gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Here's another example: The Fed wants to stimulate the economy by doing "QE." So they buy up interest bearing coupon securities from the private sector and now that interest income is being earned by the Fed, on the Fed's big old balance sheet. In place of the securities they bought, the private sector got bank reserves at the Fed, which at the time didn't pay interest and where of little to no use in the real economy. There was a surplus of bank reserves in the system and they are all parked at the Fed and the level of private bank lending is not constrained by the amount of bank reserves in the system - it is constrained by other regulations and market demand for new loans, credit quality, etc.. So during this period, the Federal Reserve earns a profit on their balance sheet - look it up - big profit. It remits this profit to the Treasury. What do you call it when interest income that would have gone to the private sector is instead not earned by the private sector and remitted to the Treasury, reducing the deficit? That's essentially a tax. Revenue to the government that reduces the deficit. What did QE do that was stimulative? It barely had any effect on Government bond rates. The Fed has studied this themselves and found a few basis points, maybe... They expanded it to MBS and it, along with very short durations of mortgages during the refinancing booms, led to tighter spreads on MBS over treasuries - that was stimulative. Was it more stimulative than the counter-stimulative effect spelled out in the first paragraph? I doubt it, but it is impossible to say for sure since we don't know what the spreads on MBS over treasury securities would have been without the Fed expanding QE to MBS. ** remember, "QE" and "QT" are just swapping one form of federal liability (what we call "money") for another. swapping in a bank reserve, even though those do now pay interest (new feature..) but removing a highly useful treasury security - the base highest quality collateral for the entire global financial system's transformation, leverage and exchange engine, is not a stimulative swap for the private sector

-

Here's one small example of how your understanding of the Fed's primary tool - short term interest rates - could very well be close to 180 degrees backward. Remember that around 80% of the US debt is owned by the private sector and the rate of interest paid on this primarily short term debt increases or decreases the level of deficit stimulus - --- Here’s the scenario. You have a stable company that doesn’t make much of anything over time but also doesn’t lose value either. It isn’t a great investment but the share price, intrinsic value, etc, is basically stable. Trades at $100 per share. You own 100 shares, $10,000. [for the dense, I am going to spell it out - this is US Dollar cash in this metaphor] This company decides to implement an all stock dividend of $5 per share annually. Not a cash dividend, a stock dividend, which is more like a tiny stock split. Let’s say they target 5% annually for this stock dividend. Next year you have 105 shares but everybody else also has 5% more stock, the company is identical to the earlier scenario and the share price starts to drift down by about 5% per year, leaving the market cap of the company essentially unchanged. Each year they do this, and low and behold, the “inflation” – the rate at which the value of one share loses value, is basically gravitating towards the “interest rate”. If the all-stock dividend is targeted at 7% annually, the stock in the above example will start to experience a loss of value, per share, of around 7% annually. If the all-stock dividend is targeted at 2% annually, the loss in per share value due to this “inflation” will tend to gravitate towards 2% annually. Do you see what I am pointing out? There comes a point in the sovereign interest rate setting game, where the interest rate on government borrowing is materially effecting the size of the deficit (because the majority of the borrowing is done at the short end, where rates are not set by market forces), and a large enough share of the government debt is “owned by the public,” – there comes a point where the artificially set interest rate from the Fed starts to act like a magnet to the inflation rate just like the stock dividend example above. They are giving you more of the same instrument.

-

That's great Dynamic - and a perfect illustration in real-time of the fact that you do not need very many great ideas in an investing career to really shoot the lights out. There are a bunch of different ways to play this game but the way you played it has worked phenomenally, with little real risk - even with "unconventional concentration." It was available to basically any value bro that hangs out on message boards like this. And it outperforms the index.

-

This is bonkers. I really get the feeling that you aren't listening to anybody here and your mind is so made up that it could take an entire 15 year market cycle to give you back the humility to realize you have a lot of things backwards. If you are trying to do this for a living, that puts you out of business and into a different industry. As a side note... for the 10th time or whatever it is... your understanding of the Federal Reserve's role in influencing inflation is likely wrong enough to be closer to 180 degrees backward. And if the all powerful Federal Reserve gets a handle on this raging inflation you think is right around the corner, you want to own "cash" in that scenario?

