gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

How would that produce a profit on index inclusion?

-

No clue. The only news I could find today was the bond sale to finance part of the Sleep Country deal. https://www.bnnbloomberg.ca/investing/2024/11/19/sleep-country-mulls-potential-bond-sale-in-rare-leveraged-buyout/

-

impressive! jk jk

-

I think there are some investors doing the 50% annually on tiny companies currently. This guy comes to mind: https://dirtcheapstocks.substack.com (this is a paid sub stack but the picks I have seen have been very good) - he is also on twitter. Also Tim Eriksen, who runs Cedar Creek Partners, will probably get close with his expert market stuff.

-

Those are the figures I was referring to but just sort of rounded them because I didn’t have the exact numbers in front of me.

-

I forget who, but someone here reads these. This is the Q3 NAIC report for National Indemnity. Definitely sounds like GUARD was the problem child during the quarter, as was pretty clear from the 10Q and mention of "new management." Sounds like about $500 million of negative development that GUARD had ceded to NICO, plus NICO sent $517m of capital (unaffiliated stock holdings) to GUARD to boost their capital. GUARD had been growing quickly for a decade or more. 20087.2024.P.Q3.P.O.3.4841235.pdf

-

General Re 3rd quarter NAIC filing came out. No equity purchases in the quarter, not much of a surprise. Kind of cool to see Gen Re get $235 per share for an Apple sale on 7/15 (basically top ticked the year so far) - and the basis on that stock was $29.94 / sh. 22039.2024.P.Q3.P.O.3.4836600.pdf

-

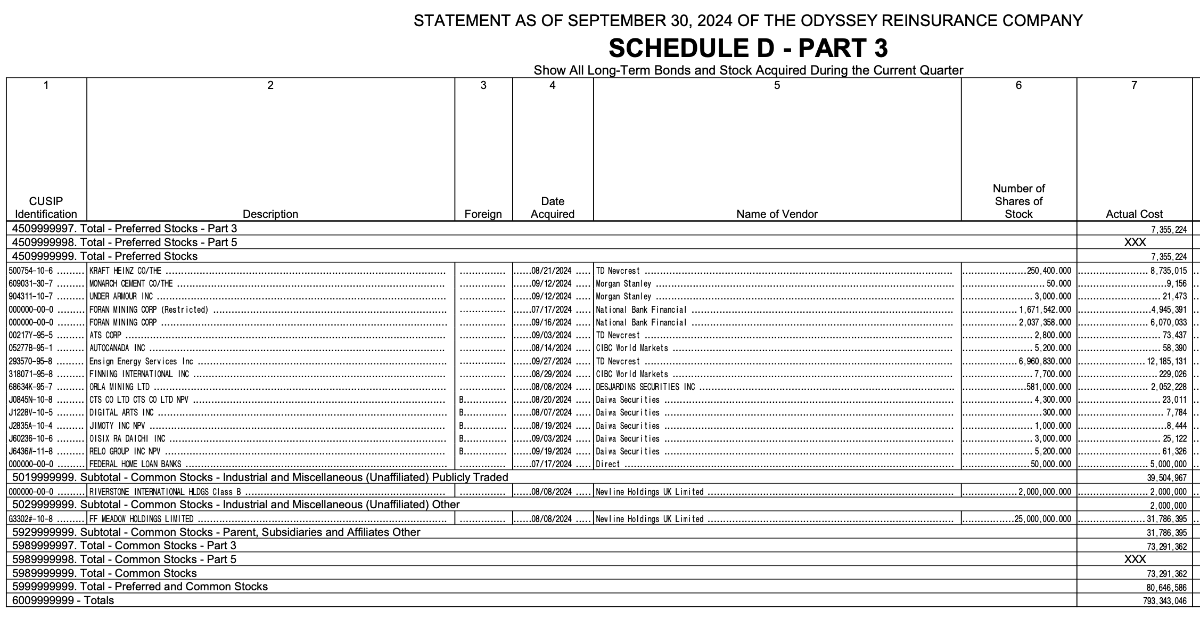

pre-13F look at the trading inside Odyssey Re in the quarter - no moves of any size this was from last night, but looks like the 13F came out today - https://www.dataroma.com/m/holdings.php?m=FFH 23680.2024.P.Q3.P.O.3.4833355.pdf

-

Tough to tell from that weird chart but is that Fair Isaac?

-

Perhaps ironically, Bitcoin, the economy and risk assets in general will probably do much better in a higher interest rate environment than in a low interest rate or ZIRP environment. It may be counterintuitive since people are taught that opportunity cost is such a big factor. Low interest rates -> bad things happening / stagnation / lots of demand for safety and liquidity / risk-off Higher interest rates -> reflation/inflation / growth / risk-on

-

It is usually so illiquid. Any new interest will move the price in the short term. The speculation here that it was Indian ex-pats buying on the perception of a great Modi-Trump relationship sounded plausible. But the Indian markets have been down lately. The airport is a hit so it doesn't matter to FIH.U but I'm selling these newcomers stock every time they bid it into the upper 16's

-

None shall pass!

-

That's impressive they know the future. Super valuable skill to have

-

Well since the company just bought $304 million USD worth of shares from him for cash I suppose he won't be pushing for another dividend increase.

-

It looks like NVO to me?

-

Just to update on this - I heard back from Fairfax tonight and any gains on the total return swaps on Fairfax's own share are taxable in Canada and it is incorporated into the tax provision in the financials.

-

It's not a great week to hang around in popular short positions!

-

Sorry I had to shut that rally down by channelling my inner Bruce. My apologies to the Johnny-come-latelies.

-

This line was weird - " Fairfax also continued its share repurchase program, spending $678 million in the quarter" Pretty sure it was more like $189 million in the quarter. Do we know who this manager is? A board member here? Underperforming the S&P 500 by over 10% annually over a long period of time is a tough sell

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

gfp replied to twacowfca's topic in General Discussion

you meant to say "can't" ? -

There is also a situation progressing where Bangalore needs to start on the second airport before Kempegowda's exclusivity period expires so most likely Anchorage will get the opportunity to develop and operate the 2nd airport on the other side of town. Airport City development plus traffic roaring back to above pre-COVID peak. Got some good stuff cooking The potential large bank deal looks like a 2025 announcement. I'm OK not winning that one.

-

I only use it on stock where there is a big spread. I often get fills that don't show up on the chart that are better than the stock officially trades at. Sometimes it takes a while but this morning the fills have been very good and pretty quick. A lot of the stuff I trade won't execute on the bid or the ask and if I calculate the midpoint and put in a limit sell it will just move the ask and signal the market I am trying to sell.

-

Using that IB mid price algorithm to sell a bit of Nelnet before earnings. Up a lot this morning.

-

Yeah I will add to the above that if you are installing a new pool definitely do your research on variable speed (as mentioned by pelagic above) and other lower-power-consumption pump options because a traditional old school pool pump can add a decent amount of usage to your power bill. Same with heaters and chillers. I recommend salt water chlorinators, which should be automatic each night and you will only have to shock the pool occasionally - never have to add chlorine outside of a shock. The salt water feels nicer anyway but make sure no hardware anywhere near it can rust.

-

In my market the water table makes the fiberglass shells pop out of the ground so they only use them indoors like new hotel pools and condo buildings.