Leaderboard

Popular Content

Showing content with the highest reputation since 04/06/2024 in all areas

-

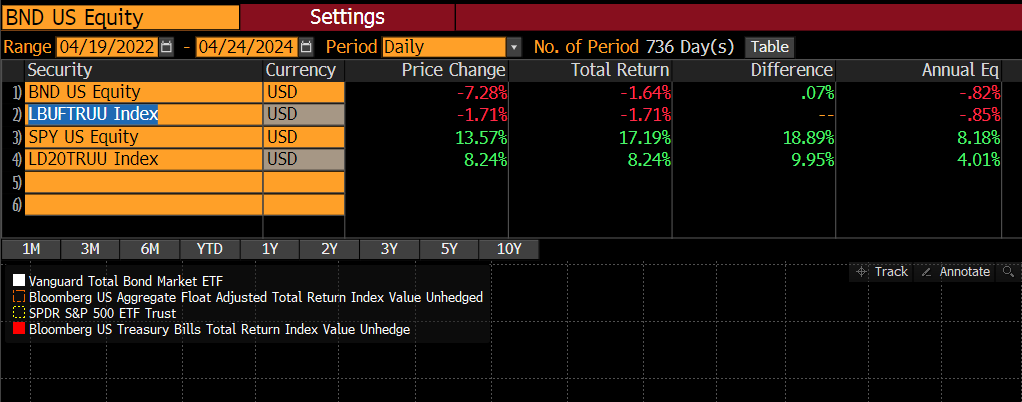

2 years later after start of thread and bonds have underperformed t-bills by 4%/yr and SPY by 8%/yr as the index's yield has increased from 3.5% to 5.25% (actually yields more since that's YTW and MBS will yield more than their YTW) I'm continuing to plow the entirety of my 401k into bonds and have recently started to buy long term tsy's on margin in my taxable (having sold most of my IG corporates after the late 2023 rally). credit risk free MBS >6%, LT tsy's approaching 5%. good stuff. I'm a buyer. no corporates. IG spreads way too low in my opinion. not for everyone but if you buy say 30% in LT tsy's at 4.8% on margin at interactive brokers, at top federal tax rate, you're making 3% after tax yield, fund w/ 6.2% margin and you have negative carry of 3% on 30% of your portfolio. At constant yields you lose 90 bps/yr on the portfolio. But in a recession where rates drop just 1%, you get 30% of your portfolio going up 20%, 2% =42% for 600 - 1200 bps of PnL when you want it most from liquid monetizable instrument. if rates go up another % you lose 15% on your 30% / -450 bps. almost no mgn requirement. JPow is making bonds great again.

1 point

1 point -

Trying to be "conservative" is a mistake. You should try to be accurate. How many great and very reasonably priced companies have value investors missed because they were too "conservative". I agree with Gregmal, you should be looking out at least 3-5 years. Trailing earnings are already priced into the stock. Forward earnings are usually too (though Meta is an example of "conservative" investors missing forward earnings by a mile). If you look at only forward earnings, every great company will look expensive. If you use trailing earnings, every value trap will look cheap. Nvidia is a great cautionary tale. In January 2022, TTM (2022) was $4.44. actual fwd (2023) was $3.34. You could have been conservative and estimated 2024 earnings at $3 or $4 or $5. But actual 2024 earnings were $12.96. Sure, you might have missed the drawdown from $300 to $100. But you would also miss the run from $100 to $900. Conservatism comes at a price. --- This also depends on your strategy. If you are buying a cyclical, you should be looking at the past 10-20 years. And then maybe overlay some thoughts on forward earnings. For a real growth stock, you should be looking out 5-10 years.1 point

-

There was no explicit mention of IDBI but it was alluded to that the decision would be post India election (early June). Generally I got the sense that activity will pick up across the board in India once the election is over. Also, I was the “someone else” who had the opportunity to sit on the panel with Viking at the dinner. I hope I made sense even if I wasn’t memorable!1 point

-

The hard reality is that Israel f****d up badly when they struck the Iranian consulate in Damascus; senior officials rolled the dice, and almost pulled the US and UK into Gulf War III. There are a lot of bills to pay for last nights bail-out, and there will be consequences. The only reason we don't have Gulf War III this morning is because Iran also has very smart generals, who managed to launch a face-saving sovereign-on-sovereign strike that was designed to reliably fail. Now it's purely a personal matter between families; the perpetrators will be known, and its old world 'eye-for-an-eye'. One day ... they will be suddenly gone, the matter closed, and we will all be the safer for it. https://www.aljazeera.com/news/2024/4/4/why-does-israel-keep-launching-attacks-in-syria Lot of very smart people acted last night; we owe them all an enormous favour. SD1 point

