MMM20

-

Posts

3,354 -

Joined

-

Last visited

-

Days Won

14

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

Right and by extension the best comp for FFH might not be BRK, MKL, WRB or IFC but actually an old school, early 2000s era Yale-backed LBO fund buying private businesses at like ~3x EBITDA with ~50% ring-fenced leverage on each position. That’s a different sort of structurally advantageous leverage profile but probably a similar risk/reward to Fairfax’s nowadays. I’m not sure how many people think about it that way.

-

Just wanted to circle back to this after ruminating on it excessively . I came to FFH from a “publicly traded investment vehicle” sort of lens and that’s still my primary framework. My sense after following the company for a few years is that for others with a similar perspective, the capitalized value of the structurally cheap borrowing gets overlooked - lost in the shuffle in the analysis despite being a big chunk of intrinsic value. Whichever way you approach it, it’s hard to see how fair value isn’t at least 30% higher and probably more like 50-100% higher - if not even well beyond that as @Hamburg Investor did a good job laying out.

-

I still don’t discount how difficult it was to actually execute that strategy over so many decades. It all looks so oblivious and easy in retrospect but Buffett still the GOAT even if leverage explains much of it. Luckily (for us) Prem had the same insight - and now the whole business is morphing toward quality, at least as a few of us value nerds define it. History doesn’t repeat but it does rhyme. Let’s debate it, Mr. Block

-

Agreed and I know I’m mostly preaching to the choir. My main point was that fair value is clearly well above accounting book value and mainly for this reason, however exactly you frame it. We can disagree how much above (for me quite clearly minimum 1.5x book), but how does it make any sense for this to still trade barely above liquidation value? I wonder if the market is actually still missing that main point or if I’m the one missing something stupid and getting lucky, in which case I need to cut this in half at least. Paranoia.

-

I disagree with your corrections. 1) Yes of course the assets show up with an offsetting liability. But that’s missing something: the structural excess delta between the return on those investments and the cost of that financing. FFH doesn’t have to borrow at 6-8% because they can borrow at 0% by underwriting to breakeven. And that shows up in the income statement in higher earnings but not fully and properly on the balance sheet. That piece of the whole thing is an intangible asset that the accountants understate and our job as analysts to fix that. Right? I make a conservative assumption for that delta and capitalize it. Isn’t that the accurate way to handle it? 2) I’m talking about the ability to underwrite to breakeven or slightly better in the long run through cycles and volatility. The year to year volatility shouldn’t factor into the assessment of intrinsic value given sufficient discipline and quality on the insurance side - and they’ve proven that at this point IMHO. Does that make sense? What am I still missing?

-

As long as you realize Mr. Buffett disagrees with you - he has written about it extensively for decades and it explains nearly all of Berkshire’s excess returns in the middle decades if you really dig into it. He has even said that he wouldn’t trade $1 of float for $1 of equity. What does that mean for intrinsic value? This is the key question for FFH investors nowadays IMHO.

-

I just have a hard time understanding the view that this should trade anywhere close to book value when the $30B+ of float does not show up as an asset on the balance sheet. Adding this structural ability to borrow tens of billions of dollars at 0 or better into to our estimate of intrinsic value, I can’t see how one can credibly argue that the output is anything less than 1.5x book and probably much higher. Buffett taught us this decades ago so I’m not onto something clever. What is the counter argument? That leverage - even of the highest possible quality and at their scale a nearly irreplicable (smart folks have certainly tried) economic asset not liability - introduces so much volatility that it flips to fragility and therefore merits a much lower valuation? Lower than anything else out there?

-

How does the massive float at FFH factor into your calculation of intrinsic value these days?

-

I've felt this way every quarter for the past few years. And yet. Give it a couple months. Or at least a couple days!

-

wait, did I imagine him saying “goddammit” before they cut off his mic?

