Spekulatius

-

Posts

19,041 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

WFC is only cheaper than USB based on HoldCo cherry picked metrics P/ tangible book, which isn't even regulatory capital. Based on earnings power, USB is quite a bit cheaper. WFC is also still operating under the asset cap which has restrained it's growth, so i think on growth USB will beat WFC as well. I think @Dalal.Holdings is correct that these guys are hyena's that have dealt with bank carcasses before, but I have little doubt that USB needs to be valued as a going concern here and tangible book only matters as far as regulatory capital levels are concerned. If we are going to tangible book including AOCI, then BAC is undercapitalized too with only ~$80B in tangible capital for a $2T balance sheet banks. Then you can write the entire thesis with BAC instead of USB which i think wouldn't make much more sense either, imo.

WFC is only cheaper than USB based on HoldCo cherry picked metrics P/ tangible book, which isn't even regulatory capital. Based on earnings power, USB is quite a bit cheaper. WFC is also still operating under the asset cap which has restrained it's growth, so i think on growth USB will beat WFC as well. I think @Dalal.Holdings is correct that these guys are hyena's that have dealt with bank carcasses before, but I have little doubt that USB needs to be valued as a going concern here and tangible book only matters as far as regulatory capital levels are concerned. If we are going to tangible book including AOCI, then BAC is undercapitalized too with only ~$80B in tangible capital for a $2T balance sheet banks. Then you can write the entire thesis with BAC instead of USB which i think wouldn't make much more sense either, imo. -

The economic miracle in Korea started in the mod 60's really but the average grunts slaving away for minimum wages did see little of the wealth that was created. The wealth went to the chaebols Samsung, Hyundai, LG, Lotte who grew in leaps and bounds with exports, based on their cost advantage (low wages). It took until the late 70's until the wealth created started to benefit the average person. These Chaebols are in a way similar to the Oligarch in Russia but I think the chances that the average Russian sees benefit from the system eventually are slim to none.

-

I briefly went through this presentation and can point to a handful misrepresentations. For once, USB management stated that they are not buying back stock for the time being and rebuild the capital buffer above 9%. USB does very well in stress test results and has smallish CRE exposure. Now, if you criticize the stress test itself, you need to do this with for all banks. Also, USB's management isn't stupid. They are aware of the $700B threshold for systemically important banks and it seems likely they had discussions with the Fed prior to buying MUFG US business. They are currently also below the asset size threshold and are running off some MUFG assets fort rationalization purposes alone. Anyways, bought a few more shares today.

-

I am not implying that China Kai Shek was great, but we do have the natural experiments of Taiwan- China, South Korea- North Korea (and West Germany- East Germany ) showing us how good communism really worked. Now the CCP is evolving obviously after Mao but I think under Xinping, they are taking a huge step backwards, because after all, he is a Neo Maoist. Both Taiwan and South Korea were army backed regimes that turned democratic over time. I would even state that Ukraine - Russia is the same thing. Ukraine slowly tries to become more Democratic in fits and starts after the Maiden revolutions, while Russia tries really hard to stay an autocratic hellhole with Putin being a Neo czar role in the 21 century. In investment lingo, Taiwan, South Korea and Ukraine are spin-offs.

-

You are most likely correct. I would also point out that starting in early 2020 just when COVID-19 hit and all the operating ratios and loss ratios improving due to less driving, it would have been hard, if not impossible for a new CEO to figure out the the underlying issues before they clearly manifest themselves in the income statement. That said, the lack of progress since 2021 when the COVID-19 effects started to wear off is bit frustrating.

-

Seems to me that Todd Comps isn't the right CEO for Geico and they need to replace him with somebody else, who can figure this out. Todd started his CEO role in early 2020 (if I see this correctly) and it seems like things started to go downhill from there.

-

@throw123 Exors overhead costs are pretty low though, despite the helicoptering. Exor always will trade at a discount to BNAV, that's a feature, not a bug, imo. I would not add right now to my smallish position, but when the discount to NAV blows out, I certainly would buy more, which is the way those Holdco's should be traded or invested in. Right now, I consider it a solid hold. I never liked the foray into Insurance years ago (buying PRE) but they managed to get out with a decent exit. Now the big question what they do with the excess cash from the insurance sale proceeds?

-

Small add to MTB.

