All Activity

- Past hour

-

My kids are older but my wife and I always invite them on our trips abroad, which they usually accept (go figure). One of them also had a speech impediment when he was young but our Pediatrician never advised us to do anything formal about it since he was otherwise a smart, energetic, highly motivated kid. Still is, and though in hindsight we wish that we'd have taken him to a specialist, he manages OK but it takes more effort than it probably should on his part.

-

They'll be opportunistic. If they find they are getting sports programming in a nice package for a fair amount, they will buy it. Sports programming is really the only thing keeping cable alive. Eventually, the streamers will replace the cable companies once they realize tie-ups with the cable companies aren't worth it any more. We're not there yet. Cheers!

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

I would like some feedback. I am in the process of updating by book on Fairfax. I am doing a pretty substantial edit - structure and content. It will probably take me 6 months before the book will be ready to be published (parts of it are a mess right now). I have two options with publishing the edits... All at once: Wait until the book is complete Publish chapters as they get completed. The new book will have a chapter on Management and Culture. The six articles above are from that chapter. My question is what option do board members prefer? Hold off... and publish everything at once? Likely late this year. Or do it in serial format - publish the chapters as they get completed. Like what I did with the Management/Culture chapter? My guess is I will complete a chapter about every 2 weeks (the next chapter, insurance, is almost done). Thanks in advance... -

Adding to Sony. It doesn't have the IP of Nintendo but at least management is restructuring to increase margins. Games are in the dumps but imaging is getting a nice tailwind from AI. Not world beaters but solid balance of businesses reasonably well run still at 6 times cf.. I like the anime stuff.

