All Activity

- Past hour

-

Always remember guys that we are only going to discuss what the Don wants us to. It will go here, it will go there, but it will be what he wants when he wants. Our media is desperate to sell the ad and the Trump orgy of topics is the premier. So today it is elections... For a few days we aren't talking war, Epstein is long gone as are many other Trump issues. Today will go nuts about elections, wild ass accusations and bizarre comparisons to developing nations are absolutely relevant...a huge threat to ou country. Just remember that if the pubs win then there is no election fraud and it has zero importance. Accusations are silly at that point, off topic, Trump will have you obsessed about something else and the ads will be a-sellin'. For a decade now and most likely until this fragile fake pathetic thing dies you will discuss what he wants. The political thread, the entire US chat box, is owned by the Don. Can't wait to see the excitement and potential of a bear market, likely the only thing that will derail Trump's domination of the US. Keep in mind after Trump is gone you'll will finally wake up to the fact that this was like nature's chaotic storm, that there's massive cleanup. You'll also see that nothing was gained that you (and me) just wasted over a decade of your life letting the Don rule your life.

-

I think compute is the way to look at it. It is a commodity so demand and supply apply. At the moment demand is pretty much infinite because AI is so compute intensive in its current guise and it is being massively subsidised for its users (with OpenAI Anthropic losing billions a year). Training the LLMs and developing new AI related software requires a lot of compute. Companies are also encouraging their employees to use AI i.e. tokenmaxxing. There also hasn't been a shakeout yet so there are a lot of startups using compute in many cases being subsidised by Nvidia or the hyperscalers and this is all supporting demand. Also many of these datacenter projects are in the pipeline so haven't gone live and aren't yet affecting supply. Nor are they hitting P+L of hyperscalers because they are accounted for as construction in progress. Their legacy cloud businesses are doing incredibly well because the AI buildout is creating a lot of extra cloud demand but supply. A lot of people are arguing that AI is a FUNDAMENTAL bubble. In other words people are extrapolating fast growth which is unsustainable. Valuations aren't as crazy as during the dot-com bubble and that is giving people a false sense of security. It is a build it and they will come approach. The problem could arise a few years down the line when supply/capacity is greatly expanded as a result of these massive investments but demand hasn't increased as fast as expected. Most of the ROI figures only really make sense if you assume either massive productivity improvements or significant job displacement (but in the latter case if that happens as fast as the hyperscalers need it to happen then the economy is in trouble because consumption represents the majority of GDP and people without jobs generally don't spend much)

-

Sanjeev [ @Parsad ], If you were a piece of classic furniture, then it's called patina, which is valueenhancing!

- Today

-

Insightful report, thank you! Recently read a quite exenstive report doing a deep dive and breakdown of Markel - coming out at more or less the same discount. Next to BRK and FFH, MKL is quite the weight in my portfolio so I genuinely hope management ups the ante with the buybacks at these valuations. I don't expect them to be as opportunistic as FFH, but still. I like the general set up of these three names over time, with FFH probably being the powerhouse whereas MKL and BRK I'd say still about 10+%-ish returns (hopefully MKL a bit more though).

-

In the UK we have to prove we are eligible to vote, have to bring voter ID, mail in ballots are highly restricted, and everybody brings their own refreshments if they need to stand in line. It’s really not a big deal. There US voting system is a bit of a mess, and there are a good number of the population that don’t trust election results. It’s strange to me that so many people are resistant to tightening the system up to ensure trust in the process.

-

I doubt any of the hyperscalers are even thinking about ROI for AI. They're doing so because they think that they have no choice cause everyone else is spending with their heads cut off. Well, except for Apple which may end up in better shape than everyone else in the aftermath of this.

-

thanks! Yes it is. It also uses 2025 YE numbers for all companies so the discount for Fairfax and Markel today will be larger than what’s shown there and Berkshire is likely also at a small discount. Because income statement and balance sheet for all is larger than at YE 25.

-

Like preventing any food and water from being given to those in lines in Georgia...etc. He's talking about taking measures to cut back on voting...how ballots are drawn up...mail in ballots...etc. He's going to make it extremely difficult for many voters on both sides...but he'll wipe out more on the left. He's going to get a proxy 3rd term or more! Cheers!