-

China without the CCP does exist, it’s called Taiwan. There is no reason to believe that China couldn't look like Taiwan’s economy if Mao had lost the civil war against Chiang Kai-shek.

-

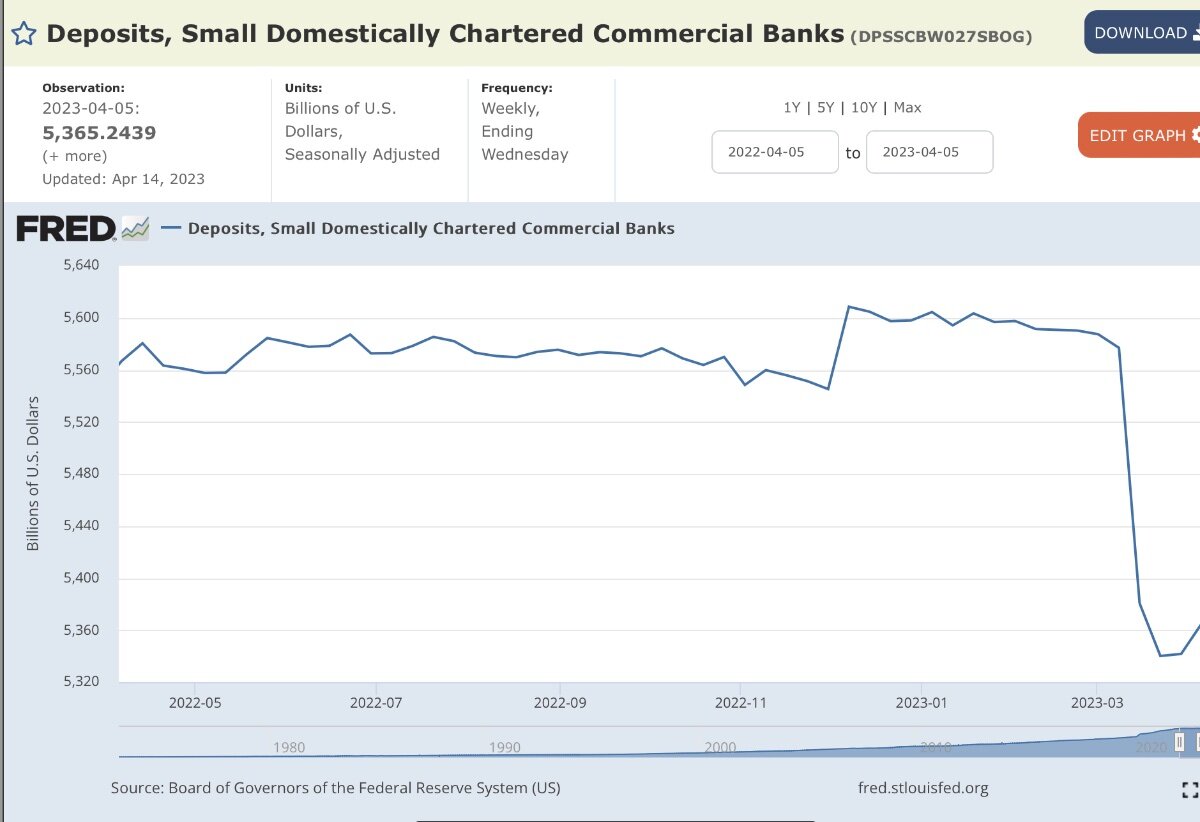

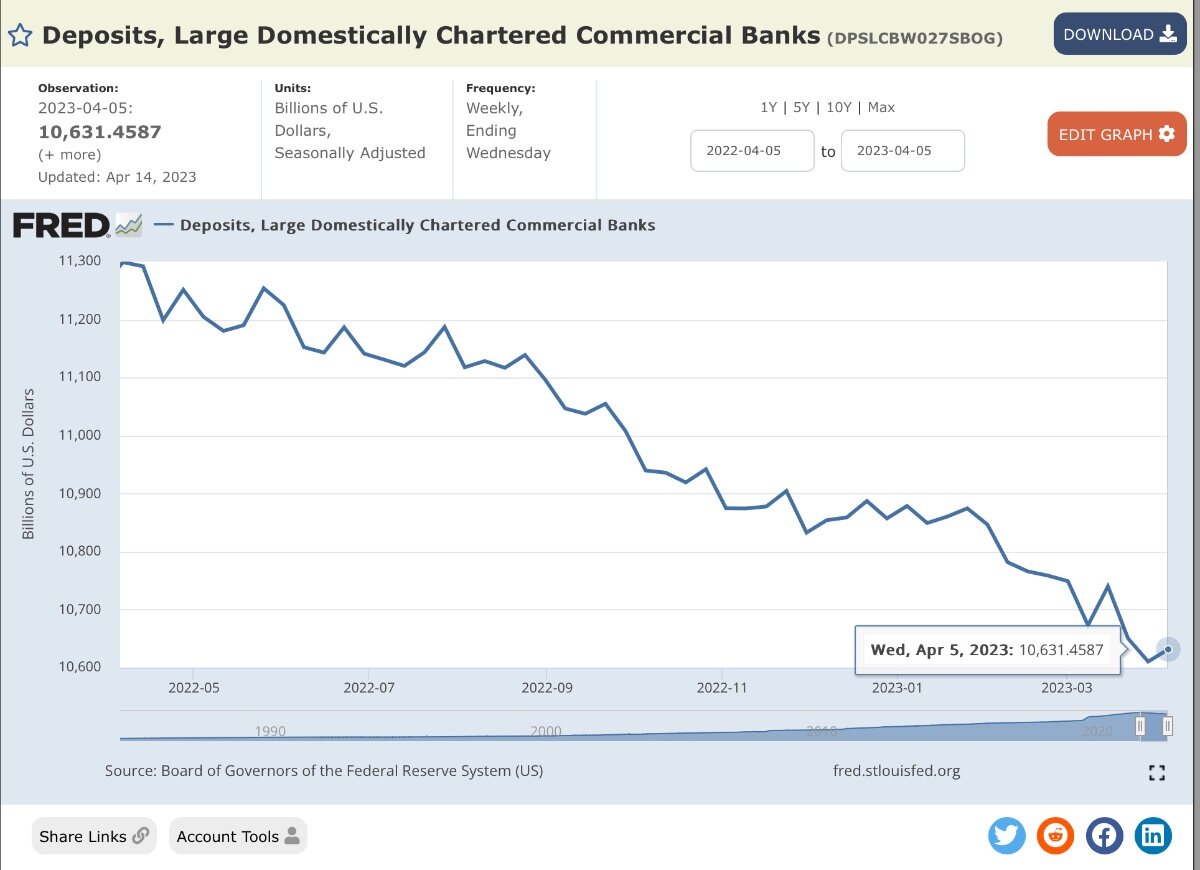

New depots number came out yesterday and indicate a stabilization both for small and large banks. I think it’s because the banks finally have started to raise their deposit interest rates. I think the Panik stage of this episode is over, at least for now, but banks will probably have more pressure on earnings (due to NIM compression) going forward. In the next few weeks, I think FRC will find a new owner. I look look forward to seeing BAC numbers which I think are a tad better than PNC’s but not as good than JPM , mostly because of drag from. They’re large fixed income positions. For all banks, the losses on securities should be smaller because the long duration interest rates came down.

-

I disagree on brilliant leadership. Xi is still a bonehead autocrat. Invest there at your own peril, especially if you are at the western side of the fence, it can end up bad very quickly.

-

