MMM20

-

Posts

3,353 -

Joined

-

Last visited

-

Days Won

14

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

https://east72.com.au/wp-content/uploads/2024/04/E72DT-Quarterly-Report-March-2024.pdf

-

?

-

https://www.valueinvestorsclub.com/idea/FAIRFAX_FINANCIAL_HOLDINGS/8951778558 Fairfax write-up on VIC from Feb 14th. Sorry if this has already been posted. "MW never discusses the earnings power of the business. Why? Because it makes a mockery out of the short thesis. In my opinion, the company, helped by higher interest rates and a hard insurance market, will be able to generate north of $200 per share in EPS per annum for at least the next three to five years. "Muddy Waters never states what the company is worth and why. It ignores all disconfirming evidence and ignores the elephant in the room – the earnings power of the business. When a company is trading at five times net income, MW must expect earnings to collapse, and if they don’t how will the short work?"

-

Zoom out… and BTW the stock was up this month.

-

Why does higher volume imply shorts adding?

-

@dartmonkey I believe it was addressed by those who rightly pointed out that leaving some money on the table in any particular transaction is not inconsistent with the fiduciary duty to shareholders.

-

It would be cool if a Canadian insurance company still trading at mid-high single digits P/E ends up being the best way to invest in the Indian growth story over the next decade (ironically maybe even better than Fairfax India)

-

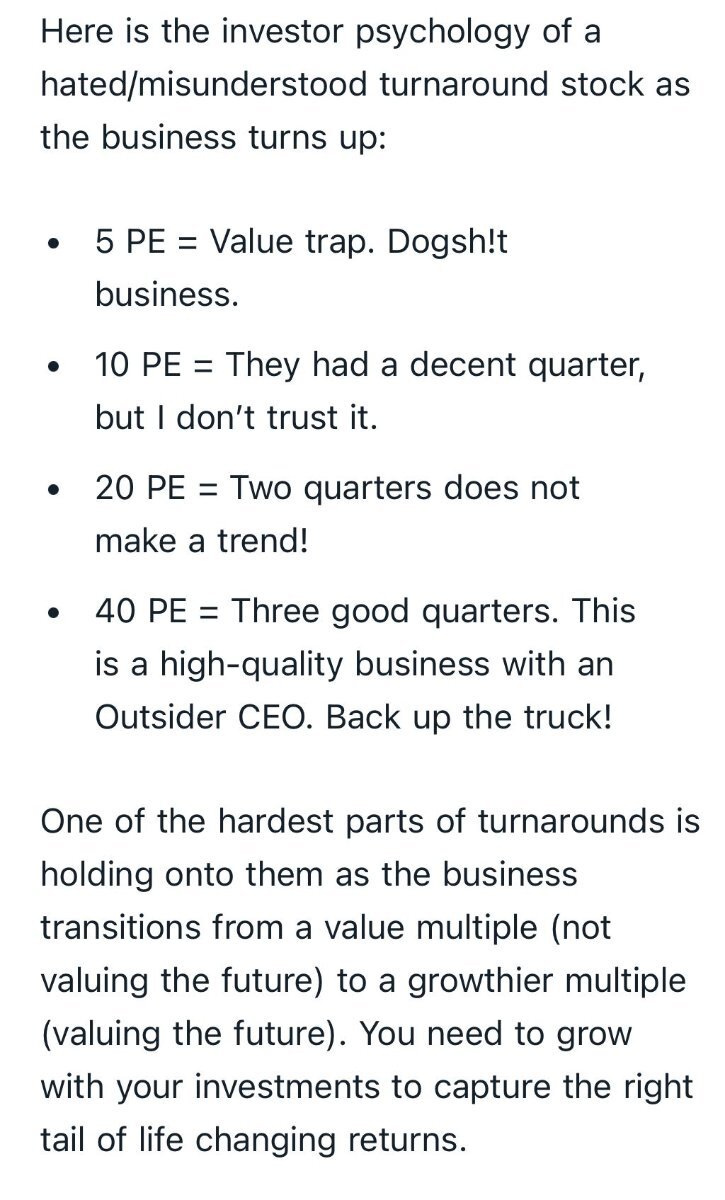

"The key in investing is finding growth in value. You want to find something that is undervalued that can get overvalued. I’ve found you make the most money by having a 1–3-year variant view on a business and buying the stock before the business turns up, inflects, or accelerates. You must be willing to buy and hold dead money and look wrong before you’re right." https://microcapclub.com/turnarounds/?ref=newsletter Feels like FFH is at the "They had a decent quarter, but I don't trust it" phase:

-

Right, so projecting gains in the equity portfolio is not an aggressive assumption whatsoever, contrary to what skeptics and bears might say. Accounting for mark-to-market investee retained earnings - full lookthrough earnings rather than just the piece paid out as dividends - in our normalized underlying earnings power really is the most accurate way to think about it. Investors trying to get the big drivers right should be aware of this (and I'm sure most here probably are) because it's something like a $500mm-$1B difference nowadays. It's not a trivial point. I wish Prem would lay this out in the letter but I understand why he doesn't.

