jfan

-

Posts

539 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by jfan

-

The blockchain war book is particularly interesting and ties in many of the debates we have here: 1) payment system vs non-sovereign money 2) A centralized system of power vs a decentralized system of governance Book describes 2 camps within the bitcoin ecosystem, big blockers and small blockers. This debate arose because of the amount of data that each block can contain is 1 Mb which causes a limitation in scaling the BTC network as a payment system. Interestingly, the big blockers comprised mostly of the China miners/mining equipment developers/big mining pools/many American-based crypto exchanges (Coinbase), and those representing big business focused on a non-Visa payment system. The small blockers comprised primarily of developers and those that wished to create a new decentralized money (their ethos was open-source, network community consensus on the underlying rules). The author describes the big blockers having a shorter time frame, believed that amount of hashing power represented the degree of influence they should have, and their understanding of the computer science was less skilled than the small blockers. Whereas small blockers were better programmers, and promoted safe coding practices not to risk disruptive hard forks, replay risk, etc in addition to their focus on network consensus of both validating and mining nodes before changes could be enforced. Both sides played by the rules of engagement and dirty as well. Bitmain was not a paragon of ethics and secretly had an IP that was called ASIC boost, that allowed their miners to hash more efficiently and helped them have a profitability advantage. Segwit was a smaller blocker BIP soft fork initiative, that effectively increased the blocksize to 2Mb without increasing the 1Mb limit (don't ask me how). However, Segwit would neutralized ASIC boost's ability to use less electricity. The code base is maintained on Github by a few smaller blockers (1 main person at the time of the books writing), and there were several Reddit, Bitcoin talk, email lists, that discussed these issues (some maintained by small and others by big blockers). Ultimately, the smaller blockers won, but this outcome wasn't because they were any better at strategy and programming skill. They made some gambles that could have turned on them very badly if the big blockers saw these opportunities, if the big blockers had better computer science skills, if ethereum had not undergone a controversial hard fork that was very disruptive to recover stolen ETH by a hacker at around the same time this debate was occurring. Long and short of it, I think BTC will always be faced with politically/economically self-interest entities that want to centralize it in additional to the technical/developer risks of keeping BTC functioning on a decentralized manner. A complete history of Bitcoin's consensus forks - 2022 Update | BitMEX Blog Below is a problem that is yet to be fixed Long and short of this meandering post coupled with @wachtwoord's paper above, a few things come to mind. 1) payment systems don't accrue value like a store-of-value function, but big centralizing forces will always be a threat because they will capture the most value if BTC is mainly a payment system 2) how decentralized are the full nodes in the network out there? 3) who is going to update, maintaining and provide the necessary solutions for bugs, soft forks as this technology progresses through time and scale?

-

@Luca I came across this short article that you might find interesting regarding the value proposition of Bitcoin. Bitcoin's unique value proposition | BitMEX Blog There are a number of technical articles as well here. I downloaded the Block Size Wars - The Battle for Control Over Bitcoin's Protocol Rules by Jonathan Bier. I just started it, but it shed some light behind the scene of its development. You might also find it helpful.

-

Research Archives | BitMEX Blog Came across this site recommended by Nic Carter from the author of Blocksize Wars.

-

What are people's thoughts on Marathon's slipstream offering? Is this a threat to transaction censorship or preference to certain transactions?

-

2024 Crypto Crime Trends from Chainalysis I have not read this one specifically yet, but have come across prior articles from the same group addressing this topic.

-

@Cigarbutt I'm not particularly tech savvy, but you can spend a few hundred dollars and build your own node as well as a nerdminer/bitaxe miner to learn about how the network works. Below are some sites to buy simplified DIY miner parts, or you could go to their respective GitHub sites. NerdMiner - bitronics.store Bitaxe My son and I built a raspberry pi used umbrel os to spin up a node. Umbrel - Personal home cloud and OS for self-hosting We spend a lot of time pontificating about why the price should or should not go up, but I think it might be useful to experiment with the user-facing technology to better understand the value proposition (if there is one) since BTC does have global reach. Hope this helps.

-

Yes, thank you this article.

