All Activity

- Past hour

-

Am I the only one here who's had a rubbish first Half of the year?

Xerxes replied to thowed's topic in General Discussion

Closing the book on first half of 2026. Overall lousy compared to market index. Oh well …. 2026 H1 => 5.7% 2025 => 24.38% 2024 => 36.96% 2023 => 24.81% 2022 => -11.48% 2021 => 20.09% 2020 => 11.36% 2020-25 CAGR stands at 21%. S&P500 had a YTD gain of 10% in the same period in USD terms, double that of my gain in YTD. -

Am I the only one here who's had a rubbish first Half of the year?

frommi replied to thowed's topic in General Discussion

Because there is no moat protecting these earnings. Barely any semi has a true moat. And the revenue is not recurring, when enough datacenters are built (and because chips are not the only bottleneck) the demand for chips will just stop, as it always has in history. Its a cyclical industry. -

I didn’t try it in the end. I’m a bit like yourself, for me quality of the company is very important. I also think I’m need to know the company too, I’m not going to buy some random bank I’ve never seen or heard of, trading at 0.5 book… or whatever. So just couldn’t see myself ever actioning these types of ideas.

I didn’t try it in the end. I’m a bit like yourself, for me quality of the company is very important. I also think I’m need to know the company too, I’m not going to buy some random bank I’ve never seen or heard of, trading at 0.5 book… or whatever. So just couldn’t see myself ever actioning these types of ideas. -

Thinking more about this - I remember someone wise once said to me that 4 is a big turning point, which I found very true. When your youngest hits 4, it's pretty glorious as you are out of a certain pit i.e. no nappies, no buggies etc. so moving around is so much easier for starters. It's one of the big shifts (followed by the teenage years, which are something else altogether....) So I'm sorry, because you are really in one of those super tough times with 3 under 4. The only other thing I can think - an obvious one - is I hope you and your partner are kind to yourselves and each other - it's easy for parents to beat themselves up about stuff, and worry you haven't done the right thing. It's the wild west out there - we all try our best (when we're not too tired!). Good luck!

-

I did for a month out of curiosity - wasn't really my thing - felt like cigar butts. I prefer quality. Problem is that these are small, illiquid things, so if every subscriber rushes to buy (esp. without reading properly), you've missed the boat. Because I'm a cheapskate, *cough* value investor, I tend to do monthlies on one or two, see as much content, and then rarely continue. But struggle to think of anything like this place, really.

I did for a month out of curiosity - wasn't really my thing - felt like cigar butts. I prefer quality. Problem is that these are small, illiquid things, so if every subscriber rushes to buy (esp. without reading properly), you've missed the boat. Because I'm a cheapskate, *cough* value investor, I tend to do monthlies on one or two, see as much content, and then rarely continue. But struggle to think of anything like this place, really. -

Am I the only one here who's had a rubbish first Half of the year?

73 Reds replied to thowed's topic in General Discussion

The question that comes to mind is, based on current and projected earnings of some of these semi stocks, why shouldn't they trade at current prices? -

@Sweet I'd ignored this thread - thought it was going to be different. I'm so sorry to hear this - I know how incredibly frustrating and upsetting stuff like this (well Parenting is Highs and Lows generally!). Hard to know what to say, but sounds like you've had lots of good advice. I know very intelligent people who started talking quite late, they were just thinking and learning in the interim. I think any reading on either side is a wonderful thing. My best wishes to you and your partner with it.

-

Volkswagen is too dysfunctional even for my taste.I think there are plays in the German industrial sector that are more straightforward in terms of chance of success. MTX was the last one that I bought in decent size.

- Today

-

Thanks - a really great post as always. Little by little I am receiving my education on this industry from you!

-

Nice to read, Mike [ @boilermaker75 ], Great service! - I hope Lyn and you enjoy it.

-

HaHa! - You just made my morning, @aws! Let's hear what you think! ...- Great deep value investment in a ... shiny turd

-

Check out spirit of math too. My three kids are still in it, oldest at the grade 11 level. Less rote than Kumon, more problem solving focus. Highly recommend it

-

Consider Kumon - reading and math. I put my daughter in at age 2 in the reading program. Now at age 4 she can read at a grade 1 level. Will be starting math next month. They are short exercise booklets, designed for repetition and developing focus. Students progress at their own rate. Fosters a great parent bond with the child, but requires patience to get through the daily homework. Would not underestimate what a child can learn. The brain is mysterious.

