nwoodman

-

Posts

1,892 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Thoroughly agree, one of my favourites. I have watched it a couple of times. Interesting to see it’s now on Amazon, I think I came across it on free to air during covid and ended up buying it, to avoid ads. Dark, gritty, and reminds me of so many great movies/shows but still unique storytelling. Glad you are enjoying it. -

So including divs FFH @ 1x’s book is a 12% CAGR. Interestingly this is close to my base case. Still plenty of room for P/B expansion and earnings growth. Extraordinary really. Thanks for the graph.

-

Thanks @Viking, the alpha is impressive. Always nice to see a position like OXY showing up that is in the "I wish I had done that, but it doesn't matter because Fairfax did".

-

Thanks, always good to see another example of a rational capital allocation coming to light

-

Nah, should have had my morning coffee before posting There has been some rumours doing the rounds about the ECB raising the minimum reserve requirements (MRR). Morgan Stanley did some modelling attached, TLDR minimal impact on Eurobank. I guess I am just a little surprised as I figured this would be up and to the right given the low valuation but Greece has been suffering their share of misfortunes of late. eemea_20230919_0946.pdf

-

Why buy for $1 when you can pay $1.20. I am not not surprised the share price went down considerably. Still under book (€1.99) so will be accretive but I am speculating that it buys some political good will down the track. I was really hoping they would get this done around market value of say €1.50-1.60 rather than €1.80 https://www.ekathimerini.com/economy/1220864/hfsf-launches-disposal-of-its-stake-in-eurobank/

-

Further to this SEBI is under the pump and in a bit of a transition phase. Madhabi Puri Buch took charge of the regulator in March 2022. She is the first non-bureaucrat to hold the post and is trying to put in systems to ease the bureaucracy. It sucks but from everything I have read there has been a few go rounds on the IPO but no show stoppers. The conversion and IPO are tied at the hip IIRC. Edit: Not excusing the situation. It must drive the team at Fairfax nuts at times. However I am sure they sleep easy with the recent life insurance license approval from the IRDAI. To me this gives them a massive play, once they have scale on, much needed infrastructure. Very accretive to their view of what constitutes a 100 year business.

-

Exactly this, I don’t want to dumb down the conversation but what they do with the windfalls of Bradstreet’s genius is key to a sensible P/B multiple. Is the equity allocation machine functional and rational as the bond machine? On balance I see somewhere between sensible to “it was great to be invited”. Deal flow is key. Nice to see Mr Market appreciating some of the great unwashed though. @viking apart from the minor quibble of whether P/Es are relevant you have been incredibly helpful. Also glad to see you are confident in your own analysis to stop trading in and out. If IRC this is your main gig, so you are doing your family proud

-

Fascinating that this popped up on my youtube feed today too

-

Great thread by the way. I should have paid more attention

-

Corporate governance reforms too. Earnings growth and a flicker of inflation is predominately due to the weaker yen. So not 100% convinced that a rising yen actually makes this market more attractive to US buyers as it may well tip it back into deflation. What I am seeing though is a shift from pure survival bias to something more positive and dare I say it competitive. Certainly quality companies still seem cheap on most metrics when compared to similar US equities.

-

Appreciate the feedback. I totally agree with your basic premise around Japanese value traps. Our difference in views around potential growth from both the recent acquisition of Iveric and subsequent minor positions is what makes a market. Thanks again.

-

Building out Japanese positions on a basket basis, my aim is to get to 15%. Then came across some broker coverage that lead to a deeper dive. Management change earlier this year lead to their chief strategy officer becoming their CEO, this also sparked interest on a qualitative basis. Read growth bias. I think they might have overpaid a little bit for Iveric but that seems to be common knowledge. However they got early clearance on Avacincaptad Pegol (“ACP”). None of this is new but I do like the new CEO’s focus on some of the recent minor investments with benefits. Looks expensive on a P/E basis until you consider the flow on, this might be a P/E 12 in a year or two vs a P/E 37 now. Also the pipeline looks promising for future growth read 3-5 years with a a focus on various cancer cures. This is not without major risks, just ask Apellis shareholders who are the competitors in the USA to ACP, where Syfovre, may have some secondary concerns around retinal vasculitis (or inflammation). It’s a Pharma so caveat emptor. It just happens to be one of the top 5 in Japan https://www.globaldata.com/companies/top-companies-by-sector/healthcare/japan-companies-by-market-cap/

