recovery from future certain employment cash flows is much less likely to rescue you and your portfolio. The other way to create ergodicity is act like a true long-term owner by thinking like one or actually have significant influence in the business. As an outside passive minority shareholder, we have neither the influence or clout to vote away poor board decisions, we can only ride along with management's decisions and choose to accept them at their word or not. Buffett and Munger can take equity positions and by the nature of their reputation, have significant sway in management. Along the theme of ergodicity, is playing games that we can reproduce and games where there are many winners. Copying Buffett and Munger in this regard, doesn't work. So as an OPMI, it behooves us to have a higher level of diversification (# of & through time) than these investing giants. As it comes to "stock-picking", it is more valuable to think about this endeavor more similar to searching and owning a participation in a collection of durable assets/businesses with a historical track record of surviving many different harsh economic realities (quality businesses). As Cliff Asness wrote recently in his paper "The Less-Efficient Market Hypothesis", the markets have become less efficient (so finding opportunities for the skilled investor) has become easier but sticking with what is right is getting much harder (longer to time for the market to realize this value). This got me thinking that being highly concentrated in a small cap value in a foreign market for example, will require significant patience and will very likely cause a long-term drag on your portfolio. It will also require you to ensure that the underlying business is of high quality (highly profitable with a long re-investment runway) and/or management is actively working at returning capital to shareholders. These positions may need to be smaller so that you and your stakeholders don't run out of patience waiting for the re-valuation event. I'll end of this post with some examples of how I would apply the above: 1) Costco/Hermes - punch-card high quality at a stretched valuation - accumulate slowly over time (time diversification for a better price) 2) Fairfax India - owns some highly durable assets in a vehicle that is not particular shareholder friendly at a very cheap price that will have a long-reinvestment runway - own in quantities directly proportional to your degree of patience 3) Stellantis - not a 100-year business that a monkey can run (although founded in 1899), available at a cheap price that is actively returning capital to shareholders hoping for an inflection point of a successful EV transition - own in quantities that won't permanently damage your portfolio if it fails and reduce your time frame of holding on it (not a buy-hold candidate) 4) Fairfax Financial - punch-card quality if the culture stays the same over time available at a very reasonable valuation - having a > 5-10% position is very rational with a 10+ year time frame (large, cheap, profitable)

-

I will check this one out. I've been listen to Driving with Dunne podcast which had a number of good discussions on EVs, China, Batteries and Software Defined vehicles. He had John Wall, SVP and Head of engineering at QNX, discuss his views on autonomous driving. His opinion only but his thoughts are that the liability issue of autonomous vehicles is very much in the air and full driver acceptance may be a ways off. His prediction in 2014 was maybe 2035, but he thinks this is likely still too aggressive (in 2024). His thoughts are that Level 1 --> 5 progress will be incremental with OEMs specifically focused on safety features and a gradual consumer adoption over time.

-

https://x.com/TaylorOgan/status/1833455617798750255 This is a video from Huawei's ADS.

-

@nwoodman @TwoCitiesCapital @rkbabang @SharperDingaan Tagging a few people that might be interested in this video/podcast A few key points: 1) passive indexing creates inelastic markets especially in well-follow large caps 2) passive indexing creates a situation where it becomes increasingly difficult for active managers to outperform 3) as % of market is invested in passive (70-80% threshold), exponential outcomes can occur 4) BTC is not the solution because it doesn't have a profit incentive because supply is fixed and ultimately the largest player will dominate BTC holdings

-

Thanks @nwoodman for the summary. This got me thinking about the whole paradox of skill and the distillation of the best of the best investors surviving in this globalized hypercompetitive market with all this fee compression from passive fund flows. The questions in my mind are: 1) with more skillful active investors out there, will it require fewer and fewer % of active mangers needed for long-term value discovery? 2) with democratization of investing, social media, will this counterbalance/offset the challenge of creating alpha? 3) will reversions to intrinsic value be faster for large cap/well followed companies and slower for those underfollowed (small cap)? If Mauboussian is right about luck playing a more contributory role in investing outcomes, how do investors maximize this? - being a generalist (cross-industry model thinking) - willingness to tolerate larger cash balances - ability to wait longer without pressures to investing from LPs - creating a lucky network (see attached link) (5 Ways to Create Luck in Investing and Life - Safal Niveshak)