-

25% tariffs on Canadian and Mexican imports.

gfp replied to SharperDingaan's topic in General Discussion

I am on Isla Mujeres. Hoping to make it home to los estados unidos hoy -

25% tariffs on Canadian and Mexican imports.

gfp replied to SharperDingaan's topic in General Discussion

i had always assumed the next leader would be that Carney guy from the Brookfield board of directors that was head of the central bank in Canada and UK, but I’m here, still stuck in Mexico, with a bunch of Canadians cause apparently they all come here when it’s cold, and they are all going to vote for this Poilievre conservative candidate. I had four or five different people tell me how smart he is, torments interviewers with his intellect, etc…. So if the Canadians in Mexico drinking heavily straw poll is to be trusted it will be Poilievre -

back on topic - yes, of course we hit the top on December of 2024 and today and it’s all downhill from here. Obviously…. And yet there are still things to buy tomorrow. That is, if New Orleans can ever open their god damned airport so I can finally leave Mexico thank you

-

basically the first 13 years of my investing career, the S&P500 showed no return [2000 -> 2013]. But it was a fine time to be an investor, even if you were just averaging into the S&P 500. There was a huge bull market in commodities, Berkshire was available many times at great entry prices, lots of individual value situations along the way. There are always good investments out there if you keep looking. The best point made up thread was that you have to find a style that works for you.

-

Fortune profile of Greg Abel. I’m stuck in Mexico missing the glorious snow in New Orleans boo hoo https://archive.ph/QcRW2

-

I'm curious what happens when an equity accounted investment was a bargain purchase but the company has zero profit and dividends reduce the carrying value to zero and then what. Let's say you have a carrying value of $100 and zero profitability. Dividends are paid out such that the $100 carrying value becomes zero. What happens when the next $50 dividend rolls in? I know when the carrying value is being depleted by D&A it just stays at zero (like Nelnet's fiber internet company). Just curious about the accounting result of the above scenario

-

the dividends don’t disappear from the balance sheet - they are there as cash (initially) and were most likely run through as earnings at some point - this only effects the carrying value of the equity method investment on the balance sheet. Just like Berkshire and OXY, Berkadia, Pilot before the buy-out, etc..

-

ETF for long term inflation indexed treasury securities

gfp replied to Dinar's topic in General Discussion

I think this is a long way of saying you will never end up taking a position in this. If you think a 2.6% real yield is interesting and want to place a bet, the time to do that is now. I highly doubt you are going to get an opportunity to put the trade on at 3%. -

Man I'm in my mid 40's now and nobody I know seems to be getting married any more. I kind of miss it, I love a wild party after a wedding. Great excuse to see old friends when everybody is scattered around the world the rest of the time. None of my tenants seem to get married either. I think we are well past peak marriage in the US. We got married in 2009 after 'dating' for 7 or 8 years and I had to pay for it - $35k at least, I think I blocked out the exact number - horrible timing with the markets but man what a party.

-

Didn't seem to put up any conflict flags with Ben Watsa

-

What does that mean Daphne?