-

.thumb.jpeg.b0384a4135d041bebd0e39ae144d51f4.jpeg)

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

longterminvestor replied to tnathan's topic in General Discussion

Listened to this podcast, RYAN section only. I'm, self admittedly, a tough critic. They are directionally correct with a few things however they make assumptions that are not accurate. Again, bodes to the thesis that distribution and the consumption of P&C insurance is greatly mis-understood. Property Casualty insurance overall is just mis-understood. There are just mechanics to insurance that are 3 & 4 layers deep that can confuse the highly intelligent investors/buyers of insurance which supports a role for brokers in the digital world for the foreseeable future. One assumption made was "Admitted vs. E&S" and why business flows into those marketplaces respectively. #1 - Every broker is incentivized to place business in the admitted market. Typically, not always, but typically an admitted placement has no wholesaler so theres no split on commission. There are certain niches/carriers who pay as high as 22%-25% commission and as a retailer placing that direct, there is no split with wholesaler - typical commission is 15%-17.5% admitted - E&S varies but 10%-12% net to retailer and 7.5%-10% net to wholesaler (Gross 17.5% to 22% is norm in wholesale + FEES....many transactional E&S policies have a $250/$500 fee in addition to commission that goes to wholesaler - some have $2500/$5000 placement fees). The extra kicker is the contingent commissions paid as well in both scenarios - when retail places admitted direct - contingents go to retailer, when placed wholesale - contingents paid to wholesaler. The reason for "preferred wholesalers" is driven by an arrangement with retail/wholesale where there could be a split on contingents so naturally a retailer will want to load up with 1 wholesaler if the retailer participates on contingents placed thru wholesale channel. Bored yet? Putting folks to sleep? Probably....thats the opportunity...insurance transaction usually just ends with "okay, lets just buy this already and deal with it next year. Its so odd actually. Its true not every retail agency can have the expertise to write up every deal that comes across the desk so naturally a wholebroker is engaged to work on accounts where no admitted market will write OR a retailer does not have an agreement to place with the admitted market who potentially could write that business. But the retailer will not "disclose" to buyer of insurance "Hey, I know XYZ admitted carrier can write this well for you but we do not have an agreement to place business with them so I recommend you call Bob down the street, he can help you and I will pass". That never happens, the retailer will just send deal to E&S market and put a deal together, and if the relationship with client/broker is decent and the price is right - the deal will trade E&S. When a large broker purchases an agency, the first thing they are gonna do is cull the E&S book and see what admitted's will offer terms on whats already there. The accretion on revenue is significant. Recently acquired broker who has $10M of premium spend E&S and getting paid 10% ($1M revenue), if that can be rolled admitted, and make 15%-17.5% or even 20%, that is a large increase in revenue for the recently acquired shop to a favored admitted carrier who has a large relationship with admitted XYZ carrier and immediately appoints newly acquired retailer. In those situations, folks like RYAN, AmWins, RPS, Bridge - will lose - but retail broker/client win. Directionally correct because E&S has been growing significantly over the past 7-10 years. Mostly because the playbook relies on a lazy retailer. Theres lost of follow up and convincing that needs to happen to get an admitted carrier to write "new" business - they just ask lots of questions (they are underwriters...obviously they ask questions). But many times an E&S brokered deal can be put together faster so if speed is the game, E&S is the cure. RYAN, AmWins, CRC have been building an army of sales folks getting weekly meetings with retailers saying "let us do the placement of coverage, you manage the client relationship." -

Am I the only one here who's had a rubbish first Half of the year?

