TwoCitiesCapital

-

Posts

6,302 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

I joined the HSA committee to provide investment expertise on their line up. I was part of a single meeting before the whole committee was disbanded and responsibilities handed over to non-investment professionals in HR using some third party consultants

-

How much money did hedge fund managers spend fighting court cases and wooing Trump during his first admin? Preferred also went up to ~$20ish (on $50 par) his first term before cratering to $2-3 afterwards.

-

Perhaps. Though IMO the introduction of hundreds is increasing the risk BTC only for the long term IMO.

-

All announcements have been full of hype and unrealistic timelines and limited on details. Until there is a resolution of the net worth sweep, lawsuits, and existing common/preferred, why would anyone give these companies additional capital simply to watch it get swept to the government's side of the ledger. Before an IPO is possible, there needs to be resolution to the lawsuits/3rd and 4th amendments. Those details are the only thing important for current shareholders - everything else is hype and hearsay.

-

+1 Have never been with a company that had decent options for their 401ks or HSAs. Most are entirely active funds with few-to-none passive index options. None have ever allowed single stock picking. And then some entirely eschew alternative allocations like Gold. In my current one, I have a ton of options for actively managed US large cap, but only a handful of options on small/mid/intl. No possibility for gold. Fixed income is only core bond funds or what is essentially bank deposit - no money market, no emerging market debt, no corporate only, no short term bonds funds, etc. And this is a financial services company!!!!! Is all very limiting. Part of the reason I've opted to roll 401ks to my IRAs when I've left companies in the past

-

Yup. This wasn't necessarily needed. Fidelity has had the ability for their employees to buy crypto in their 401ks for a few years now. But most 401k providers weren't that progressive and were concerned about the potential liability from a fiduciary standpoint. Now that it's been formalized, that removes one roadblock but not necessarily others - like risk/volatility associated with the asset class, fees for providing it, and suitability concerns. I think we're still several years out from most 401ks having this and actually think that's probably a good thing given that they're not associated with professional advice and any Tom/Dick/Harry shouldn't be gambling the entirety of their retirement on things they may not understand.

-

I dunno - he's gonna have to distract from the Epstein stuff again when Congress is back in session in September. India might prove to be a nice distraction. +1 Indian economy is pretty insular as is. I wouldn't expect external forces to have much impact at this time.

-

Yup It was pretty clear just from tallying obvious items that $90-100 in economic value was on the table. But then adjusting for how that gets accounted for, taxes, surprises on insurance (positive or negative) etc was clearly going to bring the number down - not difficult, but is just more work. I'd argue the top number is what matters and is easier to get to - who cares what is reported unless if you're the analyst guessing.

-

I don't think it's a 'complexity' issue as much as it is laziness. Fairfax has different investments accounted for in different ways - market to market, consolidated, and equity accounted. One has to follow each and know how each flows through to understand to the true value vs what is reported. And also have to follow the larger ones, at minimum, casually to know how they may be expected to flow through in an upcoming quarter. None of it is complicated - but it is significantly more work than what the analysts would have to do for an insurer that simply owns corporate bonds.

-

Thinking maybe they rally a bit later this year? Perhaps another pump if/when the Fed cuts in November? Particularly if Uptober in Bitcoin holds. But outside of speculation based on easier money, I expect they'll keep bleeding to BTC with only ETH as a potential to hold its ground (and maybe gain) against BTC since it's relative performance has been abysmal and it has similar secular factors in its favor here in the short term.

-

I'm a little disappointed too. That being said, that was as of June 30th. Always possible the "trade" is put back on now that the last three months of labor data is screaming. My only guess is that they expect long rates to rise as the front end comes down - which would be consistent with the last cut. But the last cut occurred before labor market deterioration, so I am skeptical it happens again. That's really the only reason I can see for them reducing it now. Trump replacing Fed chairs with 'yes' men would absolutely be a reason for long rates to rise.

-

We'll see. People have been calling for alt season a long time, and have basically been wrong every time so far. Bitcoin dominance is still very close to its local highs and has been in an upward trend, again, since it's 'correction' last month. I'm not saying there won't be an alt season again, but I expect if anything is different this cycle it is that piece. We will likely NOT see a repeat of 2021s alt performance runs or anything close to it. BTC/ETH having ETFs, and treasury companies, are getting capital via those markets that will NOT rotate into alts. This will be a secular advantage. While alts might have temporary blips here and there - I expect the downtrend relative to BTC and ETH to be persistent. If others see that, it's gonna keep any alt season relatively muted as a smaller % of capital rotates and the amount that does will be for a quick buck.

-

Impressed that they got the price they did on repurchases, but disappointed at the size given what discount % that would have represented. Maybe they're conserving cash until the results of the IDBI auction?

