gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

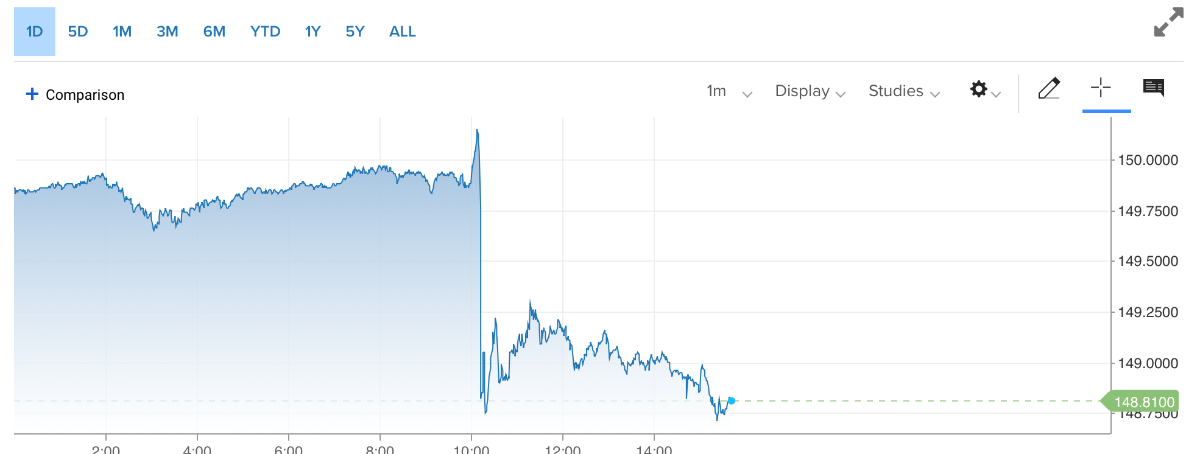

Not sure where to post this, but there was another super obvious intervention in USD-JPY today. There are some real stresses under the surface of the global funding markets. I actually think the big long bond breakdown everyone is obsessing about is just a regular seasonal move that happens every year lately but we'll find out soon enough if this is a head-fake.

-

It was removed this year. We'll see if it returns next year.

-

https://www.sec.gov/Archives/edgar/data/47217/000095017023051239/xslF345X05/ownership.xml As expected, once Buffett starts selling something like this he usually sells it all. He is about 2 million shares away from going under 10% so there may just be one more filing before he gets privacy on the rest of the sales.

-

I'm sure he's going to do great but 9 commas is a bit different than 9 zeroes or whatever you were trying to say. What is 9 commas? An Octillian? A Nonillion? Might as well be a bazillion.

-

Michael Larson - the manager of Bill Gates' stuff - recently picked up some WIW and WIA https://www.sec.gov/Archives/edgar/data/1267902/000091485123000038/xslF345X03/wf-form4_169592622975535.xml https://www.sec.gov/Archives/edgar/data/1254370/000091485123000037/xslF345X03/wf-form4_169592586757618.xml

-

Berkshire has $122k Billion in T-bills, $22.3 Billion in bonds with average maturity of something less than 2 years and $25 billion in cash earning whatever cash earns on corporate Gov. MM sweep accounts. So outside of equities, Berkshire's very large pool of float is invested almost entirely in T-bill like instruments. Berkshire will make something like $8 Billion in government interest this year. I don't know of any other insurance company, except maybe Global Indemnity recently as they shop the company for sale, that kept their entire fixed maturity portfolio at around 6 months. Just the absurdity of a Trillion dollar asset company holding only $22.3 in bonds is remarkable enough, but even those bonds are less than 2 year duration.

-

I know what you meant. I'm saying Berkshire's bond duration has 'em all beat.