-

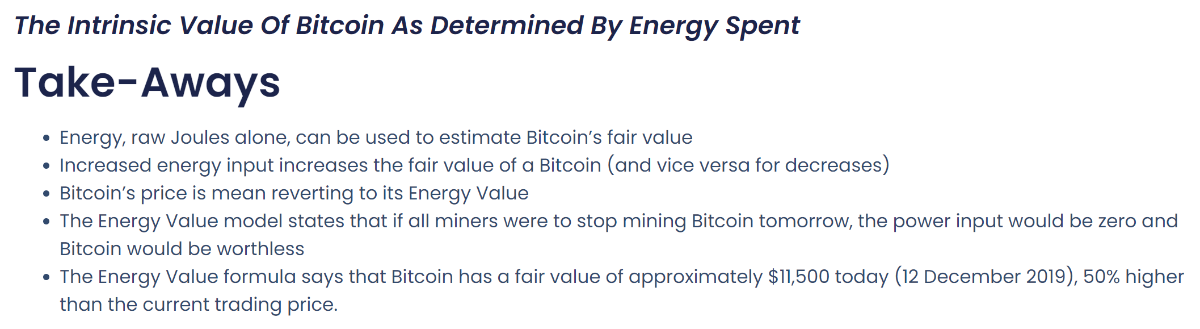

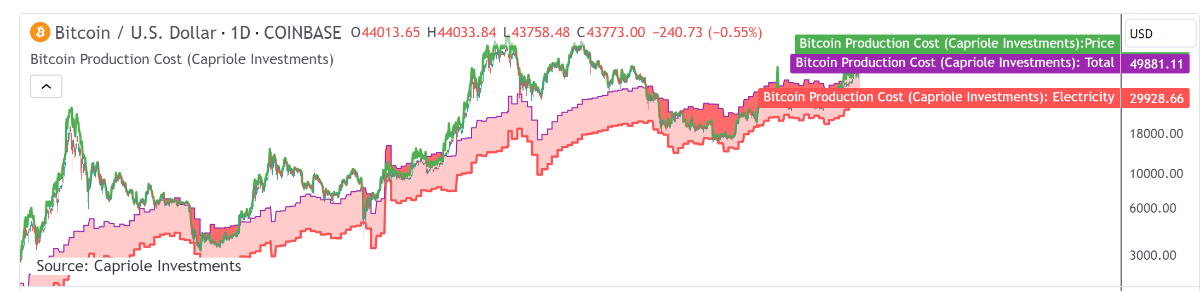

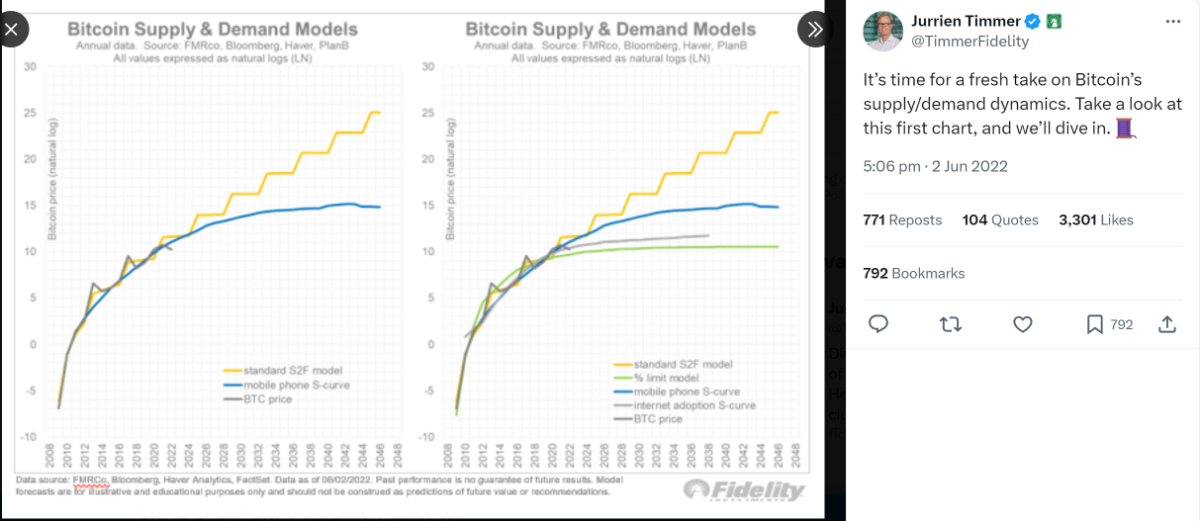

@Cigarbutt Here are a couple threads on BTC valuation 1) Capriole Investments | Bitcoin Energy-Value Equivalence From the same author with his model visualized on tradingview Bitcoin Production Cost — Indicator by capriole_charles — TradingView 2) Jurrien Timmer from Fidelity has a bunch of supply, demand, and valuation models that he posts on Twitter. 3) The Rational Root on X has some cool charts from on-chain data and price movements.

-

I know some find this show a bit polarizing, but here is a video on bitcoin mining in Africa discussing it potential impact (use of stranded energy sources and its impact on stabilizing energy supplies for the local populace). At the end, they discuss a South African company that can facilitate BTC transactions/storage without the internet. I've attached Gladstein's article here as well. Stranded: How Bitcoin is Saving Wasted Energy and Expanding Financial Freedom in Africa - Bitcoin Magazine - Bitcoin News, Articles and Expert Insights I have not fact checked the