All Activity

- Past hour

-

Looks like we could have two extremes with nothing in the middle. We need a third party that Thomas Paine would have called the Common Sense party.

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

thepupil replied to thepupil's topic in General Discussion

ELME's largest and most important asset's PSA just got terminated, sending the stock down 22%. Assuming the other 3 sell (which are past inspection periods) and 5% t-costs? very rough here, using @realassetsvaluewriteup as an initial guide 1.80: 8% cap myeh, not much room for upside assuming sale @ some discount to prior contract 1.48 : 9% cap probably have nice upside 1.24: 10% cap back up truck, put as mcuh as you're comfy putting in one building, would have to have something really wrong with the building to not sell above here. any thoughts? -

Good question and, honestly, I can't recall. Somewhat higher than BV which was 14 and change at the time. -Crip

- Today

-

Pleasure. Feedback welcome.

-

God damn it. The gnomes of Zurich are beating us 2-0

-

To our friends on the Democrat side of the aisle, how do you see - in light of Mamdani running the table in NY last night - the rise of the DSA and their attempted takeover of the party? Seems like it is happening. This is the mirror image of MAGA's takeover of the GOP. I never would have predicted that either.

-

Crazy what happens when the news folks stop pumping "things happening" that prompt gambling fools to pile into physical delivery commodities!

-

I bought a little bit of QXO today for the first time. I noticed BLDR was up and it reminded me of this former darling. Ready for that Brad Jacobs magic to commence now

-

ahhh...ok....now i get it, thanks for being upfront about this....

-

Thanks for writing and sharing.

-

What do you think intrinsic value was when you bought in 2017?

-

It is how some institutions trade although less now then when I was on the trading desk at UBS. If there was a PM or mandate change I can see it happening.

-

Tsm

-

Depends. if you are an aggressive seller sometimes regardless of price, happens all the time with institutions you will be willing to act opportunistically on block liquidity when it’s available. Even if your participation on previous days was much lower (because there was no matching block from Fairfax). Plausible scenario: Fairfax raised debt capital and potential sellers were made aware big block is available. also plausible: it was the trs also plausible but less likely: Fairfax not involved at all

-

You are right to be frustrated. Fairfax India hasn't delivered. 11 years is a LONG time. The biggest change I see is BIAL value is meaningfully increasing over the last year. That should reflect in FFI share price sooner or later..

-

That's just not how people trade. 2% of the entire company in one block trade cross. Does Fidelity even own that much? Does Fidelity get credited with owning the shares that I own through Fidelity?

-

Fidelity has been trimming lately. Maybe it was them.

-

That's our nickname for Rich Privorotsky, the analyst who put out the note. .

-

Netflix

-

what exactly is Privo ---he didn't quote Privo or anyone for that matter, so he seemed to be passing off as his own writing.

-

There may be an element of being spoiled by “great annual results” out there, but with FFH and FFHI, there are significant differences. FFH – The company is simply worth more than it’s currently selling for. How much more is debatable, but definitely more. The frustration is not hugely significant, at least from my perspective. It’s more of a curiosity at the manic nature of Mr. Market, offset in large part by the fact that every share I own is becoming a larger share of the company as they use this downturn in price to buy back shares at an attractive price. Over the past several years, the company has performed tremendously well and the share price has followed. Frustration level – very low. FFHI – The presentations by Ben Watsa as well as the quotes from the AGM a couple of years ago, shown above, point to the immense potential of India and Fairfax’ position to capitalize on said potential. I bought into it when starting my position in 2017 at $15/share. To date, capitalizing on that potential has been very slow, and that is very frustrating. Yes, BIAL continues to increase in value each passing day, but if we’d have asked back in, say, Mid-2021, when do we think we’ll be able to monetize that, the majority of the board would have guessed before mid-2026. The company’s holdings have changed here and there but not significantly so in the past 5 years. The pace of transitioning “opportunity” to “tangible returns” has been disappointing. Worth noting that my investing style really is lethargy, bordering on sloth as most of my top 5 holdings have been not only multi-year, but multi-decade (FFH, BRK, MKL, JNJ). Frustration level – Medium, but increasing. -Crip

-

No jokes on me. I was simply putting fwd what I discussed at work and my colleague put this fwd. He did say it was from Privo, I didn't see Privo and posted that part here.

