TwoCitiesCapital

-

Posts

6,408 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

The P/L - less financing fees - is settled either monthly or quarterly (I can't recall which). All of the profits they've made have already been booked and taxes paid except the most recent 1- or 3-month period. Typically, either party could end the contract at any given settlement date. Fairfax has the option to discontinue the swaps basically at any time. Depends on what your objective is - minimize taxes or maximize exposure to your own shares. The TRS allow exposure to the Fairfax shares with only 10-20% of the required notional paid. The other 80-90% can buy more shares....but yes, you'll pay more taxes.

-

The hard part is the logic makes sense, but it's not uncommon for new index additions to underperform while new index exclusions outperform which defies the logic. People front run news. I agree, but ultimately the impact might be too small to notice. For instance, suppose in 2027 we average 1.7x book, and in 2028 we average 1.8x book, and in 2029 we average 1.9x book. But they're averages - so there will be plenty of time above, and below, those levels through daily variations in share price. It wouldnt be crazy to think we could be at 1.7x and 1.9x at varying times in both 2027 and 2029. So are you even going to notice the rising multiple? Is it going to be a trend you can trade? Or should we just ignore the average multiple and focus on earnings, earnings growth, and trajectory? I think the latter is going to be more meaningful and we can simply ignore any supposed fluctuation in the multiple unless if it trades beyond the edges of reasonability.

-

For some of us, there's Bitcoin. For others, there's nature's pocket.

-

President Trump every time he sees a member of Congress insider trading: "You're lucky I'm president." President Trump to every oil and defense executive: "You're lucky I'm President" President Trump to every criminal he pardons after they donate to his campaign: "You're lucky I'm President" President Trump to his kids every time he passes them government contracts: "You're lucky I'm President".

-

Is Europe becoming uninvestable?

TwoCitiesCapital replied to lnofeisone's topic in General Discussion

So....Europe is getting its own NSA? Or have they stopped doing that in the US? Because this is sooooo 2013 -

And Bitcoin is A LOT easier to get a hold of than a second passport.... This has happened in every bear market. And hash rate falls as high cost miners capitulate. It hasn't marked the end of Bitcoin in the past - it marked the end of the bear market. And the secular, multi-year trend is still up even if you get these blips of has reduction. As pointed out previously, despite the 50% decrease in BTC price AND the 2024 halving AND the rush to AI compute - there remains more hashrate today than 12- or 24- months ago even if it's below the October high. They've run simulations where they'll allowed autonomous AI agents to determine how they'd beat want to store and make payments. In those studies, ~50% of autonomous AI agents landed on using BTC at a multi-year store of value without any direction, input, or suggestion. All other options made up the remaining 50% with no single one coming close to BTCs dominance. Stablecoins where the preferred rails for micro-payments by ~50% of the AI agents. The future is crypto/digital.

-

....yes. Gold came out of the ground backing currencies and that's what gives it value. Or biblical societies were directed by God to mine it and that is what gives it value in 2026. /Sarcasm I'm not even certain its correct to characterize this as a "second order question", but obviously the above is ridiculous and you haven't stopped to ask yourself why gold had value, why biblical societies used it, how the world collectively landed on it's use independently of one another and how it ended up backing the USD to begin with. But that's ok. You don't care about stores of value or economic theory or why it's important to have a stable money - so probably not worth your time to ask those questions.

-

"total failure" 'sToNkS'

-

By removing a stipulation of a minimum threshold of time, all you're saying is that "anything that can go down can't be a store of value" which would exclude everything....gold, t-bills, USD. Because it IS possible to have an unrealized loss in any of those items after the point the of acquiring. Having a reasonable minimum threshold for a period of time we're measuring the storing of value across allows for that natural variation in each while still holding them accountable to inflation resistance over an intermediate/longer term. Gold is highly volatile. It was up 50+% at points last year and is down 25+% from that peak. Obviously it wasn't a "store of value" for anyone who bought int he last 2-3 months...but its intended to be a "long term" store of value. Not a store of value over 2-3 months. And over rolling 5- or 10-year periods, it tends to do a decent job. Bitcoin isn't any different - but is more volatile at this time given the emerging nature of the technology, the perfect inelasticity of its protocol, and the lack of understanding of it by market participants/speculators. Like Gold - any short-term period can deviate from that "store" narrative. But over rolling 3- or 5-year periods (cuz rolling 10- doesn't provide much observation yet...) it has worked pretty well over the majority of those varying time periods.

