All Activity

- Past hour

-

Update - still textbook perfect bull flag

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

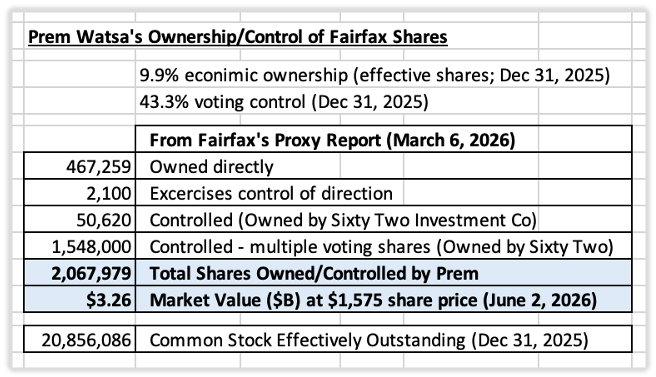

Article 2 in the series. Prem Watsa and Family Control Founder-led companies have historically been among the best long-term investments. When ownership, control, and management are concentrated in the hands of a capable founder, decisions are often made with a longer time horizon and a greater focus on value creation. Fairfax Financial is one such company. Prem Watsa founded Fairfax in 1985 and has led the company for nearly four decades. During that time, Fairfax has evolved from a small Canadian insurer into a global insurance, investment, and operating company with interests spanning dozens of countries and industries. For investors, understanding Prem's role is important because he remains Fairfax's largest individual shareholder, Chief Executive Officer, Chairman, and controlling voting shareholder. Fairfax's culture, capital allocation philosophy, and long-term orientation all reflect his influence. This article examines Prem's leadership record, ownership position, and family control structure—and what those factors mean for shareholders. Founder, Leader and Capital Allocator Prem Watsa founded Fairfax in 1985 and has led the company continuously ever since. Over that period, Fairfax's share price has compounded at approximately 19% annually, including dividends. This places Fairfax among the best long-term performing public companies in Canada and North America. But what makes Prem noteworthy is not simply what he achieved—it is how he achieved it. Warren Buffett has often said that he looks for three qualities in business leaders: Intelligence Initiative Integrity Of the three, Buffett considers integrity the most important because it forms the foundation of trust. Prem has demonstrated all three qualities throughout Fairfax's history. His intelligence is reflected in Fairfax's long-term record of capital allocation and value creation. His initiative is evident in the growth of Fairfax from a small Canadian insurer into a global organization. Most importantly, he has built a reputation for integrity that has earned the trust of shareholders, employees, customers, business partners, and communities. Two qualities have been especially important to Fairfax's success: temperament and an ability to attract talented people. Buffett has long argued that temperament is more important than intellect in investing. Throughout Fairfax's history, many of the company's most successful decisions required patience, conviction, and emotional discipline during periods of uncertainty. Throughout Fairfax's history, many of the company's most successful investments were made during periods of uncertainty and market stress. These decisions required patience, conviction, and emotional discipline. Prem has also demonstrated an uncommon ability to identify, recruit, develop, and retain talented managers. Fairfax's decentralized structure depends on capable leaders operating with significant autonomy. The depth and continuity of Fairfax's management team may ultimately prove to be one of Prem's most important accomplishments. As a result, Fairfax's success extends well beyond shareholder returns. Employees have built rewarding careers, customers have benefited from stable insurance partners, communities have received significant philanthropic support, and long-term shareholders have participated in one of the strongest compounding stories in modern Canadian business. Buffett on the importance of temperament – 1985 interview with Adam Smith: Adam Smith: What do you consider the most important quality for an investment manager? Warren Buffett: It's the temperament. You don't need tons of IQ in this business. I mean you have to have enough of IQ to get from here to downtown Omaha but you do not have to be able to play three-dimensional chess or being the top player in a bridge league. You need a stable personality and temperament that neither derives great pleasure from being with the crowd or against the crowd because this is not a business where you take polls; it's a business where you think. Ben Graham would say that you're not right or wrong because a thousand people agree with you and you're not right or wrong because a thousand people disagree with you. You're right because your facts and your reasoning are right. – Warren Buffett - Adam Smith’s Money World Interview 1985 Ownership, Compensation, and Alignment One of the most attractive features of Fairfax's governance structure is the alignment between management and shareholders. Prem's compensation package is unusually modest for a company of Fairfax's size and complexity. His annual salary is approximately C$600,000 and he receives no stock options or stock-based compensation. The more important consideration, however, is ownership. As of December 31, 2025, Prem owned or controlled approximately 2.1 million Fairfax shares, representing: 9.9% economic ownership 43.3% voting control At Fairfax's share price in mid-2026, that stake was worth more than $3 billion. As a result, the overwhelming majority of Prem's wealth remains tied to Fairfax's long-term success. Shareholders benefit