TwoCitiesCapital

-

Posts

6,303 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

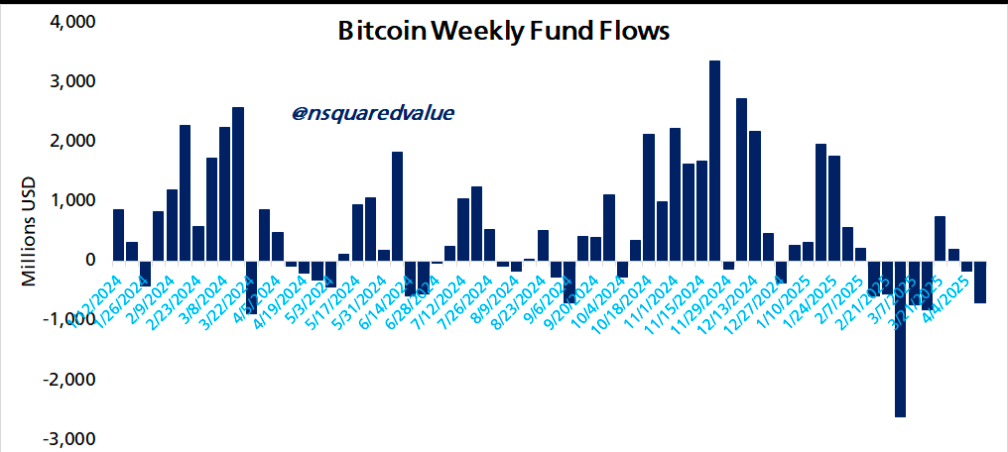

Inflows yesterday were nearly 12k BTC. We're also significantly positive the day before. To put that scale into perspective - the YTD average of all the daily net flows is ~23 BTC per day.

-

You're telling me the value of Meta/Facebook/Instagram is in the computers and not in the social network that was built? The social network is people. Meta just owns the brand that ring fences it all in and limits the ability for others to tap that and profit from it. Bitcoin? No such ring fence. Ownership of the coin gives you access to the network. The network is the individual users - not the computers. Miners and nodes play an important role - but are useless and wasted resources without the people/network.

-

Not sure I'm understanding your question. There are ways to validate how much BTC is outstanding and how much BTC you own? BTC is the network.

-

As of today? About 1/19.5 million It's definitely economically sensitive. The adoption/contraction cycle has been pro-cyclical with BTC price. I expect drops in price to slow the adoption and rises in price to accelerate it. If you zoom out though - the secular trend in adoption is up and not by small amounts. Just have to ignore the noise and the euphoria/depression moods of the market and buy when it makes sense and stop buying/trim when it makes sense. I don't intend to pay higher than $100k this yea. I cut my DCA by 30% when we went above $80k. I stopped DCA'ing entirely above $100k. Started again at the recuded amount when we fell back below $100k. At prices above $150k, is stop rolling put spreads and would start letting shares go in my IRAs. Selling taxable lots hasn't really been decided on yet. I expect the highs will ultimately be higher than that (perhaps much higher ) but also recognize the possibility of the next bear market lows could be in the $100k ballpark or below - I don't want incremental capital dead for another 2-3 years waiting for growth to catch back up so manage my risk this way.

-

Without discounting future growth - just the current network is in the ballpark of ~$60k today. The price with discounting? Depends on the discount rate you use to account for the risks to the outlook. But I expect the network growth trends to remain intact which will result in price growth of ~50+% compounded growth on that price for the next 5-7 years. And because of that, I'm willing to pay more than $60-70k today knowing that it is still the best marginal use of my capital.

-

+1 I use fiat and debt to finance life. I use BTC for long term savings outside of retirement contributions. Eventually I'll spend some of the BTC, but only when the marginal spend affords me significantly improved purchasing power OR when I've exhausted other forms of spending.

-

Because Americans are notoriously bad at understanding math... But I agree with the premise. While the average person won't sit down and do the work to realize the current situation is untenable, nor willing to give up the services that benefit them to make it more tenable, they have 'faith' that the government is operating in a responsible manner and has assets, like gold, to back this up. It doesn't actually matter if its true or not - just that they believe it. Having large stores of gold supports that belief. Dollars are backed by the 'full faith and credit' of the U.S. government. What happens to the dollar when the 'faith' is lost? It's not a bad framework. 'Energy' in general can be a decent store of value through time - though with more volatility than gold given its more industrial use cases. I view energy to be the most effective nominal inflation hedge over short periods of time. You might enjoy Michael Saylor's explanation of Bitcoin just being a vehicle to transfer the value of energy through time with your viewpoint. Oil is priced in dollars. What do you think those oil-exporting countries are exporting? And what do you think the currency people are paying in is for them to receive USD? This has been the agreement since the early 1970s when the US administration made an under the table agreement (at the time) to protect Saudi interests in the middle east in exchange for Saudis selling oil only in USD and recycling the USD in US treasuries to support the currency and bond markets.