-

-

Lol @ interest in the bank How much has that paid over the last 15-years compounded? I'd love for you to do the math. Meanwhile, good money vs bad money in pictures 2018 drop felt large. It barely registers on the graph. 2022 felt large - now looks rather small. 2026 feels large - and in 10-years will look like 2018. The lack of any sort of intellectual rigor or honesty here to simply set up straw men arguments is absurd Fiat is "bad" money by most any monetary definition of the things that define what makes money. 1) Acceptability/Fungibility? Take a look at global reserve. Becoming less and less acceptable by the year for the last 20-30 years. 2) Divisibility? Had to convert to digital to be competitive. 3) Durability? Paper money wastes away. Digital money transactions can be reversed/deleted/cancelled. 4) portability? You ever tried to carry 50-100k of cash? Again, have to convert to digital and still get bank limits, fees, permission/censorship, and delays in processing as a result. 5) scarcity? Don't hold your breathe. They print billions daily out of thin air. I'll take the non-inflationary, permissionless,fast, cheap, self-custodied real deal all day.

-

"Tells me everything I need to know" that you're ignoring the entirety of economic theory and historical observations of people spending 'bad' money before 'good' money.

-

I've transferred value on the BTC network on many occasions. But never to dispose of it. The network exists. The transfer protocol exists. The fees are low. The settlement near instantaneous. I didn't wait 90 minutes, pay a $20 fee, nor seek permission to spend my own money when doing it. I don't need Porsche to accept a payment for a new engine to prove that concept for me. It would strengthen the medium of exchange argument of Porsche accepted it, but we're still not there yet... And bears would ignore it even if Porsche did just like you're ignoring it that Ferrari does. People can't even agree that it's a store of value which is still step #1. We're still early and there's plenty of time for it to be adopted as a medium of exchange and unit of account next.

-

I've long since said it will be 1) a store of a value before it becomes 2) a widely accepted medium of exchange. Secondly, if you believe one money is rapidly becoming worthless and another is gaining in value rapidly, why would you ever get rid of the rapidly appreciating one just to prove a point to anonymous strangers on the Internet who will find a way to ignore it even if you did? 3) Buckeye made fun of Ferrari accepting BTC above as if it isn't an important use case. Here, you're making fun of me/Porsche for Porsch not/me not attempting. Bears don't get it both ways. Either a car company accepting it ilfor a large purchase is a meaningful metric, or is not, but you don't get to use both acceptance and non-acceptance as bearish arguments for BTC use cases

-

Reads story about debit transaction failing, getting permission from bank for debit transaction, it still failing, arranging wire transaction, paying fee, and still having to wait 90 minutes only to conclude it was Bitcoin that was problematic because I'didn't desire, nor attempt, to use it What an upside down world we live in... To everyone else reading this, on either side of the debate, is it just me or are the bearish arguments against just getting really weak and poorly supported?

-

Biggest holdings are Fairfax, Fairfax India, Exor, Bitcoin, Prosus & Alibaba, and Molina Healthcare. All have been miserable to flat YTD. My small names have done well, but not well enough to offset the drag from the big ones. Am like -7 to -9% YTD pending which days I check.

-

"No one." "very, very few".

-

"no, Neo. I'm trying to tell you, when you're ready, you won't have to "

