Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Here is a review from Paul Deegan of David's book. Looking forward to getting a copy of it. https://www.policymagazine.ca/more-than-a-canadian-warren-buffett-prem-watsa-and-the-fairfax-way/

-

@glider3834, thanks for posting the link. It looks like results for this holding have broken out to a much higher, sustainable level. Q2 EBITDA up 127%; 6-month EBITDA up 98% Q2 profit before tax up 243% ('Given the high seasonality in many of our businesses, the second half performance is expected to improve further over the first half.') Q2 group profit after tax up 176% Doubled the dividend from Rs.0.05 to Rs.0.10 per share. ('This reflects the expectation that the current momentum of performance will sustain or further improve over the second half of the financial year.')

-

With a MV of $1.2b, Orla is Fairfax's 4th largest equity holdings (if we include FFH-TRS as a holding). It just released results and hosted a conference call. Investors like what they read/heard - the stock was up big today. Crazy increase of $662 million, or 117%, YTD in 2025. https://ca.finance.yahoo.com/news/orla-mining-ltd-orla-q3-210715844.html

-

Here is another way to ask the question. Go with me on this one… Warren Buffett bought Coke in 1987. What made Coke such a good investment? Let’s ignore Buffett’s purchase price. At a very high level, what is it that happened at Coke after Buffett bought it (the subsequent 5 to 10 years) that made it such a good investment? And what was it that investors at the time were missing? Buffett got it. Most everyone else did not. (That might help us understand what we might be missing with Fairfax today.) Here is a start: A turnaround play? Management? Operations? Capital allocation? Reinvestment opportunities? Does anything rhyme? Obviously Coke in the late 1980’s and Fairfax today are completely different animals

-

@TwoCitiesCapital, I am not following you. Each of the 4 items that make up operating earnings is going up. As a result operating earnings has been growing nicely. With Fairfax’s equity holdings, company fundamentals pretty much across the board are improving. That tells me the companies are increasing in value (that is very different than volatility). Buying back minority interests (Brit) and continuing share buybacks are helping.

-

@Parsad when it comes to estimating earnings for Fairfax, the really interesting thing to me is how estimates have consistently been too low. And that includes me. Why have EPS estimates for Fairfax been consistently wrong (too low) every year for 5 years straight? Answer: Investors (including me) do not yet fully understand or appreciate Fairfax (the business and management). What is it we are missing? My guess is its a couple of things: 1.) We are grossly underestimating the amount of ‘hidden value’ that is residing in the company. And how much it is growing. 2.) The impact of reinvestment of current year earnings on future returns. 3.) The impact of compounding on future returns. What do other board members think? Why have we been so bad for so long at estimating Fairfax’s business results?

-

Attached below is an update to my earnings estimate for Fairfax for 2025 and 2026. 2025 = $195/diluted share (economic EPS = $233/share) 2026 = $190/diluted share (economic EPS = $200/share) Bottom line, Fairfax's fundamentals continue to improve, so my estimates for both years have increased. At the bottom I have also included the change in excess of FV over CV for associate and consolidated holdings. This is additional economic value that is being created that is not being captured in the accounting results. Adding reported EPS with this number provides a conservative estimate for the increase in economic earnings for the year. This estimate is conservative because it does not capture all the value creation that is happening under the hood at Fairfax. For 2026, I am being conservative with investment gains, given the size of gains we are likely to see in 2025. Bottom line, Fairfax is generating economic earnings of about $200/share. I think this is a reasonable number to use as a normalized number. I think it is conservative given my low estimate for investment gains. With the shares trading at $1,600, that puts the PE at about 8x. P/BV - 1.3 and the company is delivering an average ROE in the high teens. That looks pretty cheap to me for a high quality company with an outstanding long term track record that is very well positioned, well managed and very shareholder friendly. Let me know what you think.

-

@wondering, the themes that I writte about have been discussed and debated by many on this board for the past 5 years. Sometimes there has been a lot of guessing going on. The author appears to have had access to Fairfax - that is going to provide a new level of understanding for all of us on some important topics. There is no monopoly on ideas. At the end of the day, I just hope it’s a good book and does justice to Fairfax and its employees (and I expect that it does).

