SafetyinNumbers

-

Posts

2,816 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

I’m amazed how cheap some gold stocks are. Money has flown into large cap royalty companies and high quality large and mid caps but otherwise multiples are super low. No one wants to own shitcos no matter how cheap they get it seems.

-

Is the Toronto condo market going to crash?

SafetyinNumbers replied to Viking's topic in General Discussion

I’m watching not that closely because cap rates are still so low and the culture of ownership Is still so strong. I have been renting in Toronto since 2008 so I know I’m bad at market timing. -

Has anyone calculated the original invested capital? It’s been deleveraging so the carrying value has been going up and the returns going down. They could always increase the leverage if they wanted to boost returns again. A nice source of capital if it’s needed at the holdco for any reason.

-

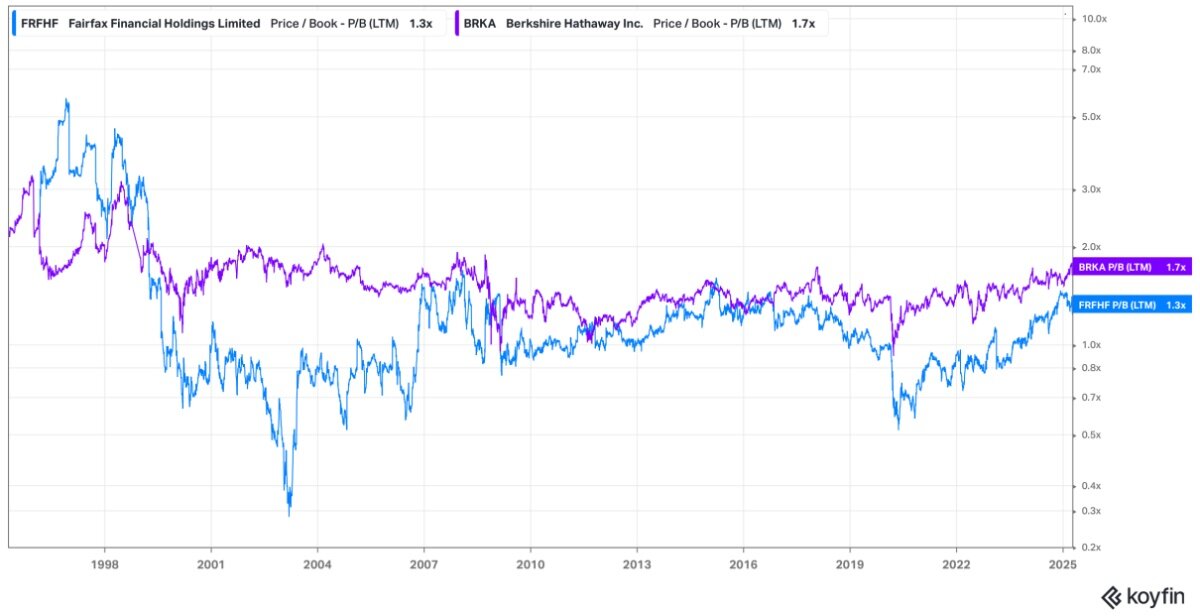

I wouldn’t buy an ETF off of it but it makes sense that idiosyncratic positions might become very cheap if they are growing value while capital is fleeing companies that don’t screen well for 15+ years post GFC. Eventually the stocks get so cheap like Fairfax that the returns are very high. Fairfax in particular has taken all the write downs on its positions but only gets to mark them up by their share of earnings. It’s an incredible set up.

-

An update on the long FFH / short XFN idea and some other thoughts post AGM https://open.substack.com/pub/berczyparkcapital/p/update-on-ffh-xfn-trade-idea-and?utm_source=app-post-stats-page&r=ecc87&utm_medium=ios

-

I don’t think most investors appreciate the context of the hedges at the time. The threat of negative interest rates was real and Fairfax has above average float so I believe it was defensive in nature. It was a bad idea but in context I can see how they rationally came to that conclusion. Today’s environment is very different. Hedging now would be speculative.