-

Exactly! By requiring only US citizens vote and eliminate voter fraud. No more elections like LA. Great plan.

-

Trump informing the world right now how he's going to get his picks elected this fall and in 2028. Erode trust in the election process, get basically a 3rd term by enacting reforms that make it hard for Democrats to vote. Cheers!

-

Serious question for you Parsad: Why in the world, would C-SPAN, the non-profit that broadcasts all Federal legislative hearings - actually broadcast such a thing? You would think C-SPAN be immediately expelled.

-

CME and ICE are each working on a futures index contract for compute capacity at data centers that use NVDA chips. One index is being created by someone who used to work at Bloomberg, the ICE one is by ORRN (sp?) which is a broker for data centers and people who want to rent computing power for AI startups. If you think AI or chip companies are overvalued but you have an opinion on the amount of Chips and energy that is going to be needed by data centers. This might be a way to play it. Both of them have submitted the contracts for approval by the cftc but they are both still pending Kalshi lets you bet on computing capacity now, but in a really stupid way. You have to buy a bunch of yes, no prediction market contracts at different prices and for your own forward pricing curve.

-

Funny! I actually have heard of this...a guy's arm got impaled on one of those pointy iron fence posts. He was just trying to climb over, but fell on his arm and his own body weight impaled him. Cheers!

-

That's not real! No way you keep talking with no hesitation or slightly warped face after you let out something like that. Cheers!

-

I embraced my lack of hair a long time ago. I'm one of those people that believe the wrinkles, baldness, belly fat, sore joints, etc are all indications of a life lived. Not necessarily well-lived, but lived! No interest whatsoever in hiding the flaws! Cheers!

-

Is the valuation framework you laid out on page 14 the framework Markel laid out in last years annual report? i hope your investors do well!

-

i had a college buddy a long while back who had to0 much to drink, tried jumping a fence like that and got caught on the leg and was hanging there. I believe he was by himself, had to get himself off and call for help. I still shiver when i think of it.

-

Came across this interesting metric while going through the Tesla fanboy reddit forum. Wiki had this to say: "[...]model was found to be approximately 80–90% accurate in predicting bankruptcy one year before the event[...]" Mainly developed for asset heavy manufacturing companies, but there have been tweaks/updates for other types(asset light) of companies as well. Seems like this commonly taught in finance academically. Just curious if anybody uses it in their work flow, and how much value it really adds(mainly if it's really as predictive as wiki claims)? I don't know if there are any short sellers that frequent this forum,, but I would imagine such a metric be interesting for them, similar to *ckedcompany during the dot.com's. Some companies that look like good candidates for buying LEAP puts, according to this metric are: Ford and Boeing. Interestingly enough, pretty much all the US airlines flashes red with this metrics.

- Yesterday

-

How to remove a deer from a fence

DooDiligence replied to DooDiligence's topic in General Discussion

I've heard similar stories from others after telling them about this. Apparently deer aren't very good at jumping fences. -

We need age limits on these bums!

-

It’s a real loss in the sense it hits book value, increases leverage ratios giving less financial flexibility and reduces the ability to grow premiums. I think the reason why Berkshire and Fairfax to a lesser extent keep a short duration is so they can take advantage of a hard market if it shows up the same time rates are going up like in 2022. It’s optionality that in theory is at the expense of higher yields but when the term structure is relatively flat, it doesn’t pay to extend duration. I can see a scenario where Fairfax extends duration but the yield curve will likely be much steeper. One of the features of FFH and BRK is there ability to take advantage of volatility as @Viking has pointed out. That’s with respect to premium growth as discusses above but also by holding more cash than they need to at the insurance subsidiaries. They can take advantage of big dislocations if they happen. Their equity holdings which are separately financed could do the same. It’s another reason FFH should trade at premium.

-

Yup, lot of them there.