-

Nobody's shorter than Warren! The master at work

-

I wonder what the losses will be on their poorly timed forward purchases of 3 year bond futures. edit: I guess most of the losses would have already been reflected in the Q2 figures? V. Watsa [indiscernible] portfolio, right, it's only the bond portfolio. And the important point that is all on 80% of our bond portfolio is government treasuries mainly, but government wherever we operate, Canada -- Canadian governments and other countries. And only 14%, I think. we said was corporate, something like that. And that's all very short term that's coming due relatively soon. And what we have done, Tom, is because these are coming due in the next 3 months, 6 months, we like the rates in the first quarter. So we locked in 3.7% -- 3.75% for U.S. government treasuries for 3 years. So we locked it in ahead of the maturity. We are happy with 3.75, could go to 4.25%, 4.5%, I don't know. It could go to 2.5, 3.75 was good. We locked it in, and that's ahead of the maturities in the next 3 months, 6 months.

-

I think that's more like a quarter million bucks in today's money but still impressive for a youngster.

-

I don't know where this came from, but I happened across this letter between Buffett and George Young, of National Indemnity, while cleaning up an old stack of papers in my office. The letter is from July 22nd, 1976 and might be interesting to some because it offers a glimpse into Warren's decision making in a letter that was never intended for public disclosure. I thought it was interesting anyway. PDF attached. geicoletter.pdf

-

The Missing Billionaires - Victor Haghani & James White

gfp replied to wolverine890's topic in Books

I am waiting around for something so I played the coin flip game linked above for 10 minutes and bet strict 20% of my bankroll on heads on each flip and still ended up with $21.13. Disappointing. I guess I didn't have a large enough sample size... -

So my local bank, HancockWhitney emailed out an 11-month CD offer at 5.4% this morning. I realize that's where the market is for CDs and this isn't exceptional but it's not exactly an encouraging sign that they are clamoring for 5.4% deposits. Then I read this article in the journal that JPM (of all places!) is offering 6% on $5 million min. on 6-month CDs! Why does JPM want 6% deposits? Just to expand relationships at the private bank? I guess if deposits are fleeing the private bank to T-bills they can offer this to try to match the after-tax return of a t-bill for someone who would pay state income tax on bank interest but not t-bill income. https://www.wsj.com/finance/banking/jpmorgan-6-percent-cd-fe862850?mod=hp_lead_pos2 Also, if the banking crisis is behind us - why hasn't the BTFP balance declined at all? Instead it keeps going up... https://fred.stlouisfed.org/series/H41RESPPALDKNWW

-

Routine renewal of the NCIB, including automatic plan to continue repurchase activity during blackout periods if they wish - https://www.fairfax.ca/press-releases/fairfax-financial-holdings-intention-to-make-a-normal-course-issuer-bid-for-subordinate-voting-shares-and-preferred-shares-2023-09-28/

-

After many many years of owning Torchmark (now Globe Life), Berkshire has just started selling down their position, selling more than half of their longtime position in the last reported quarter. Knowing Warren, he isn't going to just trim a small holding like this - so expect Globe Life to quietly dissapear entirely from Berkshire's holdings in the next 13-F.

-

Not sure I understand your question. Commercial property values have already reset down 20-30%. The replacement cost of the buildings hasn't gone down. I don't think the price of commercial insurance is closely linked to the market value of the properties except to the extent that the size of the loan on a building will set a floor on the amount of coverage a lender will let you get away with.

-

Commercial real estate, not conforming 30 year residential.