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

Article 6 - the final one in the series. Personnel Changes and Succession Planning For most investors, personnel announcements are easy to ignore. A new CFO is appointed. A division president retires. An executive receives a promotion. These events rarely affect next quarter's earnings, so they often receive little attention from investors. That is a mistake. Personnel decisions can provide valuable insight into a company's culture, leadership development, organizational depth, and succession planning. Financial statements tell investors what happened in the past. Personnel decisions often reveal how a company is preparing for the future. This is especially important for founder-led companies. The transition from a founder to the next generation of leaders is often one of the most challenging periods in a company's history. Many successful organizations struggle when the founder eventually steps aside. As a result, investors should pay close attention to how succession planning is being executed long before a leadership change becomes necessary. For Fairfax investors, the key question is straightforward: Has Fairfax built an organization capable of thriving beyond Prem Watsa? What Investors Should Look For When evaluating succession planning, three questions are worth asking: Why did the vacancy occur? How was it filled? What does the transition reveal about the company's future leadership? The answers can reveal whether a company is developing talent internally, retaining key employees, and preparing future leaders before they are needed. Succession planning is not a single event. It is a process that often unfolds over many years. Internal Promotion Perhaps the most striking observation is how frequently Fairfax fills important positions from within. Examples include: Peter Clarke becoming President of Fairfax in 2022. Brian Young assuming increasing responsibility for Fairfax's insurance operations in 2023 and 2025. Amy Sherk becoming Chief Financial Officer in 2025. Debbie Chalkley becoming CFO of Fairfax India in 2025. Gobi Athappan becoming Chairman and CEO of Fairfax Asia in 2024. Gopal Soundarajan becoming CEO of Fairfax India in 2024. In most cases, these individuals spent years—often decades—within Fairfax or Fairfax-related organizations before receiving larger responsibilities. This suggests Fairfax has invested heavily in developing talent internally and preparing future leaders. More importantly, these promotions were not emergency replacements. In most cases, the individuals had been preparing for larger responsibilities for years. This suggests Fairfax views succession planning as an ongoing process rather than a one-time event. Gradual Transitions Another notable characteristic is that important transitions are often executed over several years. The insurance business provides a good example. In 2023, Brian Young began sharing oversight responsibilities with Andy Barnard across Fairfax's insurance operations. In 2025, Young became President of Fairfax Insurance Group while Barnard transitioned to Chairman. At the same time, Carl Overy became CEO of Odyssey Group after years of increasing responsibility within the organization. Rather than abrupt leadership changes, Fairfax appears to favour a gradual transfer of responsibility. The same pattern can be seen at Fairfax India. Chandran Ratnaswami transitioned from CEO to Executive Vice Chairman while Gopal Soundarajan assumed the CEO role. Chandran remained actively involved in the business, helping ensure continuity during the transition. The 2025 CFO transition followed a similar approach, with Jennifer Allen moving to the newly created position of Chief Business Officer while Amy Sherk assumed the CFO role. Experience Is Retained At many companies, succession planning means replacing one executive with another. Fairfax often takes a different approach. Senior leaders frequently remain involved after relinquishing their former positions. Andy Barnard became Chairman of Fairfax Insurance Group. Chandran Ratnaswami became Executive Vice Chairman of Fairfax India. Prem Watsa stepped back from quarterly conference calls beginning in 2024 while remaining CEO. This approach allows Fairfax to preserve institutional knowledge while creating opportunities for the next generation of leaders. Increasing Leadership Depth One of the most important developments for investors is the increasing visibility of leaders beyond Prem Watsa. For many years, Fairfax was viewed largely through the lens of its founder. That perception has gradually changed. Peter Clarke has become a prominent leader at the corporate level. Brian Young has assumed a larger role overseeing insurance operations. Wade Burton has become increasingly visible in investment management. Amy Sherk now serves as CFO. Numerous operating company executives have assumed greater responsibilities throughout the organization. The result is a leadership team that appears significantly deeper than it did a decade ago. The Exception: Paul Rivett The departure of Paul Rivett in 2020 remains one of the more significant executive changes in Fairfax's history. Rivett served as President and was widely viewed by investors as one of Fairfax's most important executives. What matters from an investment perspective is what happened afterward. Fairfax successfully redistributed responsibilities, continued to execute its strategy, and eventually promoted Peter Clarke to President. The organization continued to strengthen despite losing a senior executive who had played a major role in the company's development. That outcome reflects positively on Fairfax's organizational depth and the strength of the broader management team. The Next Generation Succession planning is ultimately about people. Two of Prem Watsa's children currently serve on Fairfax's Board of Directors: Christine McLean (born 1978) Ben Watsa (born 1981) Importantly, both built careers outside Fairfax before assuming governance responsibilities within the organization. Christine spent much of her career at Sprucegrove Investment Management, where she served as Director of Research before becoming a portfolio manager. She currently works at Fairbank Investment Management. Ben is the founder and Chief Investment Officer of Marval Capital and previously spent more than a decade as a partner and portfolio manager at Lissom Investment Management. He also serves as Chairman of Fairfax India. For investors, the key issue is not family involvement itself. The more important question is whether future leaders possess relevant experience, independent judgment, and credibility. The evidence suggests both Ben and Christine developed meaningful investment experience outside Fairfax before assuming larger roles within the Fairfax ecosystem. Prem has been clear that the Watsa family intends to maintain control of Fairfax over the long term. At ages 48 and 45, Christine and Ben potentially have decades of involvement ahead of them. Continued family ownership could help preserve the long-term orientation, culture, and capital allocation discipline that have been central to Fairfax's success. At the same time, Fairfax's future will depend on more than the next generation of the Watsa family. The company has spent years building a deep bench of leaders across its insurance, investment, and operating businesses. The evidence suggests Fairfax is preparing not simply for a change in leadership, but for the continuation of the institution that Prem Watsa spent forty years building. What Are the Key Learnings for Investors? Several conclusions emerge from Fairfax's personnel decisions over the past five years. First, Fairfax appears to have unusually strong employee retention. Second, the company consistently promotes from within, suggesting it has invested heavily in developing talent and preserving its culture. Third, succession planning appears to be proactive rather than reactive. Leadership transitions are often planned years in advance and executed gradually. Fourth, Fairfax has demonstrated an ability to retain the experience of senior executives while simultaneously promoting the next generation of leaders. Finally, Fairfax appears to be reducing key-person risk. While Prem Watsa remains the company's most important leader, an increasing number of executives now play visible and meaningful roles across the organization. Conclusion Personnel announcements are often viewed as routine corporate news. For investors, they can be much more important. They provide insight into a company's culture, leadership development, organizational depth, and succession planning. The evidence at Fairfax suggests a company that has spent years building leadership talent internally, promoting from within, and preparing for the future. The result is an organization that increasingly looks less dependent on any single individual and more like a durable institution. That may be one of the most important developments at Fairfax over the past decade. The long-term success of the company will ultimately depend not on whether Prem Watsa remains involved, but on whether Fairfax can preserve the culture, leadership, and capital allocation discipline he spent forty years building. The evidence suggests that transition is already well underway.