-

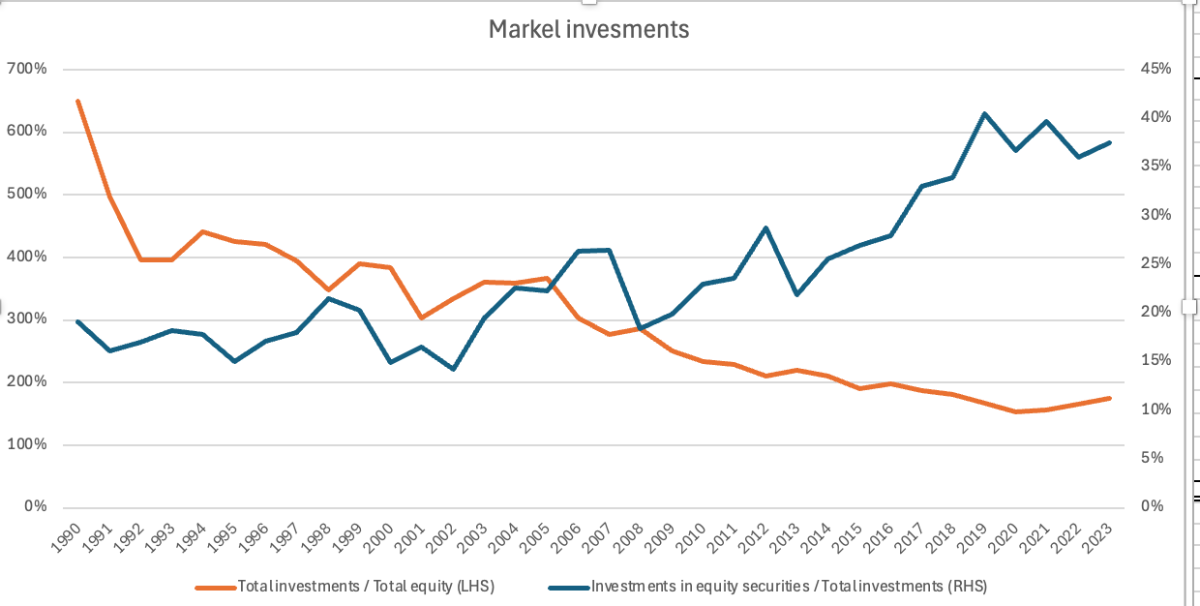

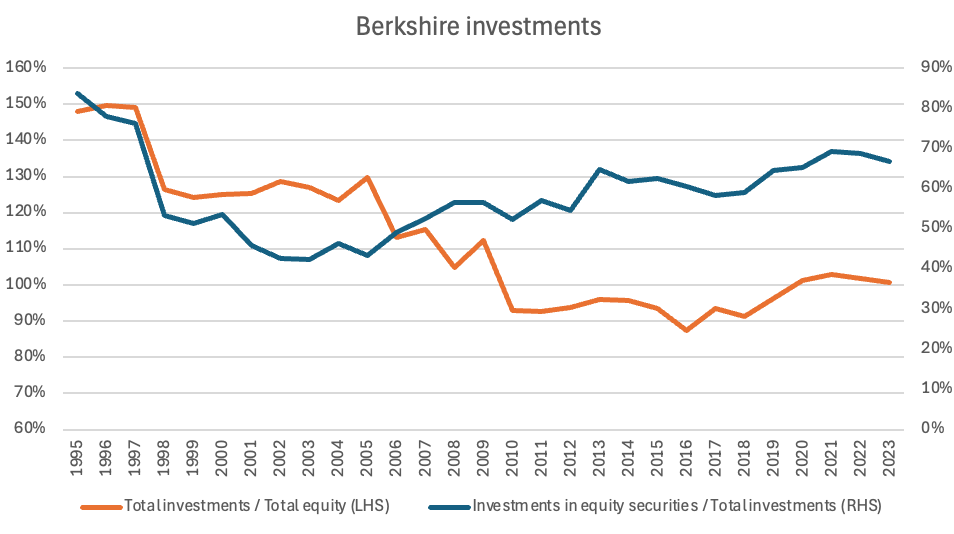

Thank you everyone for the feedback and in general I have to shout out to CoBF. For no company have I learned so much by just being engaged on a forum with so many informed posters who in my opinion are in the top 1% of investors (maybe even better) w.r.t understanding the nuances of Fairfax in a deep way. And the best part its free...When I presented, I mentioned a big part of my conviction building was reading Viking's book cover to cover (and 25 of Prem's annual reports in a row). RRR, I have thought about this question and it's a good one. There are two angles I would answer it with: i) The investment leverage an insurer operates with is linked to the mix of equity proportion in the investments. Equity requires more regulatory capital against it, fixed income less. So all else, if you have more equity in the book, you investment leverage has to run lower. Take a look at the leverage Berkshire and especially Markel had in earlier days. When they had a lower proportion of equity in the book, their investment leverage was much higher. These charts are evidence and should give you confidence that Fairfax is operating at a higher leverage partly because they can because their equity book is smaller than Berkshire and Markel. What is great about that set up today is that, have a meaningful part of the book in Fixed income is great because you earn 5% on it! Which is why today, Fairfax has the best set up with the highest ROE (as shown in my presentation). (In a zero rate environment it won't work as well i.e you would rather have lower leverage with as much in equities as possible). ii) The second lens I would use is to say, the amount of leverage Fairfax can take is highly regulated and scrutinised. So they are maximising the amount of leverage they can take based on regulatory constraints. The reason that's not risky as typical leverage because majority of the leverage comes from float which can be though of long term negative cost of capital debt. As opposed to debt which has positive cost of capital (ie interest payments) and covenants against it which can hinder you in the short term even if 1 year is bad eg. Covid but float doesn't have the same downside.

-

The way I look at it, Fairfax is leveraged, but it is a relatively locked in and safer type of leverage than a margin loan for example. I'm always hesitant to put leverage on top of leverage. Which is why I have kept away from that even when equities like Berkshire were in the doldrums. In retrospect, I could've made much better returns, but I think my sleep is worth a lot more to me. I'd rather let the masters take the leverage risk and show me good ROE numbers. As you pointed out there was a time just this past decade where Fairfax traded under 0.6x BV. In Fairfax case, I notice they are very careful with investing the float. The bond portfolio is purposefully kept to a relatively short duration often times even shorter than liabilities. Even