-

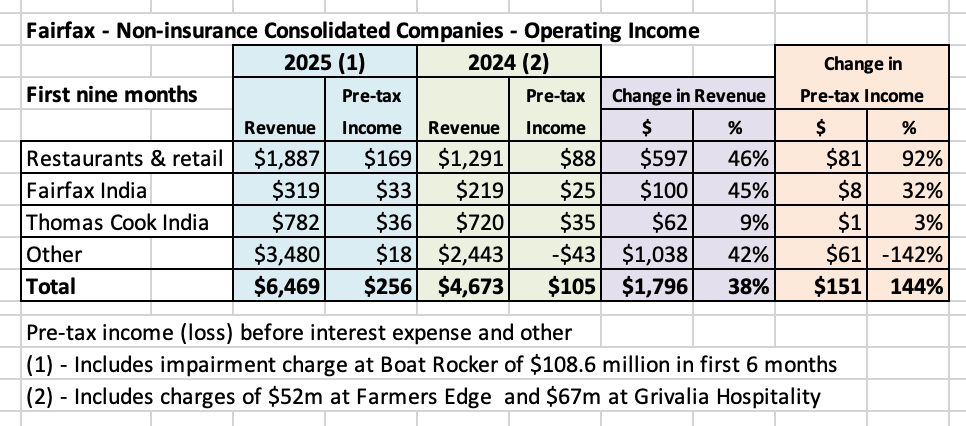

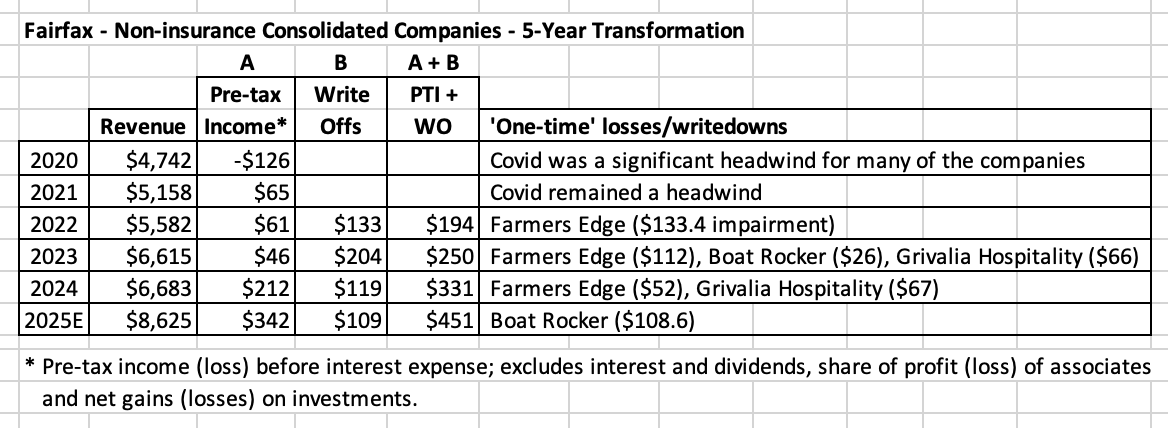

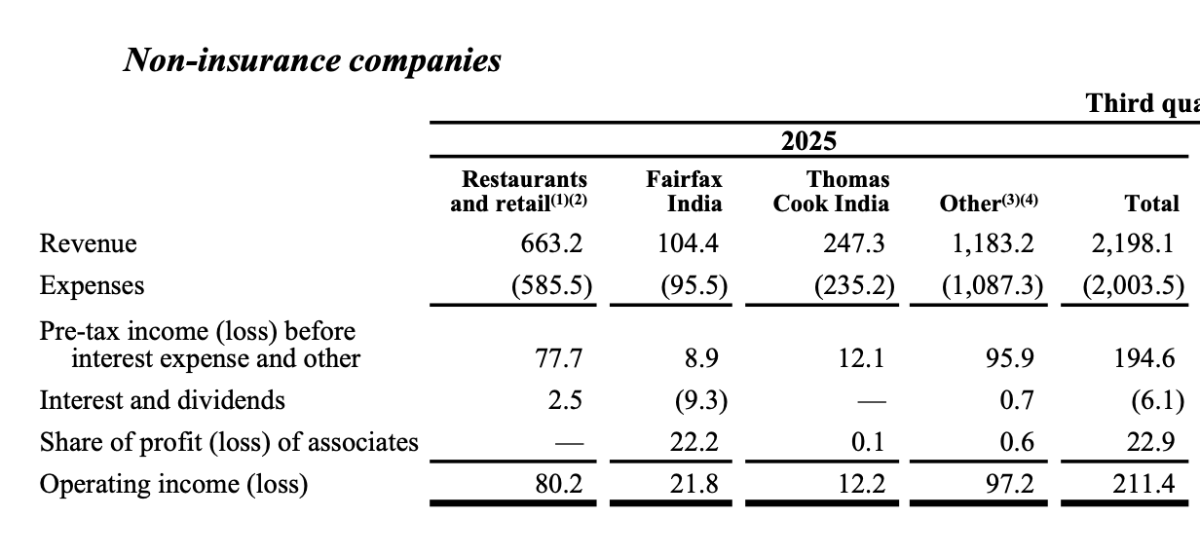

Today we will continue our review of Fairfax's Q3 earnings. To provide context, I will start with the big picture and then zoom in. Our goal is to improve our understanding of the company. Fairfax has 5 income streams that feed into reported earnings: Underwriting income Interest and dividend income Share of profit of associates Non-insurance consolidated companies Investment gains (realized and unrealized) In recent years, the first three income streams have inflected higher: Underwriting income Interest and dividend income Share of profit of associates At the same time, the fifth income stream, investment gains, has continued its strong performance. Not surprisingly, with 4 of the 5 incomes streams performing at a very high level, reported earnings at Fairfax have spiked higher. This has transformed the company. This has also spiked the stock price over the past 5 years. —————- Fairfax just reported Q3, 2025 earnings. They were very good. What was one of the key take-away from Fairfax’s Q3 results? It appears Fairfax’s smallest income stream, non-insurance consolidated companies, is (finally) breaking out. Over the first 9 months of 2025: Revenue was $6.5 billion, an increase of 38%. Pre-tax income was $257 million, an increase of 143%. But here is the key: Pre-tax income for 2025 is understated. In 1H-2025 there was a $108.6 million impairment charge for Boat Rocker (to fix this legacy problem child). If we exclude this one-time charge pre-tax income was about $366 million over the first 9 months of 2025. This extrapolates to about $500 million for the year. Yes, that is a big number for a company of Fairfax’s size. So what? The emergence of the non-insurance consolidated companies income stream is a significant development for a number of reasons: It is big and it is growing quickly - The investments have already happened. In recent years, Fairfax has been investing a significant amount of capital to grow the number of companies that fall into this bucket of holdings. 2022: Recipe, Grivalia Hospitality 2024: Sleep Country, Peak Achievement, Meadow Foods It has a long runway of growth ahead of it. Fairfax will be generating a significant amount excess capital in the coming years - which will support continued investment in this bucket of holdings. Like a coiled spring being released, earnings are now spiking higher. Of course, a new large and growing source of earnings is a significant development for long term investors of Fairfax. It will grow operating earnings. This income stream forms part of operating earnings, which are considered to be high quality sources of earnings as they are more stable and predictable than investment gains. It is not priced into the stock today. This income stream is not really on the radar of investors or analysts. As a result, it is not built into their models today. In 2025, non-insurance operating companies bucket has emerged as another large and growing income stream for Fairfax. This increases the number of material/important incomes streams for Fairfax from 4 to 5. And with the hard market in P/C insurance slowing, the timing of its emergence is very good - the non-insurance operating companies bucket of holdings will provide Fairfax with an important growth engine in the coming years. Fairfax has set the table nicely. —————- A 5-Year Journey - It doesn’t matter until it does Underwriting profit didn't matter at Fairfax until it began spiking higher in 2021. Interest and dividend income did not matter... until it began spiking higher in 2022. Share of profit of associates did not matter until it spiked higher in 2022. My guess is non-insurance consolidated holdings is (finally) spiking higher... and it is going to matter to Fairfax's total results moving forward (become a meaningful contributor). From 2020 to 2023, non-insurance operating companies delivered an average pre-tax income of $12 million per year. So it is not surprising this income stream is not on the radar of investors or analysts. My guess is this is about to change. Why? Fairfax has been busy at work for the past 5 years getting all of the companies in ‘non-insurance consolidated holdings’ performing at an acceptable level ('optimizing' the operating results of each of the businesses). Two holdings have been especially problematic: Farmers Edge and Boat Rocker. The write-offs from these two companies have been enormous over the past 4 years. The good news is both of these holdings appear to have been dealt with (Farmers Edge plan of arrangement/take private and Boat Rocker sale/merger into a stronger Blue Ant Media). After hitting some pot holes in 2023 and 2024, it appears Grivalia Hospitality’s business has also stabilized. In our table below, if we add the large annual write-offs (B) to pre-tax income (A) we can get a better read of the what the underlying run-rate of pretax-net income actually has been for this group of companies. As the very large write-offs come to an end, the strength and profitability of the businesses captured in this bucket of holdings will begin to shine through more fully. I think that is what we are starting to see. Pre-tax income from non-insurance consolidated holdings came in at $120 million in Q2 and $195 million in Q3. My guess is $450 to $500 million is likely a good annual estimate of where this income stream is at today. That is a material number for Fairfax - large enough to get the attention of investors and analysts.