-

Didn't they raise an equivalent amount of debt on June 8th? Perhaps the closing of the TRS has more to do with their ability to access debt markets vs the TRS share price? I really have no idea about their ability or inability to raise debt at this scale or interest rate.

-

LoL who used AI to write it? is AI quote you and goldman used AI to help? or are you using AI and AI is quoting goldman? or are both of you using AI and its quoting another source? or is it the biggest wtf moment of all time lol. Or hell maybe hes lurking on the forum quoting your ass haha

-

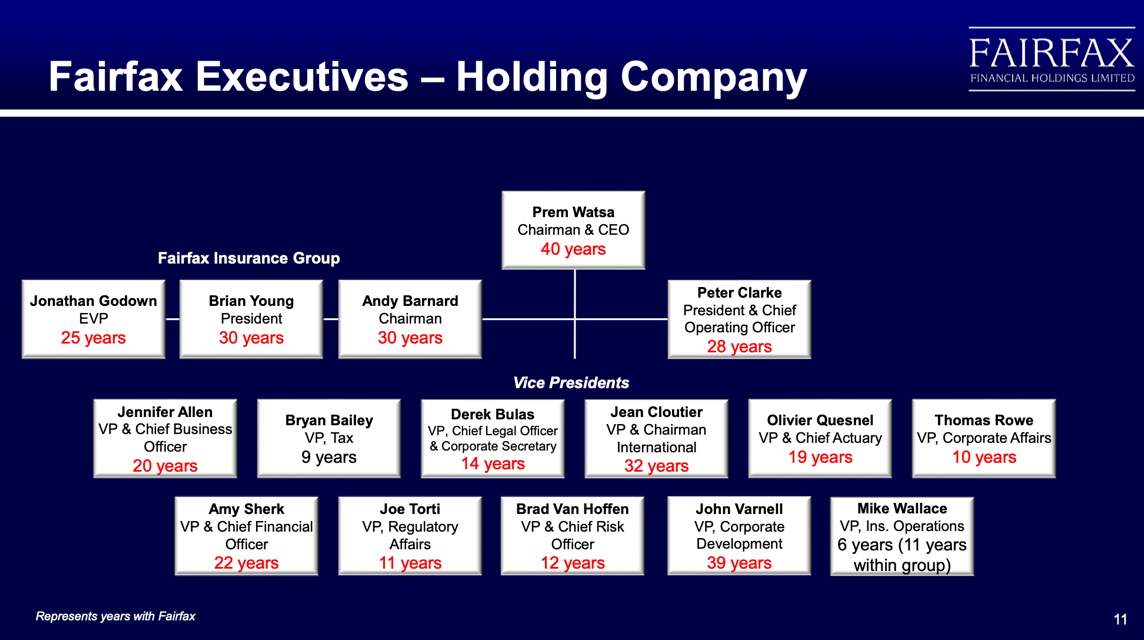

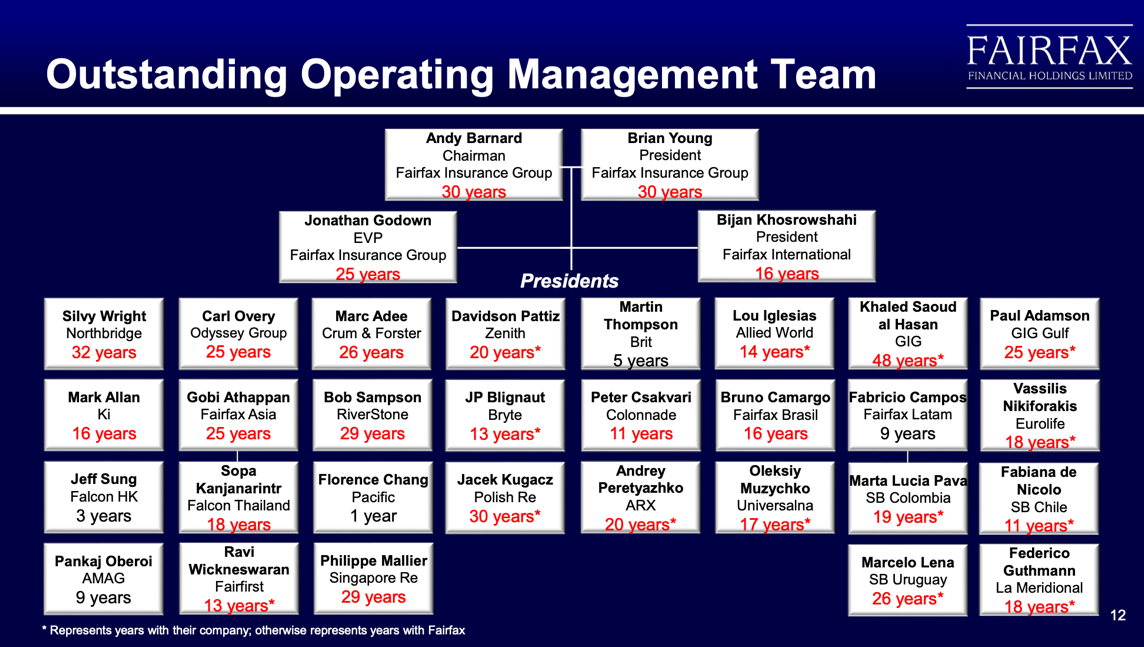

Fairfax - A Deep Dive on Management and Culture

Viking replied to Viking's topic in Fairfax Financial

Article 4 in the series Corporate Culture: An Invisible Asset Investors spend enormous amounts of time analyzing financial statements, valuation multiples, earnings forecasts, and investment portfolios. Yet some of the most important drivers of long-term shareholder returns cannot be found in a spreadsheet. Corporate culture is one of them. Culture is often described as "how things get done around here." It encompasses an organization's values, incentives, decision-making processes, and behaviours. It influences how employees treat customers, how managers allocate capital, how risks are managed, and how organizations respond when conditions become difficult. Over time, culture can become a meaningful competitive advantage—or a significant liability. The challenge for investors is that culture is difficult to measure. Unlike revenue growth, profit margins, or return on equity, there is no widely accepted metric that captures its strength. For Fairfax investors, culture matters because it influences many of the factors that drive long-term shareholder returns: employee retention, underwriting discipline, acquisition integration, leadership development, and capital allocation. Culture Starts at the Top Corporate cultures are shaped by leadership. For nearly forty years, Prem Watsa has been Fairfax's chief steward of culture. He has consistently emphasized integrity, long-term thinking, decentralization, humility, and treating people fairly. More importantly, he has spent decades embedding those principles into Fairfax's organizational structure, incentive systems, and leadership selection. The company's decentralized structure requires trust. Its acquisition strategy depends on allowing acquired businesses to retain their identities and leadership teams. Its compensation programs encourage managers and employees to think like owners. Together, these practices reinforce the culture that Prem has spent decades building. As a result, Fairfax's culture is not simply a collection of stated values. It is embedded in the organization's structure and decision-making processes. Employee Retention as Evidence One of the clearest indicators of a strong culture is employee retention. Talented people have options. When leaders remain with an organization for decades, it often suggests they value the culture, opportunities, and working environment. Fairfax has an unusually strong record in this area. The company regularly publishes organizational charts for its holding company, operating businesses, and investment team. While these charts are intended to show reporting relationships, they also reveal something more important: extraordinary management continuity. Across all three groups, many senior leaders have spent decades