gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

It's all a political choice - raise the cap on payroll tax contributions, make some tweaks like Pupil suggested, write two paragraphs that allow SS to run a negative balance ("gasp!"), do nothing and deal with the voters... It is not some unsolvable issue that should keep people up at night and it really doesn't matter at all. Except to my 80 year old mother who will come for Marco Van Basten if he takes her $4k per month or whatever it is this year. She don't play

-

part 1: as long as the company trades in the market for more that book value, a dollar retained is worth more inside the company than paid out and taxed. repurchases will ramp up to very large numbers as the stock price approaches book value so it may never happen or be very very rare that it trades at .99x BVPS. part 2: Sure gotta believe Brian Moynihan was like, wait, what?!

-

He is buying the A shares. https://www.sec.gov/Archives/edgar/data/1067983/000119312526092556/xslF345X05/ownership.xml I loaded up whatever the opposite of a "large slug" is. Less than a small slug. At better prices than that piker Greg for sure but he has other things to do. But I also own a few remaining march 20th 470-strike call options so I welcome the news

-

Date yourself without dating yourself - How many?

gfp replied to rogermunibond's topic in General Discussion

oh my gosh they don't have turntables and vinyl records in OK ?? Too much tornado risk??! -

Marco's trying to steal my 80 year old momma's social security check! She's coming for you buddy. She don't play

-

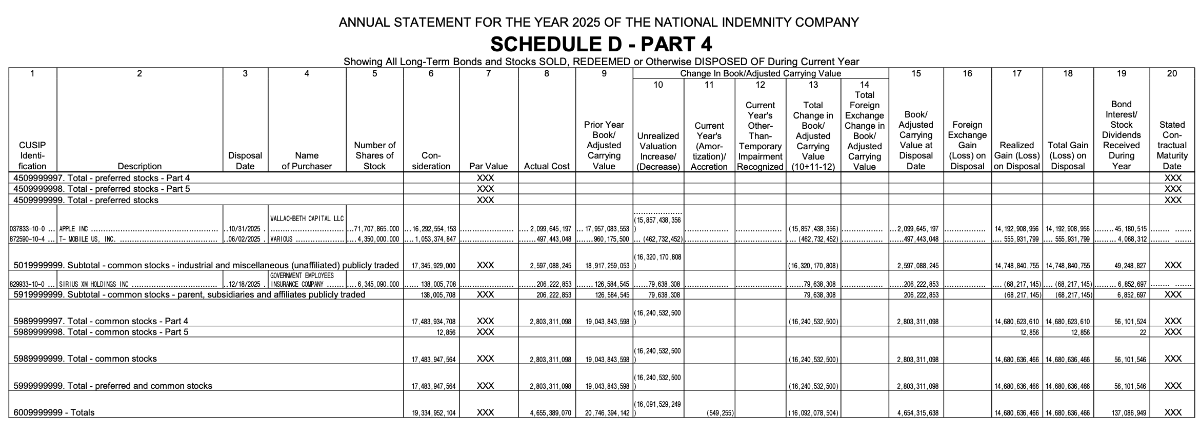

Odyssey Re year-end NAIC filing. Looks like they made a $2.5m investment in Sanjeev's fund back in 2017 and are down big? Is that correct? ODY_INV_23680.2025.P.AN.PI.O.M.5062491.pdf

-

20087.2025.P.AN.PI.O.M.5094174.pdf20087.2025.P.AN.PO.O.M.5094176.pdf

-

Date yourself without dating yourself - How many?

gfp replied to rogermunibond's topic in General Discussion

haha I saw this on twitter yesterday and I was all 20 also... Am I crazy that 'all 20' should be a super common answer? -

Time spent worrying about Social Security going "insolvent" is right up there with the biggest wastes of time possible. What social security pays out to retirees and on what terms is ENTIRELY A POLITICAL CHOICE. Social security trust fund's assets are GOVERNMENT IOUs. MONEY IS GOVERNMENT IOUs

-

Of course not. Have you forgotten Atlas's business model?

-

Thanks for posting. Dimon and others have been asking for this for quite some time. This is probably more important for @Blake Hampton to read and understand than all those Warsh dreams and promises

-

---------- Maybe its a positive then

-

Bloom Energy be bouncin' all around

-

Oh dang its a sale on foam clogs - call EF Hutton!

-

look at that size! you know what they say go big or go home

-

you may have heard about the hot war in the middle east that caused most Japanese stocks to fall last night. something about oil and inflation and worries and risk premiums...