-

I wonder if we do not see more consolidation of the nat gas producers in the US over the next year as demand from LNG exports picks up. I wonder if EXCO is viewed as being a desirable target? Not sure what region they are in and the quality of their assets.

-

My read is we are at the end of the Disney phase with Fairfax. Let’s face it, the past 5 years have been wonderful. That is not to say the next couple of years will not be very good for the company and shareholders - I think they will. My point is more that Fairfax will likely trade more like a normal stock moving forward (experiencing lots of volatility). And WE KNOW analysts are not very good at analyzing Fairfax (especially the investment management part of the business). We are getting proof of this with many of the reports that are coming out on Q3 earnings. With the hard market in P/C insurance slowing, the investment management part of Fairfax’s business is going to become an even more important part of the Fairfax story in the coming years (that is where most of the growth will come from). So I expect the disconnect between Fairfax’s improving fundamentals and analyst commentary to widen (get worse). In the near term, that will likely not be constructive for the share price. Fairfax’s story has been slowly playing out over the past 5 years. I think we are at the beginning the next chapter of this incredible book. Interestingly, I also think a large portion of the chapter has already been written by Fairfax (they have already done the work under the hood - we just don’t see it yet). It has two components: A high quality P/C insurance business. And a rapidly growing, high quality investment management business (driving higher share of profit of associates, much higher non-insurance consolidated companies and higher investment gains). Investors and analysts just don’t recognize it yet. But as it becomes more obvious (shows up in historical results) I am confident that they will discover it too (like what has been happening over the past 5 years). As we all know, what matters over the long term for any company is earnings per share. As Fairfax continues to deliver on the earnings front, the stock price will respond accordingly.

-

@SharperDingaan, I have a different take on the budget. I have heard Carney’s budget portrayed as ‘like a Stephen Harper/conservative budget.’ That is how Carney wants it portrayed - and the main stream media is running with it. But I don’t think that is close to being an accurate portrayal. Yes, it is great politics. At the end of the day, Carney did very little to improve the investment climate in Canada. He did not touch the regulatory burden. Yes, he fiddled around the edges… but after 10 years of Trudeau much needs to be done. Right now Carney is also looking like ‘big hat no cattle.’ At some point he needs to start delivering wins - the opposite has been happening (US, China and India). Carney is significantly better than Trudeau. But Trudeau was historically terrible so that does not say much. It appears Carney still believes government is the answer - not free enterprise. Stephen Harper was the exact opposite. My read is 2026 is shaping up to be a historic year for Canada. And not in a good way. Having said that, we will figure it out. But it seems to me we still have not identified the right ‘what is the problem’. (Answer: big government - at federal, provincial and municipal levels).

-

As per Prem’s comments, Fairfax’s initial investment with Adam Waterous was US$129 million. And Fairfax is poised to get C$130 million back in Q4, while still retaining a significant stake in Strathcona? If correct, it looks like Fairfax has another winning investment on its hands.

