John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

Munich Security Conference 2025 (MSC2025)[Friday, February 14th 2:30 p.m. - 3:00 p.m.] : The U.S. in the World - J.D. Vance, Vice President, United States of America. I have never before spent time really listening to Mr. Vance before. I simply must say : Godd***it he is good! He is of another, - totally different! - caliber [or breed] of a speaker than the incumbent POTUS. The messages from Mr. Vance passes pretty clear and as obvious into the content inside the upper part of my Northern European, semi-thick, semi-neanderthaloid skull. Does anyone hear anything in the speech by Mr. Vance below the three upper levels in Graham's Hierarchy of Disagreement? :

-

Welcome in the arena , @dipod

-

CEO Lars Fruergaard Jørgensen was specifically asked about it in an interview a few days ago. [I think it must have been in connection with the release last week of the Annual Report for 2024, which I'm still digesting and chewing on.] Mr. Jørgensen said he considered it manageable for the company, because the company already has production and production capacity in the US. The answer was phrased in a way, that I perceived it as not just a triviality, though. - - - o 0 o - - - Edit : Here is the interview : Bloomberg - Industries - Health [February 5th 2025] : Novo Sees Ozempic Boom Prompting Another Sales Surge.

-

Hongkong Land at 125 - Hongkong Land Holdings Limited

John Hjorth replied to John Hjorth's topic in Books

You're welcome, @xo 1 , -my pleasure! , I am still nosy about how this book ended up in this corner book store in a small town in the south of Great Brittain. Abebooks.co.uk provides a communication feature / module to communicate with sellers, in the evening at the day of recieval, I did send this to The Petersfield Bookshop : My expectations for a reply is about nill, the are no potential sale or earnings related to answering me, -anyway, let's see. -

Canadians, Which Brokerage do you use?

John Hjorth replied to KFRCanuk's topic in General Discussion

Thank you for sharing, @Xerxes, At least for me personally, it's always very interesting to hear fellow CofB&F members' personal stories and actual perceptions of the local or national banking landscape. -

Canadians, Which Brokerage do you use?

John Hjorth replied to KFRCanuk's topic in General Discussion

It's to me personally [, likely, as a North European citizen [ Dane]], really striking to read that today, the majority of Canadian CofB&F members [at least active by now in this topic] are hooked up on, and prefer RBC [ I call it RY, let it go, please], as their preferred service provider for DIY investment management. What is it at your past and ongoing customer and user experience that has made you decide so? I'm really eager to hear about it from you, who it may concern. To me personally, as a Dane, it would be like choosing Danske Bank [DANSKE.CPH] by now for that. [With that said, DANSKE is now trying to get there, - still no real interest from me, yet]. - - - o 0 o - - - That said, to keep some kind of structure and related simplicity to things, ref. @Viking s post about that above, certainly also matters, for practical purposes. -

My household and I have been continuous shareholders of FFH.TO since 30th April 2013.

-

Crystal clear, like in 'Bent in Neon'! - Here in Denmark, we have this similar expression, that goes 'Skal du have det skåret ud i pap?' [, translates to : 'Do you need it cut out of @cardboard ?'] [ Hint-hint ]

-

I bought the first few B shares at 10th September 2012 at 84.64, so that's today a bit more 12 years [, as the first shares since deciding to get real and serious about stock picking]. About a half year after [on 13th March 2013], I was so lucky and privileged to find CofB&F.

-

Hongkong Land at 125 - Hongkong Land Holdings Limited

John Hjorth replied to John Hjorth's topic in Books

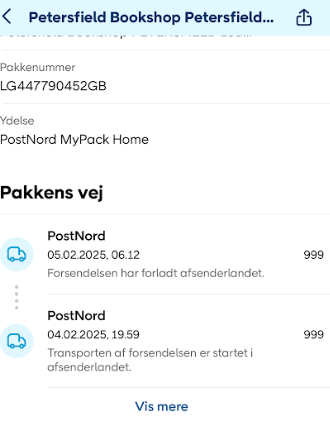

Today, the book arrived at my place at 14:30. The book is at by nature of the trade second hand, the condition was stated as 'good' [which at some market places certainly is subject to inflation], and good it was, -mint condition, except one reasonable small dent in the font binding, and some small scriblings with an old fashion graphite pencil in upper right corner on the page inside the front binder, that perhaps by their content signals this book may have been an element of a large book collection earlier in the books life and existence. The book was packaged meticulously and with care, for protection under transport. The book immediately runs into the top ten list of my personal favorite books that I own, because of the quality applied in the production process, the use of gold print, print quality in general, quality of colour photos, etc. It's simply that gem, I expected it to be. Great experience to receive it today. Here is a screen shot of the corner book shop I made the deal with, located basically in the middle of nowhere, a bit North of Portsmouth on the English South Coast. Its mind boggling to think about what it is actually possible to do and execute on in the world we live in today.