-

I tend to agree that perpetual futures are more akin to swaps than they are futures given the funding mechanism being an explicit accrual/exchange of cash on a daily basis with hourly accruals. I think they're a superior product to futures with the little experience I have trading them, but wouldn't mind if they were labeled 'perpetual swaps' instead.

-

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

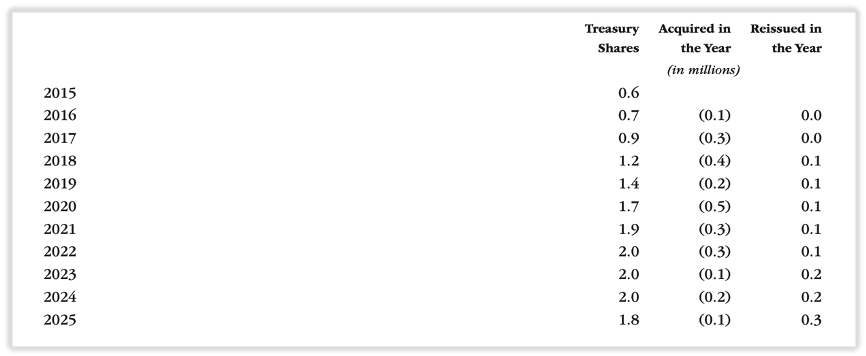

Article 5 in the series Getting Employees to Think Like Owners – Fairfax’s Compensation Programs "Show me the incentive and I'll show you the outcome." – Charlie Munger Incentives matter. People generally respond to the incentives placed in front of them. If compensation rewards short-term results, employees will naturally focus on short-term results. If compensation rewards long-term value creation, behaviour tends to follow. For this reason, compensation systems play an important role in shaping corporate culture. Over time, organizations tend to become what they incentivize. At Fairfax, compensation is not simply about attracting and retaining talented employees. It is also a tool used to reinforce one of the company's core beliefs: employees should think and act like owners. Why Compensation Matters at Fairfax Compensation programs are important at every company, but they are particularly important at Fairfax because both of its core businesses require a long-term perspective. In insurance, premiums are collected today while the ultimate cost of claims may not be known for years. An underwriting decision that appears profitable today may ultimately prove to be unprofitable. If compensation is tied too closely to short-term results, managers can be tempted to chase premium growth or underprice risk, leaving future shareholders to absorb the consequences. The same principle applies to investing. Many of Fairfax's most successful investments—including Eurobank, Stelco, Poseidon, and Bangalore International Airport—required years for the investment thesis to unfold. Successful investing often demands patience and a willingness to look beyond quarterly results. Because of the long-duration nature of both insurance and investing, Fairfax needs compensation programs that reward long-term value creation rather than short-term performance. The challenge is designing incentives that encourage employees to think and act like long-term owners. The Owner-Operator Mindset One of the defining characteristics of Fairfax is its emphasis on ownership. Prem Watsa has long encouraged employees to become shareholders, believing that ownership changes behaviour. People who think like owners tend to make better long-term decisions than managers whose incentives are tied primarily to compensation or short-term results. The logic is straightforward. When employees own shares, they participate directly in both the successes and failures of the organization. Their interests become more closely aligned with those of outside shareholders. Decisions are more likely to be evaluated through a long-term lens because employees benefit from increases in intrinsic value rather than simply maximizing short-term compensation. This owner-oriented philosophy is reinforced through several compensation and employee ownership programs across the organization. Senior Management Compensation One of Fairfax's most important initiatives involves its senior executives. For nearly a decade, annual bonuses for senior executives across the organization have generally been paid: 50% in cash 50% in Fairfax shares The Fairfax shares vest over five years. This structure accomplishes several objectives simultaneously. First, it encourages executives to think beyond the current year. Second, it promotes retention because employees must remain with the organization to fully benefit from the awards. Third, it aligns management's financial interests more closely with those of long-term shareholders. Importantly, Fairfax purchases the shares awarded under these programs in the open market and holds them as treasury shares until they vest. As a result, shareholders bear the economic cost of compensation but avoid much of the ongoing dilution commonly associated with stock-based compensation programs. Employee Ownership Programs The ownership philosophy extends well beyond senior management. Fairfax also offers employee share ownership programs that encourage employees throughout the organization to become shareholders. The objective is not to create owners only at head office. It is to encourage an ownership mindset throughout the company. Over time, Fairfax has accumulated a significant number of treasury shares on behalf of employees participating in these programs. The steady growth in treasury shares suggests that employee ownership continues to expand across the organization. Benefits and Costs Shareholders should care about compensation because incentives influence behaviour. Fairfax's programs offer several potential advantages: Better