-

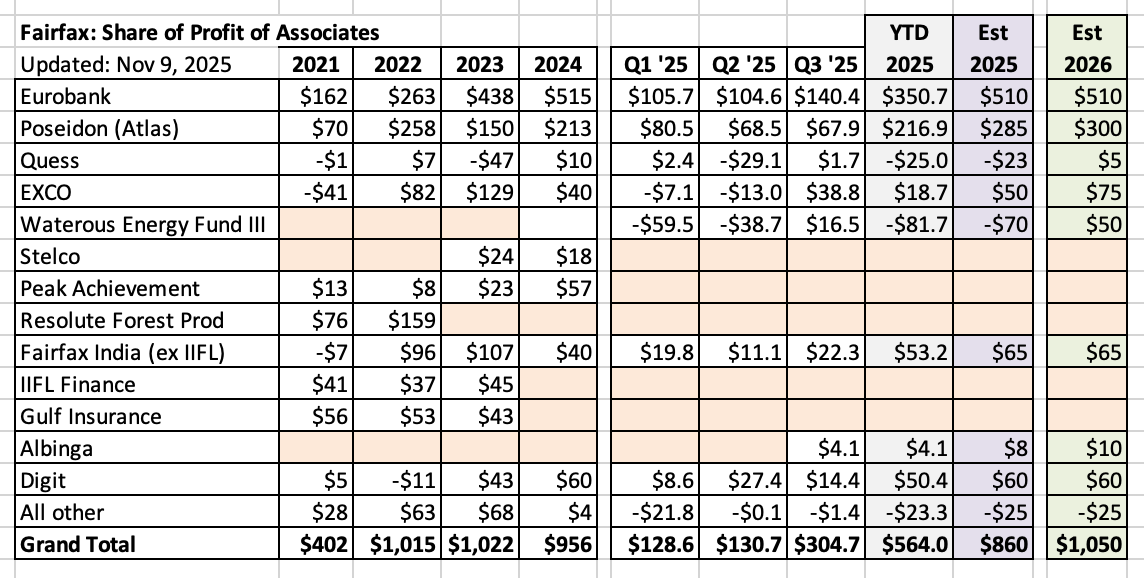

Is 'share of profit of associates' about to inflect higher? We continue our review of Fairfax’s very strong Q3 results. “Skate to where the puck is going to be, not where it has been.” Wayne Gretzky Fairfax has 5 income streams that drive its earnings. The 4th largest is share of profit of associates. How did it perform in Q3-2025? Very well. It came in at $305 million, which was much higher than expected. This extrapolates into an annual number of $1.2 billion. That is a big number. What drove the beat? Eurobank, the largest contributor, continued to deliver solid results ($140m). Poseidon, the second largest contributor, continued to deliver improving results ($68m). It has been a big tailwind in 2025. EXCO, a nat gas producer, is benefitting from higher natural gas prices in the US ($39m). This was a surprise and should be a nice tailwind in Q4 and 2026. Waterous Energy Fund III, a private equity oil and gas fund, flipped from being a big headwind in 1H to a small tailwind in Q3. Fairfax has invested a significant amount in this fund over the past year. Adam Waterous is an excellent capital allocator - this investment will be one to watch in the coming years. It should also be noted that a number of holdings have fallen out of this bucket over the past 3 years (Peak, Stelco, IIFL Finance, GIG, Resolute Forest Products). Driven by continued solid results from Eurobank and Poseidon and improving results at EXCO and Waterous III, this income stream looks poised to have a strong Q4 and 2026. A conservative annual run rate to use in 2026 is likely $1.05 billion, which would be a new record for Fairfax. Importantly, we could see this important income stream for Fairfax start to grow again. Yes, it will likely catch many investors and analysts by surprise. There is a lot of handwringing going on these days with some investors about where the growth in earnings at Fairfax is going to come from in the coming years (they are intently focussed on where the puck has been). I think we might have just discovered one source (by focussing instead on where the puck is going). There are many more...