from knowing that gains and losses are experienced alongside management. This alignment was demonstrated during the market turmoil of 2020. At a time when investor sentiment toward Fairfax was overwhelmingly negative, Prem personally purchased approximately US$150 million of Fairfax shares in the open market. He described Fairfax as trading at the largest discount to intrinsic value he had seen in the company's history. "At our AGM and on our first quarter earnings release call, I said that our shares are 'ridiculously cheap'. That statement reflected my recognition that in the 35 years since Fairfax began, I have never seen Fairfax shares sell at a bigger discount to their intrinsic value than they have recently. I have now backed up my strong words by purchasing close to US$150 million of Fairfax shares in the market over the last few days, as I believe that this will be an excellent long term investment." — Fairfax News Release, June 15, 2020 Actions often reveal more than words. Large insider purchases by already-wealthy founders are relatively uncommon and are generally viewed as one of the strongest indicators of management alignment. Family Control Fairfax is effectively a family-controlled company. While Prem owns ~10% of Fairfax's economic interest, his multiple-voting shares provide ~43% voting control. This gives the Watsa family substantial influence over Fairfax's strategic direction. For some investors, family control raises concerns. For others, it represents an important competitive advantage. The reality is that family-controlled structures can produce either excellent or poor outcomes depending on the quality of the controlling shareholder. When governance is strong, family control often promotes: Deep commitment to the business Long-term decision making Consistent capital allocation Preservation of corporate culture Stability during difficult periods Strong relationships with customers and employees Strong community focus and social purpose These characteristics can be especially valuable in insurance and investing, where the consequences of important decisions may take years to fully emerge. Fairfax's forty-year record suggests that family control has been a significant positive for shareholders. The structure has allowed management to think in decades rather than quarters, preserve Fairfax's culture, and maintain a consistent capital allocation philosophy through changing market environments. At the same time, investors should remain aware of the risks that accompany any founder-controlled organization. Potential concerns include succession planning, management entrenchment, and the possibility that future leaders may not possess the founder's abilities. No governance structure is perfect. Every structure involves trade-offs. What This Means for Shareholders Ownership structure matters because it influences incentives, decision making, and corporate culture. Fairfax remains a founder-led company with substantial insider ownership, significant voting control, and a leadership team whose financial interests are closely aligned with those of long-term shareholders. Prem's four-decade record of value creation, modest compensation, significant ownership position, and long-term orientation have all contributed to Fairfax's success. The historical evidence suggests that Fairfax's founder-led, family-controlled model has served shareholders exceptionally well. Fairfax's exceptional long-term performance, strong culture, and disciplined capital allocation are all closely tied to the leadership Prem has provided since 1985. The key question for investors is no longer whether this structure has worked under Prem Watsa. The historical record clearly answers that question. The more important question is whether Fairfax can preserve the culture, discipline, and capital allocation framework that Prem built once the next generation assumes greater responsibility. That question is examined later in this chapter when we turn to succession planning. Learn More About Prem Watsa Prem was inducted into the Canadian Business Hall of Fame in 2024. The six-minute biography prepared for his induction provides an excellent overview of his life, values, and the development of Fairfax. It is well worth watching for investors seeking a deeper understanding of the person who built Fairfax. To watch the 6-minute biography of Prem on YouTube, click the link below: - https://www.youtube.com/watch?v=SisxUC232t8

-

CME, ICE and TMXXF Thanks Lance

-

@changegonnacome, of course Israel by itself can wipe out Iran. Israel has nukes, and presumably chemical and biological weapons. Hell, Israel can just destroy Iran's oil industry and Iranian population starves to death.

-

I find the discipline of tracking long term performance AND writing an annual investment letter to myself extremely valuable. That annual discipline is even more important now that I can afford to be complacent with my portfolio.

-

I don't monitor CAGR or total return. But i once heard the phrase "money is a fickle mistress, if you don't pay attention to her she'll leave you." While the exact % return or CAGR isn't overly important to me. I dont feel like i could ever stop "paying attention" to where my money is at and what is it doing.