article below, but this is an interesting article on this country's investment arm treatment of bitcoin mining. Ethiopia To Become The First African Country To Start Bitcoin Mining (forbes.com) I think this may be how BTC addresses the Cantillon effect to some degree. Here in the West, we have no pressure to adopt or innovate around the technology, we are more concerned about it as an investment, its mainstream financialization, but in the ROW, there can be a different focus.

-

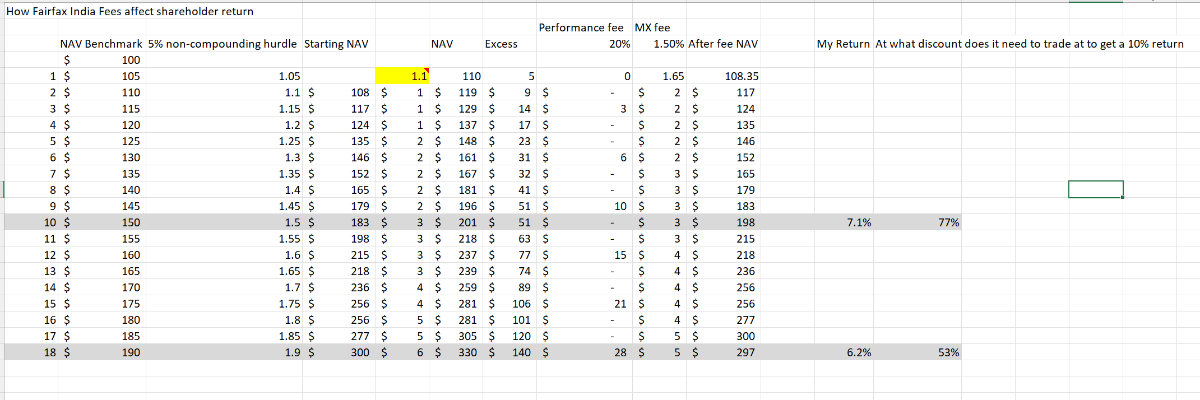

Perhaps this is already explained above in this thread. I was just trying to figure out the impact of the fees on their returns. Is my math off here? If everything was market to market instead of market to private valuation, this should normally trade at a 23% discount + hold co discount (?20%) or 57% of NAV normally given the high fees. So this implies that their true NAV needs to be at a minimum > $26/share to get a 10% return at a current market price of $15/share. To get a 15% return over 10 years, the market price needs to be at 30% of true NAV, or an intrinsic value of $50/share at current market prices.