-

Interesting to see the sleeper that is Helios Fairfax getting some interest Anyone seen any news? @glider3834 you are normally ahead of the curve

-

Astellas Pharma 4503.T

-

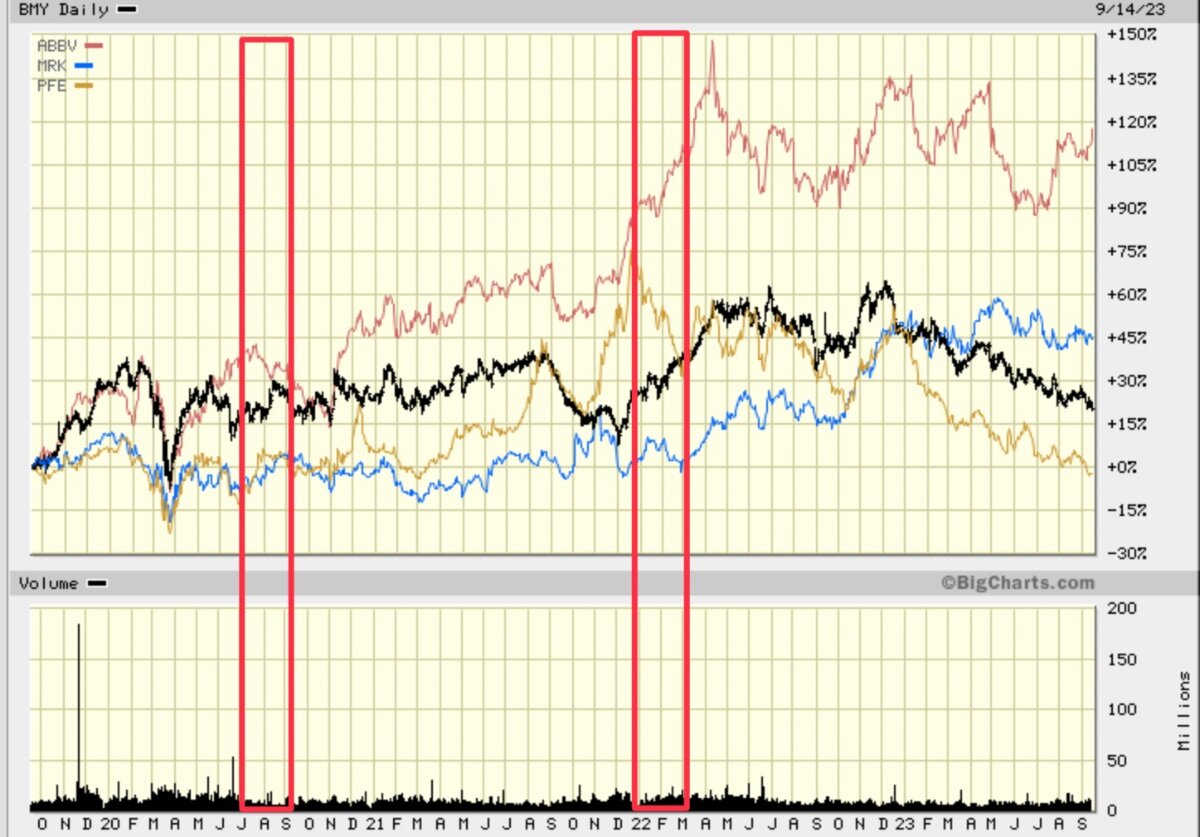

I haven’t followed it closely but I believe the stakes were disclosed in the Q3 2020 13F AbbVie, Bristol-Myers Squibb Merck, Pfizer He exited Q1 2022. So hardly buy and hold short article discussing the fact that he brought up in the idea of the pharma basket in the 2000’s https://markets.businessinsider.com/news/stocks/warren-buffett-berkshire-hathaway-buy-4-pharma-stocks-20-years-2020-11-1029815931 Exit article https://www.fiercepharma.com/pharma/buffetts-berkshire-backs-out-three-big-pharma-holdings