-

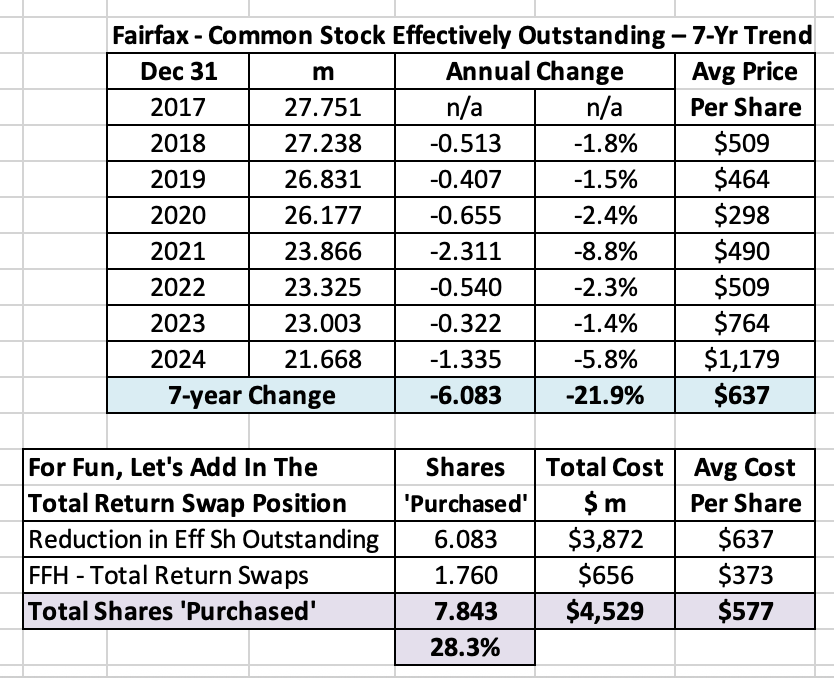

I am going to do my review of Fairfax’s Q3-2025 results in a series of posts. Today, we are going to review the P/C insurance results. Our review is going to be at a very high level - we are going to zoom out and try and look at the big picture. Getting the the big picture right is a critical part of getting an investment thesis right. ————— Fairfax is an interesting and unique company. It has two complementary businesses: P/C insurance and investment management. P/C insurance is the core engine (float) that powers the whole company. As I will explain below, P/C insurance is becoming an even more important part of the company. Over the past 10 years, Fairfax has been completely transformed as a company. One important example of this transformation has been the changes that have been happening in its P/C insurance business. Historically, investors bought Fairfax because of its investment management business. Not because of its P/C insurance business, which was considered to be low quality. Fairfax got started on transforming its P/C insurance business back in 2011, when Andy Barnard was appointed to oversee it. Fairfax’s P/C insurance companies have been on a 14 year journey of continuous improvement. Importantly, it takes years to transform a P/C insurance business (as Markel has been learning in recent years). And it takes years for the improvements to finally show up in business results (better underwriting profitability). And that is what has been slowly playing out at Fairfax. This is a really important development for long term investors. Because it means Fairfax now has two high quality businesses: P/C insurance and investment management. Of course, this bodes well for the future returns that the company will be able to deliver. This should result in higher earnings in the future. This should result in the company generating a higher ROE. Over time this should result in the stock receiving a higher multiple from investors and analysts. And as the multiple expands, the narrative around the company should also improve. Information advantage The interesting thing is, despite the growing evidence in recent years, investors and analysts have been slow to recognize or reward the improving quality of Fairfax’s P/C insurance business. This means it is likely not yet built into the price of the stock. And as we all know, one of the best ways to do well with a stock is to have an information advantage - to know something important that is (temporarily) being missed by most investors and analysts. This often happens with small companies like Fairfax (that tend to be underfollowed and misunderstood). Investors on this board have been documenting the transformation that has been slowing playing out at Fairfax over the past 5 years. This has given them a big information advantage over other investors and analysts. It has been like having a crystal ball - being able to see the future 6 to 12 months before it is understood and appreciated by the larger investment community. What is interesting is the story at Fairfax has been continually changing (getting better) for each of the 5 years. This is not normal - most companies are not that dynamic. Importantly, the story at Fairfax is still changing (getting better) in important ways that are not yet understood or appreciated. Like the improved quality of their P/C insurance business. In important respects, the Fairfax story (this iteration of the company) is just getting started - of course, that is a wonderful set-up for a long term investor. Let’s get back to our story - Fairfax’s Q3 results. Each quarter when Fairfax reports results we get lots of new and important information. When analyzing the P/C insurance business, the key question I have been asking for the past couple of years is: ‘Does Fairfax’s have a high quality P/C insurance business?’ Getting the answer to that question right is a critical input in how to properly value the company. What did we learn in from Fairfax’s Q3-2025 results? 1.) The top line is slowing. Q3 net premiums written = $6.55 billion, up 2.1%. Excluding a short term impact at GIG, they were up 3.1%. Interestingly, this is lower growth than P/C insurance peers. 2.) Underwriting profit came in ahead of expectations. Q3 underwriting profit = $540.3 million (up from $389.7 million in 2024). Q3 CR = 92.0% (was 93.9% in 2024), from decreased catastrophe losses of $150.0m (2024 - $434.5m) and growth in business volumes, partially offset by a decrease in net favourable PY reserve development to $111.2m (2024 - $130.5m). Ok. What does this mean? Is a slowing top line a bad thing for Fairfax? No, a slowing top line is not a bad thing. It is the opposite. It suggests Fairfax’s many P/C insurance companies are exercising great discipline with their underwriting. And more discipline than peers. Managing the insurance cycle “Be fearful when others are greedy, and greedy when others are fearful” Warren Buffett Over the past decade, Fairfax has provided a textbook example of how to manage the P/C insurance cycle. Grow aggressively by acquisition in a soft market (2015-2017). Grow aggressively organically in a hard market (2019 to 2025). Fairfax grew faster than peers at the beginning of the hard market (the ‘be greedy’ stage). And now it is growing at a slower rate at the end of the hard market (the ‘be fearful’ stage). What Fairfax is doing is exactly what Warren Buffet has been preaching for decades should be done. (Are investors and analysts paying attention?) Now investors and analysts will not like that Fairfax is growing more slowly than peers. And of course, this is completely wrongheaded. What are we learning about Fairfax’s P/C insurance business from Q3 results? It looks like Fairfax is managing the P/C insurance cycle very well. Top line growth is slowing. And their underwriting results are very good and improving (getting better). This is further evidence that Fairfax has a high quality P/C insurance business - and it is higher quality than most analysts and investors think. With each passing quarter, this is becoming more apparent. —————- Another thing many investors and analysts are missing Despite a slowing top line number (net premiums written), Fairfax will still be able to grow its insurance rate at a pretty good rate. How will it do this? 1.) Per share metrics are what really matter to investors. Net premiums written (NPW) matter. What matters much more is NPW/share. This is a really simple and fundamental concept. And it is ignored by most investors and analysts. My guess is Fairfax might buy back about 4% of shares outstanding in 2025. Guess what that does to NPW/share? Yes, it boosts it by 4%. So if NPW increases by 3% and the share count falls by 4% then NPW/share increases by about 7%. Of course, one of the keys is the price that is paid for the shares. Trading today at 1.3 x book value, Fairfax’s stock is cheap. So share buybacks are a great use of capital. And a great way to grow NPW/share and float/share. Share buybacks are not new to Fairfax. From 2017 to 2024, the company has reduced effective shares outstanding by 22.9% at an average cost of $637/share. The value creation for long term shareholders has been enormous, further spiking the important per share measures (like NPW and float). Fortunately, Fairfax gets it. 2.) Minority partners in Allied World and Odyssey Fairfax does not own 100% of its two largest insurance companies: Allied World and Odyssey. Minority shareholders own 16.6% of Allied World and 9.99% of Odyssey. This means that today Fairfax shareholders are not getting 100% of the earnings from these two companies. When Fairfax buys out its minority partners in the coming years it will be kind of like making two large P/C insurance acquisitions. Importantly, Fairfax is able to buy out their partners at a very favourable price (due to the call option feature put in place when the deals were initially put in place). Summary As a result, Fairfax has a number of very good options at its disposal to continue to grow its insurance on a per share basis in the coming years. What Fairfax has done here is unique in P/C insurance. But because it is different it is not appreciated or valued by investors or analysts. Bottom line, Fairfax has many levers it can pull to continue to grow its P/C insurance business in the coming years - even as the hard market slows.