-

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

AI won't fail to deliver. It probably won't even fail to meet expectations. It just won't do it tomorrow which will be the problem. The Internet was everything they said it would be and more. There was still a popping of the Internet bubble. The revenues that get written off massively exceed the profits currently being booked. The saving grace is the write offs occur over years while the profits are booked immediately. The dynamic of profits outrunning the depreciation can only exist for as long as the profit growth allows it to outrun the fractional depreciation. The moment profit growth slows/stalls is the moment depreciation catches up. -

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

1) stocks are longer duration than bonds and have demonstrated an inability to raise revenues/profits as quickly as rates. This is why they do worse than bonds in historical inflations 2) right now bonds are yield more than inflation - stocks not so much. Bonds have a better starting point because the growth hasnt been there either but the rising rates have. This is likely to help their relative performance. Particularly for shorter duration bonds (1-5 years). 3) there are plenty of options within bonds - short duration bonds, floating rate bonds, bonds with a larger credit spread buffer, CEFs at NAV discounts and double digit yields, TIPS (for longer duration hedging), etc. It also doesn't take much trading expertise to be in short duration bonds when inflation/rates are low and accelerating (2021) and move to more intermediate bonds to lock in higher yields as rates/Inflation moderate along the way (2023 - 2025). All depends on the growth rate. But in a flat or negative growth environment, I'd gladly take 20x guaranteed over 30x after having been wrong about my projected growth rates for 5 years. -

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

There are periods where it is acute and periods where it is low. Stocks, along with most investments, do well when its low and terribly when it elevates. That doesn't mean stocks are an inflation hedge - it means that leverage and productivity in the low years have been able to outrun the few bad periods we've had. But that doesn't mean bad periods don't ravage those returns when they occur or that bad periods will remain few for the next 20-30 years. It's possible. I'm skeptical the growth will be enough, on average, to fill the current multiple expansion as well as providing attractive forward returns in excess of the 5% already being provided in fixed income. The market might think that. I tend to think that earnings have already stagnated and we're beginning to see some of the weakness that has been under the surface in the labor market. Tariffs are a consideration as well - they dent consumer spending if passed through to consumers. They'll probably dent some corporate margins if eaten by the companies. My point about large the large distortions due to this AI gold rush stand. NVDA alone declared $70+ billion in earnings this last 12 months (which still wasn't enough to get real earnings growth vs 2021!). But it's $140 billion of revenue is largely going to be written off as depreciation by other companies in coming years. And that's true of ALL of these chip companies currently wallowing in cash. That's a hard dynamic to outrun the moment earnings growth peaks for these AI chip cos. Same. My equities have largely been asset plays at discounts in foreign countries and opportunistically purchased in drawdowns. Things like Exor, Fairfax, and Prosus have done well outrunning broad US equities for me and we're largely purchased based on discounts to NAVs. I'm not so ready to discount leading indicators, yield curves, and the decline in real earnings we're witnessing. Valuation in 1982 were unusually low (single digit P/Es) after the miserably inflationary decade of the 1970s. 1982 was coming OUT of the third recession in a decade. Leading indicators were turning up, unemployment was high and falling, yield curve was steepening. In other words, the bar was low for outperformance. None of that is true today. I don't expect the a similar experience as a result. They don't need to crash. They could simply replay 2021 - 2025. An earnings drawdown similar to 2021/2022 - either via recession or another spike in inflation - and 4-5 years for corporate earnings to recover to their prior real and nominal peaks like we're witnessing now. The end result of that is that real earnings basically went nowhere for a decade. Is that the type of environment people are excited to pay 30x earnings in when bonds were paying 5% the whole time? -

