MMM20

-

Posts

1,871 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

Never attribute to malice that which can be adequately explained by stupidity. Hanlon’s razor.

-

-

Really looking forward to this one!

-

Base rates are skewed heavily against us in the very long run, and something could blow us up over the next few years too. But we are looking for wildly mispriced bets and this is *still* a fat pitch, IMHO - arguably more so than at ~$350 ~3 years ago. I get the argument for selling some if it has become a huge position, though. A famous investor once told me that if you're lucky enough to find yourself in this situation and struggling with the sizing decision, no one ever went mad (or broke) just cutting it in half. I'm constantly reminding myself that given a high enough rate of compounding, even ~7%, you double your money roughly every decade. Then you just focus on your lifespan/healthspan. The exponent is really what matters. Longevity of compound > everything. That might be the #1 lesson from Buffett, IMHO. Well, that and the value of float ~5% cash is looking pretty damn good right now… but our "problem" is that Fairfax might be the single best way to invest in that thesis! Appreciate your thoughts!

-

@StubbleJumper the fact that you see it that way makes me think I’m missing something. That's a good thing and I am grateful for that too. Seems like the big vectors are lining up as if we are still in the early-middle innings, which is clearly not consensus! Of course 1100 bps of spread between investment returns and borrowing costs is unsustainable in the long run. Maybe the counterpoint is we could easily end up with 3 more years of wide spreads and then some reversion to the mean, which could easily mean $4-5B+ annual cash flow thereafter through the cycle if we get good to great capital allocation. I don’t know. In other words, even if the current state of things *is* more like a windfall than a new normal, well, it seems like a windfall of such magnitude that with good capital allocation it should permanently transform the earnings power either way. That is not priced into the stock. “To date, 2023 has been a significant catastrophe year with some estimates suggesting that U.S. insurer losses have already surpassed $25 billion this year. The events this year had been broadly felt with 44 states affected by 43 events. At the company level, these events have added 4.5 points to our combined ratio year-to-date, which is 1.7 points higher than the impact catastrophe events had on our combined ratio for the first half of 2022. Our property business has been most affected by catastrophes, adding almost 46 points to the property loss ratio so far this year, which is about 16 points more when compared to this time in 2022." - Progressive CEO Susan Griffith My underlying point is this. What if Fairfax has proven to be a truly world class company on both the underwriting and investment side of things? What are the implications?

-

I could not disagree more with this approach or characterization. The ability to underwrite profitability and operate for long term shareholder value creation and not short term optics is a massive moat in this industry full of bureaucrats and hired-gun MBAs who nearly blew up their collective balance sheet by simply matching duration risk and sticking with long terms bonds even though interest rates were at 5,000 year lows — human nature and principal agent problem, misaligned incentives. You can’t afford to risk looking dumb for a decade if you dont have an incredible 25 track record and huge personal ownership. That more than any cost advantage is what makes a moat in this business. That will not change anytime soon, even when capital re-enters and drives underwriting profitability down. Prem did what was right from a risk/reward perspective of a permanent owner and it has structurally transformed the cash flow power of the business going forward. This is far from reflected in book value right now and an output of it may very reasonably be, with conservative assumptions around underwriting and investment returns, that book value triples over the next decade. Because the cash flows and incremental return on those retained are what matters. And a stock is worth the net present value of future cash flows, not what the accountants say it is worth based on historical artifacts. Accounting book value almost completely misses the point in this case at this point in time, and nearly all others. Respectfully, investors are totally missing what is going on here if you they are focused on that metric. It is useful just to understand how the stock may trade in the short run, I agree on that much. Anyway, sorry, this gets me fired up, and maybe I’m wrong. I’ve been dead right on this for 2.5+ years now on my biggest position by ~3x in the face of skepticism bordering on derision so maybe I’m just riding high and overconfident. “What do I know?” — Montaigne I guess this is what makes a market!

-

I’ve yet to see anyone arguing FFH should trade at even a market multiple. Have you? Half that would be a ~2x! What if the board actually skews too cautious - too quick to tamp down enthusiasm and assume there is a shoe to drop, or that we’ll revert to some worst case scenario for underwriting profitability and investment returns? Maybe we are still too anchored to 2010-18 and not believing the new reality, because we as value investors reflexively blanch at anything that sounds like “this time is different.” Maybe there really has been the fundamental transformation in through-cycle earnings power (even assuming breakeven underwriting) that many of us think we see here, and Mr Market has just been slow to react b/c he is anchored to the recent past. Frankly, I could argue that the stock is easily worth $3,000+ USD to a permanent owner right now — with slightly better than breakeven underwriting through cycles, more historically normal interest rates and equity returns, and great capital allocation — if Prem and team prove to be great capital allocators for another decade or two or three. Wait until Mr Market starts doing the math again on what ~6-8% investment returns translate to for shareholders when sustainably levered ~1:1 - ~2:1 with the best possible type of leverage. I think many people are still afraid to get laughed at for doing that math. But what if that’s reality? And BTW Charlie Munger tells us that he welcomes downturns because great businesses take share when their competitors are in distress. Does that not look like Fairfax right now? And in large part b/c they were willing to look stupid and not reach for yield… b/c of a sustainable structural advantage. I assume I’ll be laughed off the board for that but there’s your enthusiastic valuation level

