SafetyinNumbers

-

Posts

2,824 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

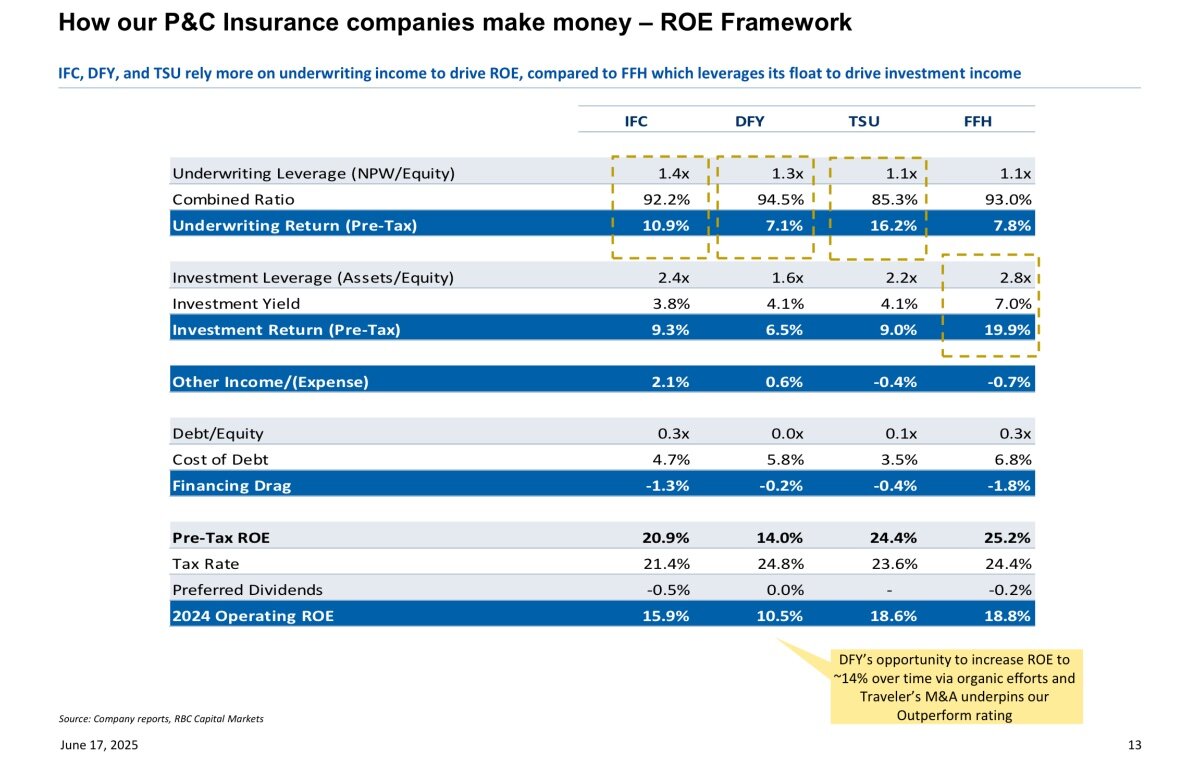

Kudos to Bart (the RBC analyst) for creating it. It shows how much leverage there is to investment returns in a very concise way. The next step is to breakdown where the returns on investments come from (fixed income vs other), see if those expectations are also reasonable and determine a range of potential returns.

-

BRK is a tough comparison because of how successful they have been on the equity side of the book and how few insurance acquisitions they have done compared to Fairfax. Vs the other Canadian P&C’s Fairfax is at the low end of the range.

-

Attaching the article I wrote last year explaining why I thought FFH’s next 30 years will look better than BRK’s last 30 since this topic is getting some discussion. Probably more relevant than ever as some holders are thinking of reducing their position in BRK now that Warren is taking a step back. BRK won mainly because Warren was really good at picking stocks and less so because of the float leverage. In this inefficient market, if FFH can pick stocks well and enjoy the float leverage, the returns can exceed expectations. Based on the current multiple expectations are low. FFH G&M 5.1.24.pdf

-

Mr. Kant spoke to the group that went on the Fairfax India trip and I found him to be very impressive. Hopefully his influence and contacts will help move things like the Anchorage IPO along which will boost FFH and FIH book values meaningfully.

