John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

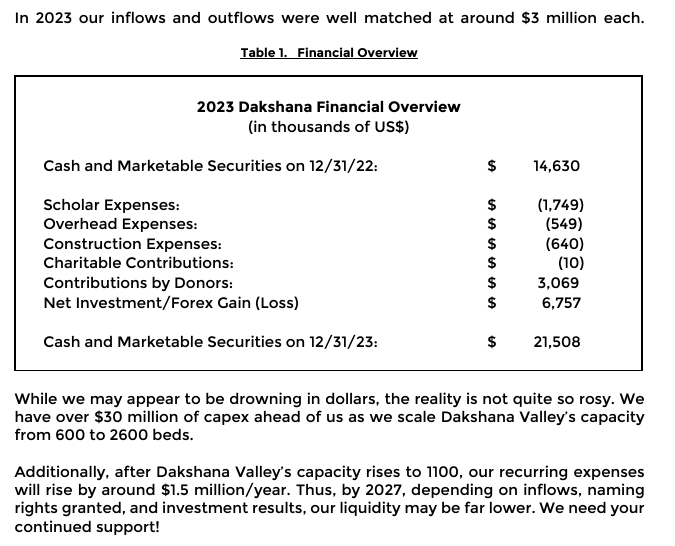

Well, here is what Monish himself as founder and chairman has to say about it [2023 Annual Report, p.4] : So the business plans and the strategy for the foundation is growth, based on clear formulated and stated ambitions, and every dollar is welcome. We all have our personal perceptions, preferences and personal frameworks for how to prioritize and allocate donations, if to donate anything at all. It certainly has a lot to do with personal perception of own financial position, too.

-

The most fascinating aspect of this fact, here posted by James [ @james22 ] above, is that it's totally up to yourself what you get in return of your one-time CofB&F subscription fee, by board participation!

-

@Eng12345, I'm happy here to contribute to moving your view and perception of the world, the reality and the truth, - and the 'absoluteness' of them all three. Rest assured, you're not the only one, nor were you in the past. - - - o 0 o - - - It must have been at the end of 2016 or 2017, I think, and I read here on CofB&F what I today would call a 'crash course' on 'Time Weighted Return', presented by @SharperDingaan here on CofB&F. In a way, my world view and absolute perception of things 'collapsed' / ''crashed' by reading that post here on CofB&F, before that, nobody would be able to tell me anything about measuring returns! - 'Naturally', I 'knew already what was to know' about that matter! - Not! Why was I not taught TWR in Finance classes as a concept back then by my professor? [That would be - likely '79 or '80 - I don't exacly remember anymore]. - - - o 0 o - - - Last year, in November, I got an invite to the 50 years anniversary celebration of my alma mater, despite personal sad condition, decided to go along with the Lady of House [It's also her Alma Mater]. Met then among a lot of other interesting persons my former professor teaching me finance. It turned out, he had spend - after I left - some years in education and research, and then left those fields, to join university management! - and did retire from that, not so long ago. Under our conversation, he asked me : 'John, what are you doing nowadays?' [Please remember here, I was a student under him]. Normally, when people ask me this question, the answer is by now: 'Nothing'. Here, my answer was : 'I'm full time engaged in showing that Eugene Fama is wrong!' He was absolutely baffled by my answer, and did not get his act together to ask supplementary questions. I suspect he stlll doesn't understand my answer. - - - o 0 o - - - Juts thinking about this episode can still cause me to crack up!

@Eng12345, I'm happy here to contribute to moving your view and perception of the world, the reality and the truth, - and the 'absoluteness' of them all three. Rest assured, you're not the only one, nor were you in the past. - - - o 0 o - - - It must have been at the end of 2016 or 2017, I think, and I read here on CofB&F what I today would call a 'crash course' on 'Time Weighted Return', presented by @SharperDingaan here on CofB&F. In a way, my world view and absolute perception of things 'collapsed' / ''crashed' by reading that post here on CofB&F, before that, nobody would be able to tell me anything about measuring returns! - 'Naturally', I 'knew already what was to know' about that matter! - Not! Why was I not taught TWR in Finance classes as a concept back then by my professor? [That would be - likely '79 or '80 - I don't exacly remember anymore]. - - - o 0 o - - - Last year, in November, I got an invite to the 50 years anniversary celebration of my alma mater, despite personal sad condition, decided to go along with the Lady of House [It's also her Alma Mater]. Met then among a lot of other interesting persons my former professor teaching me finance. It turned out, he had spend - after I left - some years in education and research, and then left those fields, to join university management! - and did retire from that, not so long ago. Under our conversation, he asked me : 'John, what are you doing nowadays?' [Please remember here, I was a student under him]. Normally, when people ask me this question, the answer is by now: 'Nothing'. Here, my answer was : 'I'm full time engaged in showing that Eugene Fama is wrong!' He was absolutely baffled by my answer, and did not get his act together to ask supplementary questions. I suspect he stlll doesn't understand my answer. - - - o 0 o - - - Juts thinking about this episode can still cause me to crack up! -

