SafetyinNumbers

-

Posts

2,816 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

All good points. The optionality on redeploying fixed income into equities could be a giant boost to ROE (buy the dip built in) and potentially the multiple if they redeploy into quality equities. I think the most common reason investors prefer MKL and BRK to FFH is because they only buy quality and FFH doesn’t have that reputation yet.

-

-

It was interesting that he said he just read the last three letters. It makes me wonder when he became a shareholder of FFH and FIH and how meaningful the position is. Ki too is AI fintech insurer. $100m investment is likely worth billions on IPO.

-

Thanks! That’s very interesting.

-

Thanks @glider3834 @nwoodman There aren’t a lot of exciting things going on the LSE lately so I can see how a business with these characteristics which are very much appreciated by the market could have outsized valuation. The initial IPO could have a meaningful boost to ROE but the business itself might be a fast growing company that screens well and keeps an outsized valuation like Digit so the benefit goes on for years via FV over CV at least. I don’t think Digit has raised Fairfax’s profile much but Ki might because it’s London-based. Europeans are used to buying Canadian stocks. Perhaps, a Ki IPO could convince a few European investors to take a look at Fairfax and recognize its long term potential.

-

Hi @John Hjorth, what’s your return expectation for Berkshire (if you think about it that way)? Personally, I’m finding most active absolute return investors have high return expectations and short time frames but there are exceptions.

-

i assume like most things that Fairfax does with partners that management and Blackstone will be part of a consensus decision. I assume they all want a good price. I don’t know if they have a need for more primary capital outside of paying off the C’s or if this marketplace approach means they are more capital light than other P&Cs.

-

Its 40% if you exclude the Class C preferred. The Class C get paid off with proceeds from the IPO at the IPO price so the higher the valuation the closer to 40% vs 20% they will own.

-

Thanks for sharing. I plan to listen this weekend. I’m curious what you and others on the board think Ki is worth?

-

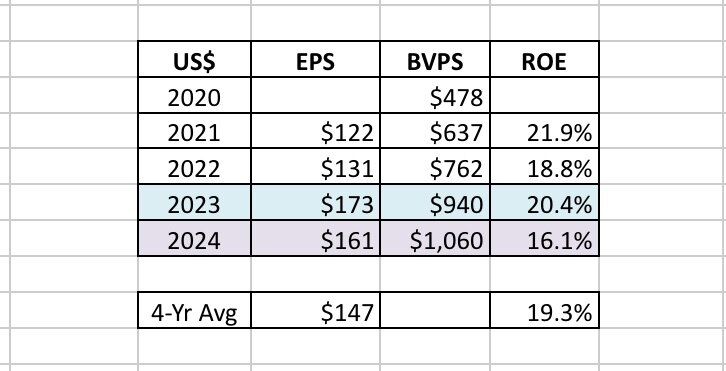

It’s in the substack I linked above. The short story is that expectations for underwriting, the equity portfolio, insurance gains like Ki and optionality of the fixed income portfolio are too low. We don’t know exactly where the gains will come from or how big they will be but given the 3:1 investment:equity leverage, it doesn’t take that much to get over a 20% ROE especially. Your comment “only get to 15%” ROE in the hard market years is misleading because it’s been better than 15% for the past 4 years. Also, the substack explains how conservative reserving delays some of the profit of a hard market until years later while the float growth is enjoyed contemporaneously.

-

Yes, I do. I wouldn’t have been buying up to last week and have 49% of my net assets in it if I didn’t think so. As I tried to explain in the substack, I use a 10% hurdle rate which means there are an abundance of opportunities in the current market that meet my hurdle. What makes FFH special enough to demand half my capital is twofold. To start, the hurdle rate seems likely to be exceeded over the next 5 years by a wide margin. I consider the chances average ROE exceeds 15% over that period to be 90%+ so the odds of exceeding 10% are even higher. I think the odds of 25% are higher than 10% by a wide margin. As a probabilistic investor, that’s a very special set up on fundamentals alone but on top of that the odds for multiple expansion seem very high and are open ended. There is lots of support for the multiple to expand including index add potential, potentially 10 years averaging >15% ROE (4 down, 6 to go) which leads to holders less likely to sell, 7m shares already repurchased or under TRS leaving less supply. I think people selling this week are playing a relative return game and not an absolute return game with a reasonable hurdle. I think the latter is most of the shareholder base but there will always be marginal holders. The less marginal shares available though means the higher the share price will go when passive and Canadian active PMs have to buy without regard for value.

