Spekulatius

-

Posts

19,046 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

Where Does the Global Economy Go From Here?

Spekulatius replied to Viking's topic in General Discussion

Found this on Reddit. Seems like this report is implying a 3-4% GDP growth headwind from real estate alone. If so, China will show barely any GDP growth this year. https://www.yielddive.com/post/what-s-going-on-in-the-chinese-realestate-market -

Windfall taxes on energy production make no sense. I agree Biden should encourage more production, especially much needed NG. It is odd that the only government that has instituted a Windfall tax, is the conservative UK government under Boris Johnson. https://www.cnbc.com/2022/05/26/cost-of-living-crisis-uk-slaps-windfall-tax-on-oil-and-gas-giants.html

-

It's not a recession until $GS shares are below tangible book.

-

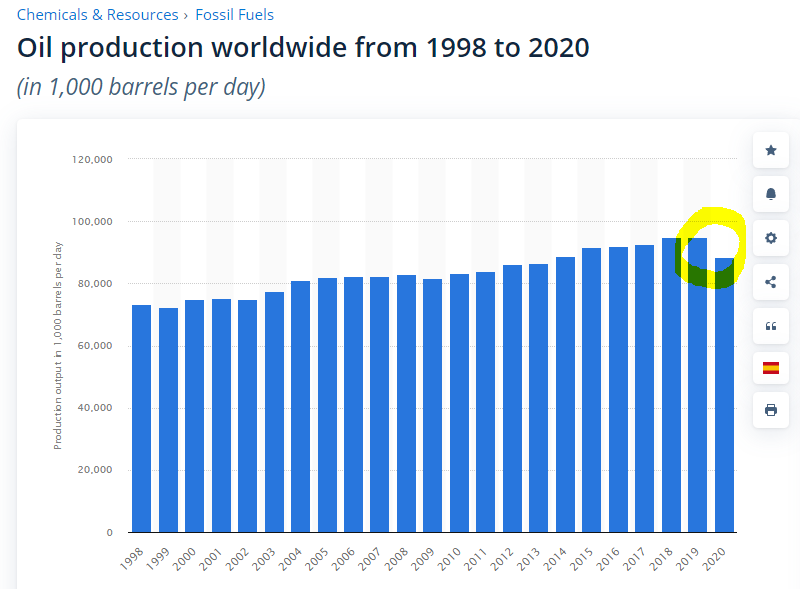

@CorpRaider All the factors you mention could matter at the margin, but I don't think they are the red X, as we used to say when trying to do root cause analysis. I think the red X is that we have seen extraordinary supply reduction in 2020 (production down 7%) and now finding it hard to get the production back. In the meantime, demand keeps rising after falling off the cliff in 2020 and then swiftly coming back. A production cut of 7% has never happened before and now we are dealing with the consequences. the OPEC has raised quotas but they can't meet them (in the past they have often produced more than official quotas). Russia is partly of the map (they funnel their crude through India and China at a discount, but their production is falling due to sanctions). I think the gap will eventually close, but it could take years - in the mean time we just will have rationing via higher prices, which I expect to affect emerging market economies the most.

-

Yes that's possible, but most other countries don't have the same ESG constraints that the US or Europe has. US is only ~10% of the total supply which matters, but it isn't really determining the outcome here. The oil majors also become more tilted towards ESG, so that could matter as well, but then there is always green washing. I think the bigger impact may be that interest rates rise overall. Edit - I looked up the cost of debt for Shell, which is a very typical Major and they only pay 4.4%, if this website is correct. This is very low - i don't see a problem here: https://valueinvesting.io/RDSA.AS/valuation/wacc

-

Well, in the long run, your return will match the return on equity, which I don't think will every be that great with Jungfraubahn. This is a stay rich stock, not a get rich stock.

-

Just because there are fewer projects in the US does not mean spot price goes higher in a world wide market. Also, aren’t all the operators swimming in cash now? Why do they need lending?

-

How so? Crude is still a world wide market with prices set at the margin. NG is still somewhat geographically bound because export via LNG is expensive and limited by infrastructure. For crude oil, that’s not the case.

-

DPW (DHL essentially) is a very cheap and well managed international logistics company. German government is not relevant here. Dividends and share buybacks provide a nice capital return.

-

Added to DPW.DE / DPSGY yesterday.

-

Nestle - multiple is too high and high EM exposure are my concerns. EM exposure will cause weakness due to currency issue and high energy prices reducing growth. i don't think it's safe pick here. I owned this in the past for many many years, but multiples were way lower back then.

-

Demand destruction for energy will occur in emerging markets first. People living there have much less disposable income. Also, the US is somewhat insulated due to the strong USD, if you add weak EM currencies to the mix, the increase in energy prices quoted in USD become even more painful.

-

SPGI withdrawing guidance, due to "extraordinary weak macro" - which for them means weak debt issues: https://finance.yahoo.com/news/p-global-suspends-2022-financial-104500674.html This likely affects MCO as well and to some extend investment banks.

