glider3834

-

Posts

1,082 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by glider3834

-

Yes petec agree - I think they are in Digit for the long term & its strategic investment, however, I think they will want to provide some liquidity to their retail individual shareholders, employee investors & VC funds at some point - but maybe they can do both via an IPO but retain majority control. They have also said they are aiming for 10% market share in GWP in India - probably will take them 3-4 yrs to get to 5% (up from their current 1.7% share) assuming mid 30% GWP growth rate. So if they are going to get to 10% - at least 7-8 years I am thinking. If they get to 5% market share & maintain their growth trajectory, I think it couldpotentially double Digit's valuation to around 7bil based on their current value of 3.5 bil with a 1.7% share If they can double Digit's valuation then assuming dilution is not excessive Fairfax's stake could be worth around $4.5 bil. But maybe an IPO route could help them get to that valuation earlier. I checked IRDAI and among insurers that have over 1% share - they are far & away the fastest growing, non-life insurer in India. There are a couple of digital insurers under 1% share including Acko that are growing at faster percentage rate but off a much lower premium level. They are also sharing the tech know-how from Digit through the rest of the Fairfax insurance business - so I think it has strategic importance - digitalisation in insurance sector is happening at a fast rate & I think Digit is a key part of Fairfax's strategy in capitalising on this. They have also talked about expanding Digit beyond India - nothing has happened yet but maybe something to watch.

-

another one https://www.barrons.com/articles/steel-stocks-industry-revival-51633128537?tesla=y

-

I would even suggest that is probably a daily conversation at Fairfax HQ with share price where it is - they are getting to a point where their operating performance will start to throw off a lot more cash over time & potentially greater divs from subs to holdco (as subs are in much stronger capital positions than last year) but if they want a more short term solution bearing in in mind they want to sit on their $1.7 bil cash position, they would need to sell something else like they did with Riverstone to give them $1-$2 bil to make the share buyback meaningful otherwise smaller buybacks will have to do for now.

-

petec I didn't see any value in FFH when I sold my shares in 2016 for approx CAD 700 at a premium to BV - I just couldn't see how a 15% return was even possible with a fully hedged equity portfolio. Then covid hit, FFH shares got beaten up and my view changed - look at some of the positive reactions to the Digit announcement in July from some of the posters on this board who have entrenched negative views on FFH With sustained positive performance from FFH, those negative viewpoints will change IMO

-

Yep agree - its now a case of watching how that story plays out

-

I am a bit more long term focused, at least 1-2 yrs, then I will see how FFH positions themselves to decide longer term what I will do. I just like the reward/risk set up now.

-

thanks bearprowler - so I guess you are saying its share price is undervalued but probably not as much as I do - thats cool we all have a different viewpoint.

-

Yes agree 2021 is a start but needs to be more. You are right - it is all about results in the end.

-

Sure but is it family control that is the primary driver of that BV discount? I don't think thats the main driver - there are other family/majority controlled insurance/investment businesses that trade at a premium to book. The difference with Fairfax is that these other businesses have a better financial/operating performance over the last few years than Fairfax. Fairfax is working on that & I think results in 2021 show they are on right path. In terms of comparison, ELF is a investment company with a Canadian life insurance subsidiary. Fairfax is mostly a global, property casualty insurer & reinsurer with large interests in non-insurance companies. So two different businesses operating in different product segments & different geographically- not really an apples to apples comparison IMO Few other observations from looking at Morningstar is that ELF offers a low income yield with limited revenue growth. ELF pays a 0.8% div yield & Fairfax pays a 2.58% div yield ELF 3 year annualised revenue growth is 3% but trades at 1.58x sales (vs 1.75 x 5 yr avg) . Fairfax's 3 year annualised revenue growth is 12.3% & trades at 0.46x sales (versus 0.79 x 5 year avg) I don't mean to imply ELF is a bad investment - have not done a deep dive so no comment on this front - I just don't think its a peer that FFH should be benchmarked against.