-

@Marco Van Basten, it looks to me like Fairfax has been pretty aggressive on the stock buyback front over the past 7 years. At the same time, they doubled the size of their insurance business and they have dramatically increased the size of their equity portfolio. They now have 5 income streams gushing cash. My guess is if the stock stays around current levels, we will see Fairfax continue to take out a meaningful number of shares in the coming months/year. Bottom line, it appears Fairfax has learned to walk (buy back stock) and chew gum (do everything else) at the same time. I like their balanced, shareholder friendly approach. Chubb is a fine, well run company. With the hard market slowing and their stock cheap, buybacks is a no brainer for them. Same with other P/C insurance companies. This is great news... a significant amount of capital (that being spent on buybacks) is being removed from the insurance market. PS: It is interesting to note that for Fairfax the average price paid in 2024 ($1,179/share) is already under the current BV ($1,204). Fairfax took out a significant number of shares in 2024. That is exceptional capital allocation. At the time, I am not sure everyone thought Fairfax was getting a good price (taking out shares at a price above BV). My guess is buybacks being done at current prices will also be viewed favourably looking out a couple of years.

-

+1 On the Q3 conference call Fairfax left lots of bread crumbs for investors who are paying attention...

-

“What possible assurance do you have that (a stock you own) will go up in price? And if you are buying, how much should you pay? What you’re asking here is what makes a company valuable, and why it will be more valuable tomorrow than it is today. There are many theories, but to me, it always comes down to earnings and assets. Especially earnings.” Peter Lynch - One Up on Wall Street How is Fairfax performing? Very well. Why do I think this? Follow earnings. Q3 net earnings = $1.15b or $52 per diluted share YTD (9 month) net earnings = $3.53b or $156 per diluted share Book value = $1,204/share, up 15.1% in 9 months (including $15 dividend) Excess of FV over CV for associate and consolidated holdings = $2.5b This item is not included in reported earnings (it would be if Fairfax's ownership stake in these equities was less than 20%). YTD increase = $1.0b, or $43/share pre-tax = $35/share after-tax How has Fairfax really been doing (economic value creation)? YTD (9 month) economic EPS = $190/share ($156 + $35) This is a conservative estimate (it does not include everything). Bottom line, 2025 is shaping up to be Fairfax’s best year ever from an earnings perspective. The company’s two business units (P/C insurance and investment management) are performing at a very high level. Capital allocation at the company continues to be best-in-class. Fairfax’s future has never been brighter.

-

So much to talk about. This might be the most important new piece of news. Fairfax has 5 income streams. The smallest is 'non-insurance consolidated companies'. I have been calling for this bucket to break out to the upside for 2 years. And I have been wrong. However, in Q2 it came in at $120 million which was quite strong (compared to past results). Well, I think we can now say it is not small anymore, coming in at $211m in Q3-2025. This is a big deal. What is a new income stream of $800 million/year (with a strong growth profile) worth? Just asking for a friend... PS: I am not sure if any of you have heard of a company called Berkshire Hathaway? You might want to take a peek at how they continued to grow their business over the long term... hint - it wasn't driven by the insurance cycle. I.E. they continued to grow in both hard and soft insurance markets.

-

@This2ShallPass, is there a statute of limitations to how long a CEO should remain in the penalty box for making a mistake (i.e. when it comes to treatment of minority shareholders)? Even the GOAT, Buffett, messed up badly at times. Should he still own all of the mistakes he made years ago today? My read is, on balance, Fairfax has been doing pretty well on the ‘fair and friendly’ front in recent years. Not perfect - but nobody is. They have been saintly with how patient they have been with many of their equity holdings, especially the terrible ones (largely gone now, thank god). The saintly behaviour bothered me much more over the years than the mistakes (related to minority shareholders).

-

@sholland, the short answer, IMHO, is if Fairfax wanted to take Fairfax India out at a low price they likely would have done it by now. It traded in the $12 to $13 range for a couple of years. Each year at the AGM a few questions are asked regarding Fairfax India. My read (today) is Fairfax is committed to keeping the current structure.

