glider3834

-

Posts

1,019 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Agree Viking - this does give Fairfax flexibility to step up the pace of share repurchases & I would be expecting this. They will balance with continuing to build cash/capital position. These sales (Riverstone & Brit stake scheduled for Q3'21) plus Digit revaluation (closing scheduled Q3'21)should meaningfully reduce Fairfax's leverage ratios - which is a big positive. I need to look into the AVLNs & how they work with Riverstone Europe sale & any financial commitment here. Would agree the insurance subs appear not to need any cash - over first 6 mths of 2021 - they sent net divs to hold co. of $122 mil ($212 from insurance and reinsurance companies less $90 mil to US Run-off) With the TRS I do have a question for the board, is it correct to say the payer of this equity swap to perfectly hedge their exposure to Fairfax, would be siting on 1.964 million Fairfax shares or 7.5% of the outstanding float in Fairfax? Given the low liquidity in Fairfax's shares I am guessing it would be difficult to purchase this size stake on open market without significantly moving the share price - so if they haven't done this, would they have purchased these shares off market? Alternatively, could they bought call options to buy equivalent amount of shares in Fairfax for the same spot price as the TRS - but then I don't believe you can actually buy call options on Fairfax shares? Curious if anyone has insights in this

-

Cheers!

-

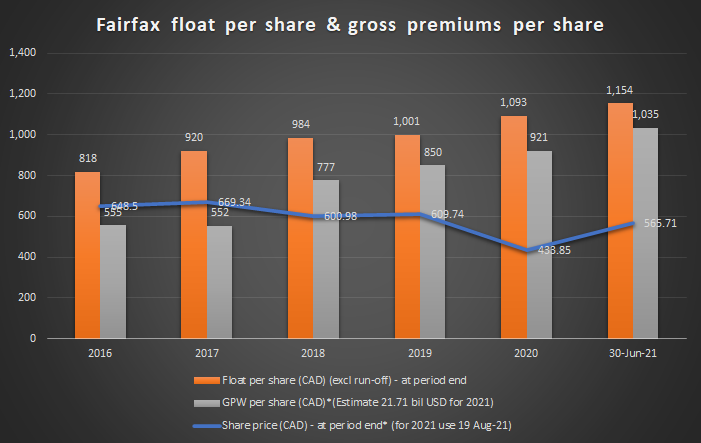

Here is another chart I have done - shows float per share (which drives investment return) & gross premiums per share (which drives underwriting profit) Both have increased substantially over the last 5 years - given these are both profit drivers you would normally expect the share price to follow - but it hasn't!