-

Wow much kudos to Israel….best I can tell from reports their missile defense systems pretty much bested these attacks . It’s embarrassing for Iran how little by way of damage they were able to inflict here…..and quite foolish in a way to reveal how weak they are relative to Israel’s military capability….hopefully this reality seeps through to the Iranian people so that they might constrain their leaders….it would be insane for that countries leadership to pursue a straight out conflict with Israel….but these sectarian regimes don’t live in anything approximating the real world…they hear god whispering in their ear.1 point

-

Who in their right mind doesn't see that 100 today is not 100 in 50 years. The 100 year Austrian bond was the height of lunacy as if Austria will be a Sovern nation in 100 years anyway? People who lend, banks ect are playing a different game with different ideas. Buffett buys treasuries to earn a bit while waiting for something real to come by like a railroad. He doesn't do it to make 1-5% Lending money long term is tough to understand unless the rates far exceed the level of inflation. In the 70's a big mac was less than 50 cents, today its 10x that or more. Our paper/ digit money looses value every day and has for a long time. Gold was 154 in 1974 today its 2400. Gold is money, paper or digits is just for transactions. Does it matter what the transaction number is? 10-100-1000 its just a digit. Will my house cost 18 million Canadian in 50 years, maybe maybe not who cares as long as its roughly the same value as today. I bet it will, gas will be 12 bucks a L, gold 25k OZ. all just a number. What we should care about is life expectancy, number of people starving, happiness, wars, have the leaf's won the cup ect1 point

-

Parsad, thanks for the notes on the AGM. I was there this year, nice to see/meet so many of the managers of FFH companies and managers of some of the larger investees. 2 things really jumped out at me this year. Firstly, more discussion on buying better businesses and letting compounding work its magic ( a la, BRK). Second, I think I heard Prem correctly, when he said they only need a 5% return on the investment portfolio to achieve their 15% growth in BV hurdle. The 30 year return has been 7.7%CAGR. It reinforces how they just need to keep hitting singles and doubles for this to be a REALLY good investment over time. A few home-runs will just be icing on the cake. The discussion on owning financials (and the 2.5x multiplier effect) in a growing economy was very interesting as well. Hard not to get excited about India for the next couple decades.1 point

-

What stood out to me: Their expertise in India and how well the bial team is executing Buffett and Jain tried to set up an insurance operation in India and gave up. I am sure they tried to invest there and found out it was too difficult. This is of course from 2010, before Modi. I would say that Watsa has been highly successful instead and it does get enough credit for this. He saw the opportunity and positioned fairfax to succeed. Bial becoming a hub for airlines in the south of India is a great accomplishment Sokol made me jump from my chair: I was not expecting that kind of growth from Atlas "we don't forecast, we react and we are fast": great line and great example with the $1B issuance not being possible today The fact that FFH might be less dependent on investment gains going forward and their improved ability to absorb cat losses: I liked that whole segment. I don't think we are there already but it is a promising start especially if they tilt their investment strategy in that direction G1 point

-

I have to say, we're 3.5 hours in and this AGM has been fantastic so far! One of the best ones I've seen...probably the most comparable to Berkshire AGM's. Prem was on it, looked great and you can see how deep the team is. If FFH has seen the light on their transformation...we may finally see the potential this company has! I've been a shareholder for 22 years...I'm more optimistic than ever! Cheers!1 point

-

Watsco !!! lol1 point

-

Depends on how short, but in general are a better inflation hedge than most other assets. The best immediate inflation hedge is oil. But oil is also exposed to idiosyncratic risks like cratering demand if the economy is also weakening (and politics!). So a basket that is heavily skewed to oil, some to gold, and some short-term fixed income should be a reasonably good hedge against inflation. Oil is immune to interest rates, but not immune to the economy. Gold/short term bonds are largely immune to the economy, but not real rates. As a basket, they should diversify the idiosyncratic risks of real rates, nominal rates, and the economy while hedging inflation. Future implications of deficit spending? More volatile inflation going forward.1 point