alignment between employees and shareholders. Improved retention of talented managers. Greater emphasis on long-term value creation. Reinforcement of Fairfax's owner-oriented culture. The programs are not free. In 2025, Fairfax awarded approximately $189 million of compensation in Fairfax shares. This represents a real economic cost that is ultimately borne by shareholders. The relevant question, however, is not whether the programs cost money. All compensation programs do. The more important question is whether shareholders receive value in return. Fairfax appears to believe that encouraging long-term ownership improves retention, strengthens culture, and aligns decision-making throughout the organization. The company's willingness to continue expanding these programs suggests management views the benefits as exceeding the costs. What This Means for Shareholders Compensation systems reveal what an organization values. Fairfax's compensation programs are designed to encourage ownership, patience, and long-term thinking. By requiring senior executives to hold shares for extended periods and encouraging employees throughout the organization to become shareholders, Fairfax aligns incentives with the creation of long-term value per share. Insurance and investing are businesses where results often take years to emerge. Fairfax's compensation structure reflects that reality. Rather than rewarding short-term outcomes, it encourages employees to think and act like owners. In doing so, the company reinforces one of the central pillars of its culture: treating shareholders as partners and building value over the long term. ------------ Supporting Material Exhibit 1: Prem Watsa on Employee Ownership (2025 Annual Report) We continue to encourage all our employees to be shareholders of Fairfax. We think it will be a great investment for them over the long term and great for the company to have our employees as shareholders in the company. As part of that initiative, close to 10 years ago we decided to have a general principle that our annual bonuses to senior executives across the company would be awarded 50% in cash and 50% in Fairfax shares that vest in five years. As these bonus shares are awarded, the company buys the shares in the market (which comes out of shares outstanding) and they are recorded as treasury shares, as shown in the table below. As the shares are vested and or exercised, the shares are then reissued and come out of treasury shares and back into shares outstanding. You can see over the years our treasury shares have increased from 0.6 million to 1.8 million today. We think this is fantastic and hope they continue to grow over time. You will notice that the treasury shares acquired have remained relatively consistent over the last five-year period, especially when compared to our increased employee numbers. Our total compensation, including benefits, paid to our employees worldwide was $2.9 billion in 2025, of which $189 million was awarded in Fairfax shares. As I have said in the past, we would love to have all our employees as owners of Fairfax. Of course, no new shares are issued for these plans. They are all bought in the market. Exhibit 2: Prem Watsa on Employee Stock Ownership Plan (2025 Annual Report) Fairfax also has an Employee Stock Ownership Plan that is available to essentially every employee in the company. The plan offers each employee the opportunity to take up to 10% of their salary annually in Fairfax shares. The company will automatically match 30% and then if certain targets are met (primarily underwriting profit), the company matches an additional 20%. The participation rates differ by company but generally for our large companies, we have a participation rate of approximately 60% and it has been increasing over time. (More on this plan in the Miscellaneous section at the end of the letter.) Miscellaneous Section (2025 Annual Report) Fairfax now has 22,000 employees in its insurance business; 10% in Canada, 30% in the U.S., 20% in Europe, 15% in both Asia and the Middle East, and the remaining 10% in Africa and Latin America. Also, Fairfax has 40,500 employees in its consolidated non-insurance businesses, mostly in Canada and India. As I mentioned earlier, we want our employees to be owners and to benefit from the performance of their company. We have strong participation in our employee share ownership plan under which our employees make share purchases through payroll deductions, supplemented by contributions from their employer. It is an excellent plan, and employees have had great returns over the long term, as shown below: If an employee earning $40,000 had participated fully in this program since its inception, he or she would have accumulated more than 4,000 shares of Fairfax worth Cdn$10.7 million at the end of 2025. I am happy to say we have many employees who have done exactly that! Of course, it is highly unlikely this will be repeated – but it will still be a great long-term investment for our employees!

