SafetyinNumbers

-

Posts

2,822 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

That’s sort of how I think about it. We own them until they vest but we don’t get the benefit from them. So not an asset but not dilutive until they vest. If FFH issued them when they vested it would be a much more expensive program.

-

I think fully diluted shares should be used for EPS and FFH does do that. For BV, it seems like double counting until they vest. Fairfax has already spent the cash which is reflected in the balance sheet and the shares don’t actually get issued until they vest. I believe the expense runs through the income statement over the vesting period.

-

James East pointed out the EUROB buybacks over on X. I appreciate the aggressiveness!

-

Are sovereign downgrades more about currency (lower) vs default or yields risk then?

-

They think they are being conservative using fully diluted share count. I think they are just wrong but it’s not a fight I wanted to have when I met with them.

-

Every Canadian PM I speak to has no idea what’s going on under the hood and they don’t care. That being said, I think the Raymond James initiation opened some eyes up in the US. Combined with Berkshire being expensive and reality setting in on Buffett’s age, I can see FFH getting a steady inflow from BRK trimmers. It doesn’t take much given the relative size and buying until parity in valuation is an easy decision if based on forward returns.

-

Thanks for sharing. Eurobank is the second biggest name in the GREK ETF and Metlen is fifth. These are big companies that are arguably comically undervalued. It’s smart for the analyst to get aggressive on Metlen before it lists on the LSE as its likely to atttact passive demand that will move the rerating along faster. The eventual LSE listing that I’m excited about is the Ki IPO. It’s got all of the characteristics to get investors very excited and perhaps award it a better than fair valuation.

-

From press reports it looks like BIAL reported record earnings but I haven’t seen the details.

-

In the PR, they say WEF III will be used for subscription receipts to keep WEF above 50%. I’m not sure why that’s important as they will release more shares to LPs anyway.

-

I believe there was a filing from Zenith on the commitment, a PR from WEF and the final confirmation in the annual report.

-

Actually FFH is ~75% of the committed capital at WEF 3 so they will be increasing their position dramatically if this deal gets done.

-

Awesome. Thanks for sharing.

-

Do we know the preferred return for Allied and Odyssey minority interests? The TRS financing rate is probably floating and the cheapest but they might run into a notional size issue again and need to reduce it again.

-

I think you misread that. They bought $75m or ~21% of the issue.

-

Looks like Aginco significantly increased its % ownership and Fairfax slightly decreased its % ownership.

-

Mako has worked out pretty well so far this year but arguably it’s much cheaper than it was when this was originally posted because a) the gold price is up a lot and b) MKO picked up a gold mine in Arizona for almost free by acquiring it out of bankruptcy. An excellent investor and skilled investing communicator just wrote it up for his substack. If you are a Canadian value investor, chances are you already subscribe but if you don’t you should even if you will never buy a gold stock (probably 99.9% of investors so you are in the majority by a wide margin!). The substack also discusses Sailfish Royalty FISH.V which has a common controlling shareholder with Mako. I am on the BOD of FISH and my position is up to date on SEDI (although easiest to check via CEO.ca). https://open.substack.com/pub/canadianvaluestocks/p/mako-mining-and-sailfish-royalties?r=ecc87&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false

-

New 13F should be out this week (May 15 is final day to file).