-

There is a thread on this forum on MarketWise, which is the public SPAC vehicle that Porter's previous company merged with. He was forced out before the SPAC deal and then came in to try to run the place after the stock tanked and then left again when he couldn't get the public company's independent board members to approve a merger of his private publishing business, Porter & Co., with MKTW. The Berkshire piece is written under his current private company's banner - Porter & Co. I don't know if that youtube video mentioned it 'cause I ain't gonna watch all that, but Porter was also implicated in the murder of his close friend (Rey Rivera) in a Netflix episode of unsolved mysteries. (I don't think Porter actually threw his close friend off a roof to his death, this particular allegation was not credible - but it didn't help the brand LOL). I have an email of a leaked communication from Porter from Sept. 2024 where he is hatching up a similar hit piece campaign against Berkshire. They are designed to scare potential customers, many of which hold a large block of BRK stock they won't sell for tax reasons. Going after BRK gets views and attention (sorry, I contributed to that by posting it here) and gets higher engagement from the outrage factor. The Sept. 2024 campaign idea was to highlight Buffett's many blunders and then predict that PacifiCorp's legal issues would bankrupt the entire company (!!!) It was sent to me to get my take on the risk of Pacificorp spreading to kill the mothership. As you can imagine, I wasn't concerned that Pacificorp would bankrupt BHE, much less BRK. Berkshire stock subsequently went up in price and I don't know if he ever ran that campaign. These guys got seriously rich in the financial publishing industry as the industry evolved from the direct mail, rent a list of addresses and mail physical sales letters at great cost, to the rise of email marketing and they basically invented the "Agora Method" of creating free daily newsletters that end up with millions of subscribers and contain promotions for paid products between the "content." That huge funnel feeds entry level price point newsletters which feeds premium and lifetime subscription products with very high price points and maintenance subscription fees. Porter's former boss Bill Bonner is the wealthiest of the Agora crowd and his family are bona fide billionaires from 40 years in this industry. The USEC promo that got them into trouble (mentioned in the youtube video) was risky because it threatened their regulation as a "general interest publication" - it was important to settle that case because losing the "general interest" designation would nuke a business that was already worth hundreds of millions of dollars at that point. Anyway, sorry to muddy the BRK thread with this nonsense - Porter probably does it for the eyeballs more than believing in the content.

-

Wow, this was a seriously bad take https://x.com/Porter_and_Co/status/2028587479687995510

-

I thought this company's work was sort of interesting. Taalas is the name. They basically are turning finished AI models into a piece of hardware, all hard encoded, where it can run inference at ridiculously quick speeds and very cheaply. I don't know if this will go anywhere but they have a model (I believe its one of the decent open source models) encoded on a large chip and have put up a demo site where you can try it out as a chatbot. It is definitely not the most impressive chat bot - but you will not believe the speed at which it spits out its answer if you are used to Gemini Pro thinking or another similar "thinking" models. Obviously there are fast software models that are optimized for speed and cost but this demo model is really really fast. Company site here: https://taalas.com This is the chatbot demo -> The answers come in milliseconds https://chatjimmy.ai

-

I'll give one important one: spending your time thinking about Kevin Warsh and the Federal Reserve is a waste of time and youth. Get out there and dig around for actual good investments to make some actual money so you have a capital base to compound so you aren't completely dependent on the job market prospects for a new graduate with a computer science degree! Don't waste your youth! Time is precious

-

Remember, young man, that my advice was to attend the university of wabuffo (read: listen and learn), not "lecture wabuffo on monetary plumbing" I know old habits die hard but listening and learning (and even - gasp! - occasionally changing your mind!) is still a financially valuable skill to pick up

-

I love SSD! Now I feel bad about answering in the sky harbour thread

-

You got your photonics deal news from NVDA putting some money into LITE and COHR. I still think COHR is in the weaker competitive position of the two. Looks like their markets caps are about equal. You still holding COHR in your "fund"?

-

It's even worse if they are above equity method and into the range of consolidating because Statutory accounting (insurance regulators) hates goodwill and limits how much they will count towards capital.

-

I was going to write out a thing but instead I'm going to drink this glass of wine and let Gemini point out the misunderstanding -> ----------AI CONTENT BELOW THIS LINE ---- BEWARE!! ---- AI IS A BUBBLE AND SHOULD BE IGNORED --------- Here is a straightforward breakdown of why holding an appreciated asset at carrying value (book value) is a mathematical disadvantage for an insurer's capital position: The Math: Book Value vs. Market Value Insurance regulators (like OSFI in Canada or the NAIC in the US) determine an insurer's capital health by comparing their Available Capital to their Required Capital. Regulators assign a "risk charge" to different asset classes. For standard equities, this charge is usually around 30% to 40%. Let's use a hypothetical example where an insurer buys an equity stake for $100, the regulator's risk charge is 30%, and the asset's market value eventually doubles to $200. Scenario A: Held at Market Value (The "Economic Value" approach) Available Capital: Because the asset is marked to market, the $100 unrealized gain is recognized on the balance sheet. Your equity increases by $100. Required Capital: The regulator requires a 30% buffer against the new $200 value. Your required capital increases from $30 to $60 (a $30 increase). Net Impact: You gained $100 in recognized equity, but only had to "lock up" $30 of it. This creates $70 of newly freed-up capital that you can use to underwrite more insurance or fund other investments. Scenario B: Held at Carrying/Book Value (The Eurobank situation) Available Capital: The asset remains on the balance sheet at $100. You do not get to recognize the $100 unrealized gain, so your equity does not increase. Required Capital: The regulator requires 30% against the $100 carrying value. Your required capital stays at $30. Net Impact: Because you haven't recognized the gain in your Available Capital, you miss out on that $70 of newly freed-up capital.