-

I believe they 49% but that does not include their CCPS which if allowed moves Fairfax to over 60% as I recall.

-

Part of the reason for me posting this thread, in addition to hearing all the cool things people are doing with their kids, is that I have one boy who will be four in the next month who doesn’t speak. He knows words, occasionally says words (animals, numbers etc) but he doesn’t really use words to communicate - he’ll take my hand and show me what he wants instead. He’s clearly very intelligent, understands a lot of things I say, and has an unusual memory and eye for detail which is well beyond his peers, but obviously well behind with verbal and communication skills. The biggest issues with his non-speaking is the low expectations of others, and others who hint at certain diagnoses. It’s also going to be a problem when he entered more formal education in the next 18 months - if he isn’t speaking by then. I was wondering if anyone else has had a similar experience and what advice they might offer.

-

Whether your own children, or your nephews / nieces, or whatever, in my view they are the only investment that really matters. I know that many on the board have cool things they do with their kids. Would be great if you could share some of those things as ideas for others. I know others are thinking about how to teach their kids about finance, and I’ve seen it in other threads. Some of you also have challenges with kids in your life and this might be a place to speak about that.

-

When did you stop tracking your returns?

backtothebeach replied to Milu's topic in General Discussion

I've always wondered what you mean by this. No need to reply if it is too confidential, ha. - Today

-

When did you stop tracking your returns?

SharperDingaan replied to Milu's topic in General Discussion

As the managing partner of our family investment funds, part of our AGM has always been a letter/presentation outlining the thesis behind each of the concentrated positions that we hold; the initial premise, what has changed, expected future pro's/con's, how it has worked out, 6-yr to date CAGR (hold period), etc. Primarily as both a training tool, and as insurance against my having an incapacitating stroke tomorrow. It has worked out very well, and also become a great tool for look-back analytics. The letter/presentation similarly speaks to the overlays of dividends, swing/pair trading, and capital repatriation. Thesis, what has changed, actual vs expected results, reconciliation of inception to date capital repatriations by family member. Primarily for reporting, training, and insurance purposes. It has also worked out very well, keeps discussion future orientated, focused, and the family informed. The hope was that nephews would take over; they aren't going to, and the family is OK with that. Ultimately, the portfolio will hold just index funds, a laddered bond portfolio in run off, UK real estate, and repatriate a quarterly distribution; mechanics evolving as required. I post, as I hold each of a MBA/CPA/CFA, and run the partnership the same way that a CEO might run a private investment business. Expected to have transitioned out well before age 75, and not put my lay person partners at excessive risk. Different strokes. SD -