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

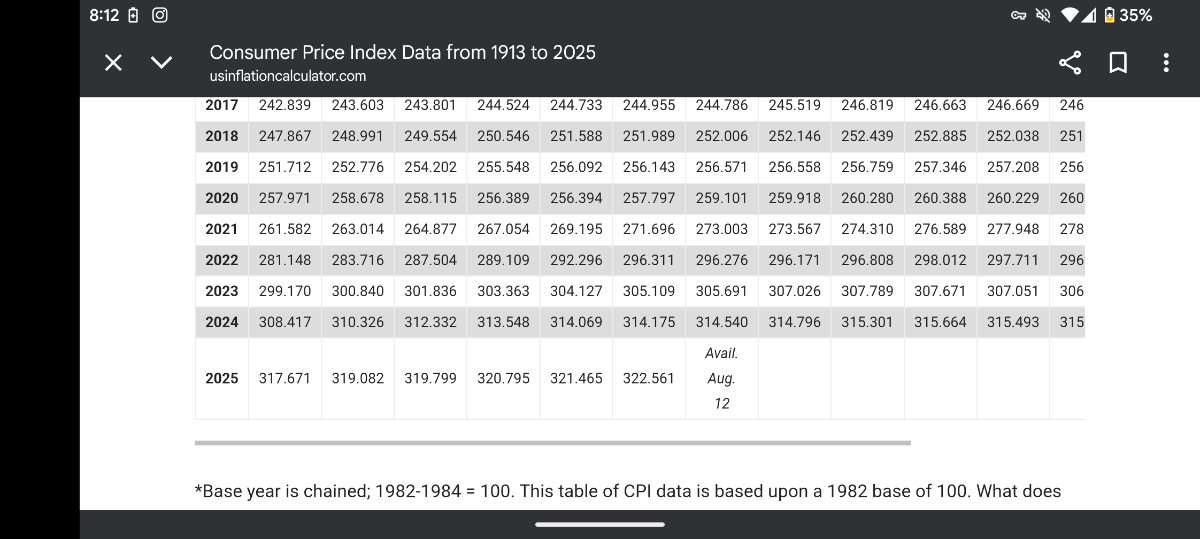

That's just not true Q4 2020 was barely higher than Q4 2019 in terms of overall price index. It wasn't until 2021 that price indices accelerated At this point in the conversation, I've provided charts, graphs, data all supporting my point - a point I've consistently held since 2021 and which the data has been bearing out. All you've provided is an opinion and 'line go up' (but not up as much as true inflation hedges nor supported by fundamental improvements in earnings). Unless if you have something of substance to debate, I think we're done here.

-

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

I didn't cherry pick a start date, Greg. I picked the last 5 years since the inflation shock started in 2021. You're hard pressed to find any date in the last 5-years on those charts that was higher than 2021. That's not cherry picking, Greg. That's a secular theme of stocks underperforming true inflation hedges. I'm sorry your ego prevents you from seeing that. Yes. I do expect multiple contraction at some point. It hasn't happened yet. Sue me. I own that the timing has been hard. I've made returns elsewhere. People used 0% interest rates to justify elevated multiples for a decade. We no longer have them and multiples are even higher.l and people are now justifying it by saying stocks hedge inflation - which clearly they havent. Not in the 1970s and not today. While contraction hasn't happened yet, I find it an even thinner argument that it'll never happen or multiples will continue to expand into infinity which is largely what YOU need to happen to be right at this point since real earnings growth is non-existent, multiples are stretched, and bonds have a significant advantage on starting yields. Because we're picking an asset that has widely been recognized as an inflation hedge for decades and comparing its performance to the so called "inflation hedging" abilities of stock generally. Why is this so hard to understand? DCA'ing gold probably still did better The crux of your entire argument here is "why are we limiting the observation period to an inflation shock and comparing to other inflation hedges when discussing relative inflation hedging performance" -

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

Would go even further to say this chart is inflated itself - because names like NVDAs revenues/profits are CaPEx of other companies. So every $ of revenue/profit NVDA is booking today is going to be written of via depreciation over the next 3-5 years by other companies. So this is counting those earnings, but not reflecting that future earnings will be reduced by the same amount as a result.

-

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

"sToCkS aRe An InFlAtIoN hEdGe"

-

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

"sToCkS aRe An InFlAtIoN hEdGe"

-

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

"sToCkS aRe An InFlAtIoN hEdGe"

-

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

You'll be right if multiple expansion can continue to infinity. I tend to believe it's revenues and profits that matter for long term durable returns and they haven't been there nor hedged inflation. Even Apple, supposedly one of the best companies in the world has had flat nominal earnings and a large contraction in real earnings growth over that period. 100+% or it's stock returns have been multiple expansion. That's not an inflation hedge - that's rampant speculation. Most names outside the mag-7 have been pretty abysmal in nominal returns for the last 5 years. Real returns are even worse. I don't have to be proven right - I already have been. Small caps have been terrible. Mid caps have been terrible. Value has been terrible. Only the mag-7 and a few cherry picked examples have done well and Bitcoin and gold probably did better for most then even some of those cherry picked examples Fortunately the equities I have owned have been some of those cherry picked examples. The currency kicker of most of them being int'l helped further. And fortunately for me, I owned gold and Bitcoin. And fortunately for me, the bonds I've owned over the same period have outperformed most equities we could be looking at -

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

Yes. But inflation has been what has worked out over those decades. Gold has basically held its own against stocks for the last 20-30 year period. I don't. The problem with democracies is they can't do the difficult things because they're unpopular and painful. But that is the only correction for previously having allowed yourself to do reckless things like run massive deficits on peace times with strong economy. Hindsight is 20/20, but this was the predictable long term outcome the moment we left the gold standard and became the reserve currency untethered to any real economic production. Yup. Prepare accordingly. I'll take this moment to beat the drum I was beating in 2022 - stocks are NOT a great inflation hedge. So invest accordingly. The 1970s were one of the worst decades of real returns for stocks in history. The inflation shock of 2021 left nominal earnings below their 2021 peak until Q4 2024. Inflation adjusted earnings STILL haven't recovered. If prices ever adjust to reflect that contraction, the indices themselves will also prove to have been poor performers over that time. Invest accordingly. -

Future Cuts to U.S. Social Security

TwoCitiesCapital replied to Parsad's topic in General Discussion

If we all just pretend that money printing and debt don't matter, you'll be right all the way up to the point it blows up spectacularly - either via default or inflation. I think that basically sums up what everyone here is saying.