It's to me personally sincere and honest talk from your side, @Rod. I think I understand it better now, after reading the shades you have added. Thanks, & peace.

-

CofB&F getting better and better!

-

@thowed, Thank you for posting, Taken at par here. [My thought here is : What the h**k is he doing here, out in the 27th potato row, with this?]

-

I personally really dislike this approach to any person, @Rod. It opens basically up for 'accusing' about any person of having whatever personal egoistic motives, second thoughts, inferior incentives, for that person doing something good for other human beings. You naturally can try to prove your point by specific example[s]. Please post that [or them] here.

-

Yeah, exactly this what @Spekulatius expressed here was the intention with my post. The sharing of what I personally thought was a nice little story, bringing up some shades and nuances to Monish Pabrais personality made visible by the story it self, instead of the monotone and stereotype expressions almost always expressed about him here on CofB&F. To me, naturally OK bringing up Cialdinis concepts here though. As mentioned above by @Vish_ram, being a money manager is a craft, here meaning why shoulden't such a business not pratice marketing activities. I personally don't need Monish Pabrais services, or for that sake any money managers services, I personally enjoy immensely being a DIY person in that respect [money management], and spend on ongoing basis a lot of time doing it, likely, like most other CofB&F members enjoy and love doing this stuff. This comment from Sanjeev [ @Parsad ] really caused a huge smile in my face! - - - o 0 o - - - Edit : Ohh, I forgot : I had actually had to pay to receive this present from Monish Pabrai! - But that part of the story I won't tell here, because it is just perfect to stir the pot over in the topic about 'Is Europe becoming uninvestable'!

-

Wikipedia : Time Weighted Return.

-

Ha, Ha! - Priceless!

-

-

It's actually a very good question, Blake [ @Blake Hampton ], Joel Stevens - Austin Value Capital [January 5th 2017] : Essay : Measuring Returns. Joel Stevens is our fellow CofB&F member @racemize. Edit : Off topic : Austin Value Capital : Misc. Writings [May be worth your time, if you haven't visited the website before.], Austin Value Capital : Misc. Resources [Ditto].

-

Thank you, @klipbaai, Exactly that experience, hopefully, for everyone reading here, was my purpose for posting about it here on CofB&F. There is nothing in life like getting surprised, in a positive way!, and sharing it! - - - o 0 o - - - Mr. Pabrais modus operandi as a money manager, feel free to include his public [promotional <- [?]] appearance in several media, is still, at least to me personally, a totally different and separate matter. - - - o 0 o - - - In post above of mine, I also forgot to mention, that I have send an e-mail to Mr. Pabrai, thanking him for the present.

-

@Milu, A quick and cursory view on your post, and I was thinking : 'That CAGR calculation here isen't right', untill noticing the '-' in front of the 2022 number! What happened to your portfolio in 2022, and thereby to you? [As far as I remember, I was personally up ~2 % in 2022 ...]

-

It's awesome!, @Xerxes, Enjoy the rest of the holidays and your travel. We'll soon enough experience what 2025 has in the bag to us all.

-

@Dalal.Holdings, Charlie [ @dealraker ] & @Gamecock-YT, Yes, But whatever it is, I'm not a friend of Monish Pabrai. I have never personally in any way interacted with him before. I have never reached out to him, and did not expect him to react towards me, based on my actions. What life so far has taught me is always to meet new persons in ones sphere, physical or digital, whatever, - always a priori in an openminded, positive and forthcoming way, subject to the least personal bias and prejudice possible for my part. So consider the post above of mine a confession of my now former personal bias, negative bias towards Mr. Pabrai personally, for my part, that I personally - perhaps unjustly and without real and rational reason in the context - have adopted by reading CofB&F over the years, which led to a positive surprise for me, and a reassessment. It is basically about the concept of appreciation - and how and when to show and signal it, and how that is managed at Dakshana Foundation, I'm sure based on policy setting by Mr. Pabrai. Let me just say, that what I did donate to Dakshana Foundation this year has been unaffected by this present, and that I already did own a copy of the book. I'll keep the gifted copy, and then give my mint and already owned copy of the book to F. [Who is F? - Maybe later, maybe not.] - Presents generating new presents is great!