-

Here are my notes on the 2024 FIH agm that just finished: Something worth keeping in mind -> in 2023 they bought back 2.9M shares, the share price was up 24%; yet, $14.9 is exactly the same price at which they completed a SIB back in 2021. A lot has happened in 3 years... slide 28 is a nice summary of the impact of fees on returns BIAL will see "explosive" growth in the next years huge number of aircraft ordered by indian airlines (1200?) number of operating airports expected to roughly 2x to. 250 (?) Air India established its 2nd HUB in BIAL -> increase in international flights (EU/US) + other flights from other parts of India Watsa said that there are lots of structure that you can set up to raise money for big opportunities; seemed very confident that money will not be a problem for FIH Sold NSE because valuation was too high and they saw downside risk given that NSE makes a lot of profit from options trading IIFL gold loans issues -> founder said there were minor "lapses", IIFL was used to set an example for others. He said they addressed all the issues raised by RBI and hope that RBI audit will confirm this (April 12th start) no fraud, no money laundering Lots of emphasis on the financial sector opportunity -> 7% real growth, 12% nominal, financials should grow at 1.5-2x the nominal = 18% I am not sure I got this correctly but Watsa said something like "we are targeting 20% rate of return, not 10-15%, need to offset some fx risk" Sanmar had a terrible year with PVC prices down 30-60% improved efficiency in Egypt focus on specialty PVC growth ahead -> China has similar population to India and uses 20M tonnes per year vs India's 4M tonnes per year Maxop and Jaynix -> "unlimited growth", their only constraint is capacity and they are expanding, huge demand Anchorage still stuck in regulatory approval, nothing will move before the election (I would expect nothing before 2025) Privatization opportunities will unlock after the election all in all, great enthusiasm as always. focused on integrity. Deepak Parekh (founder of HDFC) is their consultant for everything and this is a HUGE plus in my view. Curious if any of the guys who attended in person were able to gain other insights. G1 point

-

https://east72.com.au/wp-content/uploads/2024/04/E72DT-Quarterly-Report-March-2024.pdf

1 point

-

Lmao this dude is a clown. Imagine shorting Microsoft or Amazon because its 18% overvalued based on what you think fair value should be. If I was an investor in his fund I'd be pulling capital right now because he obviously doesn't know how to manage money. Probably has a burner on r/WSB1 point

-

This was excellent @Luca - thanks1 point

-

I watched Dune 2 again. This time on IMAX. The theatre was packed. And i am sure they are mostly second or third viewings. speaking of which, this is funny.1 point

-

Thank you for the kind way to respond on my words, @Luca & @Cod Liver Oil, I may here on CoBF appear sober or chill most days I post, but what's going on inside my head can't be really be described by representing my mental state most days as I'm sober or chill most of the time. Simply because I'm not, while I'm forcing myself to stay about fully invested all time long term. However I think I'm gradually getting better at it. It's about a large position in that Danish pharma every media is writing about, here now at above 20 per cent of total portfolio, which for me personally not is easy to sit on. So I already really have my mouth, hands and mind full with risk, that I try to relate to on a continuing basis. Also, It has become clear to me, that I likely possess a personal propensity to underestimate political risk related to foreign investments, based on my experiences in 2020 with Russian stock investments [Gazprom, Lukoil & Sberbank], however losses not cribling, but not forgotten. - And as always I may change my mind any day. ... - - - o 0 o - - - So, good luck with China! [sincerely meant!]1 point

-

That is just wild! We should all start emailing him crazy conspiracy theories about what Prem is doing. I just heard that they're going to announce that they are short BTC at the annual meeting.1 point

-

If you're looking at me, you misunderstand. I am not suggesting they ignore these. But the list I responded to had nothing about value, so it does not in any way guarantee good returns (and 10% is a good return). Plus FFH are value investors - why hope they will become something they are not? If you're looking for that, look elsewhere, would be my advice.1 point

-

Lower interest rates must also be a factor in higher margins. And we haven't really seen the full impact of reversion of interest rates to more normal (if still quite low) levels because most companies were smart enough to pile on low cost long term debt during the pandemic before the rate hiking cycle began. Financial engineering has also been a factor in stock returns exceeding earnings returns as companies were able to borrow cheaply to fund stock buybacks and a shrinking share count supports higher prices and provides a constant bid for the underlying shares. And something else that has been helping margins is that companies have been able to use inflation as an excuse to increase prices by 50% from pre-pandemic levels and even though their input costs have now come down and they've been able to make cost savings by cutting staff numbers and limiting wage increases to well below the rate of inflation these haven't been passed on to consumers. A reflection of how concentrated most markets are these days. And of course there are composition changes. You'd expect S&P margins to be higher when tech has gone from 10-15% to 30-35% of the index and in this cycle there has also been a shift in investor preferences away from low margin value stocks and cyclicals and towards high margin if low growth consumer defensives.1 point