Thrifty3000

-

Posts

637 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by Thrifty3000

-

Also, I don't think anyone should expect FFH to repurchase/retire an equivalent amount of shares upon termination of the TRS. It appears to me FFH is already using the cash payouts from the quarterly TRS gains to repurchase shares. That makes sense since they're repurchasing undervalued shares with cash proceeds from their undervalued TRS asset.

-

Regarding the TRS it sounded to me like Prem said: - all the major Canadian banks are the counterparties - the counterparties have hedging mechanisms to neutralize risk on their end - the banks can't call the TRS's before the contracted date - FFH has extended the contracts to at least 2025 (I'm not sure I heard that correctly, he may have even said 2026) - FFH can continue extending the contracts. My assumption is once FFH feels the TRS is no longer a bargain it will simply opt to not renew the contract (the exit price will factor in the underlying FFH share price as well as the carrying cost of the TRS).

-

LFG!

-

FWIW - I don't think anyone has already posted this here, and I hadn't seen it before I spent time digging on MW's site today - but on the day of the last FFH conference call Muddy Waters published a list on their website of specific questions and accounting discrepancies for Fairfax (this was separate from the original report). https://www.muddywatersresearch.com/wp-content/uploads/2024/02/Fairfax_MWQuestionsForQ423Call.pdf One example: "There is a $101.7 million discrepancy between what the acquirer reports paying for RiverStone, pro rata for Fairfax’s ownership, and the total consideration Fairfax reports receiving. The pro rata discrepancy grows to $335.4 million when looking at the cash consideration that CVC reported paying." I'm not qualified/motivated to assess the legitimacy of several of the claims. But, if anything raises an actual red flag, it might be worth asking Prem/Jen for clarification at the meeting.

-

From Jamie Dimon's annual letter... "we are prepared for a very broad range of interest rates, from 2% to 8% or even more" Notice he didn't say from 0% to 8% or even more. I believe recency bias accounts for much of Fairfax's discount to intrinsic value. Lot's of people heavily weight a return to zirp scenario in their longer term Fairfax model. Dimon lays out why he thinks 0% is off the table and why a higher rate environment is the more likely scenario. If Dimon is on the right track about rates then it seems baseline EPS estimates for FFH will be shifting closer to $200 as more investors/analysts' take zirp off the table and increase their expected portfolio yield by a couple hundred basis points.

-

I want the shares to triple overnight so I can exit and fly private the rest of my life.

-

Amazing analysis as always. Many thanks! Another datapoint investors should probably keep in mind is the fully diluted EPS. Looks like the fully diluted version of your estimates would land around: $146 per share for 2024 $149 per share for 2025 Fairfax’s share-based plans have a longer vesting period than most companies. So it’s less of a near-term concern, but something to be aware of.

-

Or, was Prem saying that he wouldn't be initiating tech investments, while the rest of the team is free to pursue tech opportunities as they see fit? That's how I interpreted it since they still have other tech investments in the portfolio.