-

As people have pointed out mathematically and examples from reality regarding difficulties with capex decisions and their respective execution, I am not sure that this simplification regarding capital lite good and capital heavy bad dichotomy is necessarily accurate. I think it depends on the type of product and the level of competition. If competition is absent or minimal (eg railway monopoly or oligopoly), a significant amount of capital invested in real tangible assets that are difficult to replace, all but guarantees a certainty in future cash flows with a very long tail could be quite desirable. Conversely, in many software businesses where it is asset light, but the product is a commodity or the competition is fierce, coupled with the fact that human capital is potentially very expensive, the cash flows may be more elusive than one thinks and the growth runway is shorter than it seems at first glance.

-

STLA

-

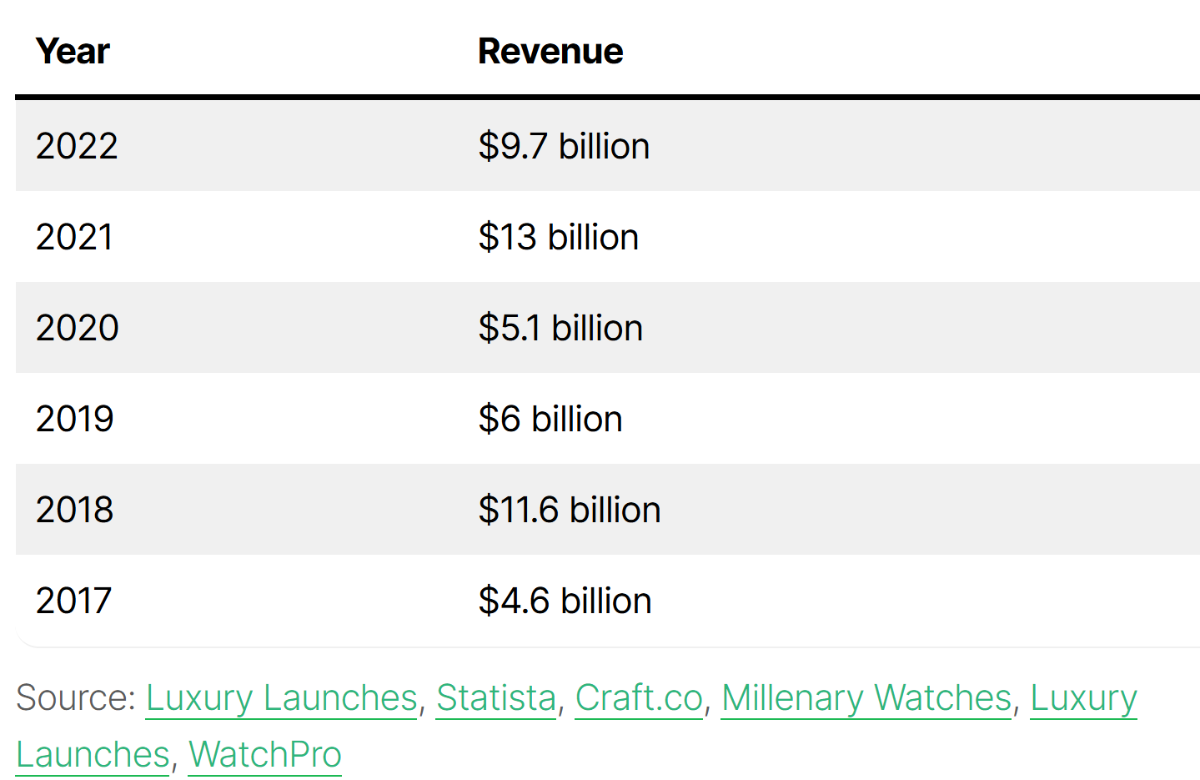

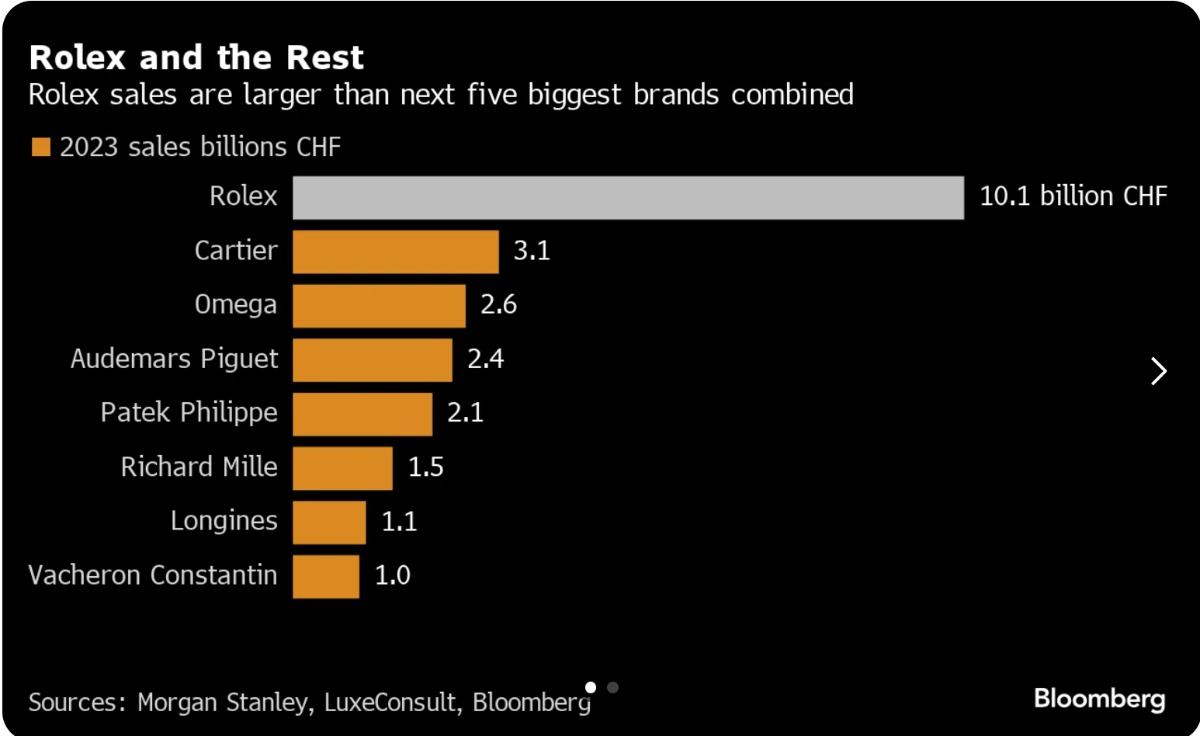

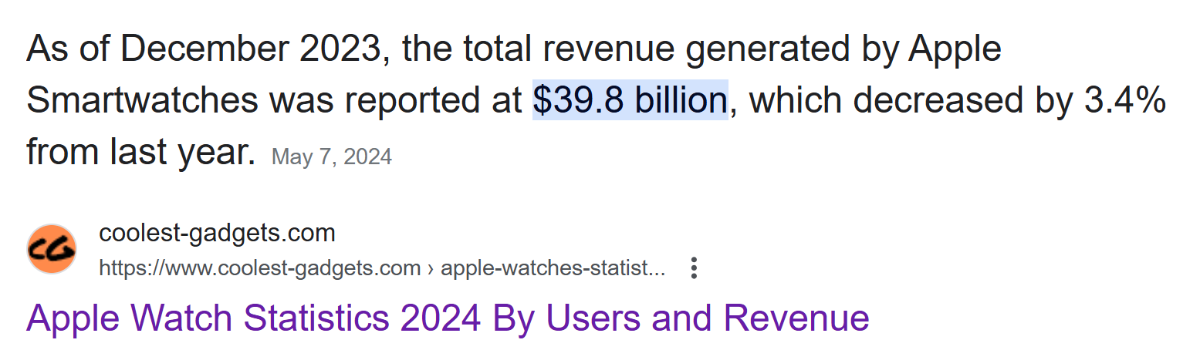

How much would you pay for untapped pricing power?

jfan replied to jfan's topic in General Discussion

Rolex revenues (USD) 10 billion swiss francs = $11.25 billion USD I think the same was said about the luxury watch marker when the quartz watch came out. Business breakdowns had a nice podcast on the history of Rolex. Can you own both? I think you can. Will you use them differently? Probably. Will you pass on your Apple watch to your heirs? Low probability. Just speculating, perhaps, the luxury watch brands, will become even more coveted because they are becoming more scarce and Apple has paradoxically increased their brand value by taking over the middle-tier markets.