-

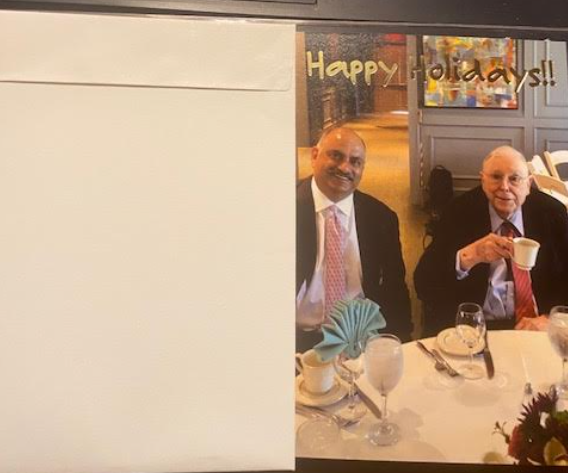

I have been searching CofB&F meticulously before posting this, to find the most appropriate topic - by topic title - to post what's on my mind here. We actually have quite a lot of topics related to Mr. Pabrai here on CofB&F, based on what he is doing, and what he is engaging in. Monish Pabrai has over the years been considered a quite controversial person here on CofB&F, based on his investment actions in Pabrai Investment Funds, combined with his promotional actions, related to his business, craft, trade. From reading CofB&F over now many years, I've understood, that Mr. Pabrai is also a friend of Sanjeev [ @Parsad ]. - - - o 0 o - - - Last year, in December, I donated absolutely pocket money to Dakshana Foundation, after which a secretary at Dakshana contacted me for information of my shirt size, to send me a T-shirt, based on that Mr. Pabrai has asked to do so. I refused, because it made no economic sense related to the purpose - helping talented indian young people from families with no or moderate means, to get good and relavant basic education, to provide for future upwards social mobility, by creating possibilities for entrance to higher Western education. - - - o 0 o - - - On 3rd December 18:55 I suddenly got a pop-up from my PostNord app in my iPhone, that a package was registered to be send to me, from Monish Paprai, Pabrai Investment Funds! I was absolutely puzzled! - I was soo nosy! - More and more nosy as the package gradually moved closer and closer to me, with tracking notifications in the app by each time it moved! -At 19th December I received notification that the package was delivered here, at home. No package anywhere to find! - I filed a report of a missing package the same day, totally upset! - Next day, in the morning, the package landed in our mailbox. It was a book : Pulak Prasad :"'What I learned about investing from Darwin", and a nice Holidays Greetings card, and the book with inserted compliments of Monish Pabrai! - I was in a really good mood the rest of the day, because of that! - - - o 0 o - - - In Danish, we have a saying : 'Skindet bedrager' [translated to English : 'The skin deceives'][, which is not meant as a racist expression, or something like that]. I think it means 'Be careful about assessing or judging other persons cursory, or perhaps based on second hand opinions, assessments and judgements, it may be a totally different experience to interact with the person directly, and also dependent on the actual context! I'm personally here not the least in doubt, that the present here, in my personal context, has been meant as a sincere token of appreciation of what I did last year! -And that matters a lot to me personally!

-

About 25 hours after launch, the curve distribution is already there!, I wonder how much it may change in the coming days?

-

It's actually an amazing interview with Alice Weidel. She is so clear cut, outspoken, honest and direct. That's not well seen and well received in politics [, which is 'bla, bla, bla - wool in mouth, say nothing]. In AfD the A is an abbreviation af 'Alternative', so it represents an opposition to the exististing 'old' German polical establishment. A political trend also seen other places in Europe, among them here in Denmark. Personally I won't consider her point of views and stances far right after Danish yardstick.

-

I have to say that KAL nailed it with his last cartoon December 19th - It really cracked me up :

-

That reads devilishly hellbent, @Paarslaars !

-

Tell me about it!, @Paarslaars! - My stuff has been like a flattening tyre here in December!, after keeping up pretty well during the first 11 months. - Ohh, welll! [<- At least we have some direction indicative smileys available here on COFB&F!]