-

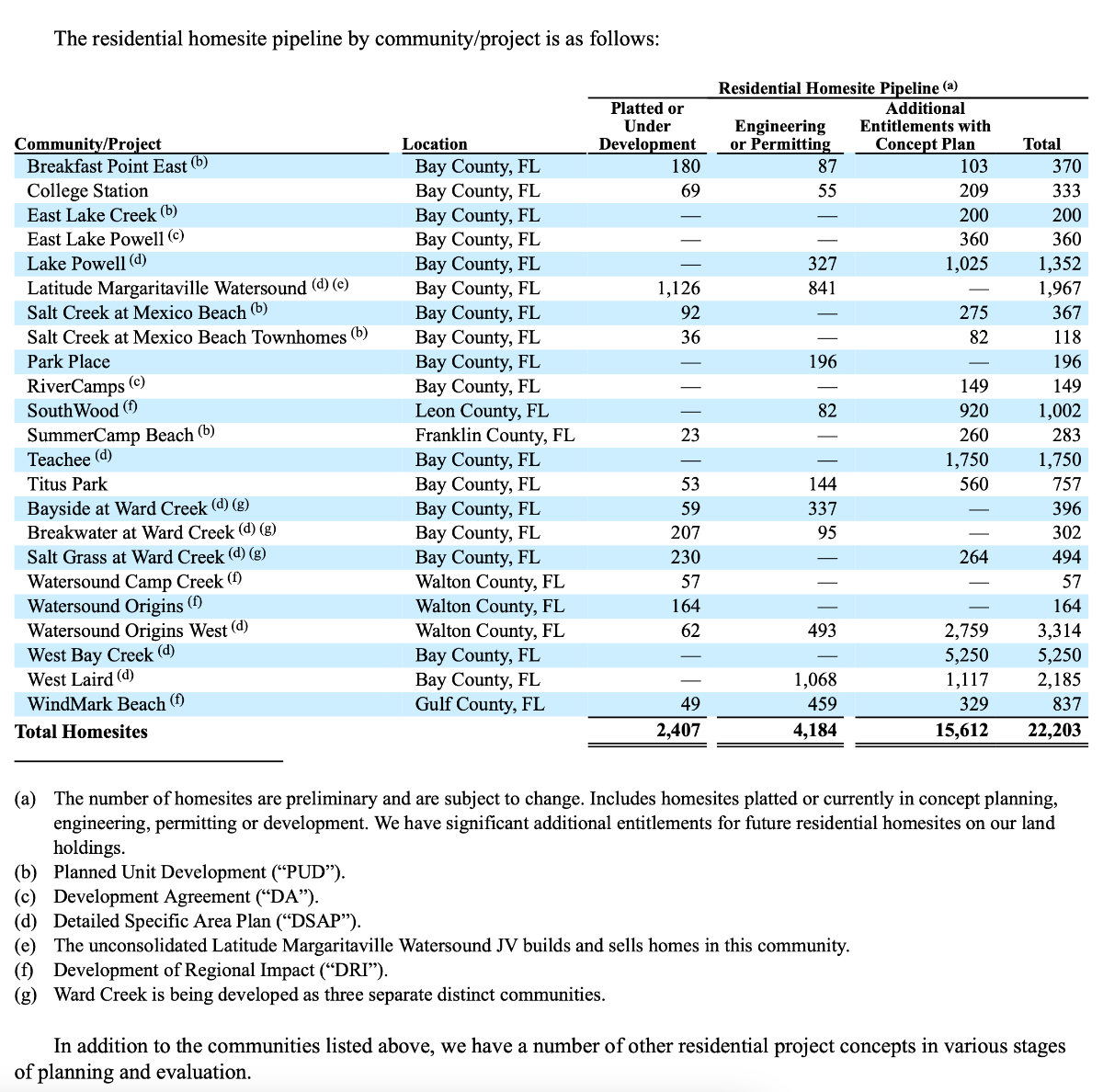

It's page 49 of the most recent Q but they include them in all reports -

-

@brobro777 you're alive! I was starting to worry about you and the wildfires when I checked the price of eggs the other day

-

ETF for long term inflation indexed treasury securities

gfp replied to Dinar's topic in General Discussion

LPTZ has options and this profile ->

-

ETF for long term inflation indexed treasury securities

gfp replied to Dinar's topic in General Discussion

I believe that is the best you will find as an ETF and the duration is probably longer than 15 years - closer to 18. If you need a longer TIPS bond maybe just buy the bond itself -

That's not exactly what he said. But, yes - Greg will have final say on capital allocation and that includes everything. Warren does firmly believe that there needs to be one person in charge, not a committee. The board of directors can fire that one person, but unless they do the buck stops with Greg.

-

https://go.pracap.com/hubfs/Quarterly Letters/2024/2024 Q4 Investor Letter - Approved v2.pdf Praetorian year end investor letter. Page 10 mentions St. Joe for those interested in that part. I would have liked to see a money weighted return figure but alas we only get "from inception" which was probably a million bucks from his dad or something along those lines. edit, re: JOE - I don't see how he gets $2 Billion of equity value, net of debt, today, for the commercial income producing endeavors. It also rubs me the wrong way when people spit out a per-acre value on 168,000 acres when they know full well that isn't the number of acres St. Joe will be developing. Use 100k - it's a plenty big number to build some credibility into your analysis. " you’re buying approximately 168,000 acres of land in Florida, much of it waterfront, for approximately $3,600 an acre," - c'mon man, give me a break.

-

Lots of annual and quarterly letters on page one of this thread

-

Lots of toppy looking charts across risk assets - it will sure be some move if they all violate these assumptions to the upside. S&P500 included

-

that's the stock they bought for all of December being cancelled at the end of the month. obviously it wasn't all purchased on December 31st. Most of it was purchased on December 20th in a block trade

-

You aren't really listening. It's not the Federal Reserve you should be focusing on - it is the US government. They are not the same thing. Excess bank reserves are not a useful or circulating form of "money" in the real economy. They are trading tokens between large banks, each other, and the Fed. Bank lending to the real economy is not being restricted by the level of bank reserves in the system. Bank reserves got so high because they were swapped for other federal liabilities - treasury securities, agency securities, etc - useful liabilities that do circulate and have great utility in the real economy. If the Fed swaps one federal liability for another it doesn't create new money. Fiscal deficits create new "money" and private bank lending growth creates new "money."