-

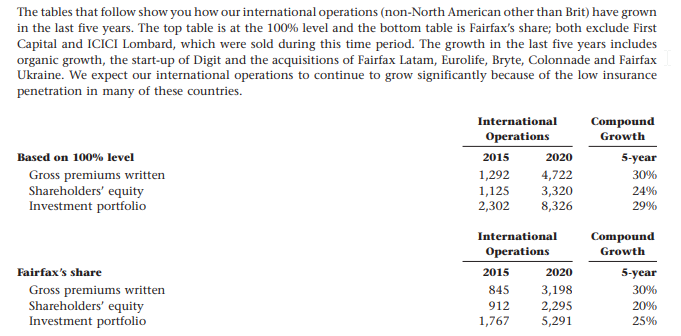

Fairfax paid $240 mil cash for AIG Europe, South America and AIG Turkey. Fairfax then onsold AIG Turkey to GIG for $48 mil https://www.xprimm.com/TURKEY-GIG-aquired-AIG-Sigorta-for-USD-48-million-articol-2,143,11-9427.htm So net purchase cost $192 mil 1. With AIG Europe, looks like Fairfax (via their sub Colonnade) bought the renewal rights & operating assets plus staff from AIG but not the liabilities, but offered to help AIG manage them (for an additional fee? not sure) Through an ongoing partnership, the company is providing claims handling and run-off management services to AIG in the European countries where business operations were acquired. Colonnade appears to have been underwriting profitably every year since 2017 & in 2020 had NPW $150mil & combined ratio 93%. 2. With AIG Latam, they bought the whole business with shareholder equity of $145 mil & GPW $580 mil in 2017. Looks like they have had issues (Chilean riots, Argentina inflation) which caused underwriting losses in 2018 (CR 119%) & 2019 (CR 117), but they appear to have focused on not growing top line just the bottom line - in 2020 they wrote $616 mil GPW ($219 NPW) with a CR 98% & had shareholder equity of $137mil. So I guess they paid $192 mil & 4 years on receiving NPW $369 mil with both subs generating underwriting profit in 2020. We can look at the acquisitions in $ terms, but I think Fairfax look at these more strategically - it costs money & time to set up an insurance business in a foreign country from scratch, apply for insurance licences etc - they got all of this with these acquisitions. In terms of Fairfax's growth internationally & their record, I think it is more useful to look at their performance across the entire international business - see below

-

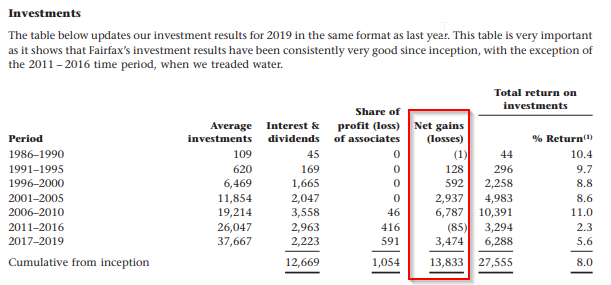

Good discussion guys - appreciate different perspectives bearprowler you said Out of curiosity, what is your valuation & target price for Fairfax? I bought CAD shares in Fairfax so paid in USD equivalent around the US$350s range (buying mostly over late last year & early this year) versus a book value which could potentially hit US$600 by this year end provided we don't see any blow up in the market. I didn't expect that operating performance and happy to sit on my hands. I agree that The Market needs to see consistent operating performance from Fairfax - but as BUffett says you pay a high price for certainty & this significant discount to book wouldn't be available if they were crushing it. More importantly, its not the discount to book that matters but knowing what percentage return they can compound that book at - its looking like 25% for this year Fy21. Is that repeatable in FY22? Probably not but I estimate over time a double digit avg compounded return of at least 12% is doable & anything on top is a bonus(also I would use an adjusted BVPS as Fairfax is carrying significant positions now well below market value eg Atlas Corp, Fairfax INdia) The BV valuation perspective has been discussed here, but lets look from another angle at Fairfax - from an earnings perspective. I estimate they can do around US1.2 bil in pre-tax profit in FY22 (excluding any investment gains) Here I have broken it down - Revenue $800 mil (UWP) based on 16 bil in net earned premium at a 95% combined ratio (see my other forum post on underlying combined ratio breakdown) $650 mil interest & dividends ( approx 2 x 1H 2021 result) $500 mil profit from associates (see my previous forum post for breakdown) $50 mil profit from non-insurance segment $2 bil - revenue less Expenses -$450 mil interest exp -$330 mil corp overhead $1.22 bil - pre tax profit If we then subtract taxes & allow for non-controlling interests we get a net result of close to $1 bil or around $38.61 per share. My estimate is forward PE of approx 10x factoring in no net investment gains plus - included in associates result is a break even result from two of their most valuable associates (Bangalore Airport & Quess) in FY22 - but these two associates are trading on depressed multiples and FY23 & FY 24 will likely improve considerably - Fairfax's fixed income positioning short duration & high quality is also depressing that PE if you believe that interest rates have the potential to move up from here. The 10 year treasury is already hinting at that possibility. With the above , I am just looking at earnings potential contribution to BVPS growth, but more than 50% of Fairfax's BVPS growth since inception has come from net investment gains (see below) - in FY21 Fairfax net investment gains of $3 bil looks a real possibility( consider up to 2bil to Q221 & Digit revaluation subject to approvals will add $1.3 bil approx more). Would you bet against Fairfax continuing to generate decent net investment gains in the next few years?

-

I was thinking about Fairfax India as well - FFH are carrying Fairfax India at around $10 per share but sitting on $20 in book value, if you can buy FFH at 30% or greater discount to book ,then provided you can say rest of FFH's book value is at a minimum at fair value (ie all else being equal) you are effectively buying Fairfax India at at 30% discount to its carrying cost or around $7 per share (compared to its share price in $13 range & its book value at around $20)

-

yep saw that too, I hope he is ok no idea either - maybe some algo traders selling on technical weakness - of course this type of trading can cut both ways, to the upside as well. Yes markets might be weak but provided we don't have some major stuff up in world economy, isn't the margin of safety looking pretty decent - I just keep scratching my head, you can buy the whole business now for 10.2 bil USD take out Digit ok lets round it down to 2bil from 2.3 = 8 bil - they paid 4.9 bil for Allied world in 2017 & it only generated 25% of their GWP premiums last year! Whichever way you start pulling the pieces apart & look at the market price - this doesn't make sense IMO. The private valuation looks totally divorced from public valuation to me. I am sure Prem & Co will find a way to get creative & take advantage (even small buybacks will be advantageous). I can't fault them operationally this year - they have done everything they can do. I am starting to think if Prem gets a great offer (& I might get in trouble for saying this) for one their key insurance businesses like Zenith for example- he should take it & maybe take out 20% of the share float at around 2/3 book value and it would also ignite the TRS position.