-

Time to transfer those ADRs to IB so you can hold the foreign share directly when they dissolve.

-

-

Thank you! That also means the number of "wallets"/individuals holding more than 1 Bitcoin is also probably quite a bit larger than reported too.

-

Question for the more technical oriented - Over time, I have moved BTC I've accumulated to a private hardware wallet in multiple transactions. For example sake, let's say I'm moving to the hardware wallet everytime I accumulate 0.25 BTC and accumulate 2 BTC. Each time, a different address was generated to send the BTC to; however, all is aggregated in the private address viewable on Ledger. So when people are looking at on-chain data, do they see a single wallet of 2 BTC? Or is it 8 separate wallets holding 0.25 BTC? Just trying to understand how my wallets roll up to the broader on-chain data when I see #s and %s of "wallets holding more than 1 BTC" and etc.

-

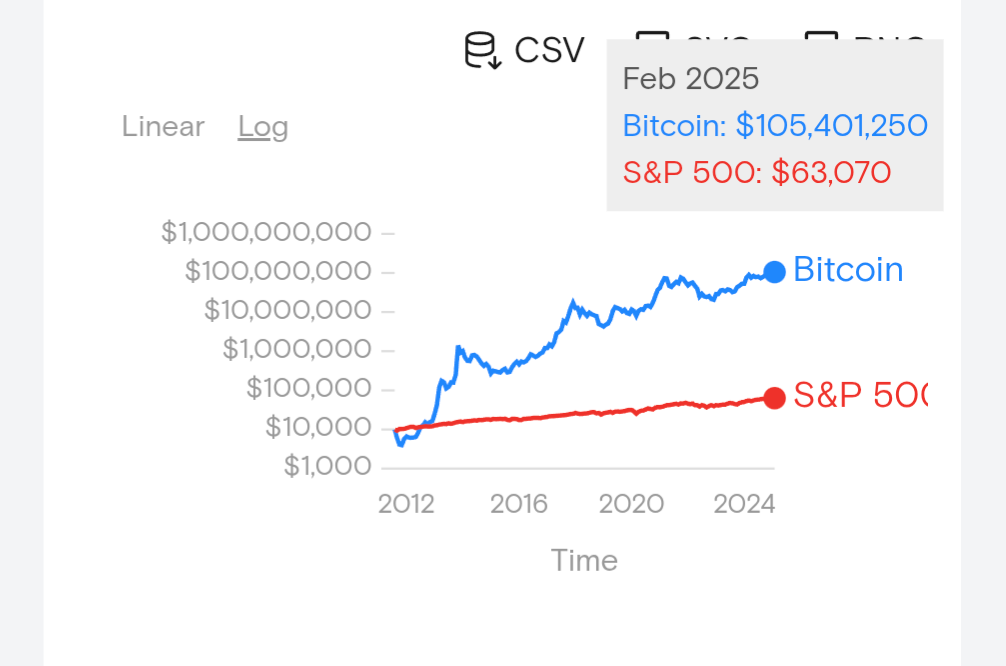

Speculation is $105 million vs $65k on a simple buy-and-hold. What other speculative bubble has that level of out performance over 13-years without popping? If you measure it in BTC ...

-

Question is - which gets abandoned first - gold or fiat? If fiat, gold will still go through the roof before beginning its own bleed to BTC. I keep thinking this is the risk to gold, that Bitcoin will bleed its monetary premium, but Gold is still doing exceptionally well this year in light of BTCs enormous inflows. It seems to me that perhaps fiat comes first and that it may still be safe to own gold awhile longer.

-

Because those investment houses control the flows of hundreds of billions of dollars, if not more, via their recommendations and proprietary models and advice/recommendations. It doesn't all flow immediately, but Blackrock allocating 1-5% to this in their strategic models is ABSOLUTELY going to influence flows in that direction. And when those flows are going to accumulate a minority of the 19 million BTC currently available? It's likely to drive a price response that is going to last secularly for decades.