-

Every time they buy back shares they increase future ROE because the current assets have the same/growing earnings power and buybacks over BVPS reduces BVPS making the numerator all else being equal.

-

I think investors that cite that book value is not relevant (especially true of BRK holders) forget that if BV is understated then it should show up in a higher ROE as you highlighted Viking. I’m not sure if the relationship between BV multiple and ROE has to make sense over time but it does provide for high margin of safety entry.

-

He’s a quant. They are never going to like Fairfax. Unfortunately a lot of brokers won’t buy anything not Morningstar approved because quants keep their jobs.

-

Thanks Viking. You have done amazing work and we all appreciate it. @kodiak got me into Fairfax originally and then I started to read the board! Every one in the eco system has helped me gain conviction. While I find the negative feedback exasperating sometimes it does help increase confidence that I’m not missing anything as it’s usually some heuristic that has nothing to do with intrinsic value that is the basis for their objections.

-

The relationship between ROE and BV is relevant for balance sheet based financials like insurance companies and banks. I think the focus on quality from institutions and quants alike has herded investors into companies that have the most predictable growing earnings based on analyst expectations so that’s part of why they keep their multiples despite not living up to expectations. Analysts at BMO for example use operating ROE alone and ignore the equity portfolio which seems overly punitive. The multiple goes up a lot if trailing 3-5 year average ROE is used instead. Alternatively could think about 1.6x BV as below plus the value of the $20b equity portfolio which seems like a reasonable estimate of fair value.

-

Arguably IFC has a big moat in Canada for retail P&C and on that basis expected ROE is considered high (~17% at current interest rates) and predictable assisted by reporting adjusted earnings i.e. ignoring gains and losses. Actual ROE hasn’t hit that in years. WRB I’m less familiar with. Fairfax will get the multiple eventually because of index flows and Canadian institutions forced to buy it to keep up with their benchmark but the narrative will be about something else.

-

I assume they will keep shrinking as the nominal amount grows but I’m not in any hurry. Effectively taking it off is just another way of reducing leverage. I do like that it helps FFH almost always beat the consensus for the quarter since analysts can’t be bothered to model it.