-

For those interested beyond just the money go up or down aspect of BTC, I came across a few neat videos on how the user experience is changing. I'm used to purchasing BTC from regulated exchanges and online brokers as well as storing on Ledger hardware wallets. There are a number of open source desktop wallets that you can download and use. The one i particularly like is Sparrow wallet. It has a really nice user experience and easy to connect with your own node. Specter wallet is another good quality standard. Nunchuk and Blue wallet have both desktop and mobile options. The hardware wallets are also evolving as well. Air gapped wallets with and without private key storage are now available and can interact with the above desktop wallets. Seedsigner is interesting as it can be built with parts totally < $70 and communicates with QR codes with your hot wallet devices. Coldcard uses microSD to airgap. Keystone pro 3 is the fancy version for these functions and extends to altcoins. Both these desktop and hardware wallets can create multi signature options to enhance security.

-

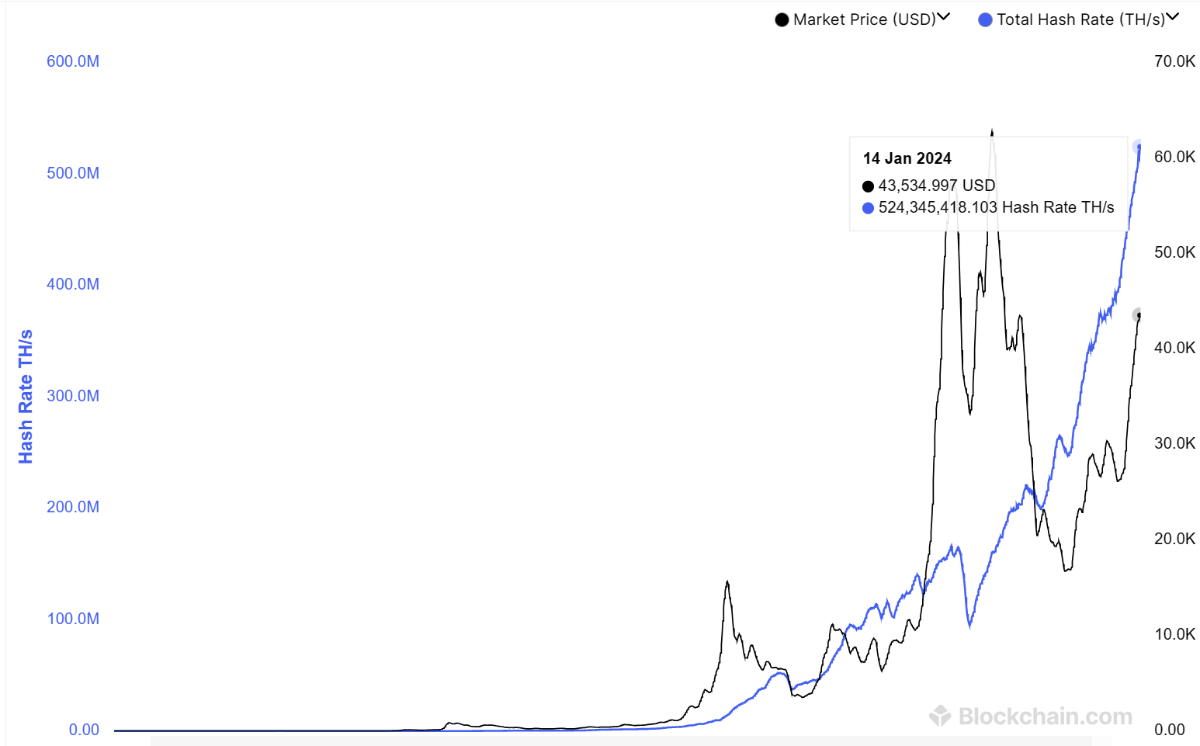

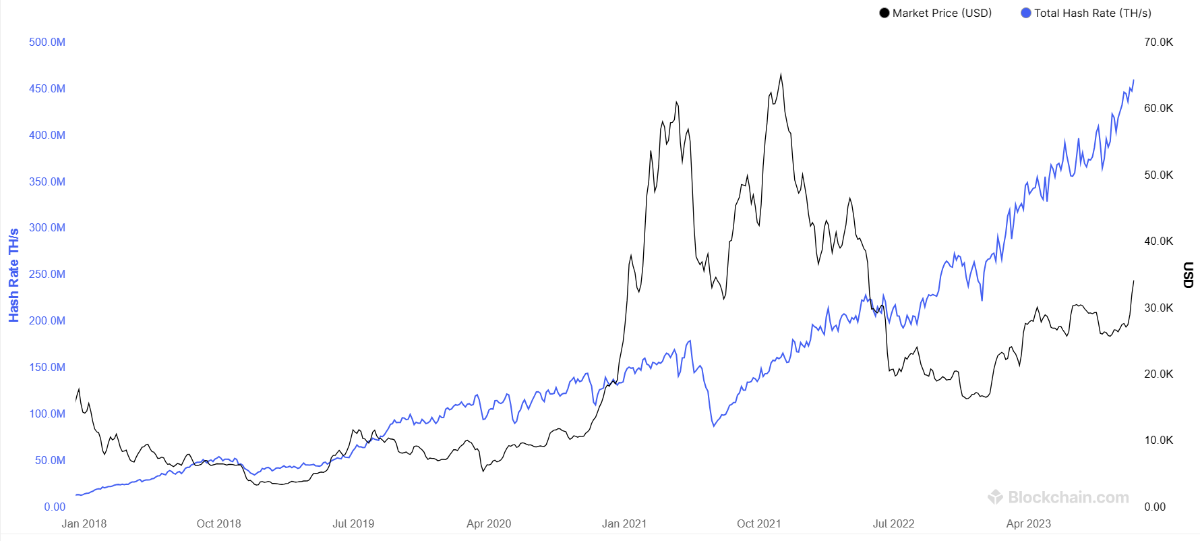

For me the biggest drivers are the continued total network hashrate increase along with the halving of the block reward after April.

-

I haven't dove deep into the public miners that out there but did quickly glance at Riot's and Marathon's 10-K. It doesn't seem to me that they do much hedging of their BTC to "sell their BTC" without dipping into their BTC treasury. Riot does hedge their power-purchase agreements and sells BTC to pay for employee compensation and likely capital purchases. Marathon has this in their filings and doesn't have any hedging/derivatives at first glance. Arguably, if their cost of mining is far less than $40K/bitcoin, and the market BTC price is dependent on least efficient miner, then these mining companies should be profitable even when the market price dives. Furthermore, they could selling their profitable BTC over time to obtain more efficient mining equipment without ever needing to hedge and likely still get to hodl most of their mined BTC. For fun, I did check out how many 140 Th/s miners I would need to have a chance to mine a block within 1 year. It