SafetyinNumbers

-

Posts

2,816 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Currency should be a help to BVPS as the hit in Q4 was through comprehensive income and bypassed the income statement.

-

I agree the TRS are essentially leverage to fund future buybacks. I just took issue with the assertion that the TRS will contribute less to profits going forward. By the way, have you calculated the quarterly contribution of the TRS since they were put on to measure the earnings volatility you are concerned about?

-

I don’t reach the same conclusion on the TRS as there are fewer shares outstanding than when they first put on and a smaller percentage change in the share price has a much bigger dollar impact. Unlike most, I also continue to expect multiple expansion so the percentage returns might continue to be robust.

-

I assume it’s at least the dividend yield since the stock is trading at the conversion price. I wonder what the rationale is for the structure. Maybe better capital treatment for Fairfax.

-

Is there a coupon on the exchangeable? I can’t seem to find it.

-

I think it’s more about who owns the minority, why they bought it and what they expected on this deal than risk of the deal closing and valuation.

-

That’s what Anchorage is supposed to do. My understanding is they have been bidding but have so far been unsuccessful. More to come.

-

I went to see KNSL in Richmond back in October. They are very smart, disciplined and have a cost advantage over their peers using technology. They write smaller business and their underwriters are more productive. I don’t want to pay 7x BV either but I understand why it trades there.

-

It will be interesting if reserve releases keep ticking up to offset some of the cat loss pressure. I assume that grows over time as premiums were growing pretty fast 4 years ago. I think the consensus reflects the impact of wildfires on underwriting income.

-

KNSL has a structural advantage on its combined ratio which is why it has such a high ROE. It’s quality because it has high returns and predictable growth so it gets a high multiple.

-

Over $15/sh from the mark to market (including ORLA converts, warrants) as it stands now in Q1 while consensus is only $30/sh in EPS. Seems like another beat is brewing.

-

I’m worried about being long all fiat currencies although I may be positioned too aggressively in that direction. I’m not too worried about the rupee. India and Indians own a lot of gold. That should help support the currency.

-

Within the first 10 days of the month FFH has to file the previous month's buyback activity. I agree with @gfp that SEDI is a pain to use. I find https://ceo.ca/ffh to be an easier way to see new filings. Btw I thought it was impressive our new CFO has ~8500 shares already!

-

Well said. Returns for Life and Reinsurance might end up being as good as Digit. More right tail seeds planted like Ki 5 years ago.

-

She also has over 8k shares based on her initial sedi filing which is pretty impressive.