-

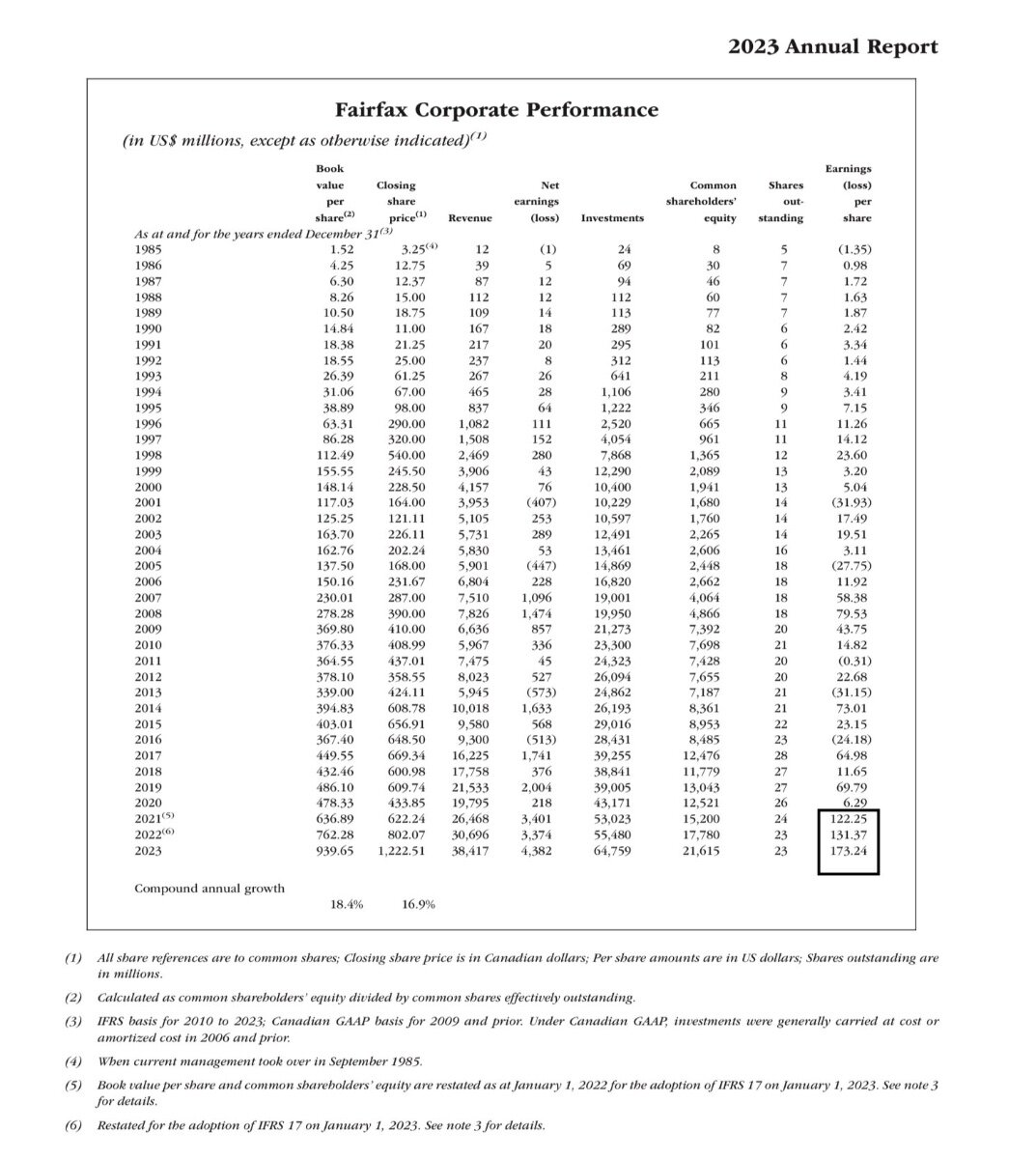

Step 1) Read this: "We had by far the best year in our history. A record underwriting profit of $1.5bn and net earnings of $4.4bn. BVPS increased 25% to US$940. In the last 3 years, our BVPS has doubled. Our operating income of $3.9bn may continue at these levels for the next 4 years.” - Prem Step 2) Study the last column, paying particular attention to the bottom right corner of this page in the annual report: Step 3) Combine knowledge gleaned from steps 1 & 2 and imagine how the chart will look four years from now. Step 4) Enjoy watching the share price climb to $2,000+ USD.

-

Elephant bumping

-

When FFH reports mind-blowing results and the stock price drops...

-

The headline was negative. The bots are doing their thing.

-

In what universe are you given ONE make-or break-question on a company’s conference call - where everyone knows your intent is to take down said company - and your ONE question is WHY DON’T YOU DISCLOSE MORE INFORMATION?? Oh brother, that was really pathetic. FFH is worth $1500 to $1800 USD per share. Kudos to Prem & Co. for a job very well done!

-

Raised the earnings guidance floor from $100 per share to $125 per share, excluding investment gains, for the next few years. (Prem said “of course there are no guarantees.”)

-

Excellent. Thank you.

-

This is. Four years is an eternity in Mr. Market years. This stock is going to be worth SO MUCH more 4 years from now.

-

I’m assuming it only impacts balance sheet (and book value).

-

Quick question: Do reserve releases flow through the income statement?

-

If you want to see what legit short cases look like I recommend getting on the Hindenburg email list. Here is their short du jour (for a company called Temenos): https://hindenburgresearch.com/temenos/ And here’s the 25%+ beat down on the Temenos market cap. Notice after extensive research - including dozens of insider interviews - Hindenburg lists over 20 specific questions for management that it is confident management can’t answer favorably. These guys do a lot of quality work. I’ve never taken a short position, but I find the Hindenburg reports interesting. Key takeaway: MW’s work on Fairfax is amateur-hour in comparison to Hindenburg.

-

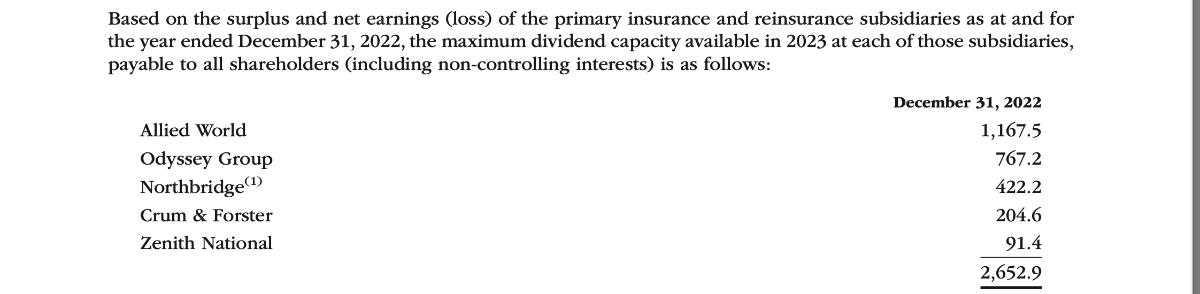

I don't think there's a risk of getting burned by the TRS. According to the annual report there's over $2 billion of subsidiary dividend capacity. Also, there's more than enough undrawn capacity on the credit line.

-

If you want to know if a short has teeth take a look at the bonds and preferreds. Example, look what happens to bonds after a Hindenburg hit.

-

+1. It’s unusual how little command of the facts Block has when asked to comment on things falling outside the scope of the written report. Imagine if you’re the counterparty sitting on $150 million of losses on your FFH TRS position and you’re worried about FFH reporting a blowout quarter. What’s it cost to get a guy like Block to pump a short thesis so you can reverse the $150 million loss and exit? $10 million? The ROI is pretty irresistible. Follow that money. (Who are the counterparties now?)

-

Curious if MW will be making anymore media rounds today.

-

I bought more today too. Reinvested the dividend.

-

In 2011, when Jefferies was under attack, I remember the CEO, Richard Handler, started posting daily updates of their financial statements on the Jefferies website to show customers and investors the short thesis was wrong. I'm curious if Prem could expedite the earnings release to today, open up the books for regulators and welcome them in with open arms, and then announce a million share buyback. Gotta pull out that elephant gun.