-

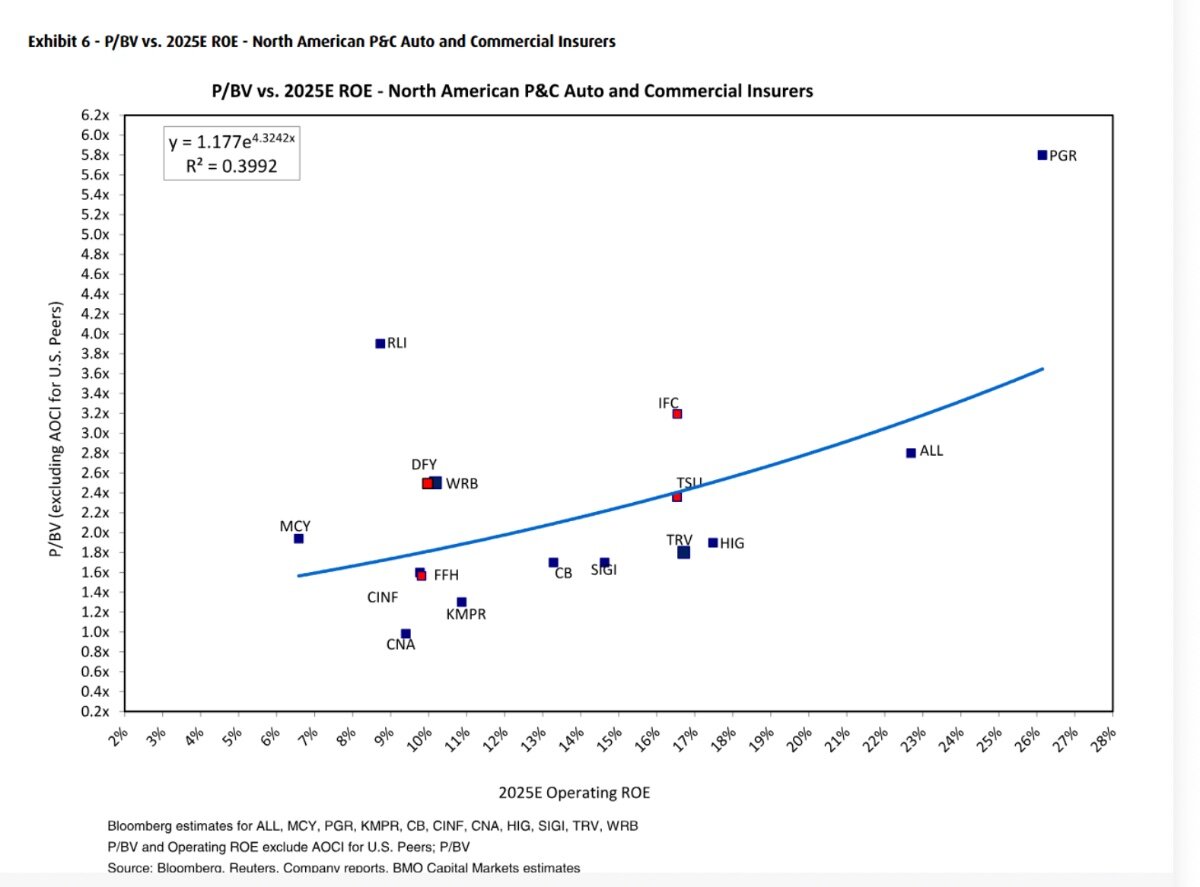

I posted this on Twitter yesterday. Still some catch up to do with IFC and WRB.

-

I think of Fairfax as expected value investors meaning they can do any kind of investment as long as it makes sense on a risk/reward basis which includes value, quality, venture capital, distressed etc… I consider myself to be an expected value investor too so I feel very simpatico with their style and it’s probably why it’s so easy for me to forgive them for their mistakes as I make them all of the time too. “Even the best investment analyst is going to be right just two out of three times.” - John Templeton

-

Actually they moved coverage back to Canada after their US analyst left a few months ago. They also initiated on IFC with a neutral. It’s possible we see some switching out of IFC into FFH on the margin as Canadian institutions are way overweight the former vs the latter.

-

That’s what I thought too but trading action suggests someone thinks otherwise.

-

It’s interesting that it’s trading through. Is there an opportunity for a bump here to get a big shareholder over the line? 1832 seems to own ~15%.

-

The P&C holdco model seems well designed for an inflationary environment because premiums are able to be increased relatively quickly for inflation expectations. Interest rates tend to go up and term premium also increases to reflect inflation expectations which increases returns given the leverage to float. These companies also own real assets via equities. For FFH if one includes the TRS, their equity book is of similar size to their shareholders equity. Real assets are more likely to outperform in inflationary environments.

-

That’s when they cancelled them. They bought them a few weeks earlier.

-

I don’t think the S&P 500 is the benchmark for equity returns. I believe they use a 15% hurdle rate for equity investments but at 3:1 leverage if they get a 5% return it still contributes to pre-tax ROE at 15%.

-

Like all quants, Canadian institutions, like growing highly predictable earnings estimates. Actually hitting them is not a real concern. It will be interesting if Fairfax shareholders hold on to their shares long enough to get the multiple expansion tney deserve. If not, more buybacks.

-

Or IFC at ~3x. Canadians are willing to pay it, just not for FFH yet. I think that we’ll get there while we still have reasonably high visibility on forward ROE which makes it easier to hold.

-

Low probability as long as AQN hangs around 20bp based on precedent. RBA also went into the Composite today so they have more competition since it’s an industrial. We might have to wait until something in the 60 gets bought and creates a spot.

-

Free link to Barron’s article: https://www.msn.com/en-us/money/savingandinvesting/here-come-the-berkshire-hathaway-wannabes/ar-AA1GbLiM

-

Great quote @kodiak

-

I think there is good reason to believe they can find more resource at Moss. The last operator was constrained by capital and by permitting which explains the short mine life. Mako doesn’t have a capital constraint and permitting should be easier under the new administration.