gfp

-

Posts

8,122 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Yowza, that will be a healthy book value print for Berkshire with a pre-tax $26.6 Billion gain on Apple in the 3 month period. $58.6 Billion pre-tax year-to-date.

-

The practical effect is pretty small though. Maybe around $2 Billion a month. The administration implemented expanded income-based repayment "help" that reduces the disinflationary impact of today's ruling. Every little bit helps though! https://www.ed.gov/news/press-releases/new-proposed-regulations-would-transform-income-driven-repayment-cutting-undergraduate-loan-payments-half-and-preventing-unpaid-interest-accumulation

-

Tell me more about this 5.15% mortgage you just got? Location, terms, length? Also, bell peppers on a cheeseburger???

-

Well according to Bill's (wabuffo) withholding chart, we are still growing wages strongly, although it is possible people adjusted their withholding percentages after a rude surprise in April -

-

Thanks for the long detailed post. I basically agree that inflation doesn't matter at all except to the extent that it potentially (and usually) redistributes real wealth unevenly between cohorts. Nobody really cares if we keep score using the metric system all of a sudden, it is just a unit of account. But when the changing of the units on the scoreboard effects different groups to different degrees we have a problem. Where we differ is that I think your wage spiral is history. Hours worked has already rolled over. Employers are reluctant to let anybody go because it was painful and expensive to find them and train them in the first place. But without sufficient new orders coming in, new hiring and wage-increase negotiations will be a memory. We'll see how it all works out!

-

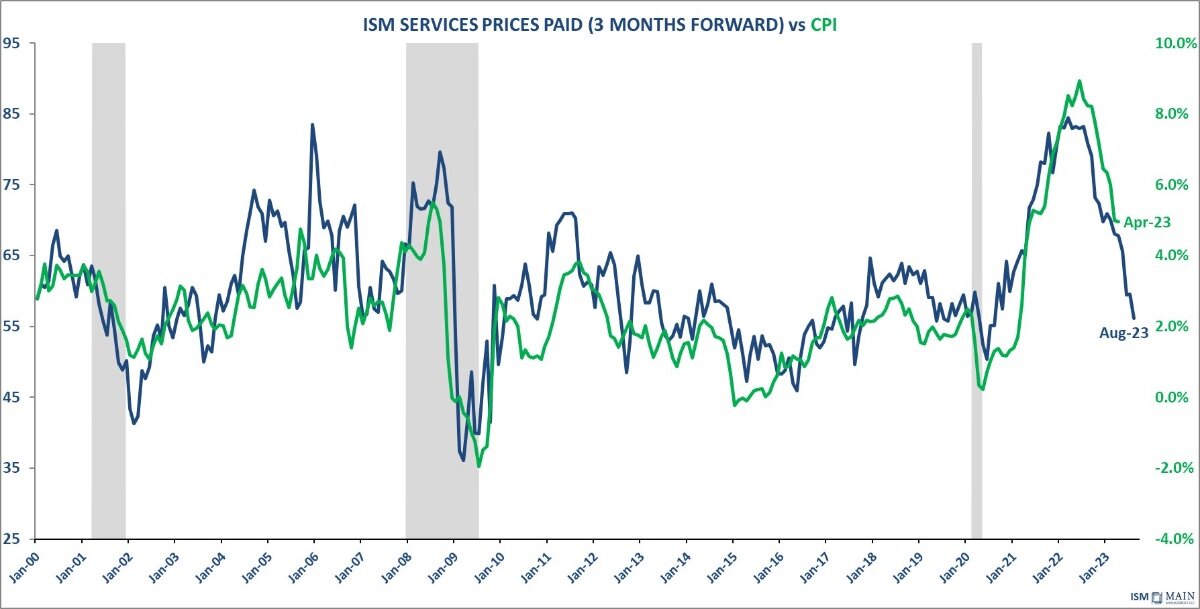

Here's a good one, ISM services prices paid index time shifted forward 3 months overlaid with CPI. Capitalism and time cure the type of inflation we had. Truflation is another example. If you think most of our inflation was caused by monetary inflation and not COVID-related supply/demand shocks, the FED isn't going to do anything to help. Only adjusting the level of the deficit will help if you think the inflation is caused by too much "money" sloshing around. Since so much of the deficit is structural at this point, you would have to raise taxes. Or CUT interest rates to reduce deficit spending stimulus. Even the Federal Reserve is losing money on their balance sheet holdings - that is additional stimulus! Government deficit plus "net interest paid by the Fed" on their money losing balance sheet while the yield curve is inverted. https://truflation.com

-

So if my napkin math checks out that is a redemption of 1,568 preferred shares during that period, at $100,000 per share face value, redeemed at a 10% premium to face (plus accrued dividends), so that sent Berkshire $172.48 million plus any accrued but unpaid dividends. I'm sure a more enterprising person could reverse engineer the size of the Occidental share repurchase for the period that would result in that level of mandatory redemption at the 50/50 over $4 TTM deal...