-

Mike [ @cubsfan ], @Spekulatius, @UK et. al., How do you asses recent developments, within the last few days? Are we by now able to see the end of these warfare activities, to stop all the meaningless madness.

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

You aren't discussing here fact and data driven, @Munger_Disciple, Never mind, now please let it go from here. -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

One never really know in advance the outcomes of shareholder votes on shareholder proposals, untill they are done and over with. Don't try to sell the fur of the bear before the bear is shot, or you may end up surprised, unleasantly. -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

Exactly, this, @gfp, I think the same, but I can't really back it up with data. The question is still interesting, though. Here on CofB&F we should really try - in cooperation with each other - to map where the Berkshire A-shares not owned by Mr. Buffett are owned / laying around. Perhaps we should add the B shares to the mapping, too, if we are already at it, to max, full possible perspective. -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

@Spooky, What is your basis for this statement? Who are those other currrent A shareholders? -

Hongkong Land at 125 - Hongkong Land Holdings Limited

John Hjorth replied to John Hjorth's topic in Books

Hum-ho : , Waiting for this book to arrive, is like investing for the long term : Wait, wait, wait, - then wait some more ... :

-

Hi Mike [ @cubsfan ], Thank for your latest two posts. They are to me personally, materially different - at least, to me, in positive way - from what you have posted lately in this topic. - - - o 0 o - - - Certainly something to think about in this situation. So, thank you. What happens inside my head, every time I try mentally pursue your line of thinking, every mental scenario 'collapses' by that we can't live with - as Europeans - to have a country in Europe the size of Ukraine [a grain chamber] existing as giant a demilitarized zone, up against Russia, existing based on welfare from other countries, including USA. A giant European DMZ wasteland - because of this initial Russian agression - is simply not an option - for us Europeans. All we Europeans not already attacked, already face a huge bill on.

-

You really don't understand a whit of what this is about for the Ukrainian people, nor do you even try to understand, Mike [ @cubsfan ], I'm not going, from this point on, to comment on your posts here in this topic going forward [waste of time], unless they derails totally, into the extremes.

-

I'm now giving up on you here in this topic, Mike [ @cubsfan ]. Yoy are just 'slinging numbers' around you with no data basis initially, and when the numbers *BS* by you is called, etc., you just move on to new 'statements' or what ever you may call it. - - - o 0 o - - - Above I posted a graph showing NATO 2024e numbers as of a date in June 2024 [, as the best estimate available, by then], and then you are contuining your posings of backward looking statements like : Get real, or you - for my part - get ignored. Enough here.

-

Mike [ @cubsfan ], You need to be forced to study your own approach, methods and strategies for discussing this matter. Bringing - by now! -what the former POTUS did, or did not, into the discussion, why is that relevant for this discussion, forward looking? As far as I've understood you're living in Chicago, and are thereby a US citizen, living in a democracy, with a government body with two chambers by constituon, and yet you still blame one US citizen for all this mess. Is that person, and thereby USA, thereby also you, responsible for the actual situation we discuss here? Or do you question the presidential election outcome [the US peoples opinion] four years ago? - - - o 0 o - - - That said, Anders Puck Nielsen, also to me personally, has now crossed a line, where I don't understand any longer how it's possible for him to continue these personal activities of his, all while maintaining his employment in the Danish military, as a Danish public servant. If I was his superior, he would by now had been called to my office for a talk - short one : Anders, pick one of those : 1. Putting you signature on a written, personal & instant cease and desist statement on my public activities on matters that releates to the security of the Danish State, because these activities aren't compatiable with my military employment. 2. I hereby resign effective x.x.2025. 3. Me firing you, because you refused to both the alternatives 1. and 2. - - - o 0 o - - - Here is an e-mail that I received from Anders Puck Nielsen yesterday at 17:25 [, and I don't mind sharing it, because his mailing list is public accessible] : Yoy don't need to click to get the answer to you question : DKK 249.00 per ticket, from Billetto : Text translation : Danish : translates to English by : Samuel Rachlin, author of a book about Putin, called 'I, Putin', ref. one of my earlier posts in this topic, is as such today independent, Anders Puck Nielsen is not.