-

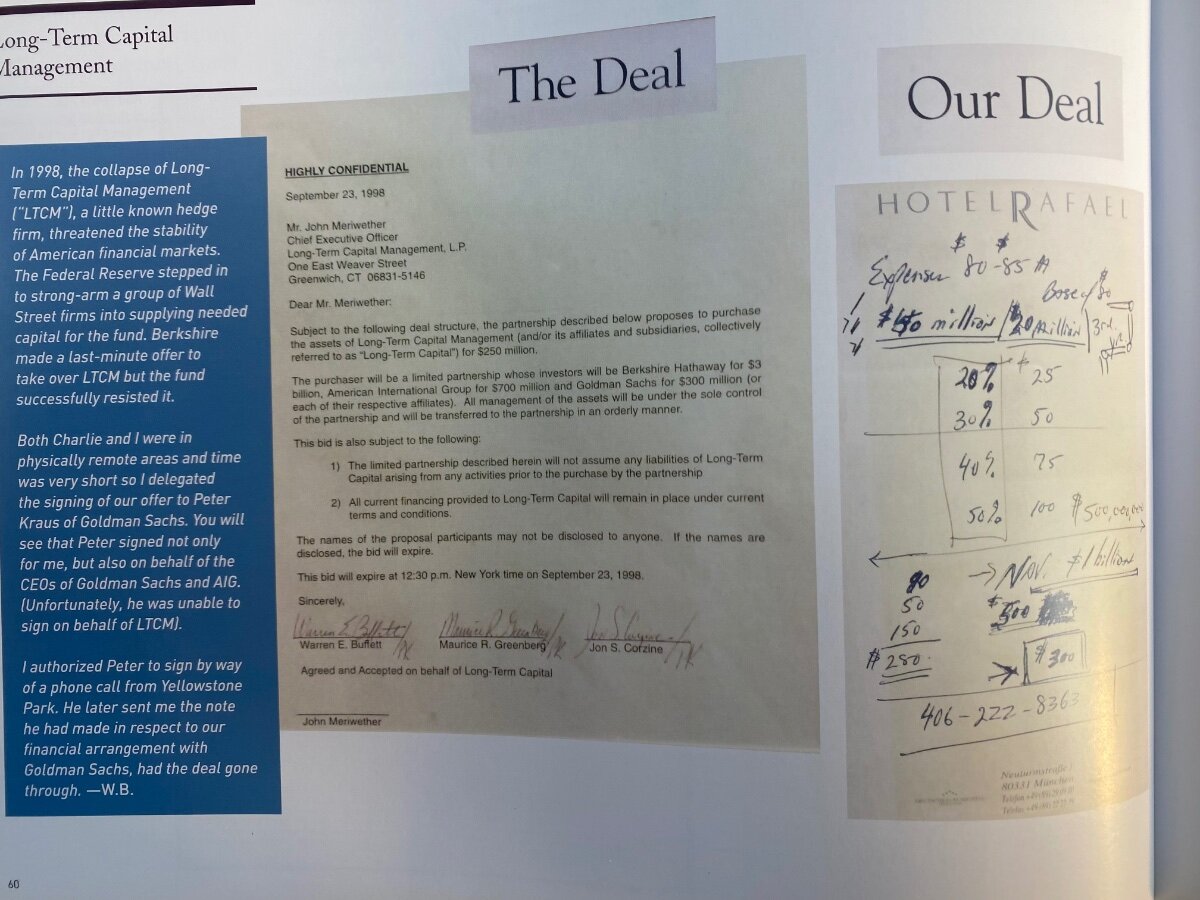

With various articles coming out on the 25th anniversary of the collapse of Long Term Capital Management, I was reminded of Warren's offer to purchase the fund for $250 million while on vacation in Yellowstone. One book I read claimed that Buffett only gave Meriwether one hour to accept the offer and a deal couldn't be negotiated in time. The Fed ultimately forced the banks to rescue the fund in exchange for 90% of the equity of LTCM. These were the same banks that were creditors to LTCM, so they were really just "bailing out themselves." The birth of the Fed put for contagion fears... This page from Berkshire's 50th anniversary book has Warren's comments on the attempt and some of the original documents. The idea was that Berkshire would put up most of the capital but the fund would be wound down over time inside Goldman's trading desk. LTCM's equity was around $400m at the time of this offer, but rapidly heading to zero. Just about all of the spreads that had widened out to extremes returned to normal over time so Berkshire's capital and staying power would have produced a decent, although far from remarkable, profit. Meriwether started another fund doing the same stuff with lower leverage after LTCM. It imploded in 2009. Then he started another fund doing the same thing after that. Most of these guys were from the Solomon Brothers arbitrage desk and of course there were some nobel prize winners in there. Here's a link to Buffett telling the story to some college kids - https://novelinvestor.com/buffetts-lessons-long-term-capital-management/

-

Fairfax certainly has exposure to hurricane risk and profit but is much more diversified in their cat exposure. Berkshire this year is extremely unbalanced in their cat exposure with unusual concentration in Florida hurricane risk. Fingers crossed, there is still plenty of Hurricane season left. Quote from Peter Clarke on the most recent (august) conference call -

-

Doesn't look like they are taking a 14% margin on that to me. I would be wary of being charged sales tax if buying something like this from Costco. Where I live sales tax is 10%.