-

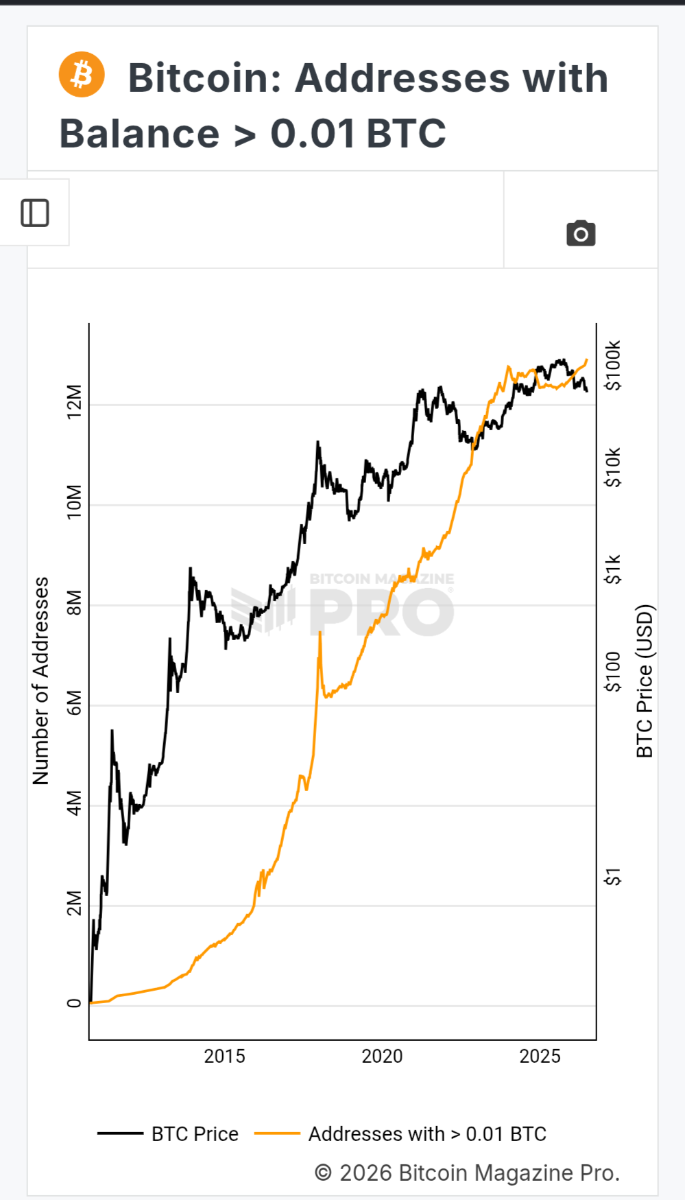

Reading comprehension not a strong suit? It may not be. But I see no superior alternative at this point and Bitcoin is the first thing that has come around that has been superior to gold in just about every way. I don't think it's "easy" to do this. I still think you're looking at this from a 1) short term 2) Western perspective and 3) focusing on a very limited subset of Bitcoin's capabilities. Longer term - fiat depreciates without exception. Bitcoin is volatile, but has demonstrated near constant appreciation over intermediate and long duration periods since it's inception. Dramatic appreciation. Relative to fiat. Relative to real assets. That growth will slow - but ANY appreciation is infinitely better than constant depreciation. Outside of the Western perspective, inflation isn't limited to 2-4% per year, or 7-8% in an inflation shock. Your monetary value erodes monthly, or the money is confiscated by the government, or your subject to US sanctions that tank your economy/currency, or your unregulated banks fail, or it gets stolen by gangs/thugs/politicians, etc etc etc Having a hard money that retains/grows over time, is permission-free and censorship resistant, self-custodied, and readily transferable globally are all exceptionally valuable qualities to have basically every where in the world - but more so in developing nations. Agreed. But I think we're seeing societal level changes. People were angry enough about the status quote to elect billionaire felon, rapist, pedo-associate and known-shyster to the White House because they were fed up enough with the status quo to believe whatever he told them about making it better....before making it worse...a second time. It won't let me attach charts for some reason, but are you not looking at wallet addresses with > 0.01 BTC in them or BTC held by ETFs or hash-rate? How could you look at this over 1-, 3-, 5-, or 10-years and claim there is no adoption and use that as evidence against BTC? Because TwoCities believes in selling worthless money before his valuable money and doesn't like selling things when they're down 50% regardless of what we're discussing. I didn't ask. Wouldn't be shocked if it was a no. But they also don't accept PayPal, Venmo, or Zelle which hasn't stopped those being from being widespread forms of payment in the economy. Why would that also have any implications for BTC at this time?