-

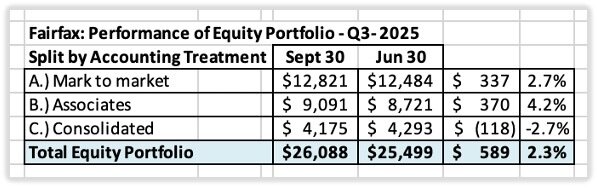

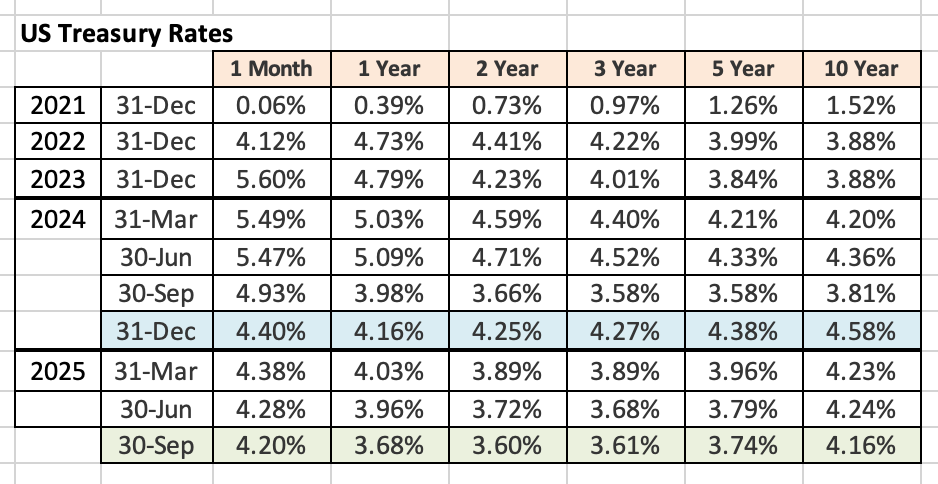

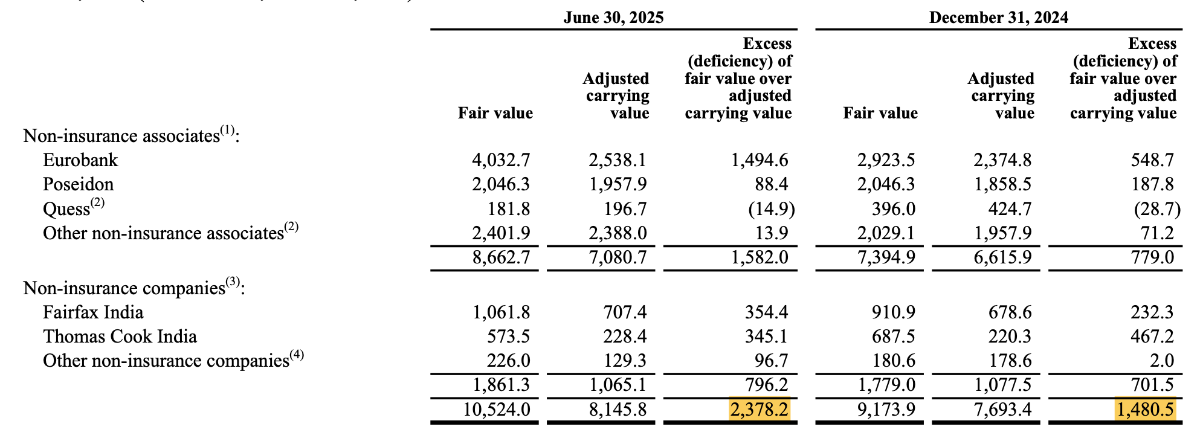

Fairfax Quarterly Earnings Preview 2025 is shaping up to be Fairfax’s best year ever in terms of earnings per share and increase in economic value per share. Outstanding. The company has never been better positioned. And the stock is selling off aggressively. And I love it. Mr Market is one amazing dude (the gift that keeps on giving). Below is a primer on a few of the things i will be watching for when Fairfax reports Q3 earnings. I think it will be another good quarter - my guess is EPS will be $45 to $50/share. Plus another $10/share (after tax) from items not captured in EPS. So an increase in economic value of around $55 to $60/share (conservatively measured). Earnings release - Thursday November 6th (about 5PM EST?) Conference call - Friday Nov 7th at 8:30 EST. https://www.fairfax.ca/press-releases/fairfax-announces-conference-call-10-24-2025/ Anything missing from my list? Please chime in with your thoughts. 1.) P/C Insurance What is growth in net premiums written? (In Q2, 2025, NPW grew 4.8%) What is CR? (93.9% in Q3 2024) What is level of favourable reserve development? (Q2 2025 was $163 million or 2.5% CR points) What is the 9 month CR? (Was 93.8% in 2024) Of all the things that Fairfax will report, I am most looking forward to seeing where underwriting income (CR) comes in. My thesis is Fairfax’s P/C insurance business is higher quality than most investors/analysts believe. And yes, results will have some quarterly volatility. We are more interested in the general trend (than any one number). In short, my view is the quality of Fairfax’s P/C insurance business is not built into the stock price. I love getting something that is valuable for free. 2.) Interest and dividend income How does it compare to Q2? (Was $666 million in Q2 2025, up significantly from $606.5 million in Q1 2025) What is average yield of fixed income portfolio? (Was 5.1% in Q2 2025) What is average duration? (Was 2.4 in Q2 2025) Interest and dividend income saw a significant increase in Q2 2025 (from the trend). Do we stick around the higher number? Or do we give a little back? 3.) What is share of profit of associates? Eurobank? Poseidon? Do the two big boys continue to deliver? Peak Achievement will be a small headwind (it is now a consolidated holding). 4.) Non-insurance consolidated holdings? (Was $120 million in Q2, 2025) Over the past couple of years Fairfax has been aggressively growing the size of this bucket of holdings. But it has been very slow to show up in reported earnings. When Fairfax reports results for this bucket of holdings (and they disappoint), I feel like Charlie Brown getting the football pulled away by Lucy before it can be kicked. But I think things might have changed. In Q2, non-insurance consolidated holdings delivered $120 million. Is this a sign this bucket has turned higher? Results in the coming quarters will tell the tale. This is important because non-insurance consolidated holdings is Fairfax’s 5th income stream. It is also the smallest. But if $120 million/quarter can be used as a run rate, that would put it at close to $500 million for the year. Not a small number. For all those investors wondering where the growth will come from at Fairfax in the coming years (with P/C insurance slowing)... well this bucket is one of a couple of examples. This growing income stream is not on investors/analysts radar today. Therefore it is not built into the stock’s price. More free stuff… I love it! 5.) Investment gains (realized and unrealized)? Equities? (How close is my $337 million estimate for mark to market holdings?) My estimate does not include Digit or IIFL Finance (both will be small headwinds in Q3). The sale of Praktiker (Greece) closed in Q3. What is the size of the realized gain? Fixed income? (Bond yields were a little lower so this will be a modest tailwind.) Bottom line, 2025 is shaping up to be a banner year for investment gains at Fairfax. Rough estimate of change in value of equity portfolio in Q3 Change in US Treasury rates in Q3 6.) IFRS 17 impact of change in interest rates I always struggle with this bucket. A growing insurance business should be a small tailwind. And lower interest rates should be a small headwind. 7.) Tax rate? Guidance for year? (Given size of investment gains, I am using a low rate of 21% in my earnings model for FY2025) Is a normalized rate still 23%ish? 8.) Share buybacks (effective shares outstanding = 21.57 million at June 30, 2025) It appears Fairfax bought back about 285,000 shares in Q3 at about $1,700/share. What is plan for share buybacks moving forward? 9.) Diluted earnings per share? My back of the napkin number is US$45 to $50/share. 10.) Book value per share? ($1,158 at June 30, 2025) What was impact of slightly stronger US$? Modest headwind to BVPS? 11.) Excess of FV over CV for associate and consolidated holdings? This was $2.38 billion at June 30, 2025 ($100/FFH diluted share pre-tax), up from $1.48 billion at Dec 31, 2024. This should be up modestly in Q3 to perhaps $2.5 or $2.6 billion. That would put the increase in 9 months at about $1 billion ($42/FFH diluted share pre-tax) A source of significant future earnings for Fairfax: Excess of FV over CV has been growing like a weed over the past 5 years. This is not surprising - the quality of Fairfax’s equity portfolio is much higher quality. The value creation in this bucket will b3 a source of future earnings for Fairfax. It’s like Fairfax has given investors a crystal ball to help them more accurately estimate future results. Except most investors/analysts are not bothering to use it. As a result they are constantly underestimating the performance of the company. It is bizarre. But true. The interesting thing is this is not the only example of where significant ‘hidden value’ is residing at Fairfax. Yes, more free stuff… PS: Knowingly ignoring important facts is not being conservative. It is bad analysis. Bad analysis leads to better understanding, decision making and results? Of course it doesn’t. Economic EPS: sum of reported EPS + increase in excess of FV over CV + increase on other items. My guess is economic EPS in Q3 will come in around $55 to $60/FFH diluted share. 12.) Miscellaneous items: Size of investment portfolio? ($65.2 billion at March 31, 2025) Any adverse reserve development in runoff? Any change to FFH-TRS position size? 13.) There has been a lot going on at Recipe in 2025. Takeout of minority partner in Q1. Purchase of Olive Garden Canada in Q3 (rights and restaurants). Takeout of Keg Royalties Income Fund in Q3. Spinout of Keg from Recipe later in Q3; partial sale of Keg to Richard Jaffray. How much of Keg was sold? Price? What is carrying value for Keg? What is new carrying value for Recipe? Recipe is a great example of the benefits of taking a company private. Fairfax and Recipe have been busy the past 3 years improving the business. My guess is their efforts have made the company much more valuable. But much of the improvement is not showing up in how it is being valued today. My guess is Recipe is a great example of a company where there is a large (and growing) amount of hidden value. Welcome to new Fairfax. Yes, more free stuff (for long term shareholders). 14.) Sale of Eurolife’s life insurance business Anticipated to close in Q1 2026. Will the sale result in a realized investment gain? If so, about how much? (It is speculated the gain might be as high as $300 million.) Among other things, this is likely a good example of hidden value being surfaced by Fairfax (that was not being captured in the excess of FV over CV bucket). We will see if this is true when we get more details on the transaction. 15.) Recently announced take private of Kennedy Wilson at $10.25/share What is the strategic rationale for this purchase? Simple investment? Or something else? Or some combination? Will Fairfax use partners? At a minimum, this looks like a good example of Fairfax being opportunistic (buying an asset at the bottom of the cycle). But I suspect there is much more to this transaction than 'buy low'. 16.) Capital allocation: An update to the priorities moving forward? After ‘maintain a strong financial position’ what is the next priority? Buybacks? Buying back the minority interest at Allied World - is there a date this has to be completed by? What is the estimated cost? How is the cost calculated (how does the call option feature work)?