- Today

-

I have never really given this sort of thing any weight. It's basically marketing material for AUM eaters and something poor people do to give themselves "wins"/gamify a process that shouldn't be gamified. If Im OK with, and understand what I own...owning it is an active decision and playing the herky jerk game of buy/sell/buy/sell is just a distraction and waste of time. I always wondered, imagine where Musk/Bezos/Gates would be if they routinely did that sort of thing with their individual businesses and entities?

-

Thanks for answers so far, the main reason I still track is a want to see if my results over the long term have been better or worse than just dumping it all into S&P index fund. So far they have been better. But I suppose the question I’d have for myself is if they ended up being worse would i then decide to go the index fund route or not. If I’m being honest I don’t think I would as I enjoy the investing challenge and process. So the tracking of returns is just a habit really that perhaps no longer serves a purpose for me.

-

Seems like this is what most big investors should be doing to some degree. Bain as part of due diligence on potential software company acquistions is having their employees vibe-code software pieces of potential acquisition targets to see if there really is a competitive advantage. https://www.ft.com/content/e5bac4d1-b1f8-43a4-bd54-b182d5357af0?syn-25a6b1a6=1

-

I know roughly if I am doing better than the index but no, I don’t track my performance. Not sure why I need to know what my cagr is.

-

Whether the USSR would have actually intervened is irrelevant....the mere tail risk that they might was enough to scare the hell out of Washington. The US had spent decades at that point meticulously avoiding a direct conflict with the USSR in theatres across the globe, and they weren't going to gamble on starting World War III on the Soviet border over a bunch of clerics running around in Tehran . That uncertainty alone gave the Islamic revolution a cold war deterrent shield in those early days. The US sat on its hands paralyzed by fear - not because they we're certain the USSR would intervene but because they couldn't be certain the USSR wouldn't! The Iranian regime exploited this Cold War anxiety to its maximum effect. You missed the second part of my explanation re: hostage crisis - yes expelling diplomats removes a foreign threat, but the hostage taking was doing double duty for the Islamic revolution. By manufacturing a 444-day national emergency, Khomeini forced Bazargan’s moderates to resign, purged all his secular rivals, and locked in absolute clerical control for the Islamic revolution. In that period every domestic rival was labelled an American agent seeking to destroy the Islamic revolution. See it wasn't just a counter revolutionary security operation- it was a manufactured crisis to allow for a highly calculated internal power grab. It allowed Khomeini to brutally consolidate power - highly rational for that narrow purpose. The realist answer here is quite simple - structural and geographic considerations drive who becomes enemies over time.......as you pointed out yourself Iran and Israel had a relatively cooperative relationship pre-1979. What changed outside the obvious? The structure of the Middle East. Think of it like a mini-version middle power version of the famous thucydides trap. When shared Arab enemies collapsed in the region, Iran and Israel were the only major powers left - a duopoly of power & influence, this made a structural rivalry inevitable as both pushed to grow its relative power in the region(Germany - France etc.). As for the US, I mean Iran didn't arbitrarily pick an enemy here....due to the 1953 U.S.-backed coup, Washington was already an established existential threat to any regime that took office in Tehran that wasn't to Washington's liking. But "who started it" is nonsense best left for kids in the playground...structural realities are what sustain conflicts over time.....the Israeli-Iran regional security competition would have inevitably pulled in D.C. over time regardless of the hostage incident to say nothing of the Cold War dynamics sitting above that. I will concede one thing however in the neighbourhood of your point above about creating unnecessary enemies - in a perfect world if Khomeini had an alternative vehicle to consolidate power domestically in 1979 to the US hostage crisis he should have taken it.....I don't know enough about the options available to him at the time to judge rationality or not but the hostage crisis did indeed move Iran from being enemy number 52 on the US's enemies list to being much much higher (to put it mildly). I think in this area one can argue that perhaps Khomeini/the regime miscalculated the ROI of the hostage crisis which is not the same as being irrational nutjobs. The moderator - mediator here is clearly capability. You've seen the threat equation before - Threat = Intent x Capability Death to America is rhetorical nonsense coming from the mouths of any Iranian who spews it - what US person goes to bed at night concerned that Iran may do something that would threaten the US's continued existence, the answer is precisely zero US persons. Look at the asymmetry in capability here. Death to Israel carries more freight as Iran is a larger country in closer proximity and as we've talked about engaged in a regional security competition with proxies to boot....but again let's be real here, Israel has the US security umbrella, vastly superior military capability, larger economy and if that weren't enough a nuclear capability. These phrases are hot air and rhetorical nonsense because simply they are not underpinned by any credible capability to carry them out. Iran is a threat to Israeli safety and security but it does not rise to the level of an existential threat to Israel. And as regards US and Israel wiping out Iran......lets be serious here, the