-

Certainly not ideal if you are a Canadian company patiently waiting for multiple government approvals in India.

-

here is the article without the FT or Fortune magazine paywall - https://finance.yahoo.com/news/american-express-ceo-called-warren-152037387.html

-

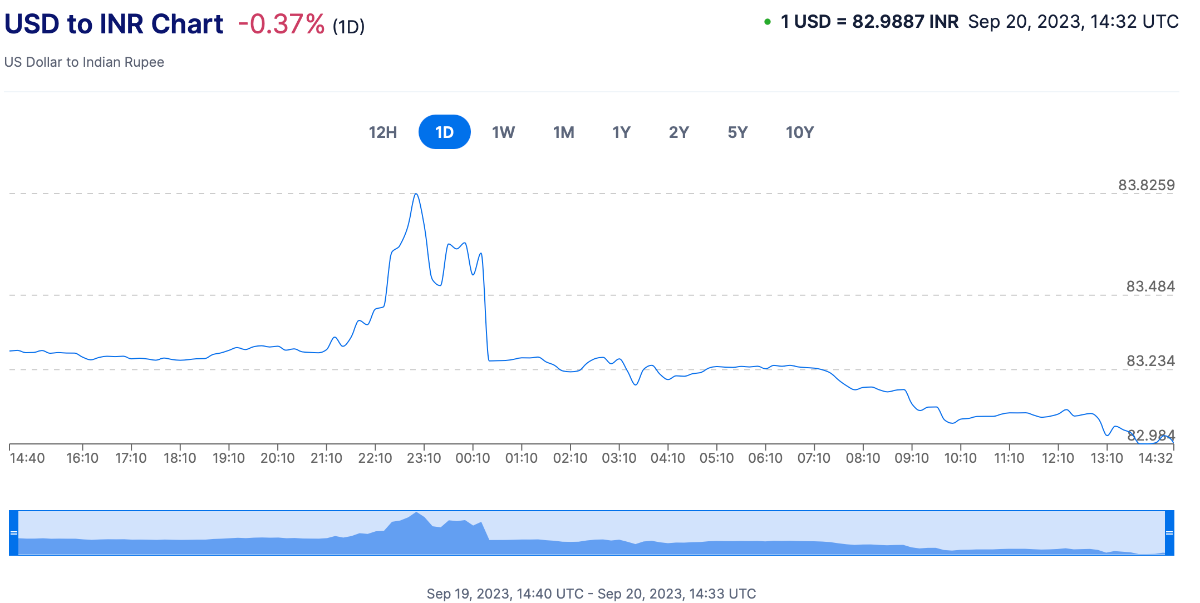

Another RBI central bank intervention to prop up the Rupee from breaking down against the dollar overnight. Lots of dollar strength in Asia.

-

But we need the Fed to fix Orange Juice, Olive oil, diesel and OPEC!

-

"the Insurer" put out a short interview and article on BHSI - a wonderful business that Berkshire started from nothing instead of acquiring. Imagine how much goodwill would be on the balance sheet it Berkshire were to buy an identical operation performing like BHSI today. https://www.theinsurertv.com/news-in-focus/godhwani-bhsi-benefits-from-berkshire-balance-sheet-and-long-term-view/?utm_source=listrak&utm_medium=email&utm_term=https%3a%2f%2fwww.theinsurertv.com%2fnews-in-focus%2fgodhwani-bhsi-benefits-from-berkshire-balance-sheet-and-long-term-view%2f&utm_campaign=Godhwani%3a+BHSI+benefits+from+Berkshire+balance+sheet+and+long-term+view