-

Thx. Still, they have plenty of ridiculously liquid assets to sell in a bad scenario, right? I can see how that view is too simplistic if the subs need all that capital to operate… but they can always pull back on growth and generate capital. Wrong way to think about it? Maybe if the stock hits a rough patch they’ll consider selling ~10% of another sub or another hidden trendy asset like pet insurance for a huge premium and buy back another big chunk of shares… those decisions are looking better and better by the week. Prem capital allocation haters increasingly in shambles. BTW, look at the trailing 3, 5, 10, 15 year returns as of now. The skepticism tends to fade when the trailing returns look good. Less career risk. Expect the compounder / quality growth crowd to return in full force soon. Not to mention the closet indexers and momentum types. And yet still ~6x P/E. Still there for the old school value guys too

-

I don’t get the concern. Don’t they have $30B+ in liquid fixed income? $40B?

-

@StubbleJumper idk… i think he pretty much said he’d like to buy back stock up to $1375 this year, which in his mind is still a significant discount to IV (which he’ll leave us to calculate for ourselves). He just told us he thinks the incremental ROIC on a purchase up to that price would be 15%+. Maybe he spoke out of turn or said too much, but idk how else to interpret it. I think IV is $2000+ as youd expect to earn a fair ~10-12% return from that point, but I’m a broken record and that’s a whole nother can of worms.

-

Thanks! So here's my follow up question. Given Prem's statement today, why wouldn't FFH go to CAD 1,375 almost immediately? The Prem put...

-

Would someone please explain this bit for the slowest among us?

-

I thought the whole point of Poseidon locking in contractual cashflows (and missing the short term spike in spot rates) was to benefit from this exact scenario, when spot charter rates eventually crashed, as they always do! Does Poseidon not have a solid cash flow stream locked in for many years? And did they not build inflation escalators into their contracts? Thanks.

-

What about little old MMM20? I taught Trevor Scott everything he knows. He just has a better PR operation

-

BVPS ~$834 + ~$33/share fair value excess of carrying value of associates = ~$867. Does the stock gap up to $900 tomorrow? Let’s see.

-

Thanks all for the responses and especially @Maverick47 for helping me understand the Florida/California dynamics better. I still will not be surprised if the hard market reaccelerates in certain pockets and in fits and starts and Fairfax ends up cash flowing its whole market cap over the next 4-5 years or so. The supply side / capital formation dynamics just seem increasingly wacky. I’m not sure how they get generally better across the board anytime soon and we know Fairfax will grow aggressively into pockets of strength.