-

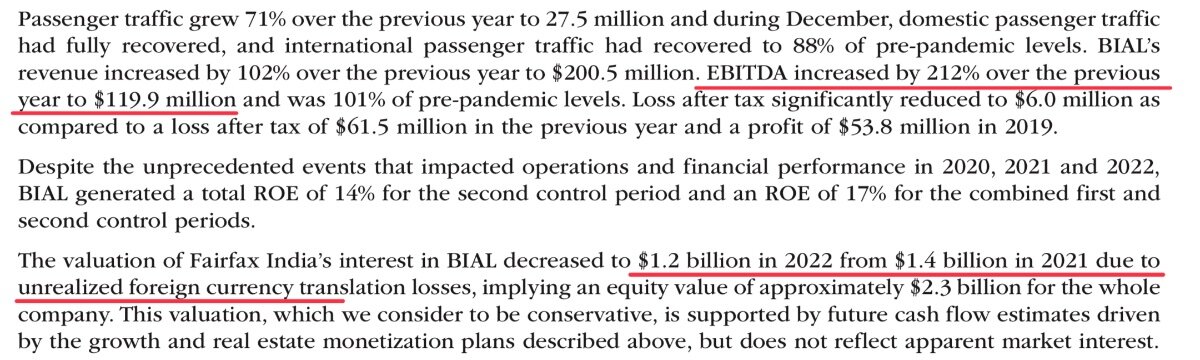

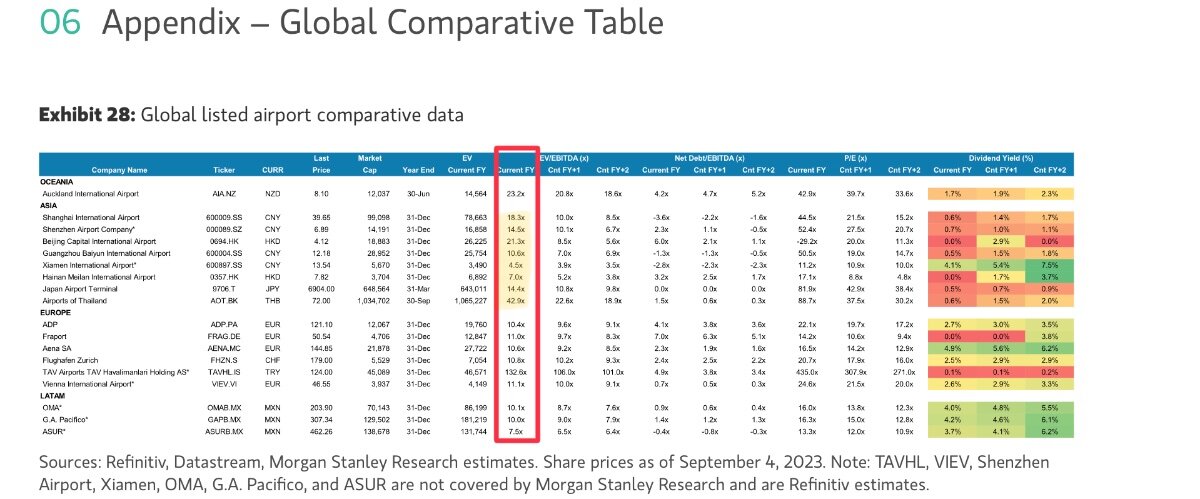

@glider3834 thanks for that. There is a good reason why we all think it is the jewel in the crown. 19x’s EBITDA of $120m to get to a valuation of FY22 $2.3bn is getting up there in terms valuation but not completely egregious given the growth this year and the future prospects. Cargo is another area that may surprise on the upside, it seemed to figure prominently in the recent Foxconn announcement. airlines_20230906_0440.pdf