would take 100 miners to mine a block in 301 days. With the state-of-the-art most efficient miner costing $14/Th, the start up cost would be $196K + operating costs. SoloChance.com - Solo Mining Chance Calculator wrt to Professor George's article, despite his stance on that only cash flowing businesses can have intrinsic value, I am glad that he did some research on how the BTC network functions, and am hopeful that he continues to dig further. Everyone has to start somewhere.

-

Here is an article from Professor George on this topic in the globe and mail. bitcoin-globe.pdf

-

My best guess is fair value is around $42k today. By the end of 2024, $100k. Ps thanks for the ETF response

-

I'm a bit confused about the difference in cash redemption vs in-kind ETFs. My basic understanding is that cash redemption requires the ETF to go out an purchase BTC with the cash they have in hand vs in-kind, allows the ETF to find a market marker that can exchange similar assets with others. Is my understanding correct? If it is the cash redemption, would the implications mean that the number of transactions at the base layer also increase in volume and so will the transaction fees due to higher demand?

-

BN

-

I think this might be a very good point. There can be things that add alot of value but can't capture any of it. Just off the top of my head, businesses such as WhatsApp and Spotify, add value but can't capture it. Meta paid >$20 billion for WhatsApp in 2014 but it has not been successful thus far in generating revenue, free cash flows, etc. But with a 1.5 billion users, this messaging network is undoubtedly created lots of value but what is the right monetary premium? The BTC network scales as people find it useful to store/transfer wealth relative to other monies that they have access too. Will this increasing demand necessarily the monetary premium? I'm not sure that there is necessarily a linear relationship here, as it will depend on the prices of commodity inputs necessary to secure the network and the progressive energy efficiencies of the technology. I could imagine that if there was a sudden abundance of cheap energy, silicon, and step change in mining efficiencies, despite increased demand, the prices could drop or moderate downward.

