John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

I share your personal sentiment here, @backtothebeach, No real news announced from Berkshire since in January 2024 about the Flying Pilot J acquisition settlement. *sigh* *Holding my head up, so I don't drop my forehead on the 'sell' button on the keyboard, out of pure boredom*

-

Here is what I phrased earlier today in this topic, unsubmitted, and as a draft : By now, I regret what I posted in this topic, about 17 hours ago. - - - o 0 o - - - We need to get along here on CofB&F.

-

Enjoy your fun, James [ @james22 ], Reuters - World - Europe [February 20th 2025] : Exclusive: US refusing to co-sponsor UN motion backing Ukraine ahead of war anniversary, diplomats say. Why do you consider it funny that someone reacting to that they can't take the words of your POTUS at par? What is actually funny about that?

-

Mike [ @cubsfan ], You're simply right. It has been dumb, naive and also reckless, I would say since 2014 [Crimea]. But you have to follow and track the extreme and violent changes going on by now, some of them by WARP speed.

-

@JoJo1, Please do your own individual check up on posts from active participants in the discussion in this topic and compare it with such members' contributions in topics in the CofB&F Investment Ideas forum. If you need some practical guidance about how to do, please feel free to send me a private message about it. - - - o 0 o - - - The variant perceptions presented here in this topic aren't really an expression of some CofB&F members in one certain 'opinion camp' lacking knowledge, competencies, nor qualifications etc. - - - o 0 o - - - -And btw, here, a belated welcome to you!

-

@JoJo1, You obviously have no idea of what you are asking about here, lol!

-

Thank you, Mike [ @cubsfan ], Now we're getting somewhere, so I can understand you. In fact, I personally think we now disagree much less than what was perhaps apperant before your last post above. This is most of all an European issue, and the European countries need to step up to it - absolutely immedially. Your POTUS is out of line and going rogue here by now. I'll elaborate later.

-

Awesome entertainment! For your information : Andreas Mogensen is Danish [, like me].

-

I agree with @Gamecock-YT here, above. Mike [ @cubsfan ], It's a behavioral problem - of yours - while discussing in this topic. Have you even thought about how you're actual phrasing of the content of your posts lately appear condecensing and patronizing, all while you - constantly, on and on - ignore and disregard the points brought up several times, by several CofB&F members, including me, about the trustworthyness of Putin, ref. the concept of 'lasting peace'. In short, you're by many European CofB&F members and others considered naive, short term, or both.

-

Related to the above part of Saturdays post by Charlie in this topic and the above mentioned WaPo article, there may exist some kind of overall guidance of the future demand dynamics, and thereby future US defense spending and capital allocation, based on investor specific knowledge about each individual defense contractor :

-

WaPo has a good article today on this initiative by the current administration : Washington Post [February 19th 2025, updated February 20th 2025] : Trump administration orders Pentagon to plan for sweeping budget cuts Subtitle : A senior Pentagon official said that money saved through the cuts could be “realigned” to other defense priorities that President Donald Trump has. - - - o 0 o - - - The initiative divides into two parts : and : Is this how the United States of America treats its veterans going forward and into the future?

-

Pretty amazing and thought provoking to read the above from Charlie [ @dealraker ] Saturday, to see what Hektor [ @Hektor ] wrote about here in this topic yesterday, and now today the above by @Spekulatius - - - o 0 o - - - Soon a new concept called "American oligarchs' will be introduced, a designation similar to that of Putins cronies, but with its own independent existence and life.

-

Thank you for sharing, Charlie [ @Charlie ], Great overview site. Yes, and as if there isen't enough else to be concerned about these days in Europe.

-

Somebody seem to have forgotten how and what this started with. Mike [ @cubsfan ] & Greg [ @Gregmal ], Du you remember? : United Nations - 8974th Meeting (Night) [February 23rd 2022] : Russian Federation Announces ‘Special Military Operation’ in Ukraine as Security Council Meets in Eleventh-Hour Effort to Avoid Full-Scale Conflict Subtitle : ‘Give Peace a Chance’, Secretary-General Stresses as Political Affairs Chief Calls for Dialogue ‘Even at this Late Hour’ - - - o 0 o - - - ABC News [February 24th 2022] : Russian President Putin announces military operation in Ukraine

-

Personally, I appreciate your posts in this topic very much, @Pelagic ! I hope you woulden't mind to share your nationality, thank you in advance, meaning also : If you mind, that would naturally also be OK, and would be respected.

-

https://truthsocial.com/@realDonaldTrump/posts/114031332924234939 @Xerxes, He is a disgrace to The Office. Do you remember the concept of 'The Alternative Reality' under his first presidential period?

-

Which interview, @Xerxes ?