AM Best upgraded Polish Re. It is always interesting to see rating upgrades to some of the smaller insurance subs as it provides some insight we normally don't have visibility to. https://news.ambest.com/NewsContent.aspx?refnum=275297&altsrc=23 //BestWire// - AM Best has upgraded the Financial Strength Rating to A (Excellent) from A- (Excellent) and the Long-Term Issuer Credit Ratings to “a” (Excellent) from “a-” (Excellent) of Polskie Towarzystwo Reasekuracji S.A. (Polish Re) (Poland). The outlook of these Credit Ratings (ratings) is stable. The ratings also reflect the lift Polish Re receives due to the support provided by its ultimate parent, Fairfax Financial Holdings Limited (Fairfax) [TSX: FFH], in particular the explicit parental guarantee in place for Polish Re. In addition, Fairfax provides technical support in areas such as reserving, retrocession protection and investment management services. Fairfax’s commitment to Polish Re was demonstrated by its PLN 78 million (USD 18 million) capital injection in 2023. Polish Re’s risk-adjusted capitalisation, as measured by Best’s Capital Adequacy Ratio (BCAR), was at the strongest level at year-end 2025, and it is projected to remain at the same level in the medium term. Further supporting factors are Polish Re’s low dependence on retrocession and conservative investment strategy. Reserve development has been positive since 2024. Prior to 2024, the runoff of motor third-party liability business exhibited material volatility. Polish Re’s adequate operating performance assessment is supported by a five-year (2021-2025) average combined ratio of 95.4% and a five-year (2021-2025) average return-on-equity ratio of 10.7% (both as calculated by AM Best). The company’s underwriting performance improved in 2025, as evidenced by a combined ratio of 92.0% (2024: 97.8%) (as calculated by AM Best). Robust investment results supported an overall net profit of PLN 85.6 million (USD 23.8 million). Prospectively, investment income is expected to be a consistent contributor to the company’s profitability. Polish Re benefits from a diversified underwriting portfolio, with operations spanning approximately 40 markets. The company’s largest markets, as based on gross written premium in 2025, are Poland, Turkey and Israel. Additionally, the company has expanded its agriculture line of business significantly in recent years. AM Best considers Polish Re’s ERM to be developed and appropriate for its risk profile and operational scope.

-

MSFT for kids and Mother in Law.

-

BB up 20% today on revenue beat. Wonder if Fairfax still owns it. We'll know soon enough. Close to 5 year highs:

-

-

Yes. I hadn’t realized that FIH had such a big stake in IIFL Capital, but in May they announced their intention to go from 30.5% to at least 51%, so that would be possible, assuming they have acquired as many shares as they intended to. They own 49% of Go Digit so I presume they would need Kamesh Goyal’s approval to make Go Digit a subsidiary, but it’s possible.

-

-

If IDBI owns 50.1% of each I think it would still count as a subsidiary.

-

Sold my BXP.L (Beximco Pharmaceuticals PLC) position

-

Dont get me wrong - never said Truman was wrong to use this new weapon as means by which to bring the Japanese to surrender. We had already committed to concept of destroying Japanese cities by bombing at that point as a means to get them to surrender......before the nuke dropped we'd levelled 60-odd cities at that point killing hundreds of thousands of Japanese. What was another city at that point when we'd done it to 60+? Moving to use the nuclear weapon was a no brainer simply as means to potentially change the trajectory of things away from needing to do a ground invasion. My core point was that people over attribute the Japanese surrender to the nuclear bombs dropping and under attribute the entry of the USSR into war two days after Hiroshima but before Nagasaki. The best evidence as the article covers is Hiroshima on Aug 7th produced no emergency meeting of the Japanese Supreme Council - Hiroshima it seems was just another city being levelled by American bombing. What did produce an emergency meeting of the Japanese Supreme Council was news reaching Tokyo on Aug 9th of the Soviet declaration of war. The answer is both things undoubtedly fed into their surrender. The nuclear taboo is such that we tell ourselves it was 100% the dropping of the bombs in Hiroshima and Nagasaki that did it. The evidence tells a more complicated story.

-

ICE, MKTX and TW Thanks Lance

-

Many thanks for this very detailed article @petec! Unfortunately I bought in here at the end of March 2020, and been watching the disaster unfold ever since, using it as a lesson in humility regarding my own modest abilities. Just to clarify a detail from your article: Helios (the asset manager) posts an annual loss of around USD 8 million, yet was carried on the books at a valuation of USD 104 million at the end of 2025? Is that a correct summary? Honestly that makes me worry about the potential gap between valuation and reality for the other assets... It would have been interesting to see a peer comparison included in your article, for instance with "The Bidvest Group Limited" (BVT.ZA). While buying into that stock during the COVID lows would also have been a mistake, it at least held up reasonably well and paid out some dividends since then.

-

haha i can do that already. I have all my financial institutions pushing via API into google big query. and have created a google gem called family CFO that can analyze probably 80%+ of my financial picture at almost any given time. I have been a big fan of journaling through my life and find a good amount of benefit from writing down my own thought. Granted my own writing style and grammar sucks so ive often taken to having AI rewrite things for me so they are more coherent to others. I think the exercise of writing my own thoughts on my investments on an annual basis would have some really solid merit from a self reflection standpoint.

-

Let's add another two months to the trend.