-

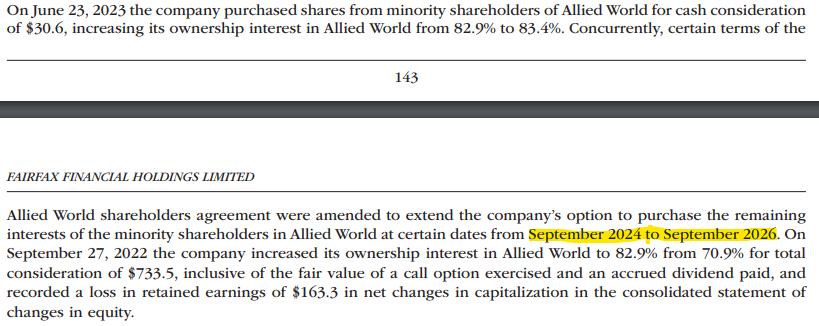

For Allied World (from annual report) -

-

Thought this quote from the WRB CEO was worth highlighting here... "Social inflation is -- it's become a bit of a buzzword in the industry. And I think just to level set it, all it is, is a reflection of a shift in society and by extension, a shift in the legal system and what's coming out of the legal system. The awards today are a multiple of what they once were. Beyond that, are there other things that are driving it? Sure, you have things such as litigation funding, along with other bits and pieces. But the big driver is just the social environment and how once upon a time, when damage was done, the legal system was there and by extension in the insurance industry to help make people whole for those damages. Today, it's a different environment where it's not just about making people whole for damages, it's also about punishing when in the eyes of a jury or sometimes a judge that there was a wrong done. So that shift, I think, is having a great impact on loss cost in general. And there's nothing that I see as far as that really slowing in any way, shape or form...Ultimately, when the day is all done, I think there's a bit of a misperception in the eyes of much of society. And that is, who pays the bill in the end? When it's a defendant paying the bill, they really don't pay the bill. It's the insurance carrier. And actually, the insurance carrier in the short run will pay the bill but ultimately, it's society that pays the bill because everyone's insurance costs go up as we are seeing that today." - WRB CEO

-

I don't mean to single this guy out, but maybe this is indicative of the marginal shareholder's mindset and partially explains why the stock remains so cheap (in addition to all the typical old biases and misconceptions). https://emergingvalue.substack.com/p/portfolio-updates-february-march I sold my Fairfax financial with a comfortable profit since I bought in Sept 2022, when muddy waters released their short report. I had bought Fairfax sometime recently when rates were starting to rise. With such nice gains in a very short period, and no idea of the impact of the short report, I sold. That could be an error to react quickly, because it looks like it is a good quality company. Anyway, with the proceeds I added to existing ones. I am not an expert on insurance, but it’s clear that the book value is aggressively noted, with some assets benefiting from an epic bubble in Indian equities and overvalued US real estate, as well as temporary high interest rates. It does seem that earnings are above the normal trend. The company keeps performing well and is cheap based on current high rates elevated earnings, so It was not the best sale. I think that is it still a good company for the long term.

-

Yeah I had to read that same sentence a few times. He needed an editor there.

-

Why doesn’t Prem account for the retained earnings of their mark to market investee companies when talking about Fairfax’s normalized earnings power? Of course dividends are only a small piece of what matters. He even mentions that the $15 dividend is only about 12% of FFH’s own operating income (IIRC) but doesn’t make this point for their mark to market investees, right? Normalized earnings power should be $150-200/share and maybe he just wants to set a lower bar? Or maybe he would argue it’s captured by the idea that they’ll sell stocks for gains over time? What am I missing? Of course we can just make the adjustment ourselves, but the way he’s doing it is selling their underlying earnings power short. Anyway, that’s my one complaint about what’s otherwise a masterclass - a great letter.