-

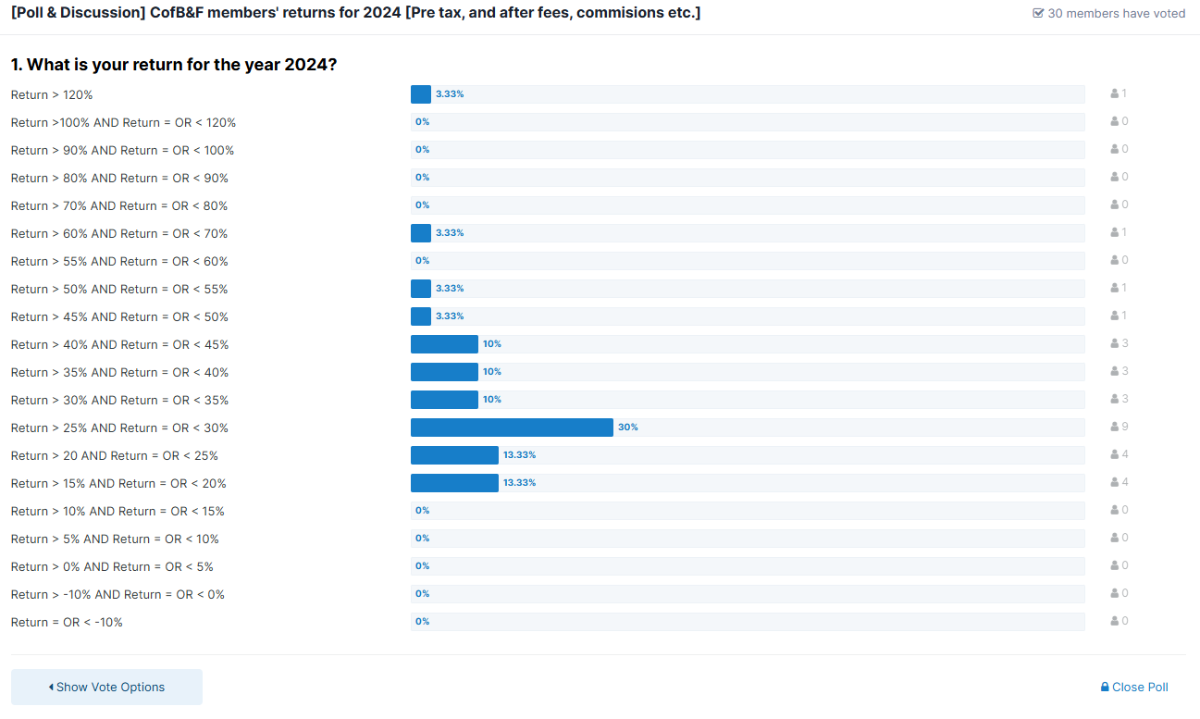

It's this time of year! -Let the show & show-off begin! - - - o 0 o - - - I've chosen a span in the poll options of 130%, materially diffferent compared to earlier years on the prior software platform for CofB&F [Simple Machines Forum], and perhaps not so fine meshed as I and perhaps others would wish, compared to earlier years' polls. It's has been a judgement call how to set it up, because of technical limitations of the number of poll options on the Envision software platform to 20. - If you may be "outside the ballpark" in the poll -, I sincerely hope it's in the positive end! - - - o 0 o - - - Markets are now about starting to close for the year, gradually around on our planet, from this afternoon in Europe, and tomorrow USA and Canada will follow suit ... The poll is set up as anonymous, meaning voter names aren't public. The poll is set up without any closing date. Also the poll is set up as non-multiple choice, meaning you can only vote on one poll option. - - - o 0 o - - - Please take the poll when you have your numbers ready! -And please also feel free to post what ever you may want to share of comments about your results for 2024, that you se fit and what's on your mind about the matter, perhaps also your comments about the precision in calculations as basis for your vote etc., if any, because it is your personal decision how to do it.

-

I Need a Laugh. Tell me a Joke. Keep em PC.

John Hjorth replied to doughishere's topic in General Discussion

Perhaps not as good as the jokes posted above, but still : Nordnet Danmark [Danish branch of Nordnet Bank AB, Sweden][December 23 2024] : Nordnet - Make investing in stocks and funds more fun I have seen this commercial on Danish TV, too. - - - o 0 o - - - To me, it looks like a Christmas shopping spree! And please look carefully at the box colour - Isen't that the - now - dropped and abolished [bold move by LVMH, btw.] - 'Tiffany teal' colour? -No price increases, please!