-

Yes. Because those are both still true? You can still buy the same houses, in the same time, overseas with Bitcoin ? It just might require more Bitcoin now given the price movement? But that isnt an indictment of its ability - it's a reflection of the current market price? Additionally, Bitcoin hash rate is down from the peak, but still higher than mid-2025 or the start of 2025 so YoY is still up and more secure than 95% of its existence? So why are you claiming these are somehow different now in June of 2026? No. You just simply haven't stated what's changed to suggest this benefits are no longer present? Still true. It takes 10 minutes to use Bitcoin and send it anywhere. I just paid $30k to a Porsche dealership in Ohio. Guess what? They don't accept PayPal, Venmo, or Zelle. They do accept debit, but my bank blocked the transaction for being above my $20k daily allowable limit ...you have limits on how much of your own money your allowed to spend BTW. Even when I asked them to raise the limit I was told 'no'. So I tried to run $20k on my debit and $10k on my credit card and just eat the processing fees - bank still declined the $20k debit. So I had to pay $20 to wire the funds and then sit in the dealership for 90 minutes while waiting for them to confirm receipt of the wire. Whole ordeal took nearly 3 hours just to make a payment... This is how the traditional banking system works. You require 1) permission and 2) time to spend your own money. And even when you have both, the bank can still fuck it up. Had I wanted to spend Bitcoin, and the dealership open to receiving it, I could have sent the hole amount in 10 minutes for pennies and saved time, fees, and headaches. It's not why I invest - but I can see the benefits to people in under developed markets. I have a hard time I understanding why having global demand would be a bad thing? Or why recognizing the perspective of others is a negative? No - was just a point that Bitcoin is still spendable and being accepted for large purchases because your post implied something had changed there? I'm still not hearing anything supporting your claims of the change that is occurring to remove the benefits that have long been demonstrated? This is a strawman - it wasn't proof it would work out great. It was simply demonstrating that the characters of a handful of involved individuals doesn't detail a thesis for an entire industry. You should probably spend that time in the sun. It's pretty clear that your comments about things having changed were empty and your relying on price confirmation bias instead of an actual developed thesis and evidence

-

With the note that I've been TOO bullish in thinking the 4-year cycle was broken.... I'm still not certain that this is the traditional bear market. Prior bears have taken us down 70-80+%. Here were sitting at ~55% with multiple sentiment, volume, and pre-based metrics flashing similar signals to prior major bottoms. It could be that this is a mid-cycle correction a-la 2019. Prior bull markets have had multiple 50+% pull backs, but were both more violent/fast to the upside and downside than this one has been. If it's true that secular adoption has broken the prior 4-year cycle and volatility continues to moderate, then an extended multi-year bull market with a handful of 40-50% pullbacks COULD be the path instead of the prior violent up/down BTC has previously done and this could simply be the first 50% correction in what is a longer term bull market with new highs to be expected in the next ~12-18 months.

-

I'm curious as to what 'benefits' you feel it's failed to deliver on? On why 2026 is different in this regard than say ~2021 when $60k was a euphoric bubble top ...but now is sign of death? I dunno about half way around the world - but I expect I may do something like this halfway across town in ~2-years. Ferrari started accepting it too - and it's not because nobody was asking. I think it's funny that you think there is an abundance of Boomers or Gen X in this trade It's been around for 15-years and I still have Boomers/GenX ask me what it is before dismissing the response 30 seconds later. Unsavory characters are everywhere. xAI/Musk don't strike me as bastions if integrity, but nobody is suggesting AI is a scam because of his involvement.

-

+1 Love to see it. This has been the thesis since I first found the company in 2012 when they had a single producing royalty, $200M in cash, and a hopeful Kami development. The path didn't end up quite that simple and the progress was hidden for years behind share issuance/debt service for the Potash royalties and a weak commodity market in general until 2021. It still seems under followed and under appreciated - the share price took days to move following the sale of the gold royalty for an amount that was a significant chunk of the market capitalization of the whole company. And it took weeks more to appreciate the reinvestment of those proceeds by taking out Lithium Royalty corp. Plenty of opportunity in this name to buy AFTER the news has been announced and I had added after both. All that being said, I reduced my position by ~10% last week. Altius has been the only name in my portfolio performing YTD and all other names are flat to down over a 6-12 month period so took some off the table near ATHs to buy other names.

-

I wouldn't say they're anymore dangerous than futures which are also available to retail. But is dependant on how much leverage the provider allows. Coinbase gives me perpetual swaps on Sunil leverage ratio terms to normal CME futures. But there are other crypto exchanges that have historically offered 100:1 leverage which is dangerous regardless of what you're trading.

-

Is Europe becoming uninvestable?

TwoCitiesCapital replied to lnofeisone's topic in General Discussion

I think what most people are missing with the Europe vs America wealth debate is that Europe doesn't get to print infinite amounts of paper money out of thin air to buy global goods/assets/products with. At least not anywhere to the extent the US gets to. Every second the USD remains the reserve currency is a second that were trading something that is largely worthless and getting something of real value. Every fiat currency does this, but being the global reserve means we get to abuse the shit out of it. That small benefit across every int'l transaction every day for decades adds up.