-

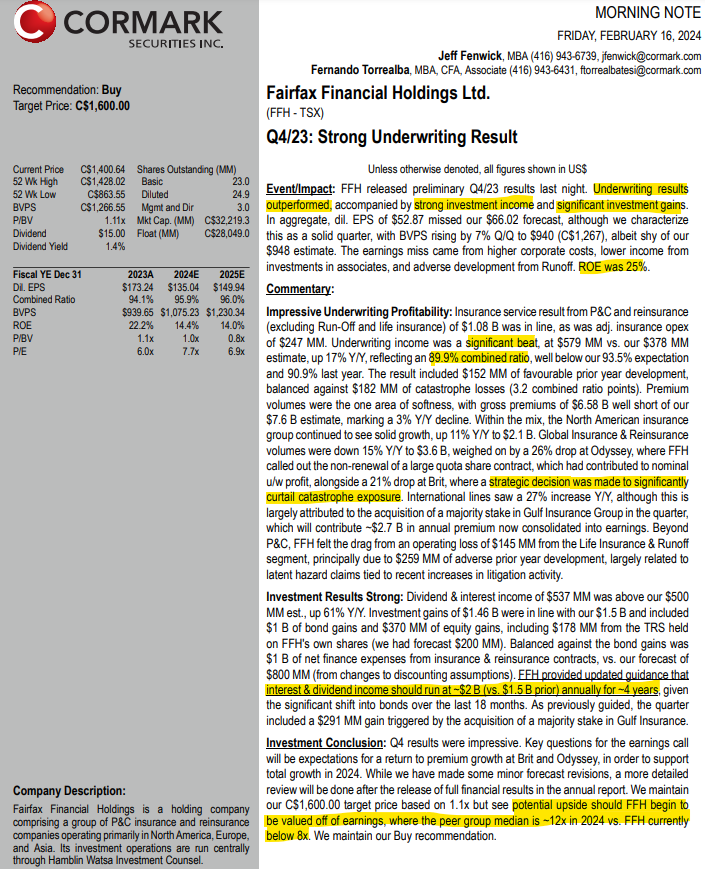

"We maintain our C$1,600.00 target price based on 1.1x but see potential upside should FFH begin to be valued off of earnings, where the peer group median is ~12x in 2024 vs. FFH currently below 8x."

-

Don't get lost in the weeds. They're expecting interest and dividend income alone of ~$2B for the next four years. That is up from ~$1.5B previously. That's just interest and dividend income.

-

Looks like another nothingburger.

-

The stock should be +50% tomorrow. Again, to be clear, it won’t be, but it should be. Anything below US$1500 is a farce with these results and outlook.

-

-

Don't we want them buying back as many shares as possible (without stretching too thin from a liquidity POV) at the current discount to intrinsic value - even if it makes them a bit less likely to get into the TSX 60? Would getting into the TSX 60 be so meaningful as to push the stock well above IV, giving them a good opportunity to issue shares? Does that tend to be the effect of TSX 60 inclusion? Idk what to root for.

-

Once you have the platform to pull off a few of these and make tens of millions, who cares? You ride off into the sunset or just hang out on your Texas ranch with your tigers and shoot at cans or whatever. You see the incentive to manipulate markets without repercussion. We should eventually see a crackdown on this sort of behavior.

-

Fair enough, and that's why I just read Bloomstran's opuses breaking down intrinsic value in gory detail. I guess therein lies the opportunity.

-

Our guy @hardcorevalue with a great summary https://tidefall.substack.com/p/short-attacks-and-tobacco-stocks

-

The question is if/when this ever becomes the consensus view. Maybe a fool's errand to even think about.

-

Maybe I’m not honorable enough but this didn’t bother me. I don’t check my facts with management before broadcasting an idea (even shorts) most of the time. What bothered me was pretty much entirely the whole “using your big platform to spread misinformation to move the market for a few days” thing.

-

@Viking so in this analogy is Carson Block sitting at home with a big bet on Atlanta screaming at his TV the whole fourth quarter? Or some prominent Pats hater on TV screaming “DEFLATEGATE!* SPYGATE!*” as they march to victory? Or a ref who throws a flag on the last drive only to get overruled on replay review? Or maybe just a drunk who passed out in his truck in the stadium parking lot before the Super Bowl even started? *both wildly overhyped nothingburgers

-

So when you do the analysis yourself to come up with an economic fair value, not accounting book value, what do you come up with? And how much did it change after MW’s report? Please let us know.

-

Sounds like might be news to you that accounting is only ever a crude approximation. “And it's not that hard to understand. But you have to know enough about it to understand its limitations because although accounting is the starting place, it's only a crude approximation. And it's not very hard to understand its limitations.” -Charlie Munger I’ve been arguing for years that FFH investors were being overly backward looking and book value accounting focused, missing the firehose of cold hard cash about to start spraying them in the face. But sure, let’s quibble over how the accountants value things a few % points in either direction when Fairfax have quite clearly lined themselves up to generate nearly the entire current market cap in cash flows over the next few years. It’s asinine.

-

BTW what they’re accused of is marking a $94 business at $100. The idea that that business is earning $15-20 in annual cash flow isn’t even in dispute.