-

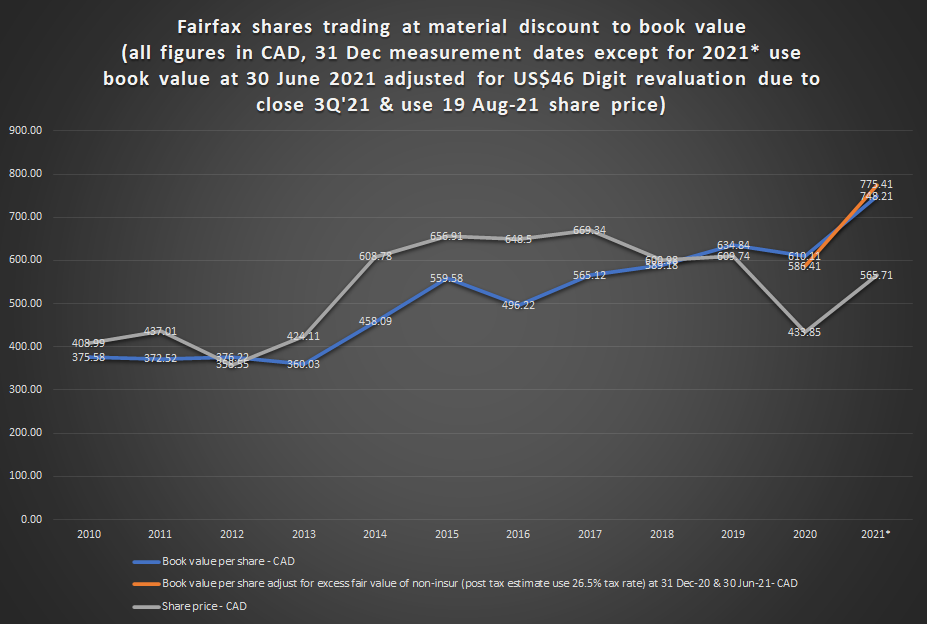

Just sharing this chart I put together - really just to visualise the significant discount that Fairfax now trades relative to book value. I notice now that Fairfax is reporting the excess of fair value over carrying value of non-insurance investments under 'Book value per basic share'. IMO Prem & mgmt would like investors to measure their progress not just in terms of BVPS growth, but also factor in this excess of fair value for non-insurance investments.

-

'Financial terms of this latest deal were not disclosed, but Fairfax will retain the real estate acquired in its original purchase, as well as a continuing royalty stream, according to a news release.' Seems to make sense but we don't have financial terms - Putnam appear to have experience in retail turnarounds, Fairfax retaining interest in upside (royalty stream) and keeping the real estate.

-

doesn't appear to be any changes in their top 15 positions apart from an 80% reduction in MCFT holding - you can see quarterly changes here https://fintel.io/i13f/fairfax-financial-holdings-ltd-can/2021-06-30-0

-

no worries Viking - yes if there is a silver lining with covid, it has resulted in greater focus on operating efficiency/cost reductions (like your good example of Recipe) or opportunity to do important upgrade work (Bangalore International Airport, Stelco) - so these businesses will be leaner, more efficient & hopefully more profitable. Yes agreed that Farmers Edge, Boat rocker have been strengthened through the IPO process & that was the right move. Really impressed by Stelco results too - after listening to conference call, looking at (very smart) recent share buyback which should take Fairfax's shareholding closer to 17% - management doing outstanding job - I can see why Fairfax are sticking to their guns & holding this one.

-

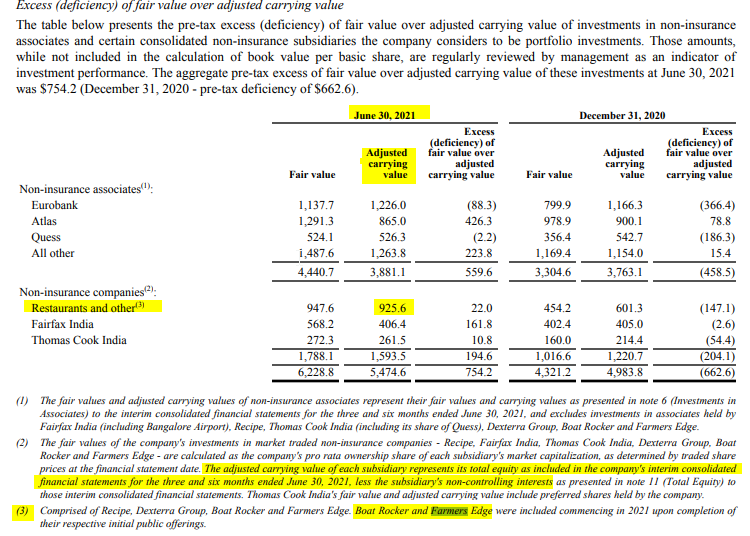

all good nwoodman - its tricky because Fairfax don't always break out figures for non-insurance subs but put them into buckets like "restaurants & other' (I guess that simplifies the reporting). I have also found this a challenge in estimating normalised earnings for non-insurance subs too , for example with AGT - I have been unable to determine their pre-tax income. I guess we can use the excess fair value over adjusted carrying value, which is how Fairfax reports, to make any adjustments to book value without trying to pull out the normalised earnings.