-

A P/B multiple in conjunction with ROE is one way of estimating intrinsic value. It makes intuitive sense that a high ROE indicates higher quality of assets all else being equal which is reflected in a higher multiple. To estimate IV for Fairfax, I use a normalized market multiple of 15x PE as it has an above average return profile and the Buffett method of book value + float. That gives me an intrinsic value range which it still trades well below. There are lots of other ways to estimate it. I sometimes think about being more precise but if that’s necessary then it’s probably not that cheap. The cheapness gives the margin of safety and Fairfax’ portfolio is full of right tail optionality which I believe means it’s more likely ROE exceeds expectations versus not. I’m surprised how cheaply people are selling their shares before the potential index addition. Even if one thinks the stock is expensive why sell before that gets announced unless one thinks it’s already priced in.

-

Most investors project their own investing style on Fairfax which is a problem when most investors are pure quality or pure value investors. It’s too hard to understand a probabilistic style of investing so they just pass. I expect them to make mistakes because I have the same investing style and also make mistakes. The net result is BVPS has CAGRed at 18%+ for 40 years and with the current set up there is no reason why that can’t continue. If someone thinks that’s expensive at ~1.4x BVPS, they should sell. They certainly have been for the past 8 years at lower multiples with the float down 7m+ shares (including TRS) since then.

-

What's your average ROE estimate for the next. 5 years and what multiple do you think that's worth?

-

I think of it as them buying back shares when they entered the TRS on a deferred payment plan. That is, the TRS, was just financing.

-

They were probably smart enough to do it in CAD. Is there a way to check?

-

We know it’s not that different since they paid a class B dividend in March as well so at most there was 9 months of accrued dividends. They can’t pay Class B dividends until the Class A are fully caught up, correct?

-

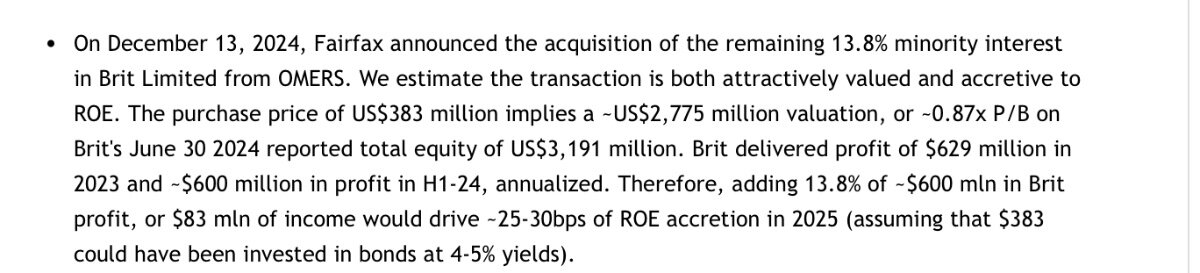

I’m just doing simple math based on the filings. We know they put in ($375m), we know the dividends they got paid (~$60.3m) and what they sold for ($383m). Might actually be closer to 5.5% but I don’t think it matters much to be exactly accurate. The 5 year yield at the time OMERS entered into the deal was 80bps so they earned a big premium for arguably very little risk.

-

They said on the call it will be filed on March 7.

-

National Bank assessed the purchase price. I think it was a 6% preferred return from issue.

-

I assume the dividend is so Prem and the employees can afford to do some good works with their wealth while they are still alive! Also, it’s probably better for people to not get used to selling if they are going to enjoy the whole ride.

-

I think it’s arguable Fairfax has a better culture and the SBC might be a big part of that.

-

One would think this fact alone would lead to the shares trading at a premium. The guy in control makes all his money from his own capital allocation decisions. True skin in the game. Berkshire seems to benefit from this trait. In the scheme of things $600k vs $1 isn’t much different when the net worth is measured in billions.

-

A nice thing about Fairfax is that Prem doesn’t take any SBC and only pays himself $600k (that agreement might expire this year) so he isn’t benefiting from salary inflation that most firms suffer from. That being said, the SBC is a huge perk because it makes the compounding even more impactful and thankfully it comes with shareholder alignment.

-

Morningstar is a quant screen and when thought of in that way it makes total sense. Brett could help increase the target price by having realistic estimates beyond the next two years and by increasing his view on the quality of the moat but he covers 20+ other companies and some of them screen well. The target price is calculated by Morningstar’s model so that’s why his estimates and moat assessment are important. As a big data exercise it makes total sense but to an idiosyncratic investor it’s nonsense.