-

Right. Are we actually still going the other direction? Supply seems to be dropping off. What if we’re in a structurally hard market, at least in certain pockets, b/c the supply side is falling apart even as demand accelerates? It seems like those in a position of strength can almost name their price in certain areas. What’s the math on FFH intrinsic value if pricing is up massively over another few years and we end up $10-15B of new float just by taking price. Am I missing something? Not possible b/c no reinsurance? Of course always worried that rate still doesn’t match risk! Premiums are rising, but so is everything else—and insurance isn’t yet expensive enough to deter buyers, with utilities and property taxes representing a bigger share of the price of a house. Even at twice the cost, insurance would “still only account for a small proportion of asset prices,” says Danny Ismail, a researcher at analytics company Green Street. https://www.bloomberg.com/news/articles/2023-07-27/homebuyers-ignore-risk-of-climate-change-insurance-meltdown When Farmers Insurance Group on July 12 said it would stop writing new homeowners policies in Florida, it became the 15th insurer in the state to take that step since early last year. Florida officials fault widespread insurance fraud for the exodus, but Farmers said it needed to “manage risk exposure” in a place where climate change threatens more natural disasters. Florida’s slow-motion insurance meltdown is happening as new people pour into the places with the greatest risk of flooding, a pattern playing out across the US. Almost 400,000 more people moved into than out of the nation’s most flood-prone counties in 2021 and 2022, double the increase in the preceding two years, according to real estate firm Redfin Corp. Counties vulnerable to wildfires and heat have also seen more people arrive than leave. Insurance cost is the main way the market signals risk to homeowners. Yet in California, Florida and Louisiana the markets are flashing warnings that homeowners are largely ignoring. “There are definitely disruptions in the feedback loop,” says Nancy Watkins, an actuary at Milliman Inc., an insurance consulting firm. Why aren’t property owners taking the hint? A Fundamental Mismatch Mortgages last 30 years, while insurance premiums are adjusted annually. When the climate was stable, Year 1 was a pretty good predictor of Year 30. But rapid warming means the perils are constantly growing, so the premium for the first year could be wildly off 10 years later, leaving homeowners at risk of far higher premiums later on. “The entire system is predicated on climate stability,” says Spencer Glendon, founder of Probable Futures, a nonprofit dedicated to climate literacy. “I think we can expect that nexus to break down soon.” ● Demographic Danger Many people moving to risky areas are retirees thinking about little more than warm weather and lower taxes “who accelerated their retirement plans,” says Benjamin Keys, a professor of real estate at the University of Pennsylvania’s Wharton School. “They haven’t experienced a weather disaster.” It doesn’t help that most people—and developers—have short memories about destruction. Or that building codes and zoning can’t keep up. ● Information Breakdown Even when buyers seek reliable information on long-term risk, it’s hard to find, with some government maps of severe flood zones dating to the 1970s. Homeowners in those areas must purchase flood insurance to get a federally insured mortgage, but people outside the zones—or those who own their home outright—have no such requirement. First Street Foundation says some 6 million homes that should be considered at severe risk of flooding lie outside those zones. And Milliman estimates there’s $520 billion of unpriced flood loss in the housing market—a number that will only increase. Then there’s the question of how much insurance should cost. Carly Fabian of consumer-rights group Public Citizen says buyers deserve access to average home insurance prices by ZIP code over time, which would help them assess where insurers believe risks are spiking and whether they’re paying inflated rates. But insurance companies have blocked such efforts, saying the information is proprietary. “They’ve proven unreliable narrators on climate,” Fabian says. ● The Government Backstop In the 1960s private insurers largely pulled the plug on residential flood coverage, deeming it too risky. The federal government stepped in with the National Flood Insurance Program (NFIP), which racks up about $1.4 billion a year in losses because it can’t charge market rates. Similar state programs in California, Florida and Louisiana only insure homes that can’t get private coverage, but with insurers backing out, they’re adding customers rapidly. Florida’s Citizens Property Insurance Corp. is already the largest single insurer in the state. The Federal Emergency Management Agency is promising reforms that will bring NFIP premiums more in line with climate risks, but Keys is skeptical. “It’s like a dad threatening to turn the car around when the kids aren’t behaving properly,” he says. “The government isn’t not going to step in and bail out people when there’s a disaster.” ● Not Yet a Deal-Breaker Premiums are rising, but so is everything else—and insurance isn’t yet expensive enough to deter buyers, with utilities and property taxes representing a bigger share of the price of a house. Even at twice the cost, insurance would “still only account for a small proportion of asset prices,” says Danny Ismail, a researcher at analytics company Green Street. But investors in mortgage-backed securities may soon start demanding coverage for the full length of the loan. “The common denominator is that risk does not really belong to the insurance companies; it belongs to the community,” Watkins says. “The insurance market is not sufficient to tackle this problem.”

-

@Viking my only comment would be to hide gridlines - ALT WVG (yes I still have investment banking PTSD)

-

I agree! The family control + massive skin in the game —> management for long term wealth creation, not income statement optics really is a massive and durable competitive advantage. Permanent owner style value investing + float = structural durable high returns through cycles. Sort like an individual investor with a 3% 30 year mortgage and no asset/liability mismatch (no quarterly or annual client liquidity to worry about)… but on steroids! They’ve proven that over almost 4 decades and we saw it play out in a big way over the past ~5 years. It seems to me that from this point on through cycles they should durably and structurally earn a ~400-600 bps spread on their mostly cash/ short term fixed income plus some longer duration investments, vs roughly zero or slightly negative borrowing cost. So therefore the recent float growth has added ~$1B of structural earning power that did not exist ~5 years ago, driven by savvy insurance acquisitions/turnarounds —> growth into the hard market. (BTW that incremental earning power would be roughly zero if they’d had to issue ~6-8% debt to finance all that incremental growth after the acquisitions!) Looking forward, that growth alone is worth an incremental $500+/share which is not reflected properly in accounting BV. IMHO that is the core of the opportunity! That’s my best Prem impression!