Valuebo replied to thowed's topic in General Discussion

Well, semi's are now 19.7% of the S&P500 and 0DTE's are over half of daily retail volume. Something tells me this won't last. Overall the market is not that crazy expensive but we have earnings growth coming out of our ears through semi's. One has to wonder what would happen in a couple of scenario's that people just aren't willing to put much stock in currently as all capital gets sucked into the same sector, leaving big pockets of the market completely discarded. There is only one prevalent scenario that many currently seems to accept: AI technology will keep improving at the same rate and hardware demand for it will far outstrip supply for the near future. I'm agnostic on it all but I do know semi's becoming 1/4th or 1/3th of S&P500 is likely to be exuberant and not sustainable unless we actually magically get true AGI. Good luck to all participating though. So I kinda wonder what the rational upside from here could be for momentum guys, AI bulls, trend followers, passive investors blindly following the indexes, ... because at some point we reach a sudden stop and people will likely once more be surprised that no bells get rung at the top. I've been selling off most of my passive investing portfolio since a few weeks as I was up nicely for the year, albeit still lagging the market of course. I'd rather hold some cash and specific individual investments than have 20% of my net worth in semi's. I've enjoyed some upside through this exposure but I'll let others bat for that extra sector market cap doubling here! -

Dividend Portfolio for Retirement Income: 6% or higher club

SharperDingaan replied to dipod's topic in General Discussion

Look at Telus. If the dividend is simply kept as is, you will do very well. SD -

Really nothing to do with Trump. The last two Prime Ministers have not been able to live in 24 Sussex, because of rat infestations, electrical issues, massive renovations that need to be conducted, etc. Nothing like the White House that did not need this ridiculous ballroom. Canadians are sometimes too humble for their own good and previous leaders felt bad about spending a large amount of money to renovate the Prime Minister's residence. Carney finally realized this cannot be delayed any further, and it does not look good for the country. It's no different than any historical site that needs renovations. Cheers!

-

6 month YTD return just isn't meaningfull, as todays stella numbers could quite easily turn into shit tomorrow. The key takeaway is what have you done today to avoid losing it if the market turns on you. SD

-

Insurance - The Engine That Drives Fairfax

Maverick47 replied to Viking's topic in Fairfax Financial

Great point! Hadn’t thought about that before, but it makes great sense. -

Insurance Brokers (MMC, AON, AJG, WTW, BRO)

Red Lion replied to tnathan's topic in General Discussion

Maybe they're trying to sail through any type of insider lockup so they can start dumping shares on the market when multiples improve? -

@dartmonkey, i appreciate the feedback. I will be making a few edits to my original based on your comments. Your second comment is bang on. When it comes to capital allocation, Fairfax bought low in 2015-2017. And from 2014 to 2025 they have also been selling high: First Capital, ICICI Lombard, pet Insurance and Ambridge. The sales realized significant proceeds and investment gains… that was in addition to the best in class growth in net premiums written per share they were able to deliver. Impressive. I have a coming article on how they have used partnerships as a strategy to grow their insurance business especially over the past 15 years. GIG is a good example of where Fairfax was the minority partner. Allied World isa good example of where they were the majority partner. What is so impressive about Fairfax is all the different levers they are pulling these days to drive per share value over the long term. Their capital allocation toolbox is full. And they have become very proficient with how they use each tool.

-

Am I the only one here who's had a rubbish first Half of the year?

brobro777 replied to thowed's topic in General Discussion

I wouldn't put myself in da circular file but it really was terrible selling all my ES futures in April for bullshit gains, just to watch it rally another 800 points afterwards. And I also got smoked shorting silver in January, only to see it drop 50 points after I covered Well at least tobacco is outperforming the markets... -