reason they haven't is because invading and occupying a massive, mountainous nation of 90 million people would require a catastrophic expenditure of blood, treasure, and political capital. The ROI on total annihilation is deeply negative. Therefore, the US and Israel make the highly rational, calculated choice to manage the threat through crippling sanctions, cyber warfare, and systematically degrading Iran's proxy networks....containing the problem without paying the suicidal cost of a full-scale ground war. Epic Fury has proved both my points above again.....nobody anywhere considers the Iranian threat serious enough to expend the massive cost required to annihilate the regime. The reason Israeli/US neo-cons can't rally popular support for further military action in Iran (boots on the ground) is for that precise reason. Put simply Iran is just not a credible of enough threat that it is politically popular enough in the US to bother to pay the high price required to annihilate them. 'First shot' arguments are just nonsense and I wont get dragged into one except to say that Iran would say the first shot was the US's in 1953 with the coup they orchestrated against the regime in Tehran....but as I said before "who started it" arguments are best left to kids in the playground. Structural contemporaneous realities are what sustain conflicts over time not who did what back in the past or when it comes to the Middle East who did what back in 500 BC or 20 AD and all that nonsense!!!!! re: Attacks by Hezbollah & Hamas.....my language wasn't precise enough here previosuly but goes back to offense-defense indistinguishability arena. Yes its offensive in nature but its fundamentally a defensive strategy... the aim for Tehran, is to impose continuous friction on Tel Aviv that sits in a geopolitical grey zone. It ensures Israel must perpetually expend capital just to manage its near backyard.....a rival expending military capital near-shore has by extension less military capital to expend offshore i.e. in proximity to Iran. Again a form of offense that is functionally defensive. It is a deterrent in the sense that it shifts the theatre of the conflict to Israel's backyard and away from Tehran. Of course the other point re: Hamas and Hezbollah that nobody likes to acknowledge but is true - is that Iran has a principal-agent problem with these groups......they exert great influence over them no doubt but they don't perfectly control them and their interests aren't perfectly aligned.....US intelligence post Oct 7th shows that Tehran was as shocked as anyone regarding what Hamas had done....indeed many commentators have indicated that if the leadership in Tehran had been aware of Hamas's plans re: Oct 7th they would have attempted to stop it for the very reasons you point out....it was an act of such brutality that it invited the dog AND the owner to be shot. Iran wants low level friction that continually consumes IDF resources & political attention in Tel Aviv but not so high that attention turns directly to Tehran. Nothing in proxy warfare management is perfect. Your local proxy pitbull designed to impose continuous low level friction on your rival and keep things in a gray zone...... is an animal you only partially control and because their risk calculus is not your your risk calculus things can go wrong.....to your point and I agree with it.....Iran has a tail risk here via this proxy network that could go badly wrong for it SOMEDAY....but let's be clear, the owner hasn't been killed yet after 45y years of imposing that brutal proxy friction. Highly brutal, highly rational. The U.S. and Israel have spent decades and billions "shooting the dogs" in Lebanon, Gaza, and Iraq, but they painstakingly avoid invading Iranian soil. Even now Epic Fury was just an aerial bombing campaign that can't gain the momentum to move to a ground invasion. Hell the US couldn't even sustain the blockade of the blockade after the bombing stopped! Why? Again because even the ROI on the blockade of the blockade was negative - never a mind a direct ground war with a mountainous nation of 90 million people which would be catastrophically negative relative to existential risk Iran poses to the US. For Israel we can argue something else but that circles back to the capability problem Israel has....it can't annihilate Iran on its own. In a perfect world the leadership in Tehran should be disappeared but the world isn't perfect - they've entrenched themselves in power there with the distributed control system the purposely designed to be regime change proof. The SOH saga proves how little it takes to shut the Straits - and the world needs some kind of central Government in Tehran controlling its vast territory (if only to keep the oil and fertilizer flowing). Turning Iran into Syria for this reason alone is not a good idea. The dilemma remains the above for Bibi/ the US etc......the Iranian threat (intent x capability) has never risen to a level where the ROI makes sense for the US/European allies to greenlight the massive investment required to take out the regime (despite Bibi's years of threat inflation) and Israel alone hasn't the capability itself.......I would love to see them gone tomorrow but it's clear the cost (relative to the actual threat level from Iran) does not meet the threshold that makes sense...I totally get it, try saying the above to the family of the victims from Oct 7th or those living under air raid sirens in Northern Israel caused by rockets coming in nightly from Hezbollah. The reality however of Epic Fury ending in an MOU has proven that devastating algebra once again.....Iran and how it chooses to execute its foreign policy is a blight on the world and the Middle East but it calibrates its chaos so the juice is never quite worth the squeeze in terms of removing the regime. The one nation for which the algebra works and it would be 'worth it' (Israel) hasn't the capability to do it alone.