-

Sure but Berkshire BV growth was less predictable then vs Fairfax now and the P/B multiple was also usually higher than Fairfax is now. It seems easier to avoid making a bad decision as it’s less of a bet on the jockey and more of a bet on the structure. Still people are selling. I attribute that more to high return expectations given how inefficient and volatile the market is vs a view that absolute returns will < 10% CAGR over the next 5 years.

-

I wasn’t disagreeing with you. Just adding something I learned during the week on Seaspan which I thought was important. I know quite a few investors have been selling because the rate of change in operating earnings ($5b pre-tax, $150/sh after-tax) is slowing. I think ignoring that they have tons of embedded gains like Seaspan, Ki, BIAL etc… is a mistake. The three of those marked at fair value might increase book value over $200/sh and of course there are other FV over CV gains like Eurobank that are disclosed to consider.

-

Sokol said that he thought Seaspan was worth ~$9b and that Fairfax’s stake is worth ~$4b which is more than 2x where it is marked.

-

-

Raymond James just initiated coverage on Fairfax Financial with an Outperform 2 rating and C$2600 PT.

-

I assume they match the currency exposure in their claims liabilities with the bonds in the investment portfolio to a certain extent.

-

Adam Waterous presented at the Ben Graham Conference today. He was introduced by Wade Burton who was very complementary and described Adam as their partner in all things energy or something to that effect. It was pretty clear that the crowd was impressed with the presentation. I’m not sure if institutions will buy Strathcona SCR.TO before it goes in the S&P/TSX Composite but the set up looks very good for contrarian investors despite the recent plunge in oil prices.

-

I don’t know. Does it matter?

-

I think $3-5b are the right bookends. It is interesting to speculate when Berkshire and Fairfax will pull the trigger. The TRS shouldn’t have an impact what Fairfax can do in the insurance subsidiaries to reallocate from fixed income to equities because they are held in the holdco. Also, they aren’t that big. For every $100 the shares move it’s only ~$6 in EPS. Book value has a good shot of being $1100 right now and they are generating a significant amount of free cash flow so I assume if the shares get hit they will be be aggressive at book value if not sooner.

-

I’m more optimistic on underwriting, at least for the next 5 years. I think the premium growth over the past 5 years likely led to operating leverage. I think they have been spending a decent amount of that on technology which hopefully ultimately helps maintain some operating leverage. I think the hard market over the past 4+ years will lead to higher reserve releases over the next 4+ years. I think interest rates are ultimately heading higher within 4 years as this US administration tries to change the world economic order.

-

Which positions have you concerned?

-

Seems that way. So it’s even cheaper than it was before. Low margin business though.

