SafetyinNumbers

-

Posts

2,824 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

FFH is still in the S&P/TSX Composite so it does get impacted. It should be something investors switch into in the Financials given USD exposure.

-

The IPO was at 272 so it’s up almost 10% from there. The business seems to be doing well so it’s probably just profit taking in an overall weak market for Indian small caps and financials.

-

It’s all relative but it wasn’t hard was it? That’s also why they agreed to a 6 month lock up.

-

What are you listening to ? (Music thread)

SafetyinNumbers replied to Spekulatius's topic in General Discussion

My favourite band is Peter Cat Recording Company. I happened upon them because they were in Toronto recently and unfortunately I found out the day of and already had plans. My favourite song is People Never Change and while it’s not one of the featured songs on the new album I think the lyrics especially are awesome. -

I went. It was a great trip. Around 20 people including ~10 investors. Every management team we met was impressive including that of Fairbridge. All of the positions seem undervalued. Hopefully more investors will go every year and that will help close the discount as I’m much likely to hold onto my position for the long term as opposed to trading vs the discount. After seeing BIAL in action, it makes one think anything is possible in India and FIH is a right tail on that opportunity precisely because it’s actively managed and not passive.

-

It’s the biggest company in the Greek ETF. It’s like saying it would be hard to do a secondary in Royal Bank.

-

They could participate pro rata in buybacks much like Exxon does when imperial Oil does buybacks.

-

FIH has a bigger discount but FFH has more leverage. Margin of safety seems high on both.

-

Fairfax India did an investor trip last week. My guess is that helped.

-

That’s helpful thanks. I gave up my CPA for a reason! At least it’s just an intellectual exercise only and not an issue that we have to worry about with FFH/Eurobank.

-

I was thinking a joint venture is like a partnership where there may be liability but an interest in a corporation would have limited liability i.e. non-recourse given the structure.

-

Joint venture would be different than equity accounting wouldn’t it? I was trying to think of a scenario where a liability would be created in an equity accounting scenario.

-

I believe a gain has to be recorded in that scenario effectively reflecting the bargain purchase.

-

Fairfax includes its share of earnings from Eurobank based on its ~34% ownership so the carrying value goes up by that amount every quarter. The dividend moves from carrying value to cash but since it’s gone through earnings once it wouldn’t make sense to put it though earnings again. Does that make sense?

-

Fairfax doesn’t have a lot of exposure to Canada. If there are big dislocations they could take advantage of them.

-

The swaps have different counterparties and different expiries. The crosses are likely just technical in nature but need to be refreshed for legal/accounting reasons. I assume they are just internal crossed from one bank subsidiary to another bank subsidiary of the same bank.

-

Today’s blocks look like them rolling the TRS. It happens every year since they put them on. There will be more over coming days is my assumption.

-

Any colour on the blocks? Time, size and who the brokers were?

-

FFH can only buy 9360 shares a day max unless they use the weekly block exemption. Yesterday there weren’t any meaningful blocks so it’s unlikely they bought more than the daily limit.

-

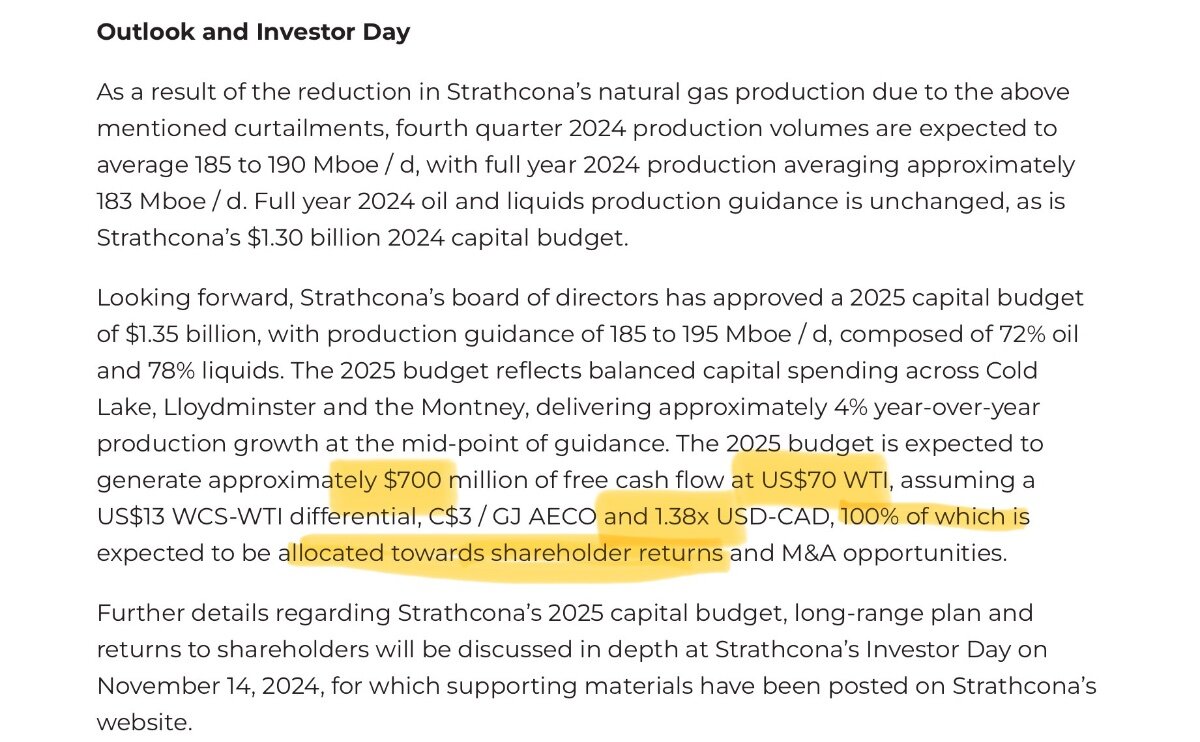

No problem. Since the Investor Day, oil is up $6, CAD is down which means FCF is probably up to ~$1b from $700m all else being equal. Meanwhile, the stock is down today because it’s not in XEG/XIC yet.

-

I think it’s just because it’s owned by value oriented investors who are worried about the market as a whole are trimming with no passive and quant inflows to offset it.

-

Have you considered SCR.TO instead of OXY? The investor day presentation especially the first 48minutes is worth a watch. Adam Waterous is already a legend on Bay Street as a banker but well on his way to making it as a creator of great companies.

-

Yeah, that’s the general idea. Stronger CAD and stronger Canadian economy is better for CAD exposed financials. It’s just a bet on the narrative impacting flows. I don’t think there is a lot of probability analysis around it.

-

Maybe sending a signal? December buybacks should also be announced by the end of the week. Given the large print near the end of December, they might have bought back over 1% of the shares last month alone. I have been picking away too despite vowing not to add anymore (it’s now a 47% position). I think the underperformance is due to some Canadian active managers moving to make their Financials exposure more Canadian and economically sensitive following Trudeau’s resignation announcement and selling that was deferred for tax reasons. Reasons to sell that are not related to FFH’s intrinsic value in other words. The short term catalysts prompted me to add but perhaps the market won’t respond as I expect. In the next 3 months we’ll have Q1 results which should be well above consensus, the shareholder’s letter and the AGM. We may also get more information about potential Anchorage and Ki IPOs. BVPS inclusive of the dividend might be $100+ higher in just over 4 months when they report Q1.

-

To be fair, I think he bought those shares on margin and I’m assuming kept what he didn’t need to sell to pay off the loan.