-

sorry Viking I have to correct my estimate- I just looked at the 2020 AR here is quote from Prem 'At the IPO value, our investment is worth Cdn$425 million but due to Farmers Edge’s losses over the years, it is carried on our balance sheet at only Cdn$303 million.' I think when Fairfax are looking at adjusted carrying value it is based on total equity in Fairfax's financial statements (not the equity in subsidiary's financial statements) - my mistake! So looks like carrying value CAD303m versus CAD110 market value now on FFH ownership share - potentially an impairment here but maybe too early to say & any impairment depends on FFH valuation/methodology Agreed not every FFH investment will work out , the overall result is really what matters & a lot of earnings report positives from ATCO, STELCO etc

-

@Viking see below - it looks like Farmers Edge is included under non-insurance companies with Restaurants & Other & adjusted carrying value appears to be calculated as total equity less non-controlling interests of subsidiary (note 2) Farmers Edge shareholder equity at Q2 2021 was around $142 mil https://www.businesswire.com/news/home/20210812005924/en/Farmers-Edge-Reports-Second-Quarter-2021-Results So would estimate carrying value as Fairfax ownership share 59.9% x $142 mil = $85 mil

-

Just listened to the Atlas earnings call & few points on this guidance - appears to exclude potential earnings growth from APR energy - they are using APR 2021 Adjusted ebitda and adjusted earnings for years 2022-24 'For the long-term guidance provided above, APR’s Adjusted EBITDA and Adjusted Net Earnings contributions to Atlas are forecasted to be ~$103mn and ~$24mn, respectively (consistent with 2021 revised guidance)' - includes current contracted cash flows only (but does not factor in any future contract wins) 'The guidance is based on the 55 newbuild vessels that we have contracted to acquire with no further vessel acquisitions assumed.' On interest/op lease expenses - does anyone have any insights around Atlas assumed libor rates & risk aspects here? Appears they are using interest rate swaps to fix rates & mitigate their variable interest rate risk exposure.

-

Out of interest - was Prem's insider buy on open market of US$150 mil one of the largest ever - I have never seen an executive insider buy of this size before?

-

I have a small indirect position in BRK but honestly I don't see a stronger investment case for BRK over FFH at the moment - a big reason for that is just the law of large numbers - how many investment options does BRK that could really turn the needle versus FFH? Also where do you see fair value for BRK? And why?

-

One of the key reasons why I made FFH my largest position end of last year Its turned into a pretty good investment for Prem so far too - perhaps that speaks volumes on his ability as an investor as well

-

I don't have an email but I would also like to communicate my comments to IR team at Fairfax

-

Honestly you have raised a good point - I agree the website needs to be optimised for mobile so that information is more accessible to investors - I have an android & when I click on the menu headings eg 'Financials' or 'News" on my mobile it will automatically direct me to the first menu item eg "Shareholder letters' under 'Financials'. I am unable to select 'Annual reports' for example on my mobile. Does anyone else have this problem? I think there should be an Investor relations email as well - this is useful for international investors who might want to submit a question outside normal business hours. Fairfax's shareholder letters are excellent in terms of communicating what is going on 'under the hood' but I agree that the website could also highlight some key messages around key investments, track record and even commitments to ESG & their incredible support for charitable endeavours. I know Fairfax believe in keeping their head office running costs low & let their results do the talking , however, even with a small marketing/IT cost they could deliver a big punch in terms of articulating their attractiveness as an investment.

-

recent article mentions Fairfax Financial Cheers https://www.marketwatch.com/story/10-stocks-that-have-what-it-takes-to-be-a-perfect-company-11628125333