-

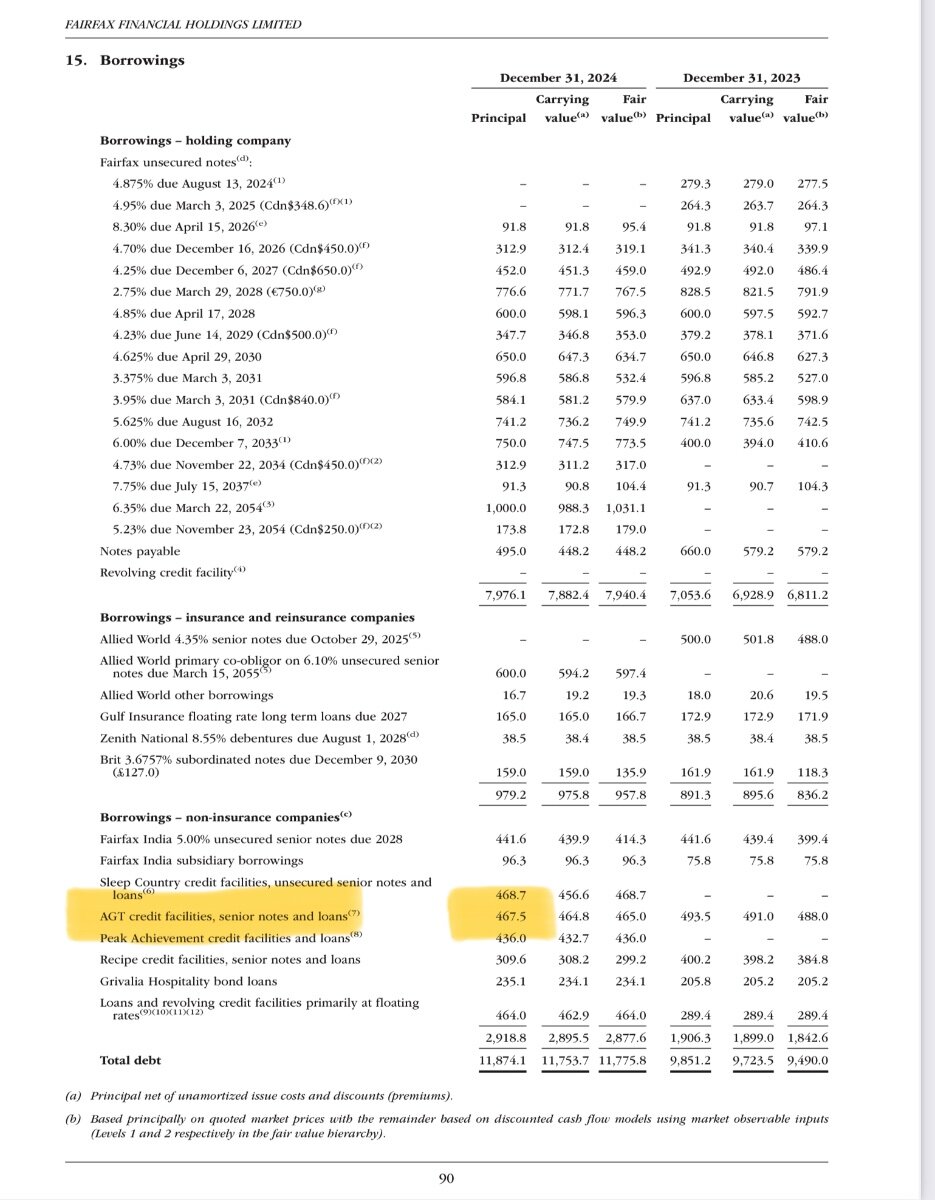

We know the debt at AGT at year end so I think we need to reduce $756m carrying value by $467.5m and then calculate the value of FFH’s equity. At 66%, I think that’s ~$190m. Seem like it’s another undervalued equity position in an equity portfolio that is the reason most investors avoid Fairfax.

-

Ardo is my fave restaurant in the city. It’s not a scene like Bar Isabel can be but the food and service are excellent.

-

The other downside is the beneficial capital treatment FFH gets in the insurance subsidiaries for owning a publicly traded company vs owning a bunch of private Indian companies directly. I think Anchorage will give them paper to do deals once it lists. They can also sell some Anchorage to buy back FIH stock to take advantage of the discount.

-

My understanding is that at 5% premium growth they can return 75% of earnings from the insurance subsidiaries. I think it’s possible we actually see an acceleration in premium growth this year as the cutting of some programs in Q4 2023 is no longer impacting comps but it of course depends on the returns available.

-

I think people confuse how hard or soft the market impacts near term profitability because they have been trained by quants to focus on the rate of change instead of absolute profitability. It does make sense for the average quality business but insurance and Fairfax in particular doesn’t screen well. A softer insurance market will mean lower float growth as Fairfax slows premium growth to compensate. We already saw some of that last year. However, a significant benefit from the hard market in underwriting profitability is deferred via reserves. We have just started to see reserve releases tick up as we lap 4 years of a hard market. Consequently, the combined ratio might come down just as market participants who don’t appreciate this nuance are expecting it to rise. Last quarter was a good example.

-

Gift link not sure how long it will last: https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/2Q4S3DIDL5CMVP6IPBZ33RY6WA/

-

Based on that you think there is too much “earnings volatility” from owning them?