with Fairfax or its operating companies. Examples include Prem Watsa (40 years), Roger Lace (40 years), Brian Bradstreet (39 years), John Varnell (39 years), Jean Cloutier (32 years), Silvy Wright (32 years), Brian Young (30 years), Andy Barnard (30 years), Peter Clarke (28 years), Carl Overy (25 years), and Paul Adamson (25 years). The significance is not that a handful of executives have remained for decades. Long tenure appears throughout the organization, suggesting Fairfax has built an environment that talented managers choose to remain part of for extended periods of time. This level of continuity is unusual among public companies and provides evidence of a culture built on trust, autonomy, and long-term thinking. A defining characteristic of Fairfax's culture is its willingness to partner with proven managers rather than replace them. Rather than imposing a centralized operating model, Fairfax typically leaves decision-making in the hands of local leaders and measures success over years and decades, not quarters. The result is an organization with remarkable management continuity—a characteristic that is difficult to replicate and one that may represent an important competitive advantage. Andy Barnard on Culture Perhaps the most credible assessment of Fairfax's culture comes from Andy Barnard. Barnard joined Fairfax in 1992 and spent more than three decades helping build Fairfax's global insurance operations. As President and Chief Operating Officer of Fairfax Insurance Group, he played a central role in developing Fairfax's decentralized structure and expanding the number of profit centres throughout the organization. Because of his long tenure and leadership role, Barnard is uniquely qualified to assess Fairfax's culture. At Fairfax's 2025 Annual General Meeting, he highlighted several characteristics that have defined the organization throughout its history: So of course, we had a fantastic year in 2024, $1.8 billion of underwriting profit. 7 of our companies achieved record underwriting profits during 2024, which we're very pleased and happy and proud to see. (W)hat I'd like to focus on… is the reasons that we've been able to achieve this success. And I'd like to go back to that slide that Prem shows every year… that shows the tenure of our CEOs across Fairfax because I really don't think there is any more important factor behind our success than what that slide reveals. Continuity of management is just so vitally important in our industry as it is in many businesses. (B)ut I think it's especially important in the insurance business. It allows us, over time, to build, to grow, to improve our operations. And we do so without the distractions and the disruptions that come from changes at the top. Now for those of you that might follow the trade press in our industry, you would see amongst many of our competitors, and I'm sort of referring to the global commercial, property and casualty market, which is really the main theatre that we operate in. But for so many of these companies, it's just a revolving door. And it's not just… the CEO. (B)ut it is also many of their key executives. And this creates circumstances that make it very hard for companies to have the stability that enables them to thrive and improve and build and grow over time. At Fairfax, our decentralized operating philosophy, whereby we keep our company separate and autonomous creates a much more favourable, much more rewarding environment for our CEOs and for their management teams. And