-

I believe that is only Credit Suisse's US operating subsidiary, but still it doesn't drum up a ton of confidence in these stress tests when the "strongest" bank by capital on your 12/2022 list has already failed by the time the results are released.

-

So... she lives in China, worked for BABA and an IT company and needs to ask you how to get a VPN???

-

So in your housing example the average homeowner has a huge fixed rate multi-decade mortgage getting inflated away right?

-

I think Chompin' Chuck has been all over ERIE for some years now. (dealraker)

-

I still don't get all this focus on inflation and the Federal Reserve. Inflation has been slayed, it is over for now. We do not have an inflationary economy at the moment - despite huge deficit spending stimulus. The Federal Reserve's overnight rate isn't what slayed inflation and the Fed doesn't have an effective tool for dealing with inflation going forward. Further rate increases are more likely to make "inflation" worse.

-

Yes, he is Jay Pritzker's nephew. Also a billionaire. His Dad, Donald Pritzker, ran Hyatt for a while.

-

Another deal for PacWest assets (Fairfax got the lion's share of the first large public deal). This one curiously leaves out any mention of the size of the discount / mark-down. https://www.businesswire.com/news/home/20230623707825/en/Ares-Management-Acquires-3.5-Billion-Lender-Finance-Portfolio-from-Pacific-Western-Bank edit: This was in the 8K announcing the deal:

-

BHE sold another ~$300m + worth of BYD shares. https://di.hkex.com.hk/di/NSAllFormList.aspx?sa2=an&sid=2508&corpn=BYD+Co.+Ltd.++-+H+Shares&sd=26/06/2022&ed=26/06/2023&cid=2&sa1=cl&scsd=26%2f06%2f2022&sced=26%2f06%2f2023&sc=1211&src=MAIN&lang=EN&g_lang=en&

-

This lady pretty much called it correctly 12 hours ago -

-

I have an extremely basic question on BTC and BTC-linked products like CME BTC futures and ETFs based on a basket of futures. Doesn't the existence of BTC-linked derivatives undermine the inelasticity argument of Bitcoin that the supply is extremely limited? Don't these BTC-price-linked derivative contracts function like eurodollars in that they are completely elastic and can expand and contract the supply of BTC-denominated "money" outside the control of the US government (in the case of a eurodollar, or in BTC's case, the rules of the thing) ?

-

Warren put out a press release regarding his annual giving - https://www.businesswire.com/news/home/20230621049174/en/Berkshire-Hathaway-Inc.-News-Release

-

Today was a perfect example of the GNRC effect when hurricanes and power outages are in the news. Up 8% on no company specific news.

-

My whole point on Generac was that the stock of a standby generator company goes up when a bad hurricane hits. You wouldn't buy puts on it. It's not an insurance company.

-

I don't really advocate trying to hedge a specific sub-risk like that for an insurance company, but cheap out of the money call options on Generac used to be an effective pairing for hurricane season. I still think it's not worth doing and haven't kept up with GNRC since I sold it several years ago. Actually, looking it up the share price has come way down from its peak.

-

Well I appreciate the sentiment but we live in the City not the north shore. Sometimes I wish we didn't live in the city, but we'll see...

-

I think they were referring to Stora Enso on the OTC thing. They aren't OTC in their native country - just go to their website to read their earnings results: https://www.storaenso.com/en/investors https://www.storaenso.com/en/investors/reports-and-presentations ( @jks327 )

-

I'm 43 now. Been doing this (investing for a living) for 23 years now. We've basically stopped doing any construction / development, so I hope I don't get fat because of that. My hair is white but I still feel in pretty good shape. I probably drink too much but I do enjoy it LOL... On one side of my family (Father's), all the men died in their 50's. On the other side, the men all lived to over 100. Not sure what to expect!

-

In my experience, most people who say this fail to realize how small Fairfax India is within Fairfax Financial's investment portfolio. You aren't getting much exposure to FIH.U by buying FFH. You do get Digit when you buy the parent. I own both.