though it's not a real risk because they don't sell these bonds, it's nonetheless a paper loss, and the market and rating agencies often consider this even if it's a transient paper loss. I think they watch this very closely. They may take additional risk on the equity side, but I think they are very careful with bonds. They're currently averaging 5% on the fixed income side without taking much risk. Thats frankly impressive. They've actually done better of late on the private equity side(cons/aff) than in publicly listed investments. It's just great to see them with so many options to reinvest cash.

-

@Viking and @Maverick47 have provided great responses. From my perspective, I have FFH at over 50% of my net assets and I’m adding my own leverage (via margin) to own it so I worry about leverage in terms of the real risk of impairment and about price volatility which could cause problems for me given my variable source of capital (the margin loans) forcing me to liquidate at the worst time. I don’t recommend anyone do this but I don’t lose sleep with respect to Fairfax based on the structure of the balance sheet, the conservatism of the valuations and the low starting valuation. The sources of Fairfax’s leverage are the float and long term non-callable debt with no near term maturities. @djokovic1 succinctly explained how Buffett thinks about insurance float for a high quality insurance company. I don’t see this leverage to be anywhere as risky as bank debt as for a well run insurance company it’s always growing. No near term maturities and long duration of issued bonds along with large revolving unused debt capacity also makes it unlikely the debt at the holdco becomes a problem. The balance sheet is conservative with respect to valuations on both sides as @Maverick47pointed out. Carrying value for the equity portfolio is well below fair value for not just what we know about (Eurobank, Poseidon etc..) but also for the positions where there is no reference price. It’s not hard to get $8b in fair value over carrying value which is 2x what we know about. The liabilities are also over stated due to the conservative reserving during hard market’s as was highlighted above. The normal interest rate environment also means holes are filled in very fast for negative surprises that show up in the equity portfolio or due to unusually large cat losses beyond reserve releases. Despite the low starting valuation for Fairfax, it’s still a stock. So bad things can happen. I have my leverage at 25% of assets so I can take a large drawdown before I need to start selling. Fairfax would have to trade below 0.95x BV. It was there a few years ago so of course we could go back but I’m making the bet that we won’t. It’s a risk I’m willing to take. What helps is that BV is growing 3-6% a quarter for the most part so my risk goes lower every day. The higher leverage should be why Fairfax trades at a big premium to MKL and BRK but the market structure keeps it at a discount. That’s the opportunity.