-

I like the successes of some african teams. They are hungry and grippy.

-

Crazy. Well done being on the ball - I'd be tempted to buy more under 2,200.

-

Yea i was deep in micron with cost basis less that $50. I felt good about my triple never dreamed it woulda been a 1T+ company. I even beleived the argument that all the AI would fill up all the storage but didnt think it would have a backlog driving them anywhere near what we are seeing now. I still have a very small position that Ill probably just let ride and see what happens.

-

Yes, when I was younger. As I grew older periodic returns became less meaningful. Today, most of my assets are privately held so there would be little to no point in even trying.

-

I track my net worth and my spending. I spend <50% of what I earn and invest the rest in real estate and investments, I have done this for several decades. I personally don't see the point in knowing the exact percentage of my investment gains year. I am unsure how I would use that information, if I didn't beat the S&P for several years, should I just move it all to an index? If I consistently beat the index or should I add leverage? I don't have interest in being fully invested in index and I don't want leverage.

-

Micron going parabolic is more luck than anything even if they held. The shortages didn't really start until fairly recently and before that the industry for DRAM wasn't really the best in terms of economics. No one even 3 years ago would have predicted that DRAM would still be sold out at prices multiple of the prior ATH

-

https://www.nbcnews.com/news/obituaries/alan-greenspan-economist-longtime-head-federal-reserve-dies-100-rcna42286 I remember when this guy did a surprise interest rate cut in Jan 2001 Marsh McLennan, which used to be MMC, went vertical for like 15 points and I got a good chunk of it Those were da days

-

More weird action on Fairfax and Fairfax India near the open

-

Likely a question for some of the wealthier folk on the board but I’m curious if you tracked your returns and CAGR etc during the earlier part of your wealth building but then when wealth got to a certain size it kind of became pointless. Obviously that number would be different for everybody depending on where they live and their lifestyle but if you are a good investor over time you will eventually get to a point where your net worth is large and whether you end up getting 5%, 10% or 20% return on that it mostly becomes meaningless. Do you still like to track it to compare yourself to others or see if you still got it, or do you now just check your net worth every now and then, and as long as it’s not dropping all is good. Maybe some people never tracked their returns, nothing wrong with that either. For me I track things quite diligently but sometimes wonder should I bother.

-

Change, you may call Iran's behavior rational but when your ideology is death and destruction to those you don't agree with, your definition of rational needs some serious adjustment. We all have to share the same World. It is really no more complicated than that. Trying to "rationalize" any definition of "rational" beyond that is truly irrational.

-

Yeah Lukaku was a bit aloof

-

I agree, Belgium looked weak here. Their whole game was odd and played without soul. Belgium used to play decent soccer with a solid defense and fast counters. The coach does not seem to use the talent he has available effectively.

-

I've been buying Adobe. Adobe sells tools to professionals, and I only think AI is gonna make those tools more powerful (they already have launched some very neat features saving professionals a lot of time). Prompting might work for some crude instructions. But translating the imagination of a creative into something tangible is probably easier by hand (mouse+keyboard) than by prompting. It's not like people are already particularly good at articulating their (creative) visions. There is competition at the edges, but I think it's a bit overblown. Adobe could buy Figma with one years' worth of free cash flow (and probably should pay for a new ballroom to make it happen)...). With all the AI slop being generated, trust is only becoming more important. I think strong software vendors with good customer relations will do fine, as long as they keep up with competition and improve their offerings. Adobe might've gotten a bit arrogant, so I don't mind if they lay off the price hikes for a bit and increase freemium offering.

-

Great game? It was fucking disgraceful. Never been more ashamed of my country's football until now. They have two draws in the weakest group of the entire world cup... Still don't understand what Lukaku is still doing on that pitch... can barely hold a ball let alone properly pass or dribble. We have little to no dribbling skills except for Lukebakio and for some reason he doesn't even get to start. I would still give the advantage to Egypt here based on the past two games.