-

they will get around $5 per share gain (which they reported in Sep) from consolidation of Eurolife & sales of Brit & Riverstone. Also would there be a small realised gain on sale of effectively a 5% BIAL stake to OMERS?

-

thanks Viking So looks like potentially a small investment loss for Q3, unless Digit is included in which case will be large investment gain. I am guessing they would report when they receive regulatory approval to increase ownership in Digit - it may also happen early Q4 before results come out but I am not holding my breath - regulatory process in India can be slow. I am interested to see Q3 profit results from associates (Eurobank, Atlas) & consolidated non-insurance subs (Recipe) - would expect to see further improvement here. We also had impact from hurricanes that will probably hurt the CR in insurance business but lets see. Unless Digit gain is included, Q3 looks to be a more muted quarter but we need to put in context of big gains in Q1 & Q2.

-

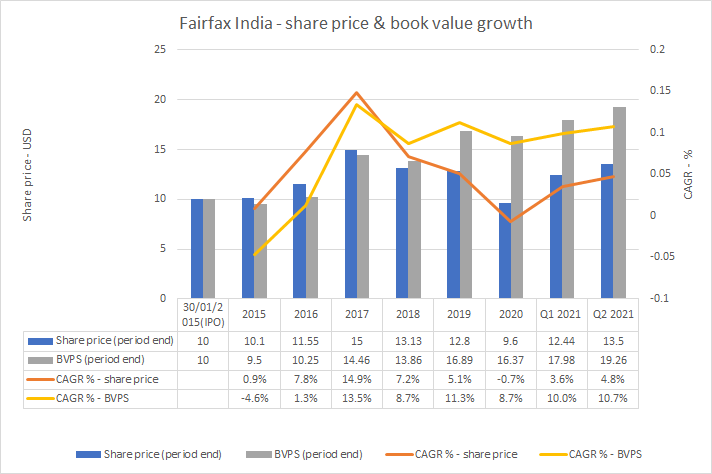

I did this chart for Fairfax India showing CAGR in share price & book value - notice how they have diverged since 2017 - some narrowing since end of 2020 but still a gap Is there a magic CAGR in BVPS gets them to trade at book value? It is also consistency in results as well. Ignoring the post IPO excitement & ratios in 2015 & 2016, if we look at 2017 the CAGR in BVPS hit 13.5% & they traded at small premium to book (1.04x book value). However, they have mostly traded at a discount to book since 2017 hitting a low point of 0.59 x book value at end of 2020 although in a 'covid' affected market when their CAGR in BVPS fell to 8.7%. If they can move that CAGR in BVPS needle above 12% & do it consistently, is it reasonable to expect the shares to trade at least at book value?

-

this is a good point Xerxes I would think longer term FFH have an incentive to own as much of Fairfax India as they can, at the widest possible discount to book value. They can do this through FIH buybacks or by taking their performance fee in 'cheap' shares. If that discount then narrows over time, FFH stands to gain. I think the IPO of Anchorage as well as providing NAV visibility also has the benefit they can potentially raise capital at or around Anchorage's NAV which they can't do now with Fairfax India - could this then enable a bigger capital base that FFH can potentially earn a performance fee on - is this a fair comment?

-

Do we know if Fairfax India or FFH will charge Anchorage a separate performance/investment management fee %?

-

actually thinking about it FFH are not taking their performance fee in cash but in shares - it sounds like they are not interested in a cash dividend but I guess they could also do dividend reinvestment - anyway going a a hypothetical rant...

-

True - could this be one factor behind the discount? Dividends The company did not pay any dividends on its outstanding multiple and subordinate voting shares during 2020 and 2019. But if investors own the underlying shares of listed stocks that Fairfax India owns, they would receive dividends & avoid management fees. So maybe thats a disincentive to own via Fairfax India. Paying dividends would also mean cash flow for Fairfax Financial. They could change the performance fee calc to total shareholder return in terms of BVPS growth plus dividends - just a thought??

-

Has anyone found the multiples on these? How do they compare to BIAL?

-

agreed Viking

-

Yes correct consolidate because they have 93% voting control even though they have less than 50% ownership

-

Yep thats right

-

Yes also think average favourable development 2013 to 2017 was around 7.7 & avg CR looks to be around 91.5 & for 2019-2020 average fav development was 3.6 & avg CR was 97.5 - so I think that might explain part of the difference. But also need to factor in the impact of covid in 2020 - if you take covid away, the CR for 2020 drops to 93.