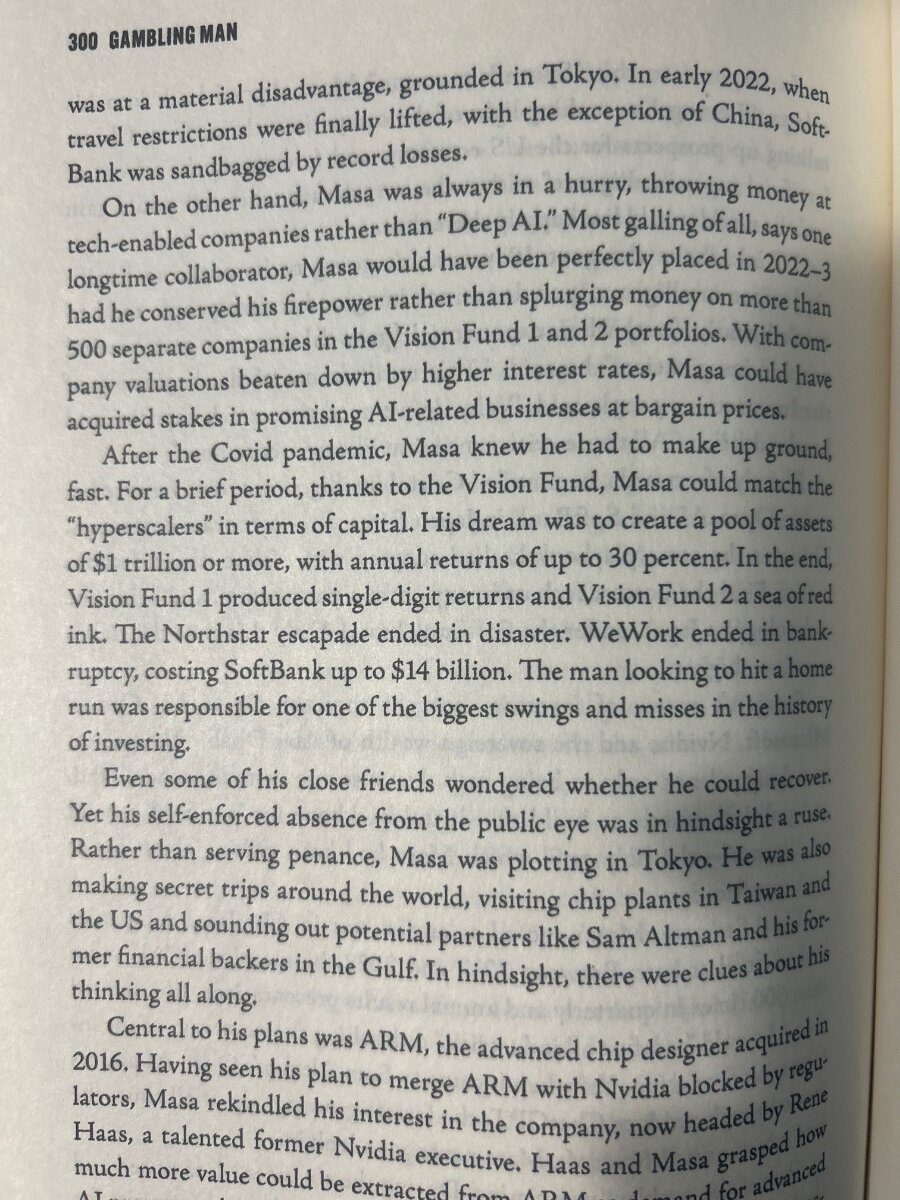

Ultimately Masayoshi Son superpower was not investing, it was his ability to believe in himself and pull on his vast network for the next big thing (I.e investment) It is telling that for someone who mentioned AI hundreds of times in the past ten years in his conference call, his company was not invested in OpenAI. It is telling that for someone who correctly identified Jack Ma as the standard bearer of e-commerce in China, he failed to correctly identify Elon Musk as the standard bearer for the space economy and EV revolution. And instead got carried away by Neumann and WeWork.

- Yesterday

-

Insurance - The Engine That Drives Fairfax

dartmonkey replied to Viking's topic in Fairfax Financial

Your numbers show that all metrics, net premiums written, investments, insurance float and book value, all increased slightly more per share than they did in absolute terms, so your conclusion ("Much of the dilution had been offset through organic growth") actually seems understated. It seems to me it should be "All of the dilution, and more, had been offset through growth." Apart from that nitpick, one other point that perhaps bears mentioning is that Fairfax has shown flexibility not only by buying insurance assets when the market was soft, but also by selling insurance assets when the price was very good. The examples that come to mind are Vault Insurance (2021), the big Pethealth sale (2022) and the life insurance business Eurolife (2025). They also bought the 50% of Gulf Insurance they didn't already own in 2024 (40% from Kipco, and 10% in a squeeze-out of minority investors.) In other words, they have been opportunistic about insurance companies, buying a lot when the market was soft, but also selling some when the market was hard, and even buying some (Gulf) when the market was hard but the strategic reasons were good. -

https://www.barrons.com/articles/berkshire-weschler-stock-davita-sirius-e9ee54aa DVA & the much maligned SIRI had a great first half of the year, plus Delta up around 50%.