I recall earnings estimates for $5 and $7 for 2023/2024 given in 2021. There was an expectation that AMZN earnings would “hockey stick” due to both AWS and retail pulling through. Currently we are looking at $1.4 this year and $2.5 next year as consensus earnings. FCF is currently negative. I think AMZN will be higher in 20 years, but I can easily see the stock being at current levels in 5 years and I think it needing 10 years to take out taking out the last high from 2021 is a possibility.

-

Buffett/Berkshire - general news

Spekulatius replied to fareastwarriors's topic in Berkshire Hathaway

Losses in HTM don’t have any regulatory capital impact for banks. That’s not because anything special was done by BAC, it’s because that’s how the regulator set the rules this way. (Losses in AFM only impact systemically important banks like VAC, JPM, C etc that are above ~$700B in size. For smaller banks, losses in AFS don’t have any regulatory capital impact either). I also think it’s correct that BAC has a $11.9B hedging loss not a gain. I guess they better on interest rates staying low. BAC isn’t as well managed than JPM, at least in terms of liability management that’s for sure. I think their earnings won’t look as good either, but we will see on 4/18 how it plays out. In my opinion, it is likely that Buffett kept VAC, it because it is necessarily better than other banks, he kept it simply because it is his largest position and selling it would have been difficult, so he just decided to do away with his smaller positions to reduce his sector exposure. -