-

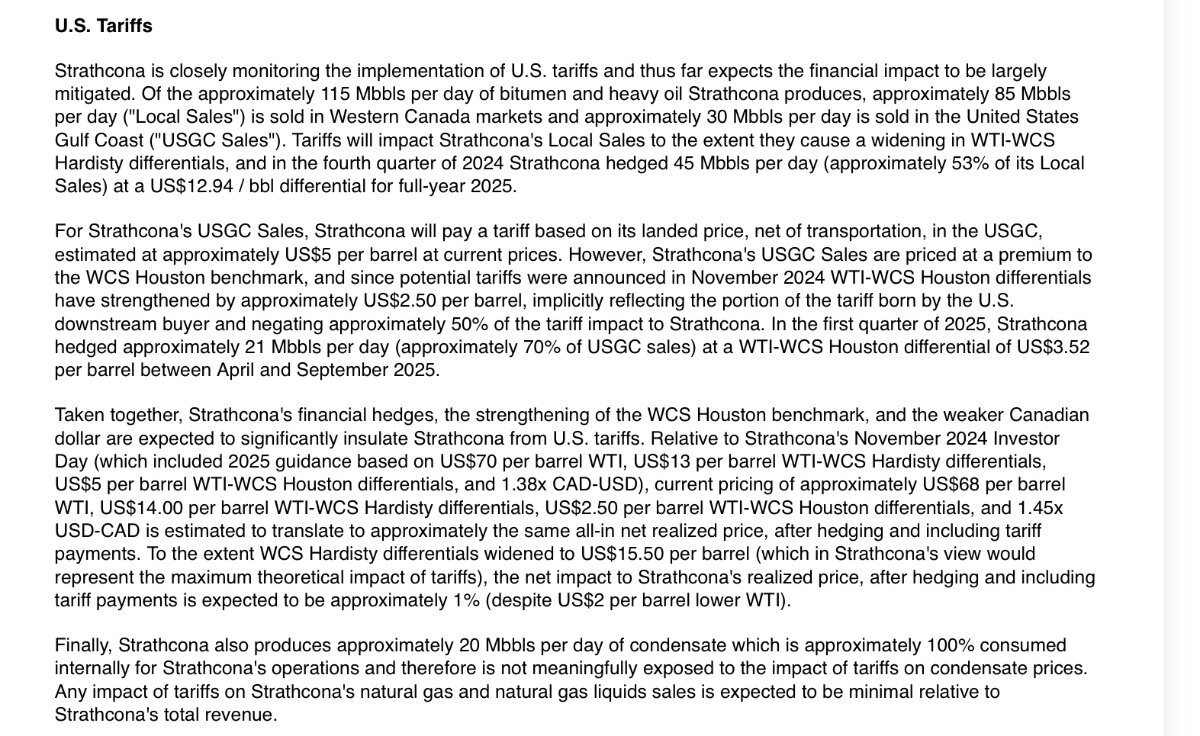

FWIW, the company had the below to say on tariffs when they released Q4 results last week.

-

If they bought the max every day but they haven’t done that historically.

-

Prem guides to $150/sh before gains for the next 4 years and CIBC is at $127 and $146 for 2025 and 2026, respectively. They are less optimistic on underwriting and don’t understand how duration works in the bond portfolio as they fear lower rates.

-

They cancelled the shares they bought in all of February on Feb 28 but they are capped at repurchasing 9,360 shares per day unless they get the opportunity to use the weekly block exemption.

-

Plus the FIH performance fee to FFH.

-

I think it’s logical to buy ahead of potential price insensitive buying but apparently most investors share your perspective which I don’t understand but that’s what makes a market.

-

It doesn’t impact the timing of your purchases at all?

-

Does the potential announcement tomorrow that it will be added to the 60 impact your decision making? I bought a bunch in January and February because I thinks the odds of the 60 add are good which could result in long lasting multiple expansion and the number of potential lottery tickets seemed to keep growing. Maybe I’m too excited about BIAL, Ki and optionality of the portfolio. It was my way of getting more defensive to a certain extent because it’s more bonds per share than the share price and buy the dip is built in. It’s now 5x+ my second biggest holding which is a gold stock (Mako Mining MKO.V). I’m guessing that is unique on this board and definitely not recommended although I appreciated Ian Cassel saying that he also owns a junior gold stock and had a 9x during the last bull market for gold stocks 20 years ago. Everyone is so focused on what could go wrong the margin of safety is off kilter. <2% positions make more sense than my 9%+ position but I feel comfortable being able to sidecar the with Wexford Capital which owns ~48% especially at what I perceive as a nonsensical discount to expected value. In that regard, similar to Fairfax!