-

@ValueArb Thanks for elaborating on your experience wrt to your bitcoin transactions, and perspective. Initially, it seemed that your posts had an adversarial edge to them but your later posts were much more helpful understanding your point of view. I really do appreciate having a healthy genuine debate helps get to the truth of a matter. I thought I might include a couple quotes from Ben Graham about speculation and investing. According to Devil takes the Hindmost, Chancellor describes how pre-1920s, bonds were considered investments and stocks were speculative. When stocks became more accepted, the yardstick of valuation hinged on 10x earnings and expected dividend yields. Around mid-1920, Edgar Lawrence Smith published a statistical analysis of investment returns for stocks vs bonds from the mid-19th century onward dispelling the myth that stocks were not investment worth relative to bonds. This changed the feeling of market participants, allowing them to perceive that stocks could be viewed as investments. Around this time, the concept of discounting future earnings was the new way of valuing stocks. Ben Graham is quoted to have said: "the concept of future prospects, and particularly of continued growth in the future, invites the application of formulas out of higher mathematics to establish the present value of the favored issues. But the combination of precise formulas with highly imprecise assumptions can be used to establish, or rather to justify, practically any value one wishes, however high, for a really outstanding issue....The more important the good will or future earning-power factor the more uncertain becomes the true value of the enterprise and therefore the more speculative inherently the company stock...Mathematics is ordinarily considered as producing precise and dependable results: but in the stock market the more elaborate and abstruse the mathematics the more uncertain and speculative are the conclusions we draw from them." From read these quotes, it seems that Graham thought that trying to estimate future cash flows was a risky and speculative endeavour. But in today's conventional understanding, valuation is all about discounted free cash flows and very little else. Perhaps it is better to utilize Graham's above definition of speculation as it seems there are many on this board that would disagree that commodities (precious and base metals), land and other assets with no immediately visible cash flows, can't have an intrinsic value. Perhaps I'll leave a couple other quotes to consider: "Strong Opinions Weakly Held" - Paul Saffro "The smartest people are constantly revising their understanding, reconsidering a problem they though they'd already solved." - Jeff Bezo

-

The volatility of the price in USD is particularly obviously high but if the value of BTC is ultimately driven by the market price of electricity and equipment to secure the network (using a proof-of-work protocol) the key variable to watch is the hash rate. As depicted above the hash rate is steadily climbing over time. Just like everyone on this board says that the market price does not necessarily reflect the fundamentals of a business and that this year's sales is not always a true reflection of a company's earnings power, we should not be particularly wed to the price volatility of BTC in USD in the short-term.

-

This is a great question and one that is so relevant that I also have been struggling to solve. I think it is a combination of your mental/emotional make-up, your portfolio limitations, and how you manage your cash. I try to be rational but I find that I'm generally too emotional and experience too much buyer's remorse and FOMO for my liking. I personally find devising a pre-planned buy/selling strategy and automating it helps reduces my bad behaviors vs trying to making on-the-fly spontaneous transactions. I also struggle with balancing having cash on the side-lines vs having to sell out existing positions to fund better new positions. After some reflection, I've been trying to adjust how I build up a position so that I can minimize my sub-optimal behaviors. Far from perfect, and still field testing it, my approach (at least the one I'm trying to refine) is: 1) Ask myself the following questions: a) To what degree do I understand this asset, the people, and industry (low, moderate, high) b) To what degree can I change my mind (depends on your own mental make-up) and reverse my position easily (depends to a degree on trading liquidity) (very hard, ok, very easy) c) To what degree can I see identify the downside, upside, and certainty of when the value realization will occur (1 out of 3, 2 out of 3, 3 out of 3) 2) Depending on the answers to my questions above, I have the following tools to build a position in the portfolio a) dollar cost average at market prices on pre-planned days over a time frame (if there is a catalyst - shorter time frame, if there is none - a longer time frame ie 2 years) (and to some extent depends on the volatility of the share prices - very volatile, shorter buying intervals, not volatile, longer buying intervals) b) a variation of the @Parsad method. If the current price will get me a 10-15% return, I initiate 10 - 30% of my ultimate target position size. At fixed % price declines, I buy increasing amounts with a willingness to go 30% over my ultimate target position size. This way I will average down to a price that might be 10-20% in the red relative to the market. At this point, the stock price expectations of the fundamentals need to be quite pessimistic AND I have to believe that this is not truly reflective of reality. This way, the stock price only needs to compound 2-4% annually over the next 5 years for me to break even. c) Or a combination of the 2 tools above 3) With respect to cash "dry powder" management, I still struggle with this as I don't like to use margin but I appreciate that time in the market is important, and the opportunities to buy and sell don't necessarily coincide with each other. I think it is reasonable to always have 5% in cash for optionality even if my bank account pays little interest but this is balanced by the fact that it gives me true flexibility. If cash builds up greater than 5%, I think (I haven't quite implemented it yet), to have some index equivalent to park the funds in and use this as funding source when the time comes. An alternative that I've been toying with is, instead of an index etf, to buy a basket of global stock exchanges as a proxy for the trading activity of the underlying index stocks. If an index is hot both on the upside and downside, the exchanges will do ok either way (a Murray Stahl idea) I don't know if this answers your question but these are some of my thoughts on this subject.