Bought some PNC today Post earnings. I quite liked the results and felt they were solid. I don’t quite get the market reaction. It is however clear that regional bank stocks are around peak profitability and at least for PNC, further interest rate rises will lead to lower NIM (due to yield curve inversion getting steeper), but I think PNC handles this quite well. Then we also are going to look at higher reserves going forward https://d1io3yog0oux5.cloudfront.net/_b0f9c850082c0d672a791c9596a58778/pnc/db/2250/21438/presentation/PNC_1Q23_ER_Presentation.pdf What I liked: 1) Expense control and headline earnings 2) Higher tangible book (expected) 3) relatively strong no interest rate income 4) detailed information about CRE exposure, deposits, NIM sensitivity What I didn’t like 1) little buybacks 2) lower NIM and earnings going forward I think PNC is a solid buy here. It is not the cheapest regional bank stock out there, but I think it behoves investors well to not do dumpster diving here. I don’t consider myself a bank analyst, but can’t really find anything that I grossly disliked looking at their 10-k and press releases or CC transcript either.

-

Noticeable absent is the question - does it make money or FCF (if it works)? Amazon has been willing in invest large amount of money into business where profitability (or even FCF) seems elusive. They have been kicking the profitability can down the road for a while. Now with AMZN being a ~$1T market cap company, that question of sustained profitability becomes ever more important.

-

I actually think that most people here, even those that are in opposing camps, would make the same decision if it pertains to sex change of their underage kid and similar cases. Personally, I would not allow it (had a discussion with our son about that) for the simple reason that teenagers tend to change their mind quite often. Once they are at age, they should be able to do whatever they want and of course have to live with their decision.

-

Can we put this transgender nonsense to rest? It has nothing to do with NYC whether you live or stay @Parsad

-

Nobody knows anything. Everyone just makes it up as they go along and that's about the only realistic way to be approximately correct and precisely wrong.

-

Bought some $PNC. I felt like the results were solid.

-

I wonder of the best way to play commercial RE are the brokers and leasing service providers like JLL, CBRE and maybe lower quality CWK. I also looked at NMRK but can's live with their shady (imo) accounting adjustments. JLL looked pretty cheap but CBRE seems to be the highest quality. With those service providers, you don't need to bet on a certain class of RE and even if office goes down the tubes, they will eventually have to figure out what to do with all these buildings at which point these brokers will get involved. Does anyone have an opinion on these RE brokers ?

-

It's for both, the condenser and the coil at the heating unit (which seems to be leaking water or there is an issue with the pan holding the condensed water). I think one issue that there has been some code change pertaining to the vent duct work that needs to be replaced (PVC not allowed any more) even though that particular quote is fuzzy on this matter. This might explain some of the jump in price from 2022 to 2023.

-

OT - On the matter of inflation, here is one datapoint regarding HVAC (replacement of an existing condenser with a new one) 16 SEER rating 3 ton unit. 2020 quote -$4560 2022 quote - $5552 2023 quote - $8296 Again same contractor, same exact unit, same scope of work. I am aghast about the 2023 quote and hence got quotes from different contractors, but the price is in a similar ballpark (I can get it a few hundred $ cheaper around $8k). Hitting myself now for not replacing it in 2020 when it had a minor issue (rotor). Now the unit went (is loosing refrigerant and leaking water in the water exchanger, so it has do be done. Probably should have bought CARR and WSO....

-

A German minister on DW/ TV poured cold water over that one and stated that Macron's diplomatic adventure was not sanctioned by Germany or the rest of the EU for that matter. He has embarrassed himself.

-

I use Capedge for alerts. It is free. Other than that, I use various watchlists in brokerage accounts, Tikr (paid) and yahoo finance.

-

The acute phase of the energy crisis is over, but there still is a chronic phase. The biggest issue I am seeing is with the French nuclear generation fleet - it has been operating at only 50% of capacity at time, straining the European power grid. The French nuclear generation fleet is aging and needs lots of preventive maintenance in the short term and replacement investment in the long term to keep it going. France also underinvested in wind energy, they could do more on that end.