-

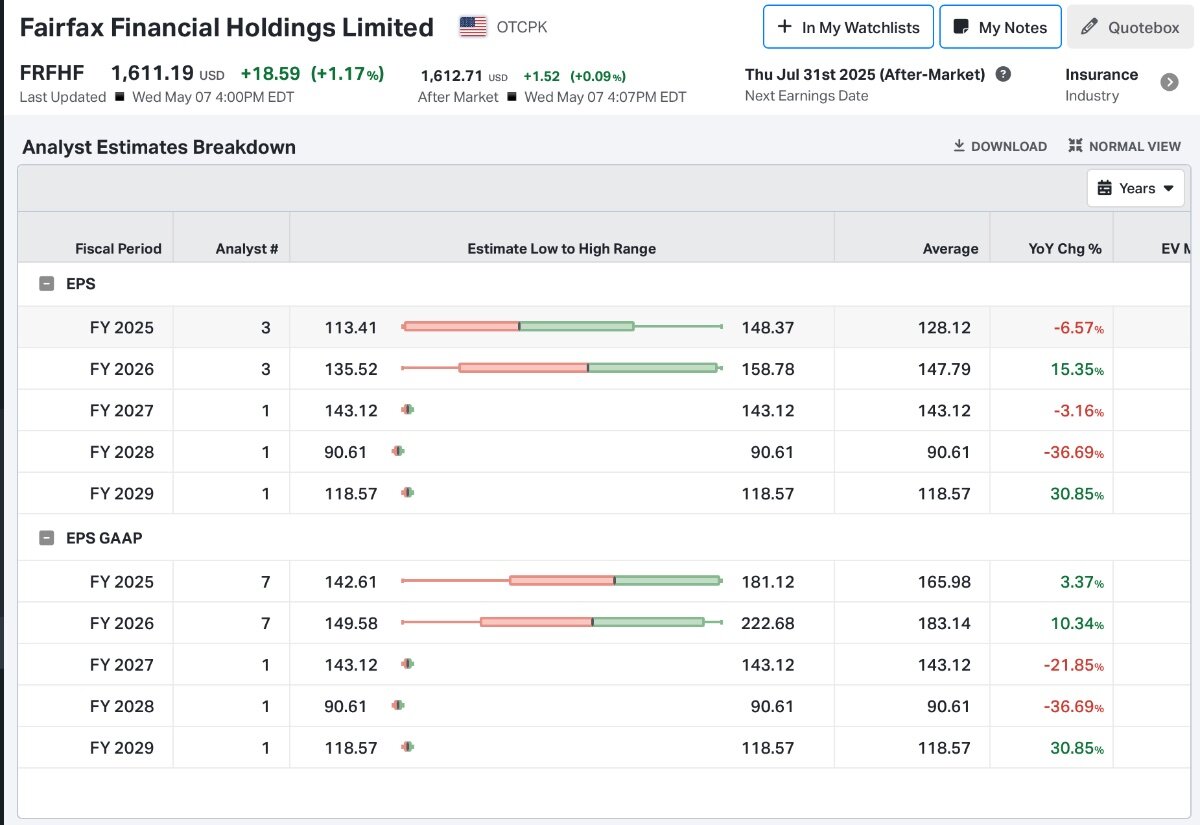

I think FFH will end up in the low 90s over the next few years as the benefits of the hard market make their way into reserve releases. Just another spot where consensus estimates are probably too low.

-

What RJ downgrade? Last thing I saw was that it was added to their Best Ideas list on Tuesday?

-

This week’s dividend was up to €0.105 from €0.09 last year so a little tastier! I wonder if FFH will sell every time Eurobank buys or if they do a block when they have to.

-

Fairfax and everyone else gets their dividend cheque tomorrow. The buyback also starts tomorrow. It’s for ~3% of the market cap from what I can tell. It will be interesting to see if it makes an impact.

-

Kinsale’s edge is being able to write policies with smaller ticket prices because they use technology to increase the productivity of their underwriters. By being fast and productive they end up with positive selection bias which increases their profitability. Fairfax seems to be spending more money recently on technology and have stated they expect to take learnings from Ki and Digit across the rest of the company.

-

The narrative is high market share, the best management and accretive acquisitions. In reality, I think it’s the analyst estimates which are tight and up and to the right suggesting growing and highly predictable earnings. They help by reporting adjusted EPS that has less volatility than IFRS EPS. Quants really dig it.

-

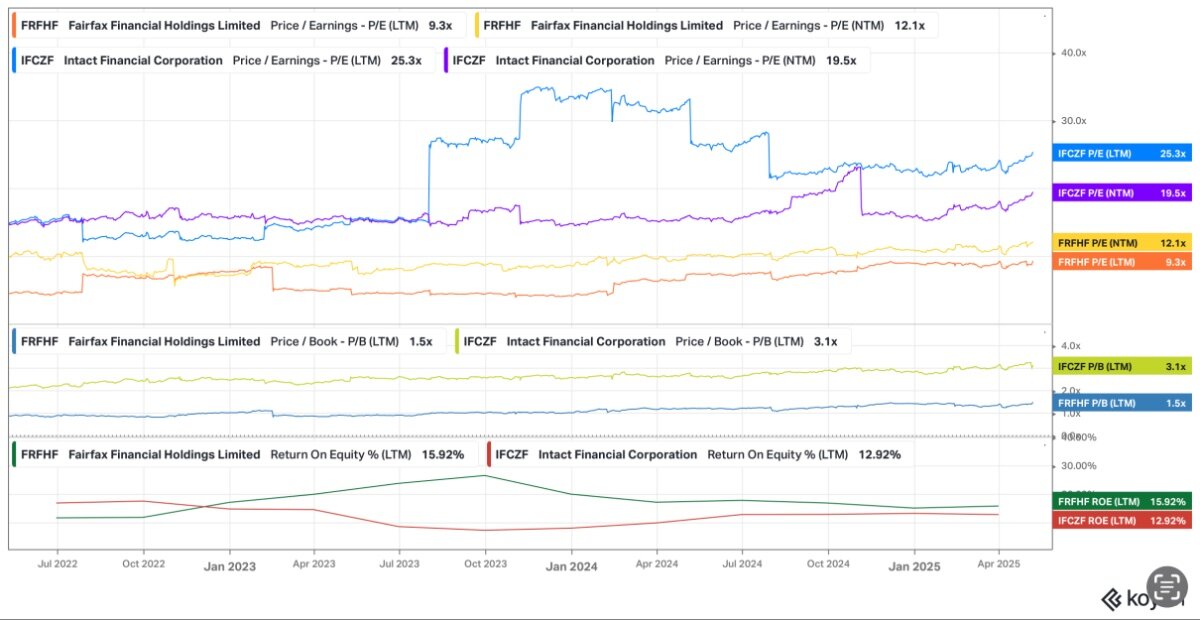

I don’t think it means necessarily that someone is too big. I think a lot of value oriented investors that have survived since the GFC have a very high fear of drawdowns so can be quick to take profits. Being on a prop desk I was trained to trade around my positions so I need to fight the urge to trim often with most of my positions. Fairfax is an exception because on a look through basis most of its assets are treasuries and the rest are very diversified. It’s really hard for ROE not to average above 15% for the next 5 years. It’s also hard for the multiple to contract much given the excess capital for buybacks and the inevitable 60 add. If I’m staying consistent with my sell plan, I wouldn’t be a seller no matter what the multiple is because I predict FTM ROE to be north of 10%. East to say, hard to do but I hope I get tested at IFC type P/B multiples. Those shareholders seem very content to hold given the 17% expected forward ROE.

-

It’s 7 shares. Someone probably made a mistake