-

Fairfax is generating an enormous amount of excess capital these days. It needs to go somewhere. Why not opportunities like KW? In terms of what is best for KW, the company is better off as a private company (IMHO). KW has been a terrible long term investment for its shareholders. That is not on Fairfax. Fairfax is executing value investing as Ben Graham teaches it - one of the big benefits of public markets is the ability to take advantage of Mr Market’s folly. Fairfax has been vacuuming up a lot of stuff it already owns in recent years - both public and private holdings. KW is just the latest example. This is a sign of very good capital allocation - all these take-outs are in businesses they already understand exceptionally well (are in their circle of competence), which should lower the risk. I love the moves.

-

I think KW’s business today would be better served being run as a private company (as opposed to being publicly traded). So Fairfax buys low AND puts the company in a better position to succeed. My summary below assumes Fairfax owns more than 50%. (Perhaps Fairfax ends up owning less than 50% - transaction details are pretty sparse. So, we will see how it all shakes out.) This is yet another example of Fairfax: Buying more of something they already own a bunch of. They understand KW exceptionally well - the business, management, culture, issues, value. Obviously, Fairfax feels KW is a great fit. Wade Burton has been on the KW board forever. Being VERY opportunistic ($10.25/share to take it private?) - The timing of this purchase is interesting (why now?). Importantly, KW looks like it is already well into its turnaround. Fairfax appears to buying at/near the bottom of the commercial real estate cycle. Building out their non-insurance consolidated company bucket. Last year it was Sleep Country, Peak Achievement and Meadow Foods. Earlier this year they took out their minority partner in Recipe and public shareholders in the Keg Royalty Income Trust. This bucket of holdings is growing like a weed. With the hard market in P/C insurance slowing, this should not come as a surprise (that capital will be shifted to other opportunities).

-

@SafetyinNumbers, your informal pole is interesting. 1.) Haven’t looked. If a 460% total return over 5 years can’t get someone interested what can? 2.) Don’t like the equity portfolio. My question is do they actually follow/understand each of the large holdings? My guess is no. If you do the deep dive into each of the holdings, get to know management and review their performance over the past 5 years, there is a lot to like. 3.) Doesn’t meet return hurdle. Fairfax is a compounding machine. It is still small. And it keeps improving itself. It is just entering its prime. If its return potential isn’t good enough, what hurdle rate are they looking for? Bottom line, for reasons outlined above (and others) I think there is a good chance Fairfax could stay on sale for an extended period of time. I would love it. That would give Fairfax the ability to keep taking out 3% or 4% of shares outstanding every year moving forward. When you include the FFH-TRS, Fairfax has already taken out close to 30% of effective shares outstanding since 2017. This has benefitted long term shareholders enormously. Even with buybacks, Fairfax still has lots of excess capital to use to drive top line growth.