-

Elon Musk may not be a white supremacist, but he is continuing a line of failing to condemn/distance from white supremacists while dog-whistling for them. We have dozens of examples of this under the Trump administration from both times around. I have an autistic brother. He doesn't Nazi salute. Any body with eyes knows what they saw and doesn't need to make excuses about it or blame it on his Asperger's. The man is a certified genius - there is no way that was accidental or unintentional. The movement in no way conveys 'my heart goes out to you' and is dramatically different than the motion he did in Asia for the same line. He knows what he did and he did it intentionally. I don't know his personal beliefs. I can believe the Nazi stuff is overplayed and exaggerated for what he did. But I can also believe a wealthy white man from apartheid South Africa who is claiming genocide against white farmers doing a Nazi salute isn't something that should be so easily dismissed. I also believe there are consequences to your actions. Isn't the Republican party supposed to be the party of individual responsibility and voting with your dollars? It would be nice to see them acknowledge that what is happening is just those sMs principles instead of pretending this a baseless witch-hunt from the left.

-

I'm trying to hedge a recession and high US valuations. Getting 4+% in intermediate treasuries and 5-6% in govt guaranteed mortgages that I can lock in, while inflation is currently well below those rates, seems a decent proposition to me - even if I'm wrong about a downturn. But I DO expect rates to go lower. I expect a lot of noise in yields until an official recession is determined/employment continues to decay. At that point, the Fed can cut, the term structure can assert itself, and money flows out of risk-on assets and short-duration instruments at 0% to intermediate treasuries yielding 3-4% bringing those yields down. Even if 20-year rates only drop from 4.5% to 3.5% - that's gonna get you somewhere close to a 15+% return, plus coupon, in an environment where nearly all else is negative.

-

Where do you instead? Europe? Japan? China? All have worse finances and worse demographics. US treasuries may suck, but for anyone required to own bonds they're still the cleanest of the dirty shirts. You can manage the risk and massively outperform the benchmark by being short duration, overweight credit, and time the fixed/floating weights, and etc. but you HAVE to own bonds. And if US bonds are in a crisis... everywhere else is likely worse.

-

+1 I haven't dug into their maturity disclosures to know if they're barbell'd - but it isn't a bad approach to get the higher yields a the front end with a leveraged inflation kicker. In Q4, they disclosed losses on treasuries and Treasury FORWARDS. Perhaps futures/forwards is how they prefer to add duration instead of cash bonds themselves.

-

Would increased issuance be BULLISH for European bonds? I'd think the opposite. Agreed treasuries are losing some luster. The writing is on the wall that the US will default. Probably implicitly via inflation, but not acting as the hedge they once were. Still outperforming stocks and still getting 4-5% YTMs in intermediate core bond funds though which I'm not upset with going into the current environment. Surprisingly, I'd say Bitcoin has held up well. Has been the recipient of some still appreciable inflows through this volatile period even if it's not bleeding as much into upward price movement. Is probably why it has tanked as much as you'd expect from "leveraged NASDAQ exposure".

-

We literally cannot do that while demanding the US $ be the reserve currency and currency of global trade. Even with massive deficits where US consumers send $ abroad to be recycled back into global trade and Treasury bond denominated reserves, we have a shortage of dollars any time there is a whiff of crisis. What happens when US consumers are no longer sending net dollars abroad? Under the current monetary regime, we basically HAVE to run trade deficits which, in turn, funds our bond issuance/fiscal deficits. Without trade deficits, there is significantly less demand for treasuries (higher rates) and structurally higher costs for the same quality of living in the US. Neither is going to be good for bonds/stocks/corporate profits.

-

Or on imaginary fentanyl. Or on bringing jobs back to America. Or on anything that the 'reason' has evolved to/from over the last 2-3 months. Trump's ONLY tool is chaos. He creates chaos and then hopes to climb the ladder for a slightly improved position as people scramble. It's a poor strategy with tons of collateral damage and destroys goodwill - but is what will characterize the next 3.5 years just like it characterized his first term.

-

Once the Fed starts cutting in earnest, term structure will force longer term yields lower. I don't know where the bottom is - I don't think it's 0.25% like it was in 2020. But sub-3% seems doable in a recessionary scenario. And I'm waiting for 3% before meaningfully reducing my duration - but have been sweeping daily P/Ls from bond funds to equity funds over the last week or so.

-

It is cheap, but illiquid, and gets creamed EVERY time there is a market pullback as a result. Anyone forced sellers/motivated sellers drive the price through the floor. Same thing on the upside though - buyers drive the name up bigly because so few shares are for sale each day. I had a few stink bids out to rebuilt the position I sold between $1 - 1.15 last year. Got a decent fill today to get a slug of it back and have more outstanding if we keep going down from here.

-

While Fairfax may have some opportunity on the equity side, I'd be most excited to see them rolling treasuries into corporates when spreads blow out. That locks in a yield advantage for years where the equities contribute to volatility of earnings in a way that bonds likely won't in the future.

-

How much are you down since the inauguration?

TwoCitiesCapital replied to Sweet's topic in General Discussion

You know - for a topic that is of zero interest to you - y'all are spending too much time posting in it.