it is that environment that allows them to continue to build and grow and improve their operations. And that's what you're seeing in the results that we've been able to achieve at Fairfax. And… we've said this many times. We may say it every one of these meetings, we are so blessed. And this gets better and better every year because of that continuity, but we are so blessed with the remarkable collection of CEOs and leaders that we have running our companies. And again, I don't think there is any more important explanation for the underwriting success that we've been able to achieve. Prem referred to our moat, the culture of Fairfax being our moat. This retention of employees is really something that is attributable to the unique culture that we've had at Fairfax: supportive, rewarding, empowering. And that's what's enabled us to have this remarkable duration. I would say if you compare us to any of the major companies in that global P&C world. I don't, think you would find anyone with close to the duration of tenure at the top. And not just at the top, at the very top, but also amongst their senior management teams that you find at Fairfax. Andy Barnard – Fairfax AGM – April 2025 Barnard's comments are noteworthy because they come from someone who spent more than three decades helping build Fairfax's insurance operations. While investors often think of competitive advantages in terms of brands, scale, patents, or cost structures, Fairfax's leaders increasingly point to culture as one of the company's most important moats. Prem Watsa has made this argument directly, and Barnard reinforced it when he noted that "the culture of Fairfax [is] our moat." The evidence supporting that claim can be seen in Fairfax's unusually strong management retention, decentralized operating structure, ability to attract entrepreneurial leaders, and success integrating acquisitions while preserving the people and cultures that made those businesses attractive in the first place. Several themes emerge from Barnard's comments. Fairfax places a high degree of trust in its people. Employees are encouraged to think independently and act like owners. The organization values humility, fairness, and long-term relationships. Most importantly, decentralization and culture reinforce one another. These traits may sound simple, but they are difficult to replicate. Competitors can copy products, strategies, and compensation systems. Culture develops gradually through thousands of decisions made over many years. What This Means for Shareholders Corporate culture is often described as an intangible asset. In Fairfax's case, it may be one of the company's most important assets. Over four decades, Fairfax has built a culture centred on integrity, trust, decentralization, accountability, and long-term thinking. These values have been reinforced through leadership actions, organizational design, compensation systems, and management selection. Culture alone does not guarantee success. Businesses must still compete effectively, allocate capital wisely, and execute well. But culture influences all of those activities. For investors evaluating Fairfax, culture should not be viewed as a soft or secondary consideration. It helps explain the company's ability to attract talented managers, retain leadership teams, and create an organization focused on long-term value creation. Like many competitive advantages, culture is difficult to quantify and easy to overlook. That may be precisely what makes it valuable.