-

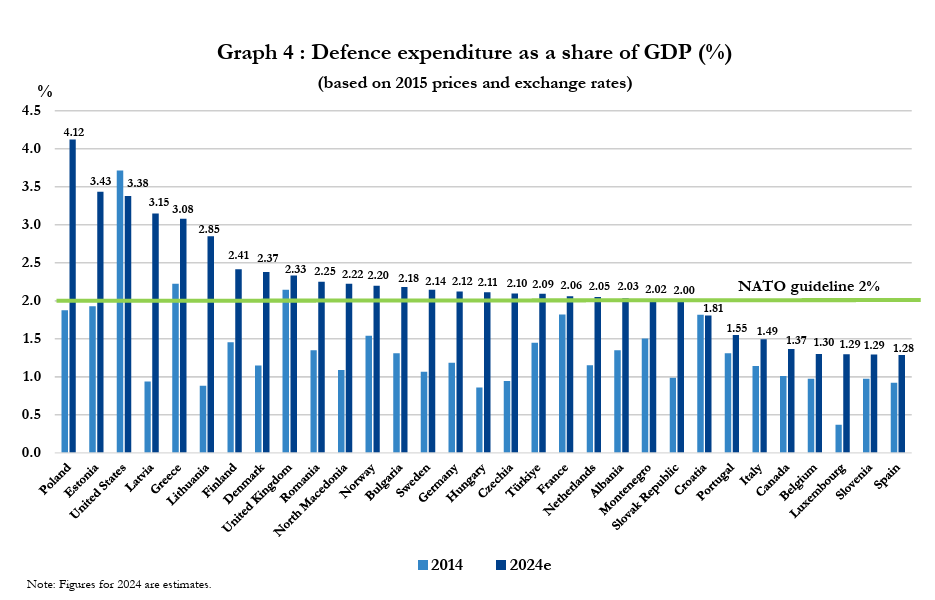

Mike [ @cubsfan ], NATO - Public Diplomacy Division [June 12th 2024] : Defence Expenditure of NATO Countries (2014-2024) Including : And the absolute majority of member countries have been ramping up since June 2024 in a material way. Here in Denmark we are already hitting 3.5 percent, by several specific political and defence decisions already taken. I.e. shipbuilding decisions can move the needle in a material way. And the political talk here in Denmark is about 5 percent now, and about how to get ends to meet in the state budget. The ramp up takes time, there exist lead times on pretty much everything in all kinds of supply chains. What naturally matters most for European countries as a whole is how UK, Germany, France, Italy and Spain are doing with this. Please note their individual rank in the graph above, and think a bit about how these countries individual economic situations are : UK, Germany, France and Italy each already have their own separate national issues to deal with, and Spain is [as usual?] just the naughty boy in the class here. - - - o 0 o - - - So, a peptalk to the laggards and ring kissing for Trump from Rutte, which is referred to by you above. Rutte is just doing the job he's paid to do with this talk. A bureucrat talking his book, which is naturally OK, but context still matters. - - - o 0 o - - - <Talk is talk, data is data.>

-

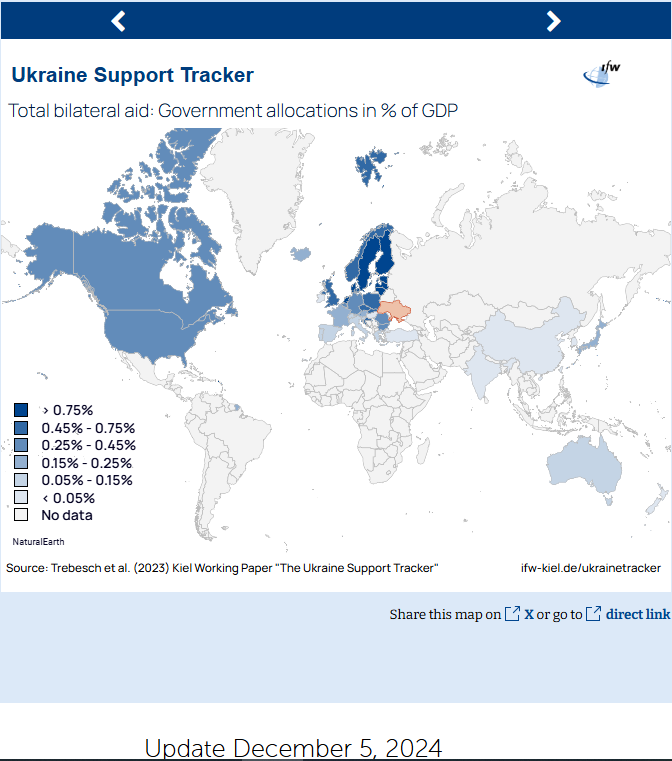

IFW - Kiel Institute for World Economy [February 6th 2025] : Ukraine Support Tracker - Total bilateral aid: Government allocations in % of GDP. Screen shot today : - - - o 0 o - - - <Do not let facts confuse you.>

-

Now you're killing me, @Xerxes!

-

YouTube - Reuters [ February 4 2025] : Trump says US sovereign wealth fund could buy TikTok | REUTERS So, now we have a POTUS yesterday asking for a plan for a soveriegn fund for the United States of America, and at the same day talking about placing a part of Tik-Tok there? - - - o 0 o - - - Are you still confused, @Xerxes ?

-

Yes, @dwy000, Here is a link to the Norwegian Wikipedia website about a SWF, here translated to english : Norwegian Wikipedia : State investment fund.