-

I think there is a chance that the auto industry become structurally better (more profitable). Reasons are EV transition, higher tech content and higher service revenues from going closer to consumers as well as offering more services. I think the EV transition could affect the business either way and make the business worse (at least in the interim) so I don’t know. I do think that the automobile business is likely fundamentally changing.

-

Establishing a position in illiquid securities

Spekulatius replied to jfan's topic in General Discussion

if you don't want to move the market, you need to wait until the market moves to you. You often get more liquidity before and especially after earnings. It also can help to put a large bid out there at a price you like to own it. Someone who likes to sell might see the bid and just fill it. Patience is definitely required - you can't force it. -

@Longnose The BHC /BLCO spinoff is an interesting one. BHC seems to be the badco and has way to high leverage, imo. Goodco BLCO looks more interesting - 350M shares, $2.2B debt and ~$3.5B in revenues. Earnings power seems a bit uncertain. I think BLCO is the one to bet on, but from my experience, it is best to let these spinoffs marinate a bit before buying them.

-

Movies and TV shows (general recommendation thread)

Spekulatius replied to Liberty's topic in General Discussion

"Dark Waters" is streaming on Peacock. Found it pretty good. Watches thee first few episodes of "Stranger Things" on Netflix. New Season out for "Russian Doll". loved the first two episodes. Trippy. "Shining Girls" on Apple TV get's better with each episode. What a time to be alive for couch potatoes. -

This podcast is pretty good on the Fed /interest rates and the impact on the economy: https://podcasts.apple.com/us/podcast/odd-lots/id1056200096?i=1000563964446 In addition, Aswath Damodaran’s recent presentations on YouTube regarding inflation and impact on equity valuations (discount rates ) are also very good. FWIW, when you listen to the odd lots podcast , the guests opinion is that the Fed has implicitly removed the Fed put, meaning that the Fed may ignore stocks going down for the time being, and just limit themselves to looking out for orderly credit markets.

-

It’s not the inflation that is impacting equity valautions, it’s the interest rate to fight it. Letting inflation run to 8% at zero interest rates is very bullish for stocks, reducing inflation to 3% with 5% interest rates not so much. But I agree there are many secondary effects like that inflation boost growth rates for certain business, (but not for others) and tightening interest rates slows down the economy which causes the growth rates to fall or even reverse. I do think that if you look at all countries with high inflation rates that eventually interest rates go up too Turkey is an exception and they ruined their currency. Alternatively, look at periods where interest rates were higher in Europe or the US you will find that equity valuations were lower. So, empirically this rule holds up. FWIW, in the end inflation means that demand is out of whack with supply. The Fed cannot increase supply but it can reduce demand via higher interest rates, which are going to slow down the economy. The Fed basically signaled to us that it is willing to accept a light recession (soft landing) in exchange for lower inflation. That may not be such a big deal, because we had already 1.5% GDP growth adjusted for inflation in the first quarter, so with another quarter at the same level, we would technically have a recession already.

-

Location is everything.

-

I don’t think that 8% inflation will stick around, but even if inflation only goes back to 5%, it would be pretty bad though. 5% ongoing inflation would require many interest rate rises to counter. Look at it this way, valuation today is 5% equity risk premium and 3% risk free interest rate implying a 8% LT return. If inflation sticks around 5%, the no way the LT bonds stays at 3%, they will have to go to 5% at least. That means that assuming the 5% risk premium stays the same, the stock market will be valued for a 10% return, implying a 10/8= 25% reduction in valuation. Then on top of that we have some economic impact on the rising interest rates likely causing a reduction in earnings At least that’s my talk on Aswath Damodarans valuation lessons.

-

Working from home this afternoon, so I got started with a Margarita early (based on input upthread). I did learn one thing when I went to the NH liquor store. Was looking for mid price Tequila and the Jose Cuervo Silver and Gold are not 100% Agave while the much less prominently displayed Jose Cuervo Traditionale that goes for about the same price is 100%. Went with the latter because I believe in the power of ingredients. Cheers.

-

bought the dip on $WDAY (starter)

-

I believe both are correct. On another topic - will the Fed ever undo printing? No, it won't because that literally would mean that the Fed would need to take $ out of peoples pocket. It's not going to happen, that's what inflation and taxes are for. Note that the recent surplus in the treasury account just did that. Those are due to tax payments for 2021 (I think) and that took money from peoples pockets into the treasury account. I know how it feels because the treasury got a big check from Spek's household as well, thanks to $LAACZ and a few transactions sales. This is actually deflationary and may have contributed to the equity market rout.

-

@SharperDingaan it's important to note that ESG is a three letter word and stands for Environment, Social and governance. Sounds like 90% of the mindshare is in the E, but social means treating Employees, customers, suppliers and doing good at the societal level and governance means that management is transparent and foremost treats shareholders right. The EV company that produces shoddy vehicles and has unsafe work practices, gets there raw materials from conflict areas, pollutes the environment there and has overpaid management and dilutes shareholders to no end should have a low ESG rating just to put out a fictional example.