-

JOE

-

Spotify

-

Wintaai/related parties own/will own securities associated with Loggerhead Reciprocal Interinsurance Exchange. A couple of articles discussing Loggerhead assuming renews from Progressive Florida customers. Progressive looking to move homeowners' policies to new insurer (wptv.com) Progressive rebalances homeowners’ book, diversifies away from Florida (insidepandc.com) Progressive rebalances homeowners’ book, diversifies away from Florida Farhin Lilywala - September 29, 2023 Progressive is rebalancing its homeowners’ book by non-renewing roughly 47,000 DP-3 and 53,000 high-risk homeowners’ policies in Florida, this publication has learned. The carrier’s strategy is to diversify away from its exposure in Florida. Progressive is exiting its non-owner-occupied book and discontinuing writing DP-3 policies in the Sunshine State. The carrier is also terminating a handful of agent appointments for its home product, accounting for 15,000 policies. The first non-renewals are scheduled for May 2024 and will continue for 12 months after. Progressive will have 200,000 property policies in force remaining in the state. Start-up reciprocal Loggerhead will offer renewals subject to its underwriting and financial standards. Agents will have to opt-in to allow renewal to Loggerhead. Last year, Loggerhead was launched as a reciprocal exchange in Florida by Todd Dixon and Jim Santo, two former Auto Club Group executives. In December, the company acquired Bankers’ Florida homeowners’ book of business. In a statement to the publication, the company said: “Florida property remains an important part of our Progressive Home business, and we have no plans to leave the state. However, we have been working collaboratively with state officials and the Florida Office of Insurance Regulation to implement changes that allow us to rebalance our exposure while continuing to serve Florida homeowners. While we know these changes are not welcome news for those that are directly affected, we’re encouraged by and grateful for the work of Florida state officials who recently helped enact needed legislative reforms that are stabilizing the insurance business environment and encouraging new carriers to enter the market. We’ve been able to identify a current property carrier, Loggerhead Reciprocal Interinsurance Exchange, in which we have entered into an agreement with to offer replacement policies to affected policyholders of our rebalancing decision subject to their underwriting and financial standards. The actions we’re taking are necessary to ensure that we can continue to write business in Florida in a meaningful way—and we expect these actions will better position us to build a stronger, more stable, and more competitive Progressive Home business for consumers and independent agents in the long run.” The announcement follows news this week of Nationwide sending out non-renewal notices impacting 10,525 North Carolina personal lines policies up for renewal from December 2023 to July 2024. Of that number, 5,781 of the policies will be non-renewed based on their risk profile according to the carrier’s hurricane hazard assessment tool. The remaining 4,744 policies will be referred to the North Carolina Insurance Underwriting Association, also called the Beach Plan, the state’s last-resort insurer for those who can’t obtain coverage through the open market.

-

This is from a well followed financial educator that my work colleagues follow intently on social media.