-

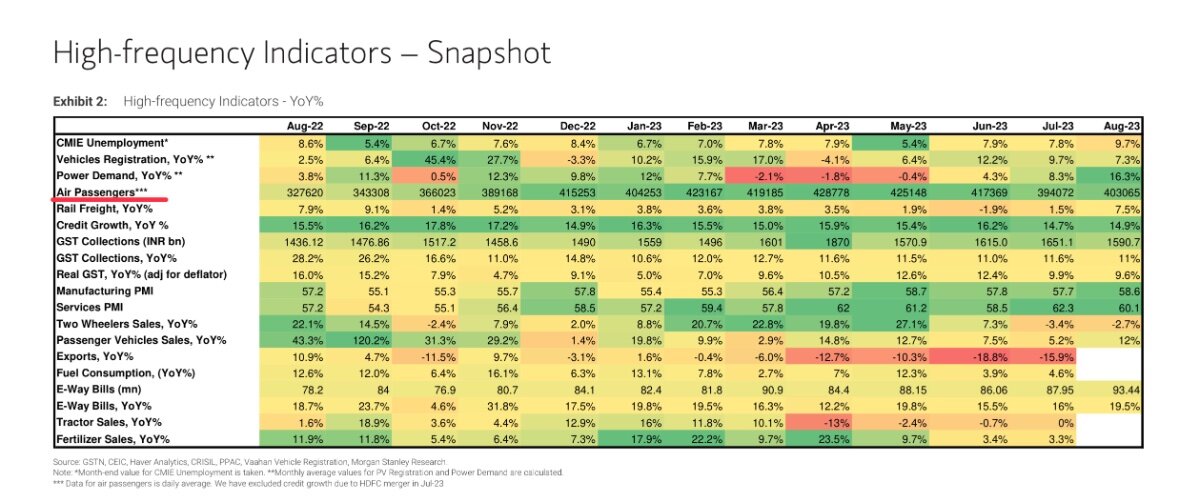

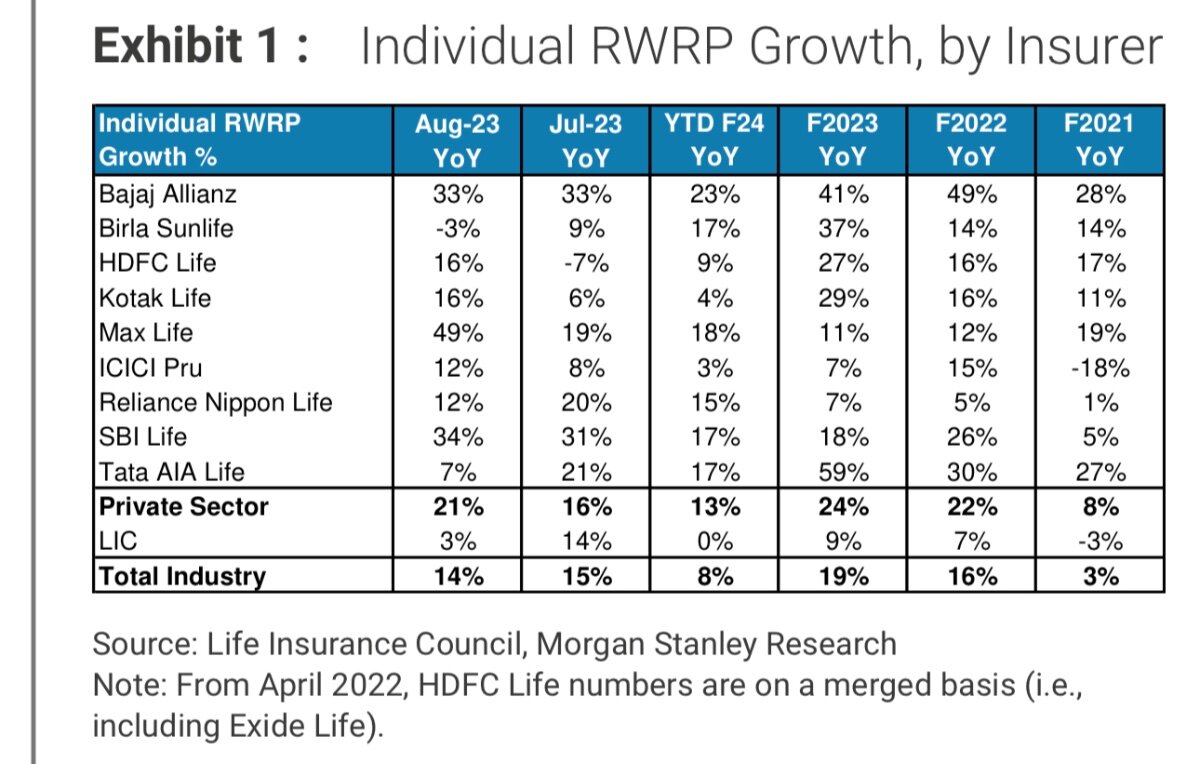

MS out with a note on August figures for Indian Life…industry growing like a weed. Looking forward to seeing Digit in this table ASAP india_20230907_1625.pdf

-

Small (<1%) positions in each of Buffett’s 5 Sogo Shosha 8001.T, 8002.T, 8031.T 8053.T, 8058.T

-

Thanks hadn’t seen that one. Even 1x’s P/TBV doesn’t sound stretched. Very bullish indeed. Short of some catastrophe, Eurobank alone should get written up by around USD1B in the next couple of years. I was always a little suspicious of FFH’s stated book value but there is certainly no shortage of examples to the contrary.

-

Thanks for this. Seems like a good deal. I was surprised there wasn’t a mild increase in MS PT but as you point out it is more a 2025 story. Love that deferred gratification. Foran Mining hitting ATH too. Have a great weekend all

-

Added to 7974.T Nintendo (now 5%) New position 6758.T Sony (~1%)

-

After the horrendous fires this is a real kick in the teeth “Torrential rains have flooded homes and roads in Greece. Storm Daniel has battered western and central parts of the country, prompting hundreds of calls to emergency services to pump out water” https://x.com/reuters/status/1699082462754668929?s=61&t=DXjj7hLwsZeynV3C6VIPzA “And it may only be getting worse for the region in the coming days. Weather forecasting site Severe Weather Europe says that Daniel could lead to the development of a medicane, a "tropical-like cyclone" in the Mediterranean. Weather models show such a system could form over the Ionian Sea this week, the forecasters said, as an ongoing marine heat wave fuels extreme weather. Medicanes usually need ocean temperatures of 26 degrees Celsius, just under 79 degrees Fahrenehit, to form, the forecasters said, and there has recently been "more than enough warmth in place to support the sub-tropical development." Weather models show that if it does form, it could bring wind gusts of roughly 62 miles per hour. It's unclear if it would be closer to Sicily and Malta or the Libyan coast. “ https://www.cbsnews.com/news/greece-historic-flooding-more-than-2-feet-of-rain-in-just-a-few-hours/