-

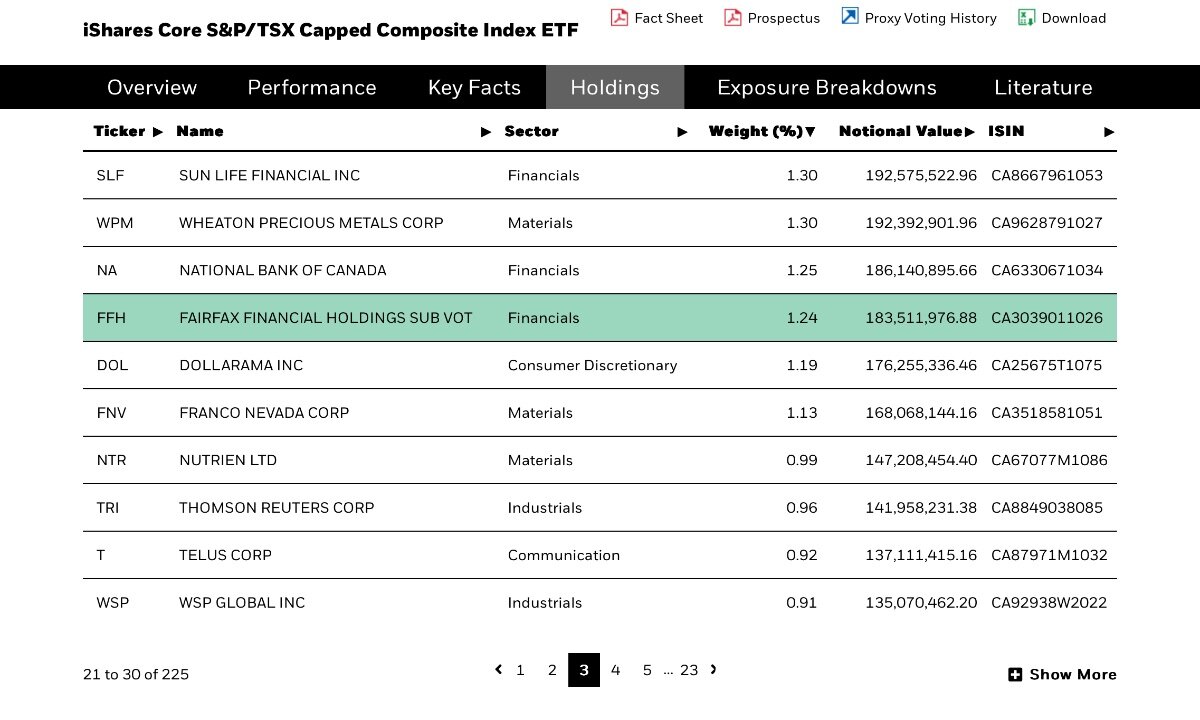

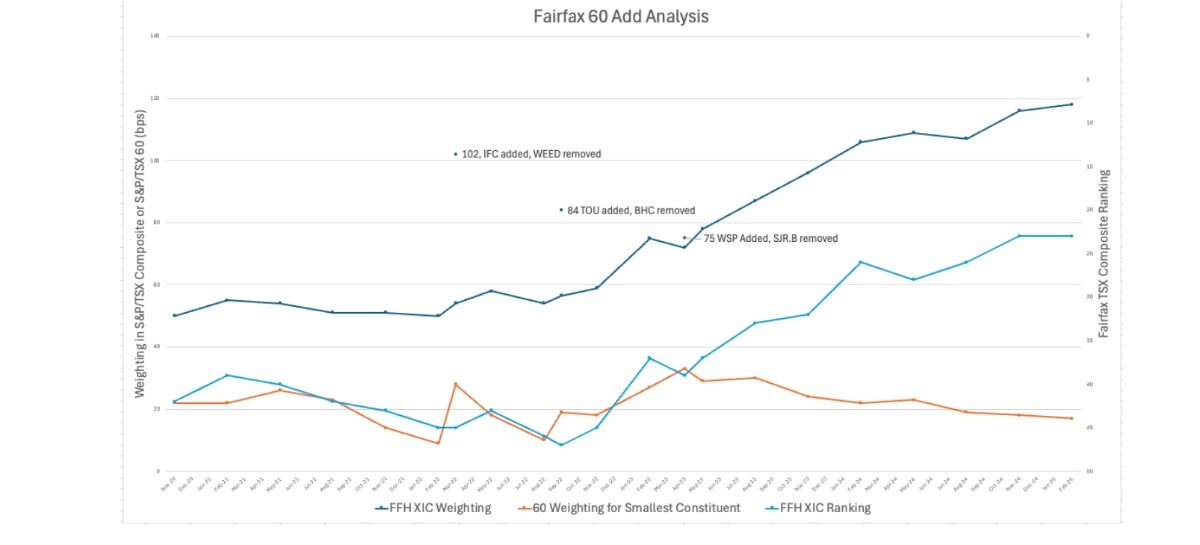

Float cap matters more than market cap. On that basis it’s 24th! Plus a chart that shows the progression of the weighting and rank for the past few years.

-

SCR reported earnings and put out their annual reserves letter to shareholders. I estimate FFH owns ~7-7.5% of the company which is a ~$260m position which is a much lower mark than a few years ago when it was private and the CAD was much stronger. The earnings were in line. They kept 2025 guidance despite the impact of tariffs based on a combination of spreads tightening, hedging and CAD weakness. They highlighted YTD production is at the high end of guidance so it’s possible it will be upgraded mid year. They also increased their regular dividend from $0.25/q to 0.26/q explaining its linked to production increase and/or decrease in costs. Recall during the investor day, they suggested the regular dividend could be $3 in 2030 and now we know how they will get there. Regular dividend increases should make SCR attractive to dividend ETFs and benchmarks over time. First it has to get into the S&P/TSX Composite though which is just a matter of time. I think the shareholder letter is a terrific read so I have attached it. Over time, I think their execution and communication will result in a very loyal shareholder base that will hold it even when the stock trades above NAV as opposed to well below it as it does now. That’s my plan at least. Strathcona-2024-Reserves-Letter-Final.pdf