-

@SafetyinNumbers@Parsad I respectfully disagree! All that matters in the intrinsic value calculation is the net present value of distributable cash flows to a permanent owner. So all I care about is the core cash flowing power and how it will be retained and reinvested. That will of course drive growth in book value, but that’s a lagging output. Aren’t low cost commodity producers classically great businesses? That’s about as volatile an earnings stream as you can get! And if one ever trades at a low multiple of mid cycle earnings, isn’t that an opportunity for value investors? Look at what Buffett is buying nowadays! Let’s say a new company raises $100M and succeeds wildly. They are doing $1B in annual EPS right away with a long runway and wide moat. Do we still value the stock at ~1.5x the ~$100M BVPS because “that’s where peers are trading” - or something else? I would argue Fairfax recently did something like that with its mid 2010s insurance acquisitions. Would Fairfax’s intrinsic value be higher if they replaced their now massive quantum of float with fixed rate debt? Earnings would be lower but more predicable year to year. Would the company therefore be *worth* more? Fairfax should trade at a higher multiple if it has more insurance float - truly an asset and not a liability - due to the impact on cumulative future cash flows - even though they will certainly be *more* volatile! I understand that Fairfax may *trade* at a lower valuation than a company of similar quality with a lower but smoother stream of cash flows, because Mr Market tends to prefer smooth… but isn't that exact disconnect a classic opportunity for value investors? A stock is also not worth less just because GAAP accounting doesn’t slap us in the face with the underlying value. Float is a textbook example - it is an accounting liability but an economic asset. If we are comparing to BRK, Buffett has told us exactly that repeatedly over the years. And if BRK’s float was ~1.5x its equity book value today, you gotta think Buffett would still be writing a whole lot about valuing float. Float is a truly massive economic asset for Fairfax now. NAV is US$1500-2000 per share, and float is a big chunk of the delta to accounting BV. It may appear like theyre be overearning right now, but if you do the work to adjust accounting BV to economic reality, ~$150 ‘23E EPS makes a lot of sense as a normalized number! I think the crux of the opportunity in FFH right now can be best summarized as exactly that: accounting book value significantly understates intrinsic value and mostly because of the massive float growth of the past few years - both how it has changed the core earnings power and what it says about Fairfax management! A business with a durable competitive advantage that earns elevated returns over long periods of time and has ample room for growth should be considered great whether or not (1) those returns are volatile or (2) it shows up properly in GAAP EPS or BVPS. Accounting often misleads the value investor and we have to do the work to get at economic reality. That is true here in an extreme way. Sorry for the long and rambling post. I am right and you are smart so you will see it my way eventually. Is that the munger quote? Lol.

-

Still can't believe that Fairfax seems to trade primarily on book value. IMHO this more than closet indexing, technicals, volume, skepticism about Prem or anything else is why the stock is still so ridiculously cheap despite Fairfax's transformation into a top 20 insurer and cash flow machine...

-

Maybe this should be a DM, but check out https://www.credible.com/home-insurance - no spam calls, first heard about it from Mr Money Mustache https://www.mrmoneymustache.com/mmm-recommends/credible/ - they handled the shopping around part and quite literally saved me ~15% by switching to GEICO (—> Liberty Mutual). No affiliation but delete if too tangential / off topic...

-

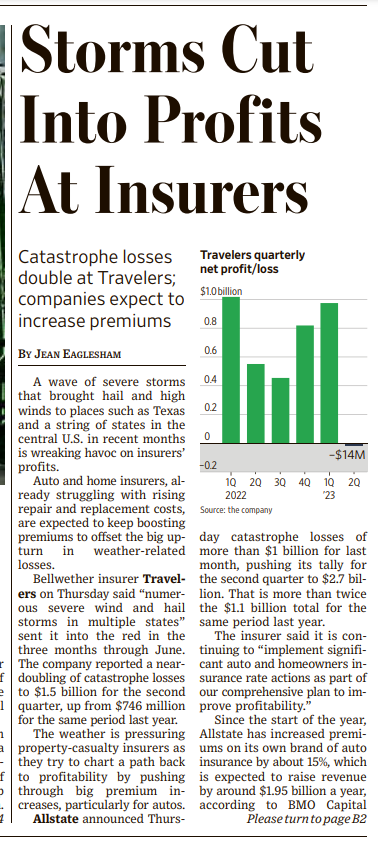

What if the hard market reaccelerates and @Viking's '24/'25 numbers are way too low? https://www.wsj.com/articles/facing-big-storm-losses-insurers-aim-to-boost-rates-f70211d6?st=mu1hv017qtasvf1&reflink=desktopwebshare_permalink

-

Whenever you see a comparison over some specific and arbitrary time horizon rather than something like rolling 3-/5-/10-year periods, you should squint your eyes a little and wonder why they picked that specific period. I think that's a useful thing for every investor to understand and apply across the board.

-

What I’m trying to do is think through this off of normalized earnings looking forward… maybe helpful, maybe not, fair enough. There will of course be extreme volatility around that core structural earnings power and risk of various 100 year floods. But there is also some chance that the outcome is much better