-

Mike [ @cubsfan ], Why do you continue to derail this topic with these kinds of political nonsense and *BS*, not related to the war we discuss here? To me, by doing so, you are playing with the posting privileges of others in this topic, who can stay on topic here.

-

The yearly Semper Augustus Letter expected this Friday [21st February], obviously whole production process and release under supervision of Big Oil :

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

Berkshire Hathaway - Press Release [February 18th 2025] : 2024 Annual Report Release Information. Saturday 22nd February 2025, at around 8:00 AM eastern time. -

Upon the MSC2025 conference, I was this morning met by the following cartoon on JP.dk - what a great start on the day! :

-

Yes, Roger [ @rogermunibond ], There is to me personally no doubt that SDs [ @SharperDingaans ] starting post in this topic has merit, because of the way all this tariff talk has been communicated by the newly sworn-in POTUS has been highly influential on general sentiment towards USA at the populations in countries being allies with USA and being hit by this tariff talk. To me personally, it's a real and tangible thing building up here in Europe by now. I'm pretty sure for EU, it'll be swift eye-for-an-eye, tooth-for-a-tooth priciples of reactions by measured reponses against USA with regard to tariffs, based on an inner solidarity priciple - 'one for all, - all for one' - not some whining by filing of complaint cases against USA in WTO. - - - o 0 o - - - Posted certainly not with the intent to politicize the topic, and here trying to be careful and conciderate in phrasing, not to stir the pot.

-

The Economist January 25 2025 edition has Euro area 2024 GDP growth at 0.8 per cent, not 0.1 per cent.

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

And the cash continues gushing in every day at Bershire, a bit below USD 3 B per month.*) [That's actually ~ USD 100 M - per day ] Has Mr. Buffett stopped taking showers and is now taking baths like Scrooge McDuck in cash and T-Bills? *) USD 25.9 billion for the first 9 months of 2024.

-

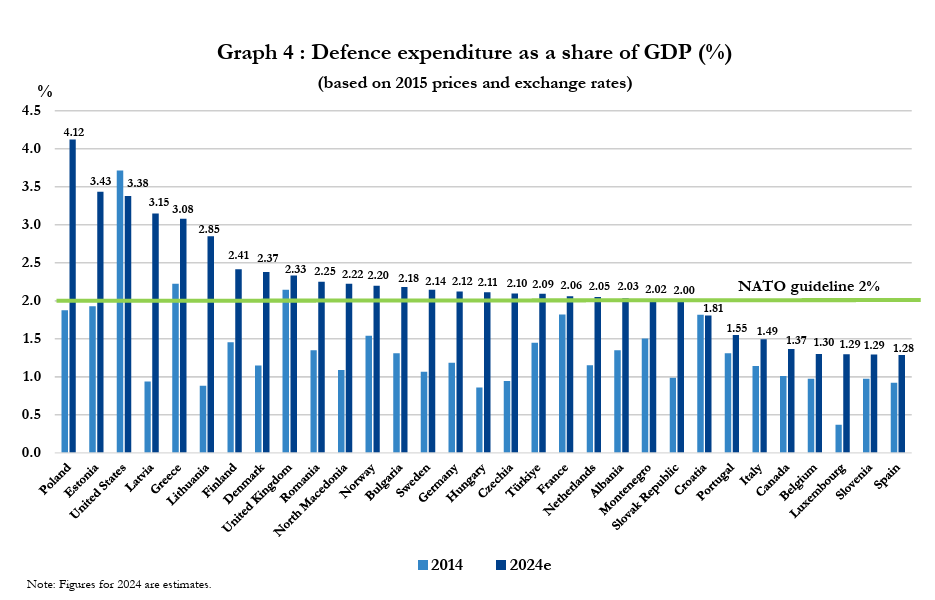

Thank you for an absolutely awesome post here, @nsx5200, Very good points. One could also call it hypocrisy or the application of double standards. It actually made my Saturday morning reading your post and the related stuff. - - - o 0 o - - - Edit : Also, please mind the actual narritive as discussion basis in the actual situation on the security conference in Munich contra latest known facts about defence spending by NATO member countries : USA representatives states that Europe is the laggard and the culprit, while the fact is that USA is not even the frontrunner here, likely Canada also holding its head low in this ongoing discussion. - - - o 0 o - - - Pravda [Friday, 14 February 2025, 22:25] : Northern European leaders urgently meet on the sidelines of Munich Security Conference after Trump's statements. Danish Prime Minister's Office [February 14 2025] : Joint Nordic-Baltic Leaders' Statement on Ukraine 14. February 2025 - Nordic-Baltic Leaders' Statement (Denmark, Estonia, Finland, Iceland, Latvia, Lithuania, Norway, Sweden). Please note where you find these countries located in the graph above. Europe isen't just 'Europe' in this context, there are certainly shades and nuances to the situation, which there thus also should be to the discussion.