-

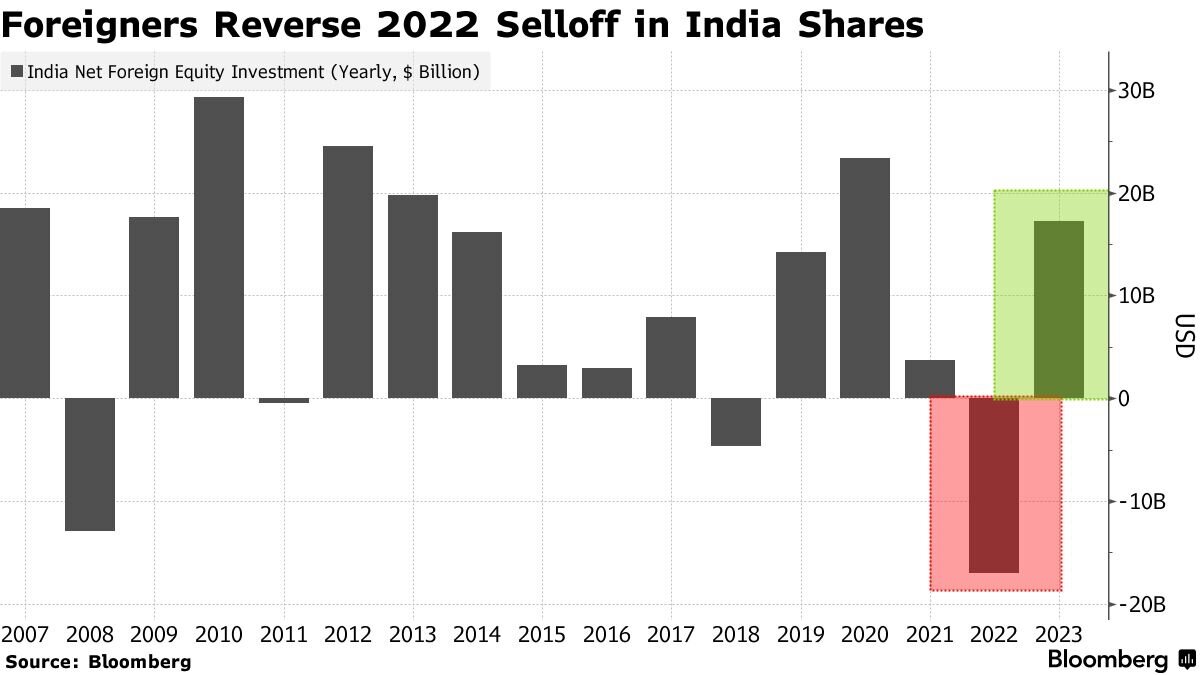

A couple of pro India (or should I say Bharat) pieces from Bloomberg today, they are positively ebullient 1. India Has Become a Beacon of Macro Stability: Chinoy Sajjid Chinoy, chief India economist at JPMorgan, discusses India’s economy and the upcoming G-20 and inflation in the country. He speaks on Bloomberg Television. https://youtu.be/Rlu53BOEwWo?si=AuuJH7gcKaT5_BNx 2.Foreign Funds Reverse $17 Billion Record Exodus in India Stocks Stocks in India are in the midst of a multi-year rally with the key benchmarks S&P BSE Sensex and NSE Nifty 50 Index headed for their eighth consecutive year of advances. A strong corporate earnings performance, robust economic growth and political stability are drawing investors even as they flee other Asian emerging markets. https://www.bloomberg.com/news/articles/2023-09-05/foreign-funds-reverse-17-billion-record-exodus-in-india-stocks?srnd=india-v2#xj4y7vzkg

-

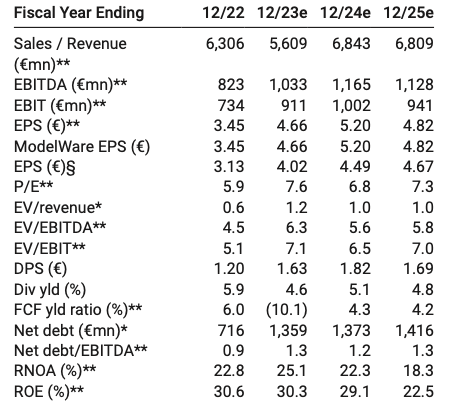

For those who like digging around in Fairfax's equity positions, MS released an updated earnings model for Mytilineos (attached). I agree with all you analyst haters, so treat it in the spirit of "entertainment". MYTIL, including options, is closing in on being a $US400m position for Fairfax and small in the grander scheme of things. See it as another example of an FFH asset rapidly regressing to the mean (+89% YTD). MYTIL share price is currently €38.01, MS PT is €45. "MYTIL offers a unique trifecta - multi-faceted Energy growth, unique aluminium business, and highly synergistic business model. These attributes coupled with an undemanding valuation point to a compelling risk-reward." MYTILINEOS_20230824_2100.pdf