-

Circling back on the sizing thing, I thought this was a helpful framing: https://harveysawikin.substack.com/p/value-investing-lessons-from-major My sense is that this one's something between "Long-Term Champion" and "Medium-Term Performer" (more the former IMHO) and I'm planning accordingly. In the mid-00’s, I established a managed account for my children at a brokerage. When I took personal control of the account in 2010, I sold several of the positions and with the proceeds bought Microsoft, making it approximately 20% of the portfolio. Since then, I have barely touched the account, and now Microsoft represents 75% of the value, having mightily outperformed the rest of the stocks. The overall return on the portfolio has been increasingly converging with the total return on Microsoft since 2011 and, if the latter keeps performing, this will be even more so. Admittedly, not every stock is a Microsoft, and if I had let, say, Disney grow into a 75% position, I would have been upset, and my long-term return compromised when it halved a couple of years ago. I have given this dilemma a lot of thought and have concluded that the two approaches (sell positions at fair value vs. hold everything static forever) are irreconcilable. You can, however, draw lessons from each one to try to generate attractive returns without taking reckless single-stock risk. One way to do this is to separate your portfolio into three main categories. Long-Term Champions are companies you believe to be long-term compounders. A stock like that should be held, trimmed sparingly, and only significantly reduced when it becomes highly overvalued, or changes in some fundamental way. Fundamental change is not something that cannot happen to a Cézanne but can and does to a company, e.g., because of macro events, technological disruption, or management changes. Medium-Term Performers are companies you like but cannot visualize as a potential Cézanne. Here it becomes more important to manage its weighting in your portfolio. Cyclicals such as resource companies go in this bucket, since they are vulnerable to large commodity price fluctuations over time. These kinds of stocks can graduate to the top category if they have excellent managements and/or operate in the right sectors. Of course, medium-term performers can also be downgraded to the uninvestable category. Arbitrages are stocks that you think are currently undervalued and where you see a catalyst for value-recognition – but have no conviction beyond that point. In these cases, you need to remember to sell when the stock reaches the range of fair value, and if it is not very liquid, to leave something on the table for the market. In the past I have made the mistake of holding onto less liquid stocks for the top tick and finding it hard to sell on the way back down. A framework like the above cannot be applied mechanically because the markets are always presenting investors with new circumstances. Still, even if it does nothing other than make an investor hesitate before deciding to reduce a Cézanne or Matisse stock just because it “went up a lot”, then it is valuable.

-

smart kid

-

I hope they never split the stock. If you can’t do the absolute bare minimum to understand that the share price alone is arbitrary and meaningless (and you can buy partial shares at seemingly every broker these days) then buy an index and focus on other things. Not splitting the stock is one way to attract the investors they deserve, at least on the margin.

-

Sounds like we're in a similar boat. I'd sold the BRK in my retirement accounts a few weeks ago to buy ~10% more FFH on the Muddy Waters report, and I just sold those extra FFH shares and bought the BRK back ~3% higher. But it's small and I sense that my return expectations are lower than most. If I can just beat cash owning a little bit of BRK as a cash substitute, I'll be happy. If BNSF and BHE are as troubled as he suggests, I might be nervous if I were one of those people with ~80%+ of my net worth in it with, like, a ~$10 cost basis... a high class problem!

-

He’s said so himself and it’s the source of blowback from Marc Cohodes and others who think it’s unethical.

-

Any reason to believe he didn't cover almost the entire thing the day of the campaign, as he often does? If there is, I haven't seen it.

-

The opposite of respect is not really disrespect but indifference. Probably time for him to fade into irrelevance.

-

A couple years ago I would’ve said that’s a huge intraday swing in a megacap. Efficient markets.

-

I always assume his top priority by far in any political thing is avoiding nuclear war. It’s been that way for 6+ decades now, right?

-

+1 and I wouldn’t be able to write anything if my best friend just died. Re BNSF and BHE, even if we take his comments at face value and assume they might really invest the minimum incrementally (and maybe even take capital out), investors have to keep in mind that ~10 years from now BRK’s assets should be ~60-70%+ about the incremental investment decisions between now and then. It’s still about the cash generation and capital allocation rather than any particular asset. Do you trust Greg, Ajit, Ted and Todd? That’s almost all that matters. And maybe WEB actually lives to 112.

-

Right and by extension the best comp for FFH might not be BRK, MKL, WRB or IFC but actually an old school, early 2000s era Yale-backed LBO fund buying private businesses at like ~3x EBITDA with ~50% ring-fenced leverage on each position. That’s a different sort of structurally advantageous leverage profile but probably a similar risk/reward to Fairfax’s nowadays. I’m not sure how many people think about it that way.