-

I agree with your intent - transparency, simplification (as long as its enhances value) will help investors better understand Fairfax & ascribe a higher multiple to the shares. With a very large TRS position, Fairfax (& shareholders) have everything to gain from this outcome! But how to do this? Non-insurance companies provide the insurance business with diversification & this is also helps support Fairfax's capital position (see also Berkshire, Markel who have successfully done this). A pure insurance platform business I believe would theoretically need to hold a greater proportion of its assets in fixed income (when interest rates are extremely low) & that would likely result in lower investment returns. I think IPO'ing these assets to effectively put a market multiple on non-insurance subs whose value might otherwise be hidden is one strategy which they are doing & it also provides those companies with access to the capital markets. Providing better communication around what Fairfax actually owns (see 2020 Shareholder letter & prem's breakdown) Impact of Covid is not be underestimated - it has really had a big impact on Fairfax's non-insurance businesses that are operating in travel, retail, hospitality - I think as vaccination drive continues, the impact from Covid will start to ease & we will start to really see the earnings potential from these businesses. Does it make sense to monetise investments now that are still enduring the impact of covid? I think thats a case by case decision as the IPO market is excellent at the moment. re Hamblin Watsa - it was brought in house & in the 1992 letter (quote below) Prem talks about why they did it - point 3. probably relevant here "Why did HWIC make sense for Fairfax? Mainly, for the following three reasons: 1) It was a very good investment for Fairfax. Under very reasonable assumptions (i.e. no incentive fees or additional funds under management), Fairfax could achieve its 20% return on investment. Also, a multiple of 3.8 times revenue and 8 times pre-tax earnings was reasonable compared to private transactions and public valuations of investment counselling firms. Furthermore, we paid for most of the purchase by issuing shares of Fairfax at a fair price of $28 per share. 2) It brought proven investment management into Fairfax. 3) It removed my perceived conflict of interest and placed all of my interests in one pot." I agree with you having investments eg in real estate (Kennedy Wilson) or family run businesses (BDT) being managed by investment managers with great track records who are experts in their niche. Fairfax are right pursue this operating model for their non-insurance businesses IMO & avoid picking up turnarounds. I would like to see Fairfax raising cash where-ever possible & buying back shares - if there was one investment they should make now, this is the one of the best ones to help drive BV growth, earnings & higher market multiple..

-

at bottom of p73 of Interim showing the fair value (7138) & carrying value (5211) for non-insurance associates (including Fairfax india) as presented in the consolidated financials - there is a difference of 1.9bil The carrying value includes Fairfax India but appears they are also including non-controlling interests for Fairfax India in 1301.2 carrying value . Non-controlling interests own 71.6% or 931 mil (around 36 per share) which might explain difference?? Disclaimer here - I haven't read the actual RBC report & methodology, I just saw the headline posting in this thread so quoted from there Anyway I think better to work on $29 excess per share number as this is being reported by Fairfax - I think its worth pointing out that FFH are using Fairfax India share price (currently circa US$13 per share) as fair value for their Fairfax India stake not book value (circa $19 per share) in that $29 number so I think its conservative IMO Using US$29 excess plus BV $541 (30 June) plus expected Digit revaluation $46 (3Q21) gives adjusted BV of US$616 or P/Adjusted BV =0.7 still cheap IMO

-

+1 I agree with Viking I sold my shares in FFH in 2016 when it was trading at around CAD 700 per share because with their hedged positioning I couldn't see enough catalysts at that share price. I re-established new holdings in the C$450 ish area over the last 9 mths, but the difference this time is that I can write a full list of catalysts now - most of which have been discussed on this forum The risk/reward set up is completely different now IMO But everyone is free to have their own views - I like hearing the bear arguments as a counter-check on my own investment thesis to see if I have missed something

-

no worries

-

interesting article - could China's regulatory moves could provide further tailwinds for Digit, Fairfax India & FFH?? https://www.bloomberg.com/news/articles/2021-07-30/venture-capital-firms-turn-to-india-with-china-s-tech-crackdown Does anyone remember Prem saying something along these lines- in China the opportunities are known but the risks are unknown, but in India the risks are known but the opportunities are unknown

-

Gregmal when you look for an inflection point for a stock - are you looking at technical stuff like trading volume or daily buy/sell ratios?

-

for what its worth - interesting both Cormark & Scotiabank raised their price targets further on 2/8 after Q2 results https://www.marketbeat.com/stocks/TSE/FFH/price-target/

-

if BV is $541 (30 Jun-21) & we adjust for expected $46 increase from Digit revaluation of convertible preferred shares in Q3 & adjust a further $57 (see below - from RBC recent analyst report) - can we say adjusted BV is closer to US$644 per share (versus $431 share price) for a P/adjusted BV = 0.66? “The excess of estimated fair value over carrying value of all Fairfax non-insurance associates